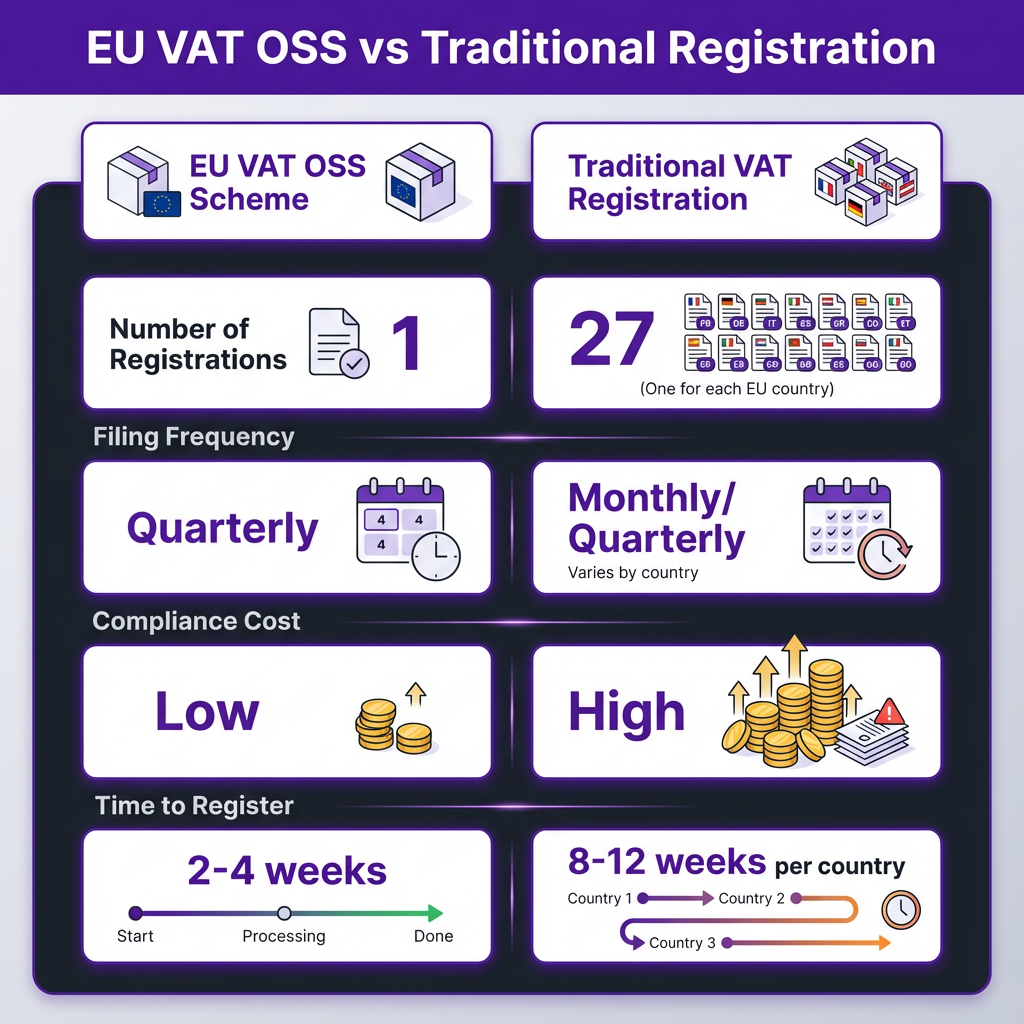

Selling SaaS to EU customers? The EU VAT OSS (One-Stop Shop) scheme is the most efficient way to handle VAT compliance across all 27 EU member states. Instead of registering for VAT in every country where you have customers, OSS lets you register once and file a single quarterly return covering all your EU B2C sales.

In this complete 2026 guide, we’ll walk you through everything SaaS founders need to know about the EU VAT OSS scheme — from registration requirements to quarterly filing, and how to automate the entire process.

What Is the EU VAT OSS Scheme?

The One-Stop Shop (OSS) is an EU VAT simplification scheme introduced in July 2021. It allows businesses selling digital services (including SaaS) to consumers in multiple EU countries to:

- Register for VAT in just one EU member state (your “member state of identification”)

- Charge VAT at each customer’s local rate (ranging from 17% to 27%)

- File a single quarterly OSS VAT return covering all EU sales

- Make one payment to your member state, which distributes funds to other countries

Before OSS existed, SaaS companies had to register for VAT separately in every EU country where they exceeded the local sales threshold — a compliance nightmare that could require 27 separate registrations and filings.

Who Needs to Register for EU VAT OSS?

You must register for EU VAT OSS if you meet both of these conditions:

- You sell digital services (including SaaS, software licenses, ebooks, online courses) to EU consumers

- Your total cross-border B2C sales to EU customers exceed €10,000 per year

The €10,000 threshold applies to your total B2C sales across all EU countries combined, not per country. Below this threshold, you can continue charging VAT at your home country’s rate (if you’re EU-based) or at the rate of your customer’s country (if you’re non-EU based).

