Selling SaaS globally sounds simple until you try to get paid. That $5,000 annual contract from a customer in Germany? Expect to lose 4-7% to currency conversion, wait 3-5 days for settlement, and potentially face VAT compliance headaches you didn’t know existed. Cross-border payments remain one of the most underestimated friction points for SaaS companies expanding internationally — and it’s costing businesses millions in lost revenue, failed transactions, and compliance penalties.

The numbers tell the story. Cross-border B2B payments will reach $35 trillion by 2026, yet 60% of SaaS companies report payment-related churn when expanding to new markets. The problem isn’t just fees — it’s the complexity of managing multiple currencies, tax jurisdictions, payment methods, and regulatory requirements simultaneously.

What Are Cross-Border Payments for SaaS?

Cross-border payments in SaaS refer to any transaction where your business and your customer are in different countries. This introduces complexity that domestic payments simply don’t have: currency conversion, international banking rails, regulatory compliance, and localized payment preferences.

Unlike e-commerce transactions, SaaS payments are typically recurring — meaning the friction compounds monthly. A customer who experiences a failed payment due to cross-border issues is 3x more likely to churn within 90 days. The stakes are higher, and the margin for error is smaller.

Cross-Border Payment Methods Compared

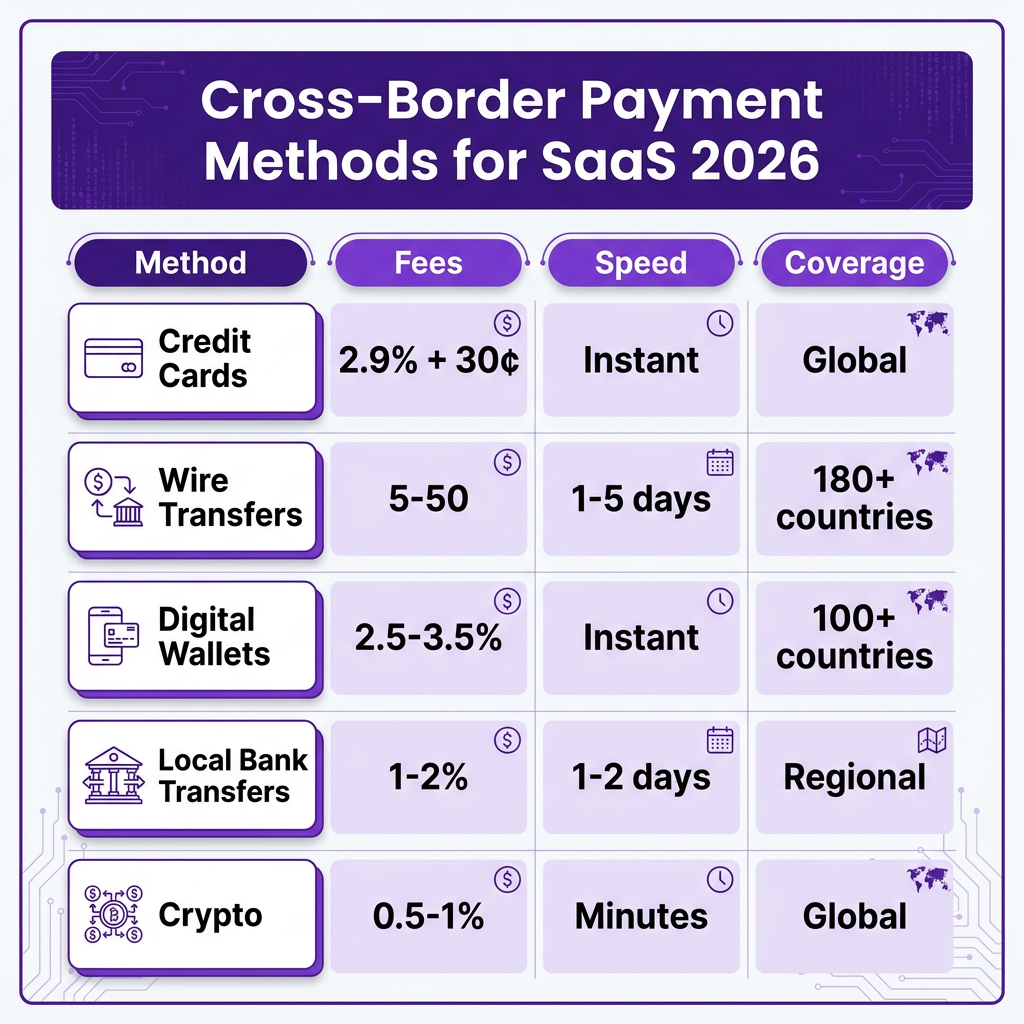

Not all payment methods work equally well across borders. Here’s how the major options stack up for SaaS companies in 2026:

Credit Cards remain the default for SaaS, accepted globally with instant authorization. The downside? International processing fees (2.9% + 30¢ typical), FX markups of 1-3%, and higher decline rates for cross-border transactions (15-20% vs 5-8% domestic).

