Selling digital products globally sounds simple until you realize every country wants a cut. VAT in the EU, GST in Australia, sales tax in 45 US states, consumption tax in Japan—and each has different rates, thresholds, and filing requirements. Get it wrong, and you’re looking at fines up to €25,000 per jurisdiction, account suspensions, and potential criminal charges.

This guide covers everything you need to know about the Merchant of Record (MOR) model: what it is, how it works, who needs it, and how it compares to handling tax compliance yourself. By the end, you’ll understand why 68% of internet users paying for digital content monthly has created a $2.5 trillion market—and why tax compliance has become the make-or-break factor for scaling globally.

What Is a Merchant of Record?

A Merchant of Record (MOR) is the legal entity responsible for processing payments, collecting taxes, handling refunds, and maintaining compliance in every jurisdiction where you sell. When a customer buys your digital product through an MOR platform, the MOR—not you—is the seller of record on the transaction.

This distinction matters because tax liability follows the seller of record. If you’re selling directly through Stripe or PayPal, you’re the merchant of record. That means you must register for VAT in 27 EU countries, track economic nexus across 45 US states, file quarterly returns in Australia, and stay current with ever-changing tax rules in 130+ countries. Miss a filing deadline in Germany? That’s up to €25,000 in penalties. Fail to register in the UK? You’re breaking the law from your first sale.

An MOR absorbs this liability. They register for taxes, calculate rates at checkout, file returns, remit payments, and handle audits. You get a single payout, a single 1099 (or local equivalent), and zero compliance burden. According to Research and Markets, the Merchant of Record software market grew from $11.61 billion in 2024 to $13.20 billion in 2025—and is projected to hit $35.43 billion by 2032 at a 14.96% CAGR. That growth reflects a simple reality: global tax compliance has become too complex for most businesses to handle alone.

