Selling digital products to EU customers? You’re legally required to collect and remit Value Added Tax (VAT) on every sale. With 27 member states, each with different rates and rules, EU VAT compliance can feel overwhelming for SaaS founders and digital product creators. This guide breaks down everything you need to know about EU VAT for digital products in 2026 — from registration thresholds to filing requirements, and how to automate the entire process.

What Is EU VAT for Digital Products?

EU VAT (Value Added Tax) is a consumption tax applied to goods and services sold within the European Union. For digital products — including SaaS subscriptions, e-books, online courses, software licenses, and downloadable content — special rules apply under the EU VAT Directive on electronic commerce.

Since 2015, the place of taxation for digital services is determined by where your customer is located, not where your business is based. This means if you’re a US-based SaaS company selling to customers in Germany, you must charge German VAT at 19% and remit it to German tax authorities.

The rules apply to B2C (business-to-consumer) sales. B2B sales are generally exempt from VAT collection requirements when the customer provides a valid VAT identification number under the reverse charge mechanism.

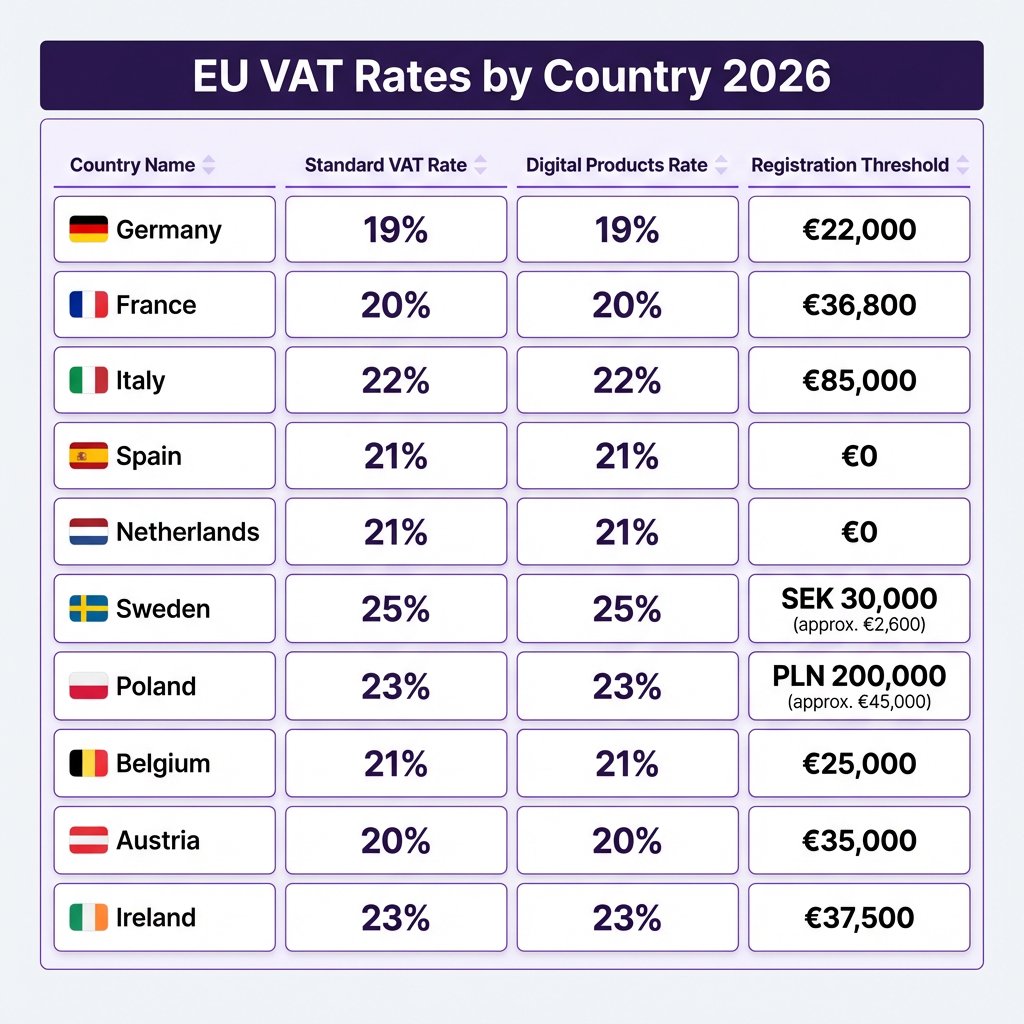

EU VAT Rates by Country (2026)

Standard VAT rates vary significantly across EU member states. Here are the current rates for major markets:

- Hungary: 27% (highest standard rate)

- Denmark, Sweden, Croatia: 25%

- Finland, Greece, Ireland, Poland, Portugal: 23-24%

- Italy, Slovenia: 22%

- Belgium, Czech Republic, Netherlands, Spain: 21%

- France, UK (Northern Ireland): 20%

- Germany, Romania: 19%

- Cyprus, Malta, Luxembourg: 17-19% (lowest standard rates)

Some countries offer reduced rates for specific digital products. For example, e-books often qualify for reduced rates (as low as 5-9% in some jurisdictions). However, SaaS and most software generally fall under standard rates.

