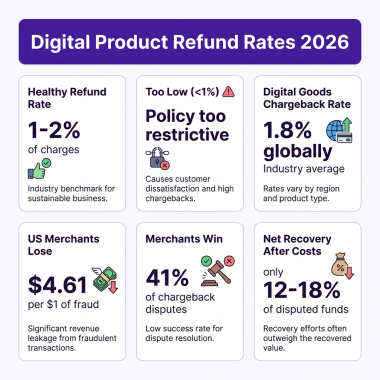

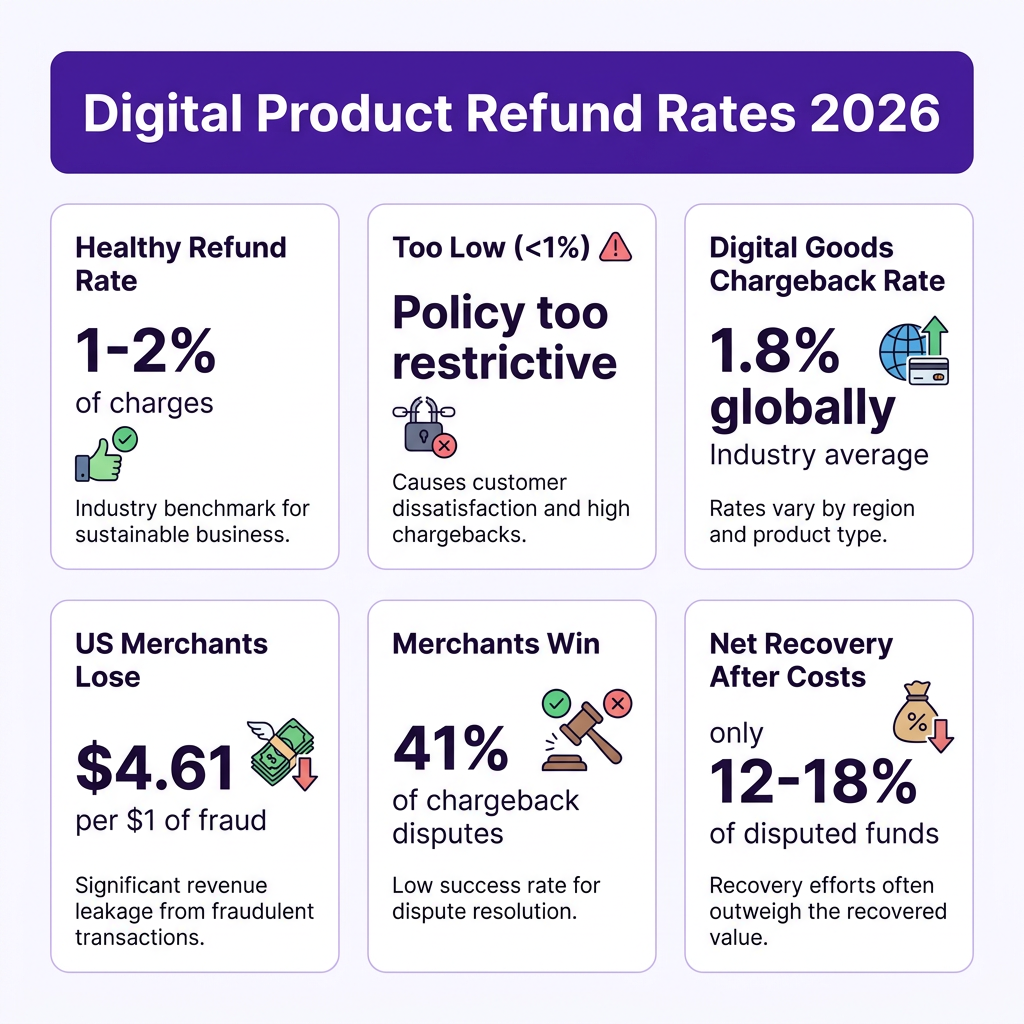

Digital goods chargebacks cost US merchants an average of $4.61 for every $1 lost — and nearly 79% of those disputes are friendly fraud: legitimate customers who skip the refund process and go straight to their bank. If you’re selling digital products or SaaS subscriptions and you haven’t thought carefully about your refund policy, you’re probably losing money in two directions at once: through bad refund decisions and through chargebacks you could have prevented.