EU-Based vs Non-EU SaaS Companies

If you’re based in the EU: You use the Union OSS scheme. You register in your home country (or another EU state if you prefer) and file quarterly returns there.

If you’re based outside the EU: You use the Non-Union OSS scheme. You can register in any EU member state of your choice — many non-EU SaaS companies choose Ireland, the Netherlands, or Germany for their business-friendly tax authorities and English-language support.

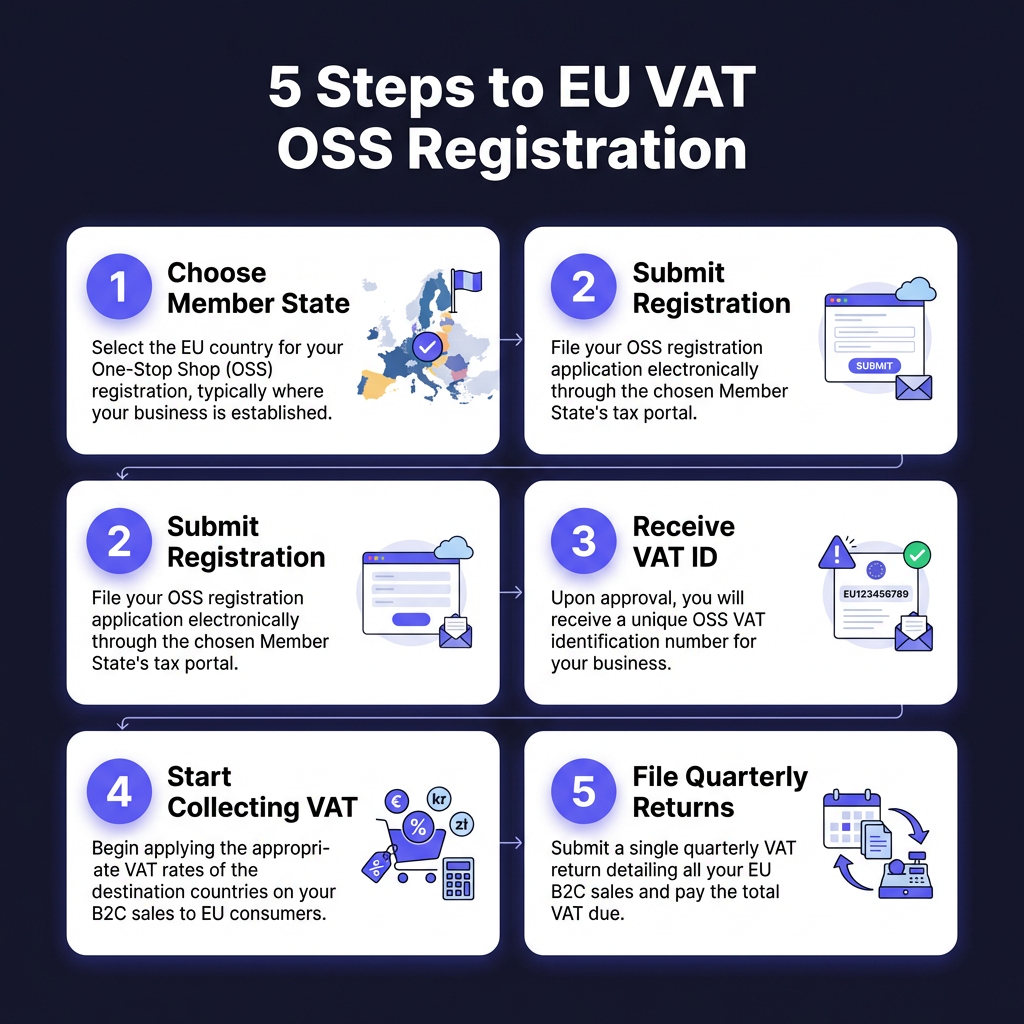

The 5-Step EU VAT OSS Registration Process

Step 1: Choose Your Member State of Identification

Select the EU country where you’ll register for OSS. Consider:

- Language: Can you communicate with their tax authority in English?

- Digital infrastructure: How user-friendly is their OSS portal?

- Processing time: Some states process registrations in 2 weeks, others take 6+ weeks

- Support quality: Responsiveness to questions and issues

Popular choices for non-EU SaaS companies include Ireland (English-speaking, tech-friendly), the Netherlands (efficient digital systems), and Germany (robust infrastructure).

Step 2: Gather Required Documentation

You’ll typically need:

-

li>Certificate of incorporation or business registration

- Proof of business address

- Director/owner identification

- Description of your digital services

- Estimated annual EU sales volume

Step 3: Submit Your OSS Registration

Most EU countries offer online OSS registration portals. The application typically takes 30-60 minutes to complete. You’ll receive an acknowledgment immediately and your OSS VAT ID within 2-6 weeks.