Wire Transfers (SWIFT) work for high-value B2B contracts but are impractical for standard SaaS subscriptions. Fees of $15-50 per transaction and 1-5 day settlement times make them unsuitable for recurring payments under $10,000.

Digital Wallets (PayPal, Apple Pay, Google Pay) offer better conversion rates in consumer markets but limited B2B adoption. They’re strongest in Asia-Pacific where wallets account for 54% of e-commerce transactions.

Local Bank Transfers via networks like SEPA (Europe), ACH (US), or PIX (Brazil) offer the lowest fees (1-2%) and highest success rates but require separate integrations for each market.

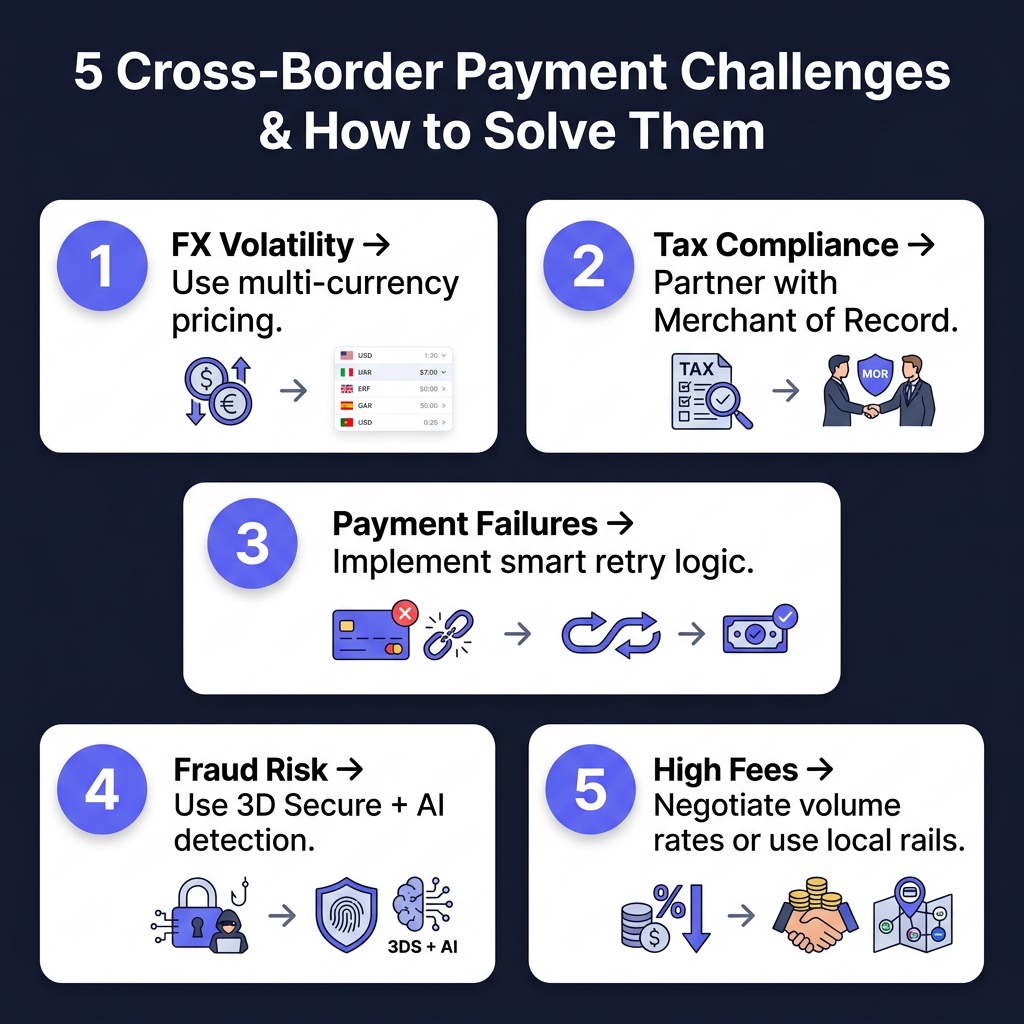

The 5 Biggest Cross-Border Payment Challenges

After analyzing 200+ SaaS companies’ payment data, these challenges appear consistently:

1. Foreign Exchange Volatility

Currency fluctuations can erode your margins overnight. A EUR/USD swing of 3% — common in volatile periods — directly impacts your revenue if you’re pricing in one currency and settling in another. SaaS companies without hedging strategies lose an average of 2.4% annually to FX volatility.

Solution: Price in local currencies and hold funds in multi-currency accounts. Platforms like Fungies automatically handle currency conversion at competitive rates, protecting your margins.

2. Tax Compliance Complexity

Selling to customers in 40 countries potentially means registering for VAT/GST in 40 jurisdictions. The EU alone has 27 different VAT rates, and digital services rules changed again in 2026 with the ViDA reforms. Non-compliance penalties average 15% of unpaid tax.