This guide covers how to handle digital product refunds in 2026 — specifically how to build a policy that reduces chargebacks, builds buyer trust, and doesn’t kill your conversions in the process.

Why Digital Product Refunds Are Different

Physical products have a simple refund loop: customer sends it back, you inspect it, you refund. Digital products don’t work that way. Once a customer downloads your ebook, activates your software license, or accesses your course, the “product” has already been consumed. There’s no box to return.

This creates a genuine tension: you can’t reverse delivery, but being too restrictive with refunds pushes customers toward chargebacks — which are far more expensive and damaging than just issuing the refund.

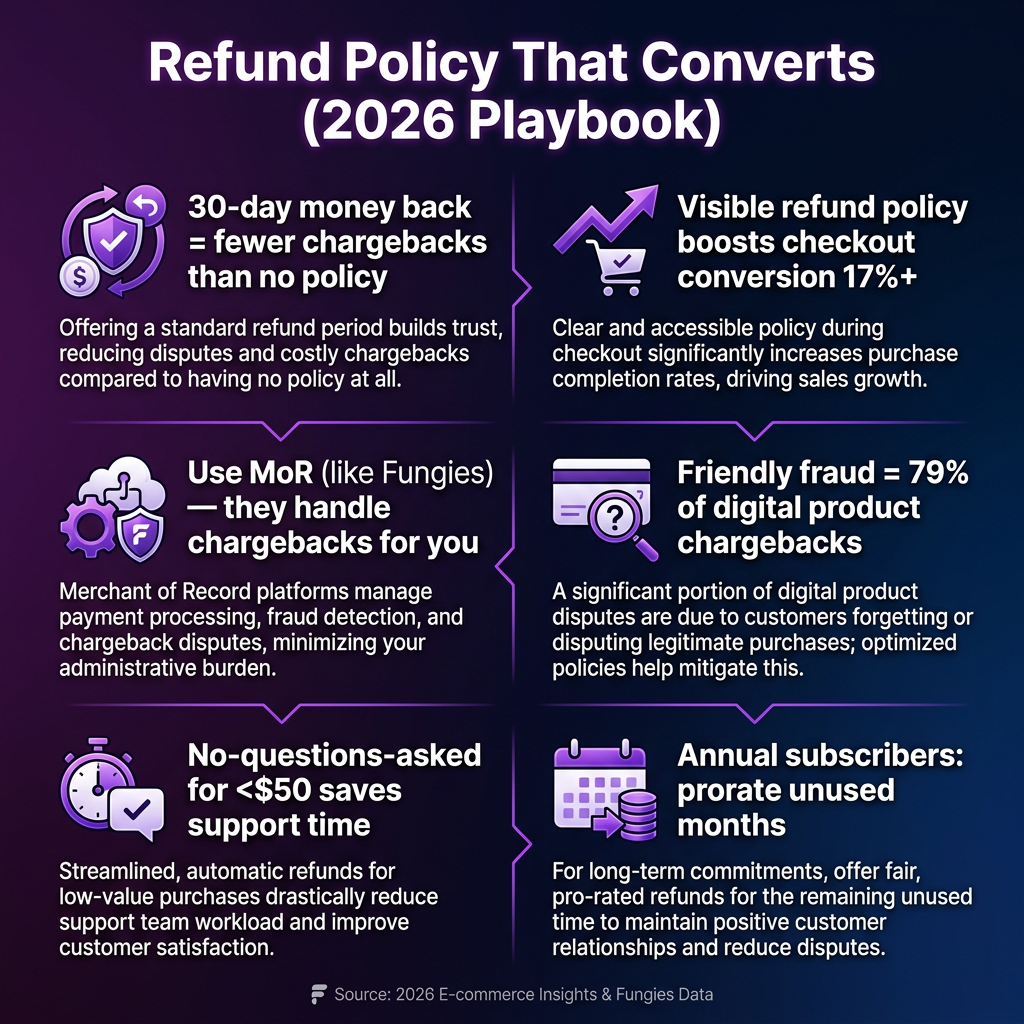

The data backs this up. Digital goods merchants see chargeback rates of 1.8% globally, versus 0.5% for physical goods. That’s not because digital buyers are more fraudulent — it’s because many sellers make refunding hard, so dissatisfied buyers use their bank as the path of least resistance.

What a Healthy Refund Rate Actually Looks Like

According to Dodo Payments, a healthy SaaS refund rate is 1–2% of total charges. If you’re below 1%, your policy is probably too restrictive — which sounds great until you realize those unhappy customers are filing chargebacks instead of refund requests. If you’re above 3%, something is broken: either your product doesn’t deliver what you promised, or your checkout flow is confusing people into accidental purchases.

The goal isn’t to minimize refunds at all costs. It’s to have a clear, fair policy that converts refund requests into resolutions — not disputes.

The Business Case for a Generous Refund Policy

Here’s the counterintuitive truth: offering a clear, visible money-back guarantee increases revenue for most digital product sellers. Buyers evaluating your checkout page see your refund policy as a trust signal. A visible guarantee reduces purchase anxiety, and that directly impacts whether they click “Buy.”

The math is simple. If a more generous refund policy increases your conversion rate by even 2–3%, and your actual refund rate stays at 1.5%, you come out ahead. The customers who refund would have been unhappy anyway — the ones who convert because of the guarantee are net new revenue.