Step 4: Configure Your SaaS Billing System

Once registered, update your payment system to:

- Charge VAT at the customer’s local EU rate (not your home rate)

- Apply the correct VAT rate for each of the 27 EU countries (rates range from 17% in Luxembourg to 27% in Hungary)

- Display VAT-inclusive pricing for B2C customers

- Collect and store customer location evidence (IP address, billing address, bank location)

Step 5: File Quarterly OSS Returns

OSS returns are due quarterly:

- Q1 (Jan-Mar): Due by April 30

- Q2 (Apr-Jun): Due by July 31

- Q3 (Jul-Sep): Due by October 31

- Q4 (Oct-Dec): Due by January 31

Your return must break down sales by EU country and VAT rate. Payment is made to your member state, which distributes funds to other countries.

EU VAT Rates by Country (2026)

Standard VAT rates vary significantly across the EU:

| Country | VAT Rate | Country | VAT Rate |

|---|---|---|---|

| Hungary | 27% | Sweden | 25% |

| Croatia | 25% | Denmark | 25% |

| Finland | 24% | Greece | 24% |

| Ireland | 23% | Poland | 23% |

| Italy | 22% | Spain | 21% |

| Belgium | 21% | Netherlands | 21% |

| France | 20% | UK | 20% |

| Germany | 19% | Cyprus | 19% |

| Luxembourg | 17% |

Common EU VAT OSS Mistakes to Avoid

Based on our experience helping hundreds of SaaS companies with EU VAT compliance, here are the most common pitfalls:

1. Not Registering Soon Enough

Many SaaS founders wait until they’ve clearly exceeded the €10,000 threshold. But if you’re growing quickly, you should register proactively. Late registration can result in penalties and backdated VAT liabilities.

2. Incorrect Customer Location Determination

EU VAT rules require two pieces of non-contradictory evidence to determine customer location. Common mistakes include relying solely on billing address (customers may use foreign credit cards) or not storing location evidence for audit purposes.

3. Missing the Quarterly Filing Deadline

Late OSS returns incur penalties that vary by member state but typically start at €50-€200 plus interest on unpaid VAT. Set calendar reminders for the filing deadlines.

4. Confusing B2B and B2C Sales

B2B sales to EU customers with valid VAT numbers are handled under the reverse charge mechanism and don’t go through OSS. Only B2C sales are reported via OSS.

Automating EU VAT OSS Compliance

Manual EU VAT compliance is complex and error-prone. Modern SaaS companies typically use one of three approaches:

Option 1: Tax Automation Software

Tools like TaxJar, Avalara, and Quaderno integrate with your billing system to automatically calculate VAT, collect location evidence, and generate OSS returns. This gives you control but requires ongoing management.

Option 2: Merchant of Record (Recommended)

A Merchant of Record like Fungies.io acts as the legal seller of your SaaS product. The MoR handles all VAT registration, collection, and filing — you simply receive payouts net of fees and taxes. This is the most hands-off approach and is ideal for SaaS companies wanting to focus on growth rather than tax compliance.

Option 3: Manual Compliance

Possible for very early-stage SaaS with minimal EU sales, but not recommended as you scale. The time cost and risk of errors typically outweigh any savings.

Ready to Simplify Your EU VAT Compliance?

Join hundreds of SaaS companies using Fungies.io — automated EU VAT collection, OSS filing, and global Merchant of Record services.

No credit card required

FAQ: EU VAT OSS for SaaS

Do I need OSS if I’m below the €10,000 threshold?

No. Below €10,000 in annual EU B2C sales, EU-based companies charge their home country VAT rate, while non-EU companies charge VAT at the customer’s country rate but don’t need to register for OSS until they exceed the threshold.

Can I use OSS for B2B sales?

No. B2B sales to EU customers with valid VAT numbers use the reverse charge mechanism. The customer accounts for VAT themselves. You only need to validate their VAT number and include it on invoices.

What happens if I don’t register for OSS?

If you exceed €10,000 in EU B2C sales and don’t register, you’re operating non-compliant. Tax authorities can impose penalties, backdated VAT liabilities, and in serious cases, block your ability to sell in their jurisdiction.

How long does OSS registration take?

Typically 2-6 weeks depending on the member state and completeness of your application. Ireland and the Netherlands tend to be faster (2-3 weeks), while some Southern European states take longer.

Can I change my member state after registration?

Yes, but it’s administratively complex. You need to deregister from your current member state and re-register in the new one. It’s better to choose carefully from the start.

Conclusion: Simplify Your EU VAT Compliance

The EU VAT OSS scheme is a significant improvement over the pre-2021 system, but it still requires careful attention to registration, rate calculation, and quarterly filing. For growing SaaS companies, the most efficient path is often partnering with a Merchant of Record who handles all EU VAT compliance on your behalf.

Whether you choose to manage OSS yourself or outsource it, the key is staying compliant from day one. Tax authorities across the EU are increasingly sophisticated at identifying non-compliant digital sellers — and the cost of getting caught far exceeds the cost of proper compliance.

Ready to eliminate EU VAT complexity? Fungies.io handles OSS registration, VAT collection, and quarterly filing as part of our Merchant of Record service — so you can focus on building your SaaS, not navigating tax regulations.