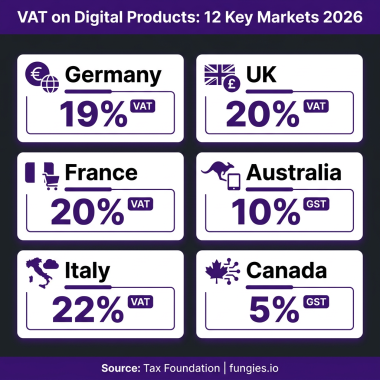

Global VAT Rates on Digital Products: Key Markets

Key Statistics at a Glance

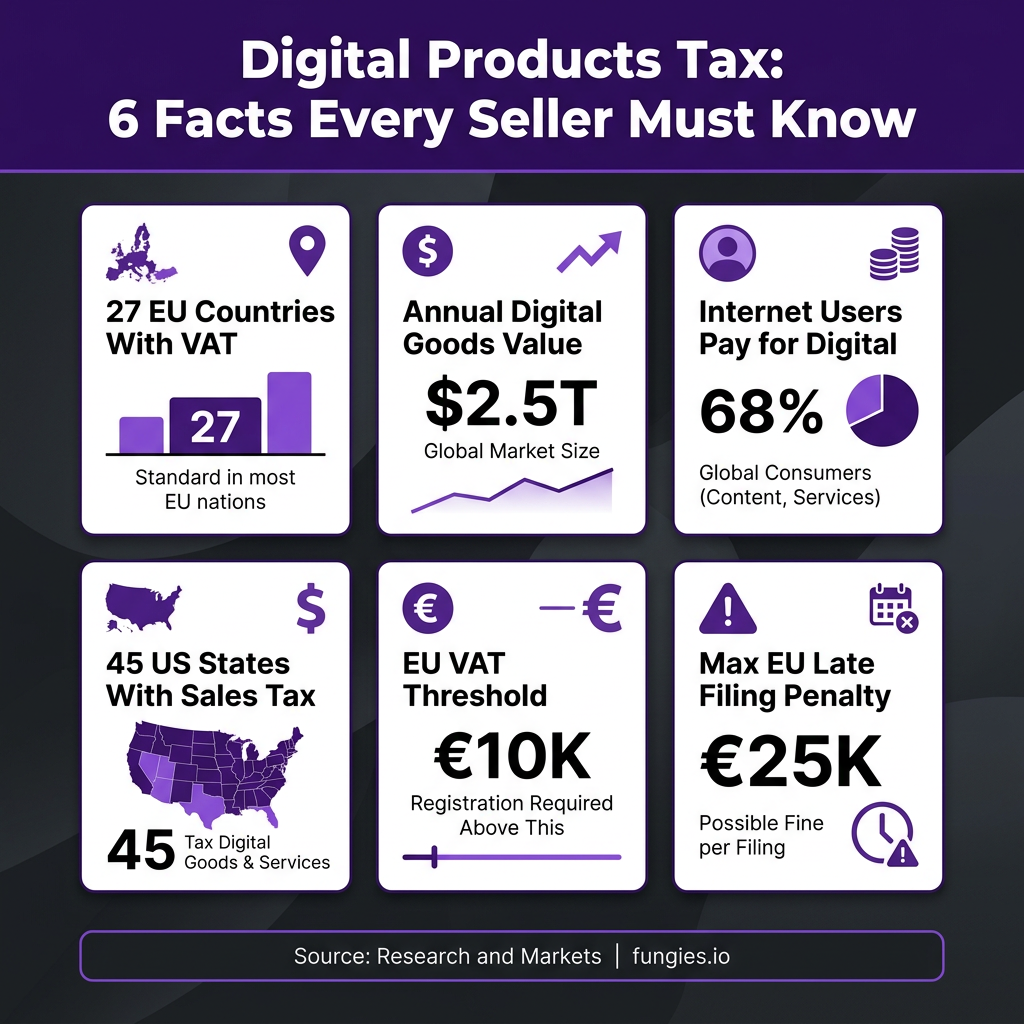

- 27 EU countries require VAT registration for non-resident digital sellers with no threshold—compliance starts at sale #1 (European Commission)

- $2.5 trillion in annual value created by digital products globally (Swell Ecommerce)

- 68% of internet users aged 16+ paid for digital content monthly in 2025 (DataReportal)

- 45 US states impose sales tax, with economic nexus thresholds typically at $100,000 or 200 transactions (TaxCloud)

- €10,000 EU-wide threshold applies only to EU-established businesses; non-EU sellers have zero threshold (Nexway)

- 9.5% VAT compliance gap in the EU in 2023—the difference between expected and actual VAT collected (European Commission)

- 25 US jurisdictions now tax SaaS in some form, up from just a handful five years ago (Anrok)

- €25,000 maximum penalty for late VAT filing in Germany, plus 10% of assessed VAT (Vertex)

- $13.20 billion Merchant of Record software market size in 2025 (Research and Markets)

- 14.96% CAGR projected growth rate for MOR software through 2032

Country-by-Country Tax Rules for Digital Products

Tax compliance for digital products varies dramatically by jurisdiction. Here is what you need to know about the major markets:

European Union: The VAT OSS System

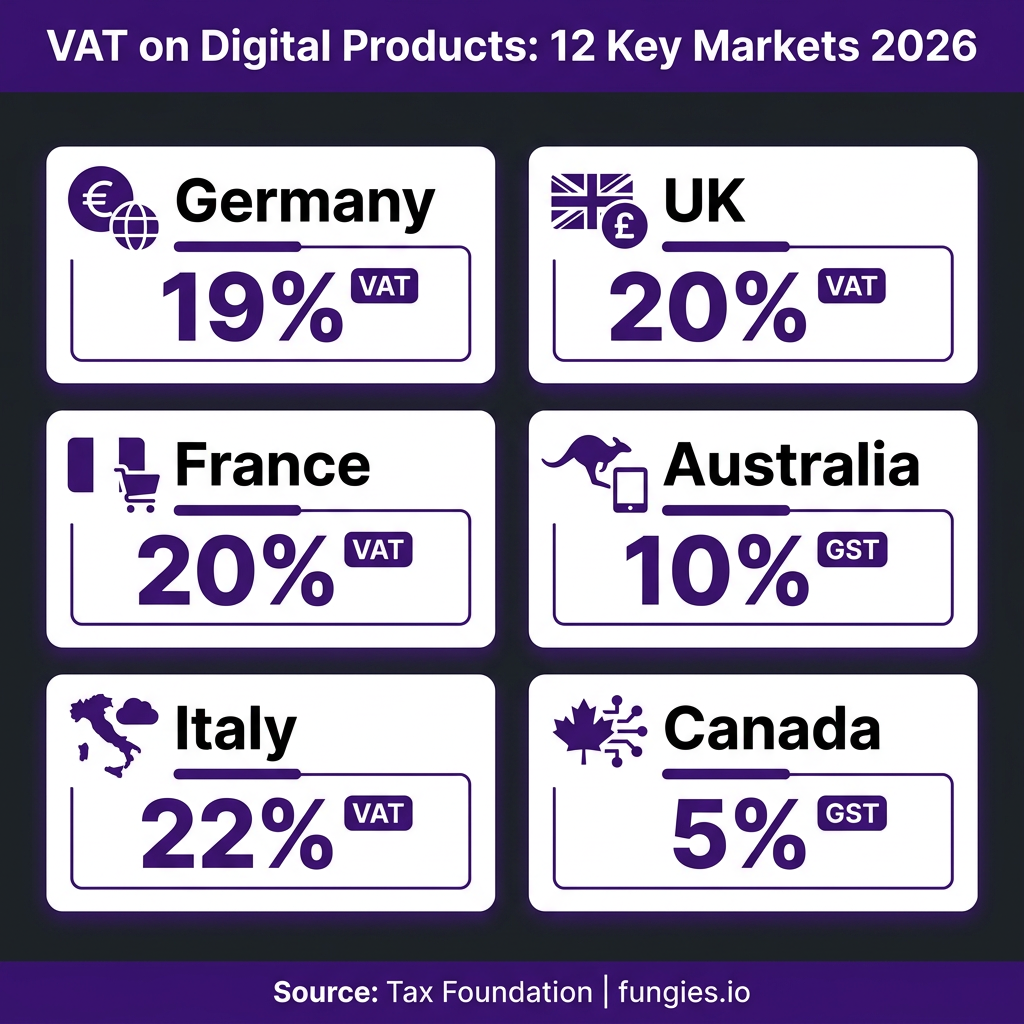

The EU has 27 member states with VAT rates ranging from 17% (Luxembourg) to 27% (Hungary), averaging 21.8%. For non-EU businesses selling digital services to EU consumers, there is no registration threshold—you must register for VAT from your first sale. The EU VAT One Stop Shop (OSS) allows you to register in one member state and file a single quarterly return covering all EU sales, but you still need to charge the correct VAT rate for each customer’s country.

Key EU VAT rates for 2026: Germany 19%, France 20%, Italy 22%, Spain 21%, Netherlands 21%, Poland 23%, Ireland 23%. Filing is quarterly through the OSS system, and penalties for non-compliance range from €50 to €25,000+ depending on the country and severity of the violation.

United Kingdom: Post-Brexit Rules

The UK charges 20% VAT on digital services sold to UK consumers. For non-UK businesses, there is no registration threshold—you must register from your first B2C sale. The UK left the EU VAT OSS system post-Brexit, so you will need a separate UK VAT registration and must file quarterly returns through HMRC’s Making Tax Digital (MTD) system. Late filing penalties start at £100 and escalate based on the VAT owed.