There’s also a chargeback angle. When customers know they can get a refund by asking, they ask instead of disputing. Merchants win roughly 41% of chargeback representment cases, but after fees and second chargebacks, the net recovery rate drops to just 12–18%. A $50 refund you processed yourself beats a $50 chargeback that costs you $73 after fees every time.

| Scenario | Cost to You | Customer Outcome | Effect on Future Sales |

|---|---|---|---|

| Proactive refund (you issue it) | ~$50 product revenue | Resolved, no dispute | Neutral to positive |

| Chargeback (customer files with bank) | $50 + $15–30 chargeback fee + time | Dispute process, 60–120 days | Damages merchant score |

| No refund, no chargeback (rare) | $0 | Customer leaves angry | Negative reviews, lost trust |

What to Include in Your Digital Product Refund Policy

A good refund policy for digital products covers six things. Skip any of them and you’ll get edge cases that cost you more time than just writing the policy right the first time.

1. The Time Window

30 days is the industry standard and the sweet spot. Shorter than 14 days creates anxiety. Longer than 60 days invites abuse. For annual SaaS subscriptions, offering a 30-day window at the start of the subscription (not 30 days from any renewal) is common and defensible.

2. Access vs. Non-Access

Be explicit: if the customer has downloaded the file or accessed premium content, are they still eligible? Most digital sellers say “yes” for reasonable requests within the window and “no” after substantial use. Define “substantial use” in your policy — don’t leave it ambiguous.

3. Subscription Handling

Monthly subscriptions: typically no refund for the current period, cancellation takes effect at end of billing cycle. Annual subscriptions: prorating the unused months is fair and dramatically reduces chargebacks on high-ticket plans. Many SaaS founders resist this, but the math favors prorating — an annual customer who gets a partial refund is less likely to dispute the full charge.

4. What Disqualifies a Refund

State it clearly. Common exclusions: products that have been fully consumed (a one-time event pass, a license key that’s been activated on multiple devices), requests that come in after the window, and obvious abuse patterns (multiple refund requests from the same customer/email/card).

5. Process and Timeline

Tell customers how to request a refund and how long it takes. “Email [email protected] with your order number. We process all requests within 2 business days.” Simple. This alone reduces chargebacks because it sets expectations.

