Here’s a stat that might surprise you: 45-50% of B2B payments are now initiated digitally, yet most SaaS companies still struggle to offer their enterprise customers the payment flexibility they actually want. If you’re only accepting credit cards in 2026, you’re likely leaving money on the table.

I’ve spent years analyzing payment infrastructure for SaaS businesses, and one thing is clear — the companies that win big contracts aren’t just offering better software. They’re making it easier for customers to pay them. Enterprise buyers have specific preferences, compliance requirements, and cash flow considerations that dictate how they want to settle invoices.

In this guide, I’ll break down the 10 best B2B payment methods for SaaS companies in 2026. You’ll learn which options work best for different transaction sizes, how fees compare across methods, and which payment rails enterprise customers actually prefer.

What Are B2B Payment Methods?

B2B payment methods are the financial rails businesses use to transfer money between companies. Unlike consumer payments, B2B transactions often involve larger amounts, longer payment terms, and more complex approval workflows. The global B2B payments market is projected to exceed $1.2 trillion by 2028 in the U.S. alone.

For SaaS companies specifically, payment method choice affects everything from cash flow timing to customer acquisition. Enterprise buyers often have procurement policies that restrict which payment types they can use. Understanding these constraints — and accommodating them — can be the difference between winning and losing a six-figure contract.

Why Payment Method Choice Matters for SaaS

Honestly, most SaaS founders underestimate how much payment flexibility influences enterprise deals. When a CFO evaluates a new vendor, payment terms and methods factor into the total cost of ownership calculation. Here’s what the data shows:

- Cross-border B2B payments are growing at 6-8% CAGR, faster than domestic volumes

- Companies using digital B2B payments report up to 80% reduction in payment cycle times

- ACH transfers cost 50-70% less than credit card processing for large transactions

- Real-time payments via FedNow and RTP now support transactions up to $10 million

The bottom line? Your payment infrastructure isn’t just a back-office concern — it’s a competitive advantage.