United States: Economic Nexus Chaos

The US has no federal sales tax. Instead, 45 states (plus DC) impose their own sales taxes, each with different rates, rules, and product taxability. Following the 2018 South Dakota v. Wayfair Supreme Court decision, states can require out-of-state sellers to collect sales tax based on “economic nexus”—typically $100,000 in annual sales or 200 transactions in the state.

Here is the problem: SaaS taxability varies by state. As of 2026, SaaS is taxable in 25 US jurisdictions, but the rules differ—some tax B2B and B2C, some only B2C, some exempt SaaS entirely. You need to track your sales in every state, monitor threshold crossings, register promptly, and file returns in each jurisdiction where you have nexus. Penalties vary but typically include fines plus interest on unpaid tax.

Canada: GST/HST Complexity

Canada imposes a 5% federal GST on digital services sold to Canadian consumers. The registration threshold is CAD $30,000 in worldwide taxable sales over four consecutive calendar quarters. But it gets complicated: some provinces add provincial sales tax (PST), creating combined rates up to 15% in certain jurisdictions. British Columbia charges 7% PST on out-of-province digital sales with a CAD $10,000 threshold, while Saskatchewan charges 6% PST with no small-supplier exemption.

Asia-Pacific Markets

Australia charges 10% GST on digital products and services sold to Australian consumers. The registration threshold is AUD $75,000. New Zealand charges 15% GST with a NZD $60,000 threshold. Japan’s consumption tax is 10% with a JPY 10 million threshold. South Korea charges 10% VAT with a KRW 80 million threshold. Each requires separate registration, quarterly or annual filing, and has its own penalty structure.

Global Digital Tax Rates Reference Table

| Country | Tax Rate | Registration Threshold | Filing Frequency | Late Filing Penalty |

|---|---|---|---|---|

| Germany | 19% | No threshold (non-EU) | Quarterly via OSS | Up to €25,000 |

| France | 20% | No threshold (non-EU) | Quarterly via OSS | Up to €15,000 |

| Italy | 22% | No threshold (non-EU) | Quarterly via OSS | Up to €25,000 |

| Spain | 21% | No threshold (non-EU) | Quarterly via OSS | Up to €12,000 |

| Netherlands | 21% | No threshold (non-EU) | Quarterly via OSS | Up to €5,000 |

| Poland | 23% | No threshold (non-EU) | Quarterly via OSS | Up to €15,000 |

| United Kingdom | 20% | No threshold (non-resident) | Quarterly (MTD) | Up to 15% of VAT due |

| Australia | 10% | AUD $75,000 | Quarterly/BAS | Up to 75% of GST owed |

| Canada | 5% GST | CAD $30,000 | Annual/Quarterly | Up to 20% + interest |

| Japan | 10% | JPY 10 million | Annual | Up to 35% of tax due |

| South Korea | 10% | KRW 80 million | Quarterly | Up to 20% of VAT owed |

| Norway | 25% | NOK 50,000 | Bi-monthly | Up to 60% of VAT owed |

| Switzerland | 8.1% | CHF 100,000 | Quarterly | Up to 20% of VAT due |

| New Zealand | 15% | NZD $60,000 | Bi-monthly | Up to 40% of GST owed |

Digital Products Tax: Key Statistics

Tax Obligations by Business Type

Different business models face different tax compliance challenges. Here is how tax obligations break down:

| Business Type | Key Tax Obligations | Common Mistakes | Risk Level |

|---|---|---|---|

| SaaS Companies | VAT in EU/UK from first sale; economic nexus in 25+ US states; GST in Australia/Canada | Assuming B2B SaaS is exempt; missing nexus thresholds | High |

| Content Creators | Income tax + VAT on digital products; 1099-K reporting (US); EU VAT on courses/templates | Treating all income as “passive”; not registering for VAT | Medium-High |

| AI/API Companies | Same as SaaS; potential DST (Digital Services Tax) in some jurisdictions; B2B reverse charge | Misclassifying AI outputs for tax purposes | High |

| Game Developers | VAT on digital downloads; sales tax on in-app purchases; platform withholding obligations | Relying on app stores to handle all taxes | Medium |

| Ebook/Course Sellers | EU VAT on all digital sales; US sales tax where nexus exists; self-employment tax | Not charging VAT to EU customers | Medium |