Who Needs to Register for EU VAT?

You must register for EU VAT if you sell digital products to consumers in EU member states and exceed the distance selling thresholds. As of July 2021, the rules changed significantly with the introduction of the One-Stop Shop (OSS) system.

Under the current rules, there are two main approaches:

1. One-Stop Shop (OSS) Registration

The OSS allows you to register in a single EU member state and report VAT for all EU sales through a single quarterly return. This eliminates the need to register separately in each country where you have customers. The OSS is available for both EU-established businesses (Union OSS) and non-EU businesses (Import OSS).

2. Individual Country Registration

Alternatively, you can register for VAT in each EU country where you exceed the €10,000 annual threshold for cross-border B2C sales of digital services. Below this threshold, you may be able to charge VAT at your home country’s rate if you’re EU-based, or you may not need to charge VAT at all if you’re outside the EU.

How to Calculate and Collect EU VAT

Proper VAT collection requires accurate customer location verification. EU regulations require two non-contradictory pieces of evidence to determine the customer’s location:

- Billing address country

- IP address geolocation

- Payment method country

- Customer account address

Your checkout system must apply the correct VAT rate based on the customer’s location and maintain records of the evidence used for at least 10 years. The VAT amount must be clearly displayed on invoices and receipts.

For a €100 SaaS subscription sold to a customer in France, you would charge €100 + 20% VAT = €120 total. The €20 VAT must be remitted to French tax authorities through your OSS return or French VAT registration.

Filing EU VAT Returns

VAT returns must be filed quarterly through the OSS portal or directly with each member state’s tax authority. Key deadlines:

- Q1 (Jan-Mar): Due by April 30

- Q2 (Apr-Jun): Due by July 31

- Q3 (Jul-Sep): Due by October 31

- Q4 (Oct-Dec): Due by January 31

Late filing or payment can result in penalties ranging from €50-€500 per return plus interest on unpaid VAT. Some countries impose higher penalties for repeated non-compliance.

Common EU VAT Mistakes to Avoid

Based on audits and compliance reviews, here are the most common mistakes businesses make with EU VAT:

- Incorrect location determination: Using only billing address without IP verification

- Wrong rate application: Applying your home country rate instead of customer location rate

- Missing OSS registration: Continuing to register in multiple countries unnecessarily

- Poor record keeping: Not maintaining location evidence for the required 10 years

- Delayed registration: Waiting too long to register after exceeding thresholds

- Incorrect B2B classification: Not validating VAT IDs for business customers

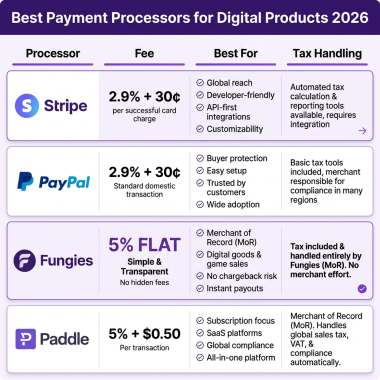

Simplify EU VAT Compliance with Fungies

Stop worrying about VAT rates, registration, and filing. Fungies acts as your Merchant of Record — we handle all EU tax compliance automatically.

Start Free Trial →No credit card required • Automatic VAT handling

Automating EU VAT Compliance

Manually managing EU VAT for multiple countries is error-prone and time-consuming. Modern solutions can automate the entire process:

Tax Calculation APIs

Services like TaxJar, Avalara, and Stripe Tax can automatically determine customer location, apply correct rates, and generate compliant invoices. These integrate directly with your payment processor and checkout flow.

Merchant of Record (MoR) Services

A Merchant of Record acts as the legal seller of your products, handling all tax compliance, including EU VAT registration, collection, and remittance. This shifts the compliance burden entirely to the MoR provider. Fungies.io offers Merchant of Record services specifically designed for SaaS and digital product sellers, handling EU VAT automatically with no additional integration work.

FAQ: EU VAT for Digital Products

Do I need to charge EU VAT if I’m based outside the EU?

Yes. The rules apply based on where your customer is located, not where your business is based. US, UK, and other non-EU businesses must charge EU VAT on B2C digital product sales to EU customers.

What’s the difference between OSS and IOSS?

OSS (One-Stop Shop) covers digital services and goods within the EU. IOSS (Import One-Stop Shop) is specifically for goods imported into the EU with a value up to €150. For digital products, you only need OSS.