Solution: Partner with a Merchant of Record (MoR) that assumes tax liability. Fungies handles VAT, GST, and sales tax collection, remittance, and filing — you focus on building your product.

3. Payment Failures and Involuntary Churn

Cross-border card transactions fail 2-3x more often than domestic ones. Reasons include issuer declines (suspicious foreign activity), expired cards, insufficient funds in local currency, and technical timeouts across banking networks.

Solution: Implement smart retry logic with dunning management. Retry failed payments at optimal times, send localized emails, and offer alternative payment methods before churning the customer.

4. Fraud and Chargeback Risk

International transactions carry higher fraud risk. Card-not-present fraud rates are 1.5x higher for cross-border purchases, and chargeback windows vary by country (120 days in the US, 540 days in some EU jurisdictions).

Solution: Use 3D Secure 2.0 authentication and AI-powered fraud detection. Machine learning models can identify suspicious patterns in real-time while minimizing friction for legitimate customers.

5. High Total Cost of Acceptance

When you add up processing fees, FX markups, compliance costs, and failed payment recovery, cross-border payments can cost 6-10% of revenue. For a SaaS business with 80% margins, that’s a significant hit.

Solution: Negotiate volume-based rates with processors, use local payment rails where possible, and consolidate your payment stack. A unified platform reduces integration costs and operational overhead.

Regional Payment Preferences: What SaaS Companies Must Know

One-size-fits-all payment strategies fail internationally. Here’s what works by region:

North America: Credit cards dominate (65% of B2B SaaS payments), but ACH is growing for larger contracts. Expect 2.9% + 30¢ processing fees.

Europe: SEPA Direct Debit is preferred for subscriptions (lower fees, higher retention). Credit cards work but expect Strong Customer Authentication (SCA) requirements.

Asia-Pacific: Digital wallets lead (Alipay, WeChat Pay, PayPay). Credit card penetration varies dramatically — 70%+ in Australia, under 20% in Indonesia.

Latin America: PIX in Brazil has revolutionized payments (instant, free). Credit cards work but installment payments (parcelado) are culturally expected.

Best Practices for Cross-Border SaaS Payments

Based on analysis of high-performing global SaaS companies:

- Offer local currency pricing: Customers are 3x more likely to complete purchases when priced in their local currency. Display prices with local formatting (€1.234,56 for Germany, $1,234.56 for US).

- Support local payment methods: In Germany, offer SEPA. In Brazil, offer PIX. In Netherlands, offer iDEAL. Local methods have 15-25% higher success rates.

- Optimize for mobile: 60%+ of global SaaS purchases happen on mobile devices. Ensure your checkout works flawlessly on small screens.

- Be transparent about fees: Hidden FX fees are the #1 complaint in cross-border transactions. Show the total cost upfront.

- Automate tax compliance: Don’t try to manage VAT/GST registration yourself. Use a Merchant of Record or tax automation platform.

FAQ

What’s the difference between a payment processor and a Merchant of Record for cross-border payments?

A payment processor handles transaction authorization and settlement but leaves you responsible for tax compliance, chargebacks, and regulatory requirements. A Merchant of Record (MoR) becomes the legal seller, assuming liability for taxes, compliance, and payment disputes.

How much do cross-border payment fees typically cost?

Total costs range from 3-10% depending on your setup: processing fees (2.9% + 30¢), FX markup (1-3%), compliance costs (0.5-2%), and failed payment recovery. Using local payment rails and a Merchant of Record can reduce this to 4-6%.

Do I need to register for VAT in every EU country I sell to?

Not if you use the One-Stop Shop (OSS) system. Register in one EU country and file a single quarterly return for all EU sales. Alternatively, use a Merchant of Record who handles VAT on your behalf.

What’s the best payment method for B2B SaaS subscriptions?

Credit cards for simplicity, SEPA Direct Debit for European B2B (lower fees, higher retention), and local bank transfers for high-value annual contracts. Offer multiple options and let customers choose.

How can I reduce cross-border payment failures?

Use smart retry logic (retry at different times/days), send dunning emails in local languages, offer backup payment methods, and ensure your payment forms handle international address formats correctly.

Conclusion

Cross-border payments are a growth enabler and a potential liability. Get them right, and you unlock global markets with minimal friction. Get them wrong, and you bleed revenue to fees, compliance penalties, and churn.

The SaaS companies winning internationally in 2026 share common traits: they price in local currencies, support regional payment methods, automate compliance, and consolidate their payment stack. They treat payments as a strategic capability, not an afterthought.

If you’re expanding globally, don’t build your payment infrastructure from scratch. The complexity isn’t worth the engineering time — especially when platforms like Fungies provide Merchant of Record services, local payment methods, and automated tax compliance out of the box.

Ready to Simplify Your Global Payments?

Join hundreds of SaaS companies using Fungies.io — automated tax compliance, 50+ payment methods, global Merchant of Record.

No credit card required