Tax Remittance: What It Means and How It Works

Tax remittance is the process of sending collected taxes to the appropriate tax authority. When you sell a digital product for €100 in Germany with 19% VAT, you collect €119 total. That extra €19 is not yours—it is held in trust for the German tax authority until you remit it, typically quarterly.

Here is where it gets complicated: you need to remit to every jurisdiction where you are registered. Selling to 27 EU countries means 27 different remittance schedules, bank accounts, and compliance requirements. Some countries require monthly filings above certain thresholds. Others have bi-monthly or annual schedules. Currency conversion, international wire fees, and timing differences create additional complexity.

Late remittance triggers penalties. In Germany, late payment incurs interest plus penalties up to 10% of the assessed VAT. The UK charges daily interest on late payments plus escalating penalties based on the VAT owed. Australia can impose penalties up to 75% of the GST owed for intentional disregard of tax law. These penalties compound—miss multiple filings, and you are facing a financial crisis.

Fines and Penalties: What Non-Compliance Costs

Tax authorities worldwide are getting more aggressive about digital VAT enforcement. The EU’s VAT compliance gap—the difference between expected and actual VAT collected—was 9.5% in 2023, representing billions in lost revenue. Governments are investing in technology to close this gap, and digital sellers are in the crosshairs.

| Jurisdiction | Fine Type | Amount | Interest Rate | Criminal Threshold |

|---|---|---|---|---|

| Germany | Late filing | Up to €25,000 + 10% of VAT | Base rate + 2% | Intentional tax evasion |

| UK | Late payment | 2-15% of VAT owed | Bank of England base + 2.5% | Fraudulent evasion |

| France | Non-filing | Up to €15,000 | 0.4% per month | Organized fraud |

| Italy | Late filing | Up to €25,000 | Official reference rate | Aggravated evasion |

| Australia | False statement | Up to 75% of GST owed | Short-term Treasury bond rate | Tax fraud |

| US (varies by state) | Failure to file | 5-25% of tax owed | Variable by state | Willful evasion |

Beyond financial penalties, non-compliance can trigger account suspensions on payment platforms, frozen funds, reputational damage, and in severe cases, criminal prosecution. The UK prosecuted over 1,000 tax fraud cases in 2024, with average sentences increasing year over year.

Merchant of Record vs Self-Compliance

How Merchant of Record Solves Tax Compliance

A Merchant of Record transfers tax liability from you to the MOR provider. Here is how it works: when a customer buys your product, the MOR is the seller of record on the transaction. They collect payment, calculate and charge the correct tax rate based on the customer’s location, remit taxes to each jurisdiction, file returns, handle refunds, and manage compliance.

You receive a single payout—typically within a few days—minus the MOR’s fee. No VAT registrations. No quarterly filings. No tracking nexus thresholds across 45 states. No risk of penalties for missed deadlines. The MOR handles everything, and their compliance becomes your compliance.

Fungies.io operates as a Merchant of Record for digital product sellers, SaaS companies, and content creators. For 5% + $0.50 per transaction, Fungies handles VAT in 27 EU countries, GST in Australia and New Zealand, sales tax in US states, and compliance in 50+ countries total. You get a single integration, a single payout, and zero tax compliance burden.

Compare that to self-compliance: registering in 27 EU countries (€500-2,000 each), filing quarterly returns (accountant fees €200-500 per filing), tracking US nexus (software $200+/month), potential penalties for errors (€5,000-25,000), and the time cost of managing it all (40+ hours annually). For most businesses, the MOR fee is significantly cheaper than the true cost of self-compliance.