10 Best B2B Payment Methods for SaaS Companies

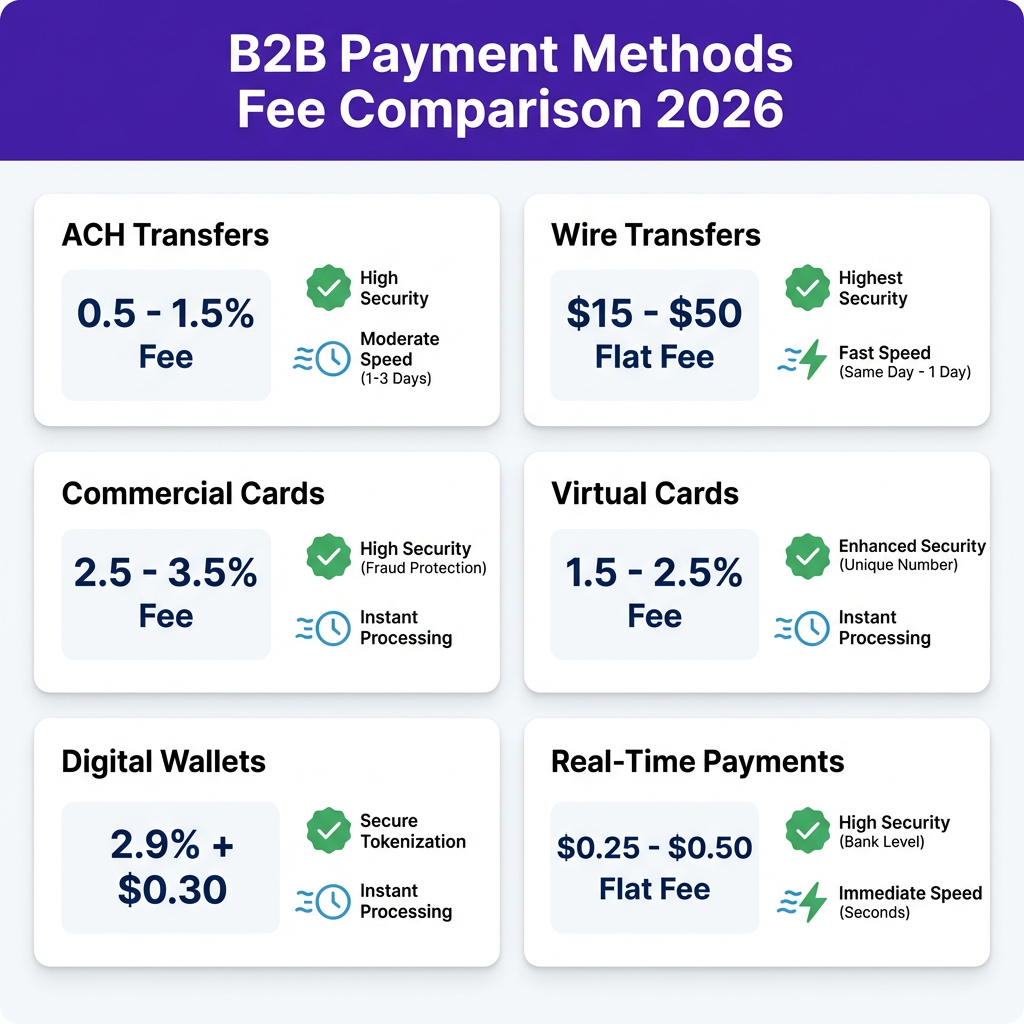

1. ACH Transfers

ACH (Automated Clearing House) transfers have become the workhorse of B2B payments. They’re cost-effective, reliable, and widely accepted by enterprise customers.

Key Features:

- Processing fees: 0.5-1.5% per transaction

- Settlement time: 1-3 business days

- Ideal for: Recurring subscriptions, invoices over $1,000

- Security: Bank-level encryption, NACHA compliance

Pricing: Most ACH processors charge a flat fee of $0.25-0.50 per transaction plus a small percentage. For a $5,000 invoice, you’re looking at roughly $25-75 in fees — significantly less than credit cards.

Best for: SaaS companies with subscription revenue and enterprise customers who prefer direct bank transfers.

2. Wire Transfers

Wire transfers remain the gold standard for high-value B2B transactions. While they’re one of the least common methods by volume, they account for a significant portion of B2B payment value due to their use in large international deals.

Key Features:

- Processing fees: $15-50 per transaction (flat)

- Settlement time: Same day (domestic), 1-2 days (international)

- Ideal for: Enterprise contracts, international deals, transactions over $10,000

- Security: Fedwire, CHIPS, or RTP networks

Pricing: Domestic wires typically cost $15-30. International wires run $35-50 plus potential intermediary bank fees.

Best for: Annual contracts, enterprise deals, and situations where immediate settlement is critical.

3. Commercial Credit Cards

Commercial credit cards remain highly popular with buyers despite the processing fees. For SaaS vendors, accepting cards is often non-negotiable — the potential lost business from not accepting cards far outweighs the fees.

Key Features:

- Processing fees: 2.5-3.5% per transaction

- Settlement time: 1-2 business days

- Ideal for: SMB customers, self-serve signups, transactions under $5,000

- Security: PCI DSS compliance, chargeback protection

Pricing: Standard processing runs 2.9% + $0.30 per transaction. Enterprise merchants can negotiate rates down to 2.2-2.5% with sufficient volume.

Best for: Self-serve SaaS products, smaller contracts, and customers who prioritize convenience over cost.

4. Virtual Credit Cards

Virtual cards have exploded in popularity for B2B payments. These digitally-generated 16-digit numbers offer enhanced security and spend controls that finance teams love.

Key Features:

- Processing fees: 1.5-2.5% per transaction

- Settlement time: Same as credit cards (1-2 days)

- Ideal for: Controlled spending, one-time vendor payments

- Security: Single-use numbers, tokenization, spend limits

Pricing: Virtual cards often qualify for lower interchange rates due to enhanced data (Level II/III). A Mastercard study estimates virtual cards can deliver $0.50 to $14 in cost savings per transaction for banks.

Best for: Expense management, controlled vendor payments, and situations requiring enhanced security.

5. Real-Time Payments (FedNow & RTP)

Real-time payments are crossing from “nice-to-have” to “business necessity” in 2026. With FedNow now operating alongside The Clearing House’s RTP network, instant 24/7/365 settlement is finally mainstream in the United States.