6. Access Revocation

For digital downloads and SaaS, state that access will be revoked upon refund. This is both legally clean and practically necessary — you can’t let someone keep using a SaaS tool they’ve been refunded for.

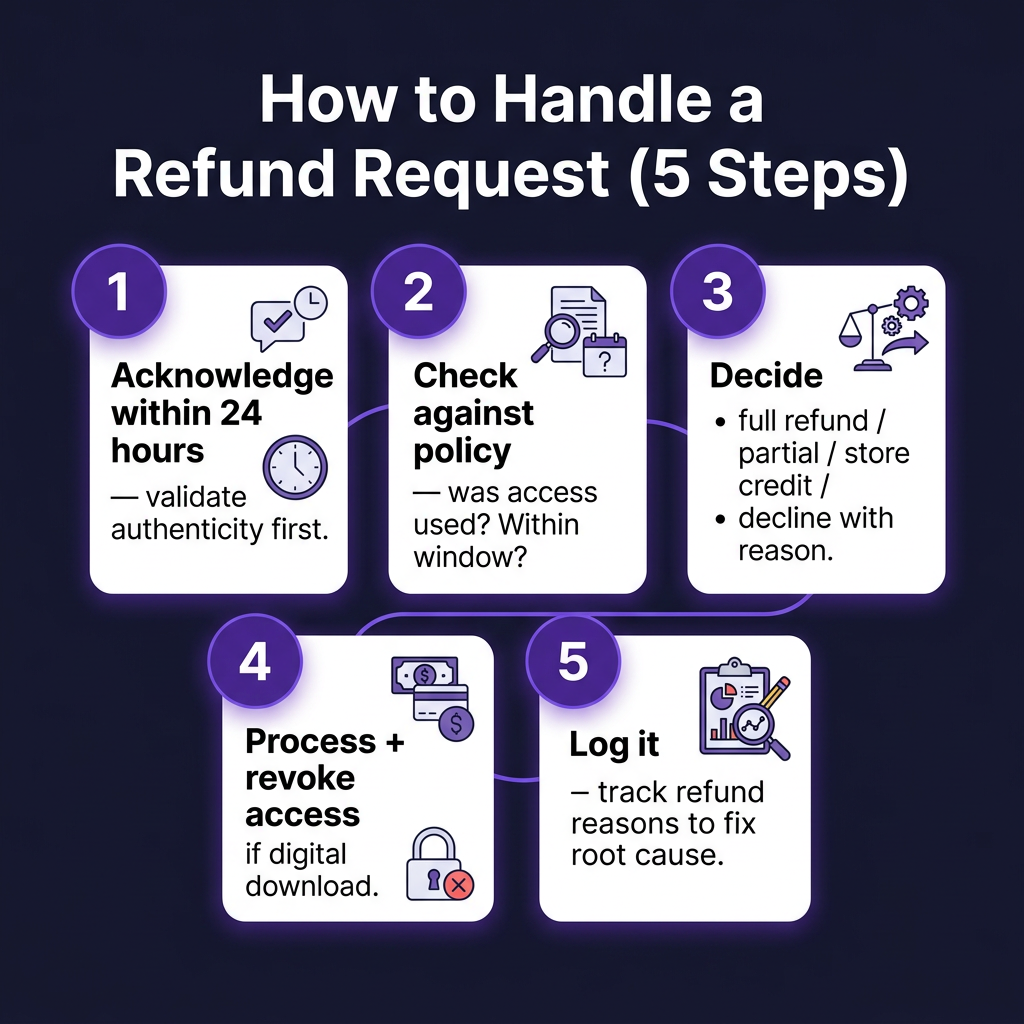

How to Handle Refund Requests (5-Step Process)

The process matters as much as the policy. A great policy handled badly still creates friction and frustration.