Can I avoid EU VAT by using a payment processor?

No. Standard payment processors like Stripe and PayPal don’t handle VAT compliance for you — they just process payments. You still need to calculate, collect, and remit VAT yourself unless you use a Merchant of Record service.

What happens if I don’t comply with EU VAT rules?

Non-compliance can result in penalties, interest charges, and potential blocking of your payment processing. Tax authorities can also pursue unpaid VAT across borders through mutual assistance agreements. The reputational risk of being labeled non-compliant can also damage customer trust.

Do free trials require VAT collection?

No VAT is due on genuinely free trials where no payment is collected. However, if the trial automatically converts to a paid subscription, VAT applies to the paid portion from the conversion date.

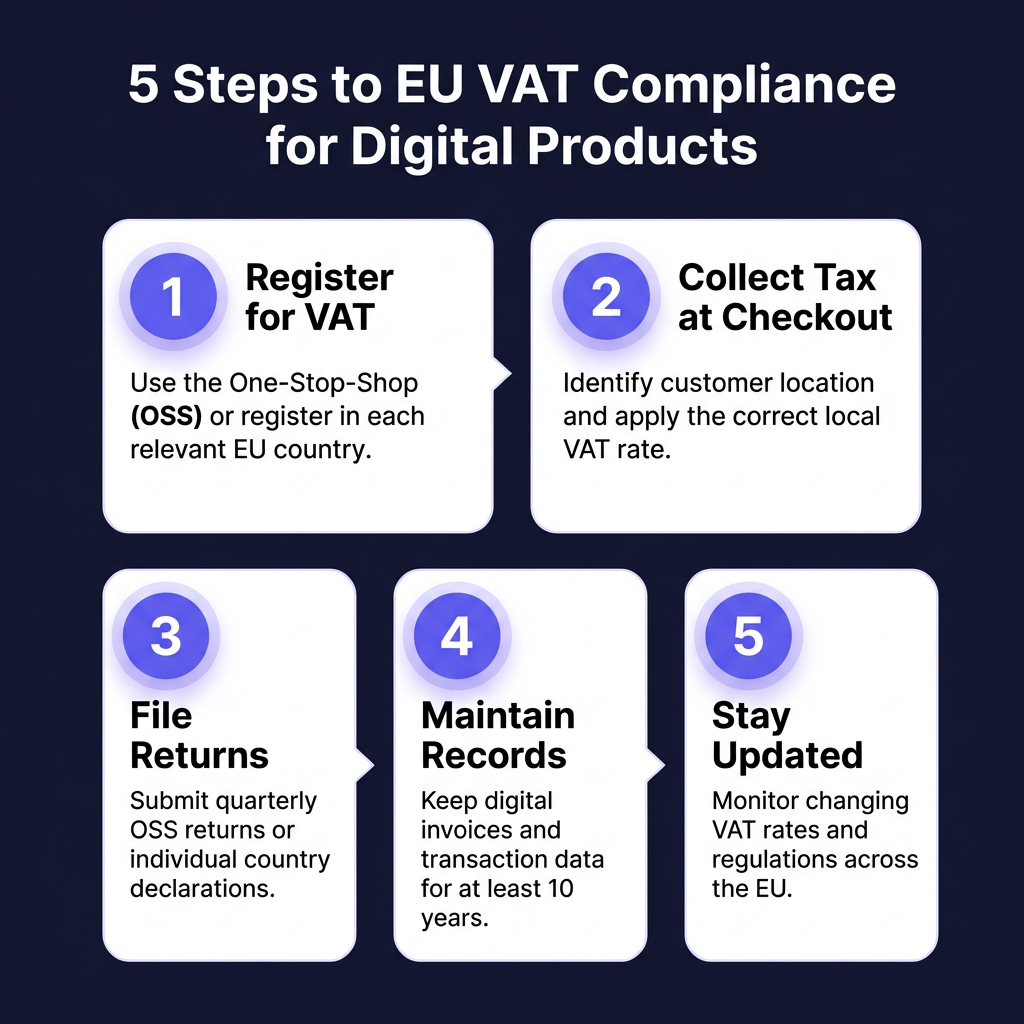

Conclusion

EU VAT compliance for digital products is complex but manageable with the right approach. The key steps are: register for OSS (or individual country VAT), implement accurate location verification at checkout, apply correct rates based on customer location, file quarterly returns on time, and maintain proper records for 10 years.

For most SaaS founders and digital product creators, the simplest solution is using a Merchant of Record like Fungies that handles all EU VAT compliance automatically. This lets you focus on growing your business instead of navigating tax regulations across 27 countries.

Ready to simplify your EU VAT compliance? Start your free trial with Fungies and let us handle the tax complexity while you focus on building.