Key Features:

- Processing fees: $0.25-0.50 per transaction

- Settlement time: Instant (seconds)

- Ideal for: Urgent payments, cash flow optimization

- Security: Bank-grade, irrevocable settlement

Pricing: Real-time payments are significantly cheaper than wires for instant settlement. FedNow’s transaction limit increased to $1 million in July 2025, while RTP supports up to $10 million.

Best for: Time-sensitive payments, treasury optimization, and businesses wanting to differentiate with instant settlement.

6. Digital Wallets (Apple Pay, Google Pay)

Digital wallets aren’t just for consumers anymore. B2B buyers increasingly expect the same payment convenience they get as individuals. The U.S. proximity mobile payment transaction value is expected to reach $1.2 trillion by 2028.

Key Features:

- Processing fees: 2.9% + $0.30 per transaction

- Settlement time: 1-2 business days

- Ideal for: Self-serve checkout, mobile-first buyers

- Security: Tokenization, biometric authentication

Pricing: Similar to credit card processing. The convenience factor often justifies the cost for smaller transactions.

Best for: SMB self-serve plans, mobile-optimized checkout flows, and reducing friction in the buying process.

7. Account-to-Account (A2A) Payments

Open banking is driving a major shift toward A2A payments — direct bank-to-bank transfers without card networks or intermediaries. This is one of the fastest-growing B2B payment trends.

Key Features:

- Processing fees: $0.40-0.50 per API call (flat)

- Settlement time: Instant to 1 day

- Ideal for: High-value transactions, recurring billing

- Security: Bank-grade, Strong Customer Authentication

Pricing: A2A transactions typically cost a fixed fee rather than a percentage. For a $50,000 supplier payment, the difference between a 2.5% card fee ($1,250) and a $0.50 A2A fee is transformative.

Best for: High-value B2B transactions, cost-conscious enterprises, and businesses seeking alternatives to card networks.

8. Blockchain-Based Payments

Blockchain has moved from experimental to mainstream for cross-border B2B payments. In 2026, 71% of global financial institutions are either testing or deploying blockchain solutions for international transactions.

Key Features:

- Processing fees: 0.5-1% (significantly lower for cross-border)

- Settlement time: Minutes to hours

- Ideal for: Cross-border transactions, multi-currency operations

- Security: Distributed ledger, immutable records

Pricing: Blockchain reduces cross-border transaction fees by up to 70% compared to traditional wire transfers. The global market value of cross-border blockchain transactions is projected to surpass $4.5 trillion by end of 2025.

Best for: International SaaS companies, businesses with global supplier networks, and early adopters seeking cost advantages.

9. Payment Links

Payment links offer a flexible, low-friction way to collect B2B payments without complex integrations. They’re particularly useful for invoice collection and one-off transactions.

Key Features:

- Processing fees: Varies by underlying method (typically 2.9% + $0.30)

- Settlement time: Depends on chosen payment method

- Ideal for: Invoice payments, one-time charges, email collections

- Security: SSL encryption, tokenization

Pricing: Most providers don’t charge extra for payment links — you pay the standard processing fees for whatever method the customer chooses.

Best for: Invoice collection, non-technical sales workflows, and businesses wanting to offer payment choice without complex development.

10. Embedded Finance & Payment Orchestration

Embedded B2B payments represent the future of SaaS monetization. By integrating payments directly into your platform, you can turn a cost center into a revenue stream.

Key Features:

- Processing fees: Varies (platforms often earn revenue share)

- Settlement time: Depends on underlying rails

- Ideal for: Vertical SaaS, platform businesses, marketplaces

- Security: PCI DSS, SOC 2 compliance

Pricing: Embedded B2B payments are projected to handle $16 trillion in transactions by 2030. Mid-market B2B platforms can command 2-5% commissions on embedded payment volumes.

Best for: SaaS platforms with payment-adjacent workflows, vertical SaaS companies, and businesses seeking new revenue streams.