Step 1: Acknowledge Within 24 Hours

Auto-responders work fine here. The customer needs to know their request was received. Silence for 48+ hours after a refund request is one of the top triggers for chargebacks — the customer assumes you’re ignoring them and escalates to their bank.

Step 2: Validate Authenticity

Before processing, confirm the requester is actually the account holder. Match the email to your customer record, check the order ID, verify the purchase date. This catches a small but real number of fraudulent refund requests (someone requesting a refund on a product they didn’t buy).

Step 3: Apply Your Policy — Then Use Judgment

Policy is the starting point, not the final word. A customer who’s 32 days past a 30-day window but clearly had a technical issue deserves a different response than someone who downloaded the file 29 days ago and “just changed their mind.” Your support team needs authority to use judgment within defined limits — say, up to $100 without escalation.

Step 4: Process the Refund and Revoke Access

Do both at the same time. Revoking access before processing the refund is bad practice and creates disputes. Processing the refund without revoking access is operationally messy (especially for SaaS). If you’re using a Merchant of Record like Fungies, Paddle, or Creem, refunds and access management can be linked through your billing system.

Step 5: Log the Reason and Track Trends

This is the step most founders skip. Every refund request has a reason. If 30% of your refunds cite “product didn’t work as expected” — that’s a product or documentation problem. If 40% cite “I accidentally signed up for annual when I wanted monthly” — that’s a checkout UX problem. Refund data is free product feedback.

| Product Type | Recommended Window | Access Policy on Refund | Chargeback Risk Without Policy |

|---|---|---|---|

| SaaS (monthly) | No refund, cancel at period end | Access until period end | Medium — customers dispute on principle |

| SaaS (annual) | 30 days full + prorate remaining | Access revoked at refund | High — large charge, long to forget |

| Digital download (ebook, template) | 30 days, file not redistributed | Revoke download links | Low — small amounts, less disputed |

| Online course | 7–14 days / before lesson 3 | Revoke course access | Medium-high — common “didn’t like it” disputes |

| Software license key | 14 days / before first activation | Deactivate license | High — easy to “return” while keeping |

| Game / in-game assets | Platform-dependent (usually 0–7 days) | Remove assets from account | Very high — frequent friendly fraud |

The Friendly Fraud Problem and How to Defend Against It

Nearly 79% of digital product chargebacks are friendly fraud — valid purchases where the cardholder disputes the charge directly with their bank rather than requesting a refund. This is the specific problem your refund policy is designed to prevent.

Friendly fraud happens for a few reasons:

- The refund process was unclear or hard to find — so the customer defaulted to their bank

- The refund was declined unfairly — so the customer escalated

- The customer is genuinely bad-faith — wants to keep the product and the money

You can eliminate the first two causes with a good policy and process. For the third, your defenses are: clear transaction descriptors (so customers recognize the charge), delivery confirmation emails (proof they accessed the product), and Verifi/Ethoca alerts through your payment platform (which can intercept disputes before they become formal chargebacks). Combined, these tools can cut chargeback volume by up to 80%.

This is one concrete advantage of using a Merchant of Record. Platforms like Fungies, Paddle, and Creem handle chargeback disputes on your behalf — they’re the merchant of record on the customer’s card statement, so the dispute lands with them, not with you. They have the infrastructure and legal standing to fight chargebacks efficiently, and your chargeback rate doesn’t directly threaten your own merchant account.

How Merchant of Record Platforms Change the Refund Equation

If you’re using Stripe directly, you’re the merchant of record. That means chargebacks land on your merchant account, you fight them yourself, and high chargeback rates can get your account suspended. For founders selling to a global customer base, this is a real operational risk.

When you use an MoR — Fungies, Paddle, Creem, or similar — the MoR is the legal seller on the customer’s receipt. Chargebacks go to the MoR, not you. The MoR has dedicated teams to dispute friendly fraud, bulk relationships with card networks, and fraud screening baked into their checkout flows.

This doesn’t mean you outsource all refund decisions. You still define your policy and handle initial support. But the chargeback liability shifts — which is the expensive part. For most indie SaaS founders and digital product sellers, that alone justifies the 5% MoR fee over handling payments yourself.