B2B Payment Methods Comparison Table

| Payment Method | Fee Range | Settlement | Best For |

|---|---|---|---|

| ACH Transfers | 0.5-1.5% | 1-3 days | Recurring subscriptions |

| Wire Transfers | $15-50 flat | Same day | Enterprise deals |

| Commercial Cards | 2.5-3.5% | 1-2 days | SMB customers |

| Virtual Cards | 1.5-2.5% | 1-2 days | Controlled spending |

| Real-Time Payments | $0.25-0.50 | Instant | Urgent settlements |

| Digital Wallets | 2.9% + $0.30 | 1-2 days | Self-serve checkout |

| A2A Payments | $0.40-0.50 | Instant-1 day | High-value transactions |

| Blockchain | 0.5-1% | Minutes-hours | Cross-border |

| Payment Links | Varies | Varies | Invoice collection |

| Embedded Finance | Revenue share | Varies | Platform businesses |

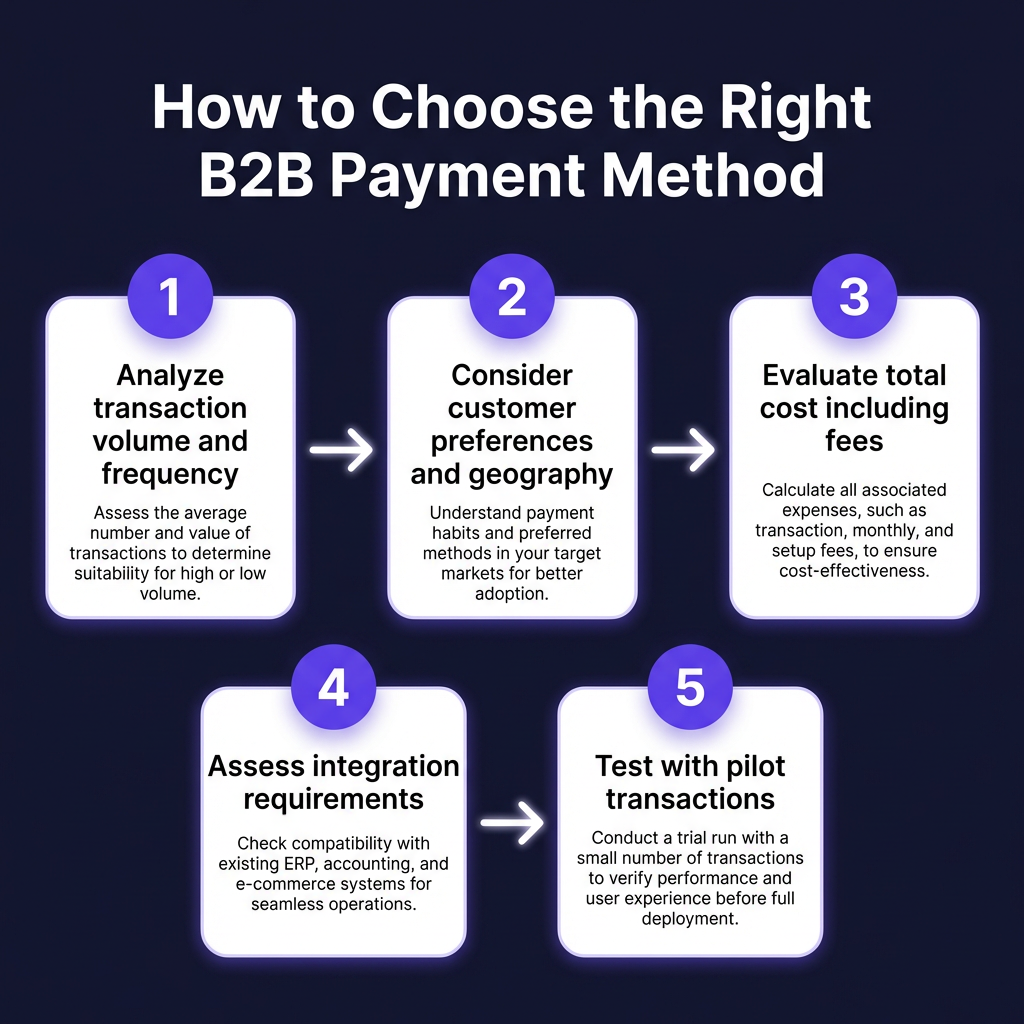

How to Choose the Right B2B Payment Method

Selecting the optimal payment mix isn’t about picking one winner — it’s about offering the right options for different customer segments and transaction types. Here’s my framework:

1. Analyze Your Transaction Profile

Start by looking at your current payment data. What’s your average transaction size? How many payments do you process monthly? What’s your customer concentration? High-volume, lower-value transactions favor different methods than low-volume, high-value deals.

2. Consider Customer Preferences

Enterprise customers often have procurement policies that dictate payment methods. Some can’t use credit cards for large purchases. Others require ACH for recurring payments. Survey your top customers — their preferences should heavily influence your payment strategy.

3. Evaluate Total Cost of Acceptance

Don’t just look at processing fees. Factor in:

- Integration costs

- Reconciliation time

- Failed payment rates

- Chargeback and fraud risk

- Cash flow impact from settlement timing

4. Plan for International Expansion

If you’re selling globally, your payment strategy needs to accommodate local preferences. European buyers often prefer SEPA transfers. Asian markets may favor local payment methods. Choose a payment infrastructure that can scale internationally.

The Future of B2B Payments: 2026 and Beyond

The B2B payment landscape is evolving rapidly. Here are the trends shaping the next 12-24 months:

AI-Powered Payment Intelligence: By end of 2026, approximately one-third of B2B payment workflows will use autonomous AI agents. These systems don’t just process transactions — they optimize routing, predict cash flow, and detect fraud in real-time.

Embedded Finance Explosion: Embedded B2B payments are expected to reach $2.6 trillion in 2026, growing at 25% annually. SaaS platforms that integrate payments directly into their workflows will capture significant value.

Real-Time as Default: Within 12-24 months, real-time settlement will be table stakes, not exceptional. FedNow and RTP adoption is accelerating, with 96% of manufacturers expecting real-time payments to replace traditional checks.

FAQ: B2B Payment Methods for SaaS

What’s the cheapest B2B payment method?

For high-value transactions, A2A payments and ACH transfers are typically cheapest. A2A costs around $0.40-0.50 per transaction regardless of amount, while ACH runs 0.5-1.5%. For a $10,000 payment, ACH fees would be $50-150 versus $250-350 for credit cards.

Should SaaS companies accept wire transfers?

Absolutely, especially for enterprise deals. While wires cost $15-50 per transaction, they’re preferred for large purchases and international deals. The fees are negligible on a $50,000 annual contract, and offering wires can be a competitive advantage in enterprise sales.

How do real-time payments compare to ACH?

Real-time payments (FedNow/RTP) settle instantly versus 1-3 days for ACH. They cost slightly more ($0.25-0.50 vs $0.25-0.50 for ACH) but offer 24/7/365 availability and immediate cash flow. For time-sensitive payments, the speed advantage often justifies the cost.

What’s the best payment method for international SaaS sales?

For cross-border transactions, blockchain-based payments offer the best cost-to-speed ratio — up to 70% cheaper than wires with settlement in minutes to hours. For established markets, local payment methods (SEPA in Europe, Faster Payments in UK) provide the best customer experience.

Can I pass payment processing fees to customers?

Surcharging (passing credit card fees to customers) is legal in most U.S. states but regulated. For B2B SaaS, it’s often better to build fees into pricing rather than surcharging — enterprise buyers expect transparent pricing without surprise fees at checkout.

Conclusion: Building Your B2B Payment Strategy

The SaaS companies winning in 2026 aren’t just building better software — they’re removing friction from every part of the buying process, including payments. Offering the right mix of B2B payment methods can shorten sales cycles, improve cash flow, and differentiate you from competitors.

My recommendation? Start with a foundation of credit cards and ACH for broad compatibility. Add wire transfers for enterprise deals. Experiment with real-time payments and virtual cards for competitive advantage. And keep an eye on A2A and blockchain as they mature.

If you’re looking for a payment solution that handles the complexity for you, Fungies offers an all-in-one merchant of record platform with support for multiple B2B payment methods, automatic tax compliance, and global coverage. Get started free and see how streamlined payments can accelerate your SaaS growth.