Refund Policy Placement: Where to Put It

Your policy doesn’t help if no one can find it. Placement matters both for conversion and for chargeback defense (you need to prove the customer had access to the policy).

- Checkout page — a one-line summary with a link (“30-day money-back guarantee. See full policy.”) near the payment button

- Order confirmation email — include the refund process and a direct link to the policy

- Onboarding email sequence — remind new customers of the window, especially in day 1–3 emails

- Help center / FAQ — a dedicated refund policy page that support can link to

- Footer — standard placement that chargeback arbitrators will look for as evidence of disclosure

Key Takeaways

- A healthy digital product refund rate is 1–2%. Below 1% means customers are chargebacks instead of requesting refunds — which costs more.

- 30 days is the standard refund window for most digital products; use 7–14 days for content-heavy courses with a clear consumption threshold.

- Annual SaaS subscribers should get prorated refunds for unused months — it’s fair, it’s defensible, and it prevents $300+ chargebacks.

- Log every refund reason — if more than 10% share a single reason, that’s a product or UX problem, not a refund problem.

- Using a Merchant of Record shifts chargeback liability away from your merchant account — for global sellers, this is often worth the fee difference alone.

FAQ

Are digital product sellers legally required to offer refunds?

In most jurisdictions, no — SaaS and digital products aren’t subject to the same return laws as physical goods. However, EU consumer law is an exception: EU customers have a 14-day “cooling off” right for digital purchases, waivable only if the customer explicitly acknowledges they’re receiving immediate access. If you sell to EU customers, your policy must address this. Using an MoR that handles EU compliance (like Fungies or Paddle) is the simplest way to stay compliant without becoming an EU VAT expert yourself.

What’s the difference between a refund and a chargeback?

A refund is initiated by you (the seller) through your payment system. A chargeback is initiated by the customer through their bank or card network. Refunds cost you the product revenue. Chargebacks cost you the product revenue plus a dispute fee ($15–30 per case), plus time, plus risk to your merchant account if your rate exceeds 1% of transactions. Always prefer refunds over chargebacks — make it easier to request a refund than to file a dispute.

Should I offer a no-questions-asked policy?

For products under $50, yes — the support time cost of investigating a refund request often exceeds $50 in labor. For higher-ticket items or subscriptions, “no questions asked” is a conversion tool but may invite abuse. A middle path: “no-questions-asked within 14 days, reviewed requests between 14–30 days.” This converts well while giving you a layer of protection against serial refunders.

How do I handle refund requests after the policy window?

Use judgment, not policy. A customer who’s 35 days in but had a billing issue they couldn’t reach you about deserves different treatment than someone who used the product for 29 days and is now requesting a refund because they found a cheaper alternative. Document your reasoning and make a decision. Refusing reasonable late requests pushes customers to chargebacks — and you’ll lose that dispute anyway if the customer has a legitimate grievance.

Conclusion

Your refund policy isn’t just legal fine print. It’s a conversion tool, a chargeback prevention mechanism, and a signal to potential customers about how much you trust your own product. The founders who think carefully about refunds — instead of defaulting to “no refunds on digital products” — end up with lower chargeback rates, higher conversion rates, and customers who actually come back.

If you want the chargeback liability off your plate entirely while you figure out the rest, Fungies handles it for you as your Merchant of Record. You define the policy, we handle the disputes. Sign up in minutes — no enterprise sales call required.

References

- Dodo Payments — SaaS Refund Management: Policies, Automation, and Best Practices

- JustPricing — 47 Chargeback Statistics for 2026

- Ringly.io — 52 Ecommerce Fraud Statistics 2026

- Gitnux — Chargeback Statistics 2026

- Saastr — What Is a Good Refund Policy for a SaaS Product?

- TermsFeed — Refund Policy for SaaS Apps

- PayPro Global — How to Handle SaaS Refund Requests