FAQ: Merchant of Record and Tax Compliance

What is the difference between a payment gateway and a merchant of record?

A payment gateway (like Stripe or PayPal) processes payments but you are still the merchant of record. You are responsible for tax registration, collection, filing, and remittance in every jurisdiction. An MOR (like Fungies, Paddle, or Lemon Squeezy) becomes the seller of record, absorbing tax liability and handling all compliance. Payment gateways charge 2.9% + $0.30 but leave you with the compliance burden; MORs charge 5% + $0.50 and handle everything.

Do I need to charge VAT on SaaS subscriptions in the EU?

Yes. SaaS is considered a digital service under EU VAT rules. If you are selling to EU consumers, you must charge VAT at the customer’s local rate (ranging from 17% to 27%). For non-EU businesses, there is no registration threshold—compliance starts at your first EU sale. You can either register for VAT in each EU country or use the One Stop Shop (OSS) system to file a single quarterly return covering all EU sales.

What happens if I don’t collect sales tax in the US?

If you have economic nexus in a state (typically $100,000 in sales or 200 transactions annually) and don’t collect sales tax, you are liable for the uncollected tax plus penalties and interest. States can audit your records going back several years, assess the tax you should have collected, and impose fines ranging from 5% to 25% of the tax owed. Some states also pursue criminal charges for willful evasion. The 2018 Wayfair decision made it clear that physical presence is not required for nexus—economic activity alone can trigger obligations.

How does the EU VAT One Stop Shop (OSS) work?

The EU VAT OSS allows businesses to register for VAT in a single EU member state and file a single quarterly return covering all EU B2C sales. You charge VAT at the customer’s local rate, report all sales through the OSS portal, and make a single payment that is distributed to the appropriate countries. This eliminates the need for 27 separate VAT registrations. However, you still need to track rates for each country, calculate VAT correctly at checkout, and file quarterly. Non-EU businesses can use the Non-Union OSS scheme.

What are the penalties for not registering for VAT in the EU?

Penalties vary by country but are severe. Germany charges up to €25,000 for late filing plus 10% of assessed VAT. France fines up to €15,000. Italy also reaches €25,000. Beyond fines, you will owe back taxes plus interest (typically 2-4% annually), and tax authorities can freeze your accounts, suspend your ability to sell, and pursue criminal charges for intentional evasion. The EU’s 9.5% VAT compliance gap means governments are actively hunting non-compliant sellers.

Conclusion: The Smart Choice for Global Sellers

Global tax compliance for digital products is not getting simpler. New jurisdictions are adding digital taxes regularly, existing rules are becoming more complex, and enforcement is intensifying. The EU’s 9.5% VAT gap, the US’s fragmented economic nexus landscape, and the proliferation of digital services taxes worldwide create a compliance burden that most businesses cannot handle alone.

A Merchant of Record is not just a convenience—it is risk mitigation. For 5% + $0.50 per transaction, you eliminate the possibility of €25,000 fines, the complexity of 27 EU VAT registrations, the tracking burden of 45 US state nexus rules, and the time cost of quarterly filings. You get a single integration, a single payout, and the freedom to focus on growing your business instead of managing tax compliance.

The $13.20 billion Merchant of Record market exists because it delivers value. As digital commerce grows toward $29 trillion by 2035, tax compliance will only become more critical. The question is not whether you can afford an MOR—it is whether you can afford not to have one.

Ready to eliminate your tax compliance burden? Create your free Fungies account and start selling globally with zero tax liability. Handle payments, taxes, and compliance in 50+ countries with a single integration.

Sources & References

- Research and Markets — Merchant of Record Software Market Global Forecast 2025-2032 (market size data)

- Swell Ecommerce — 32 Digital Product Sales Statistics 2026 (digital goods value, user payment data)

- Future Market Insights — Creator Economy Market Analysis 2025-2035 (creator economy size and growth)

- Precedence Research — Digital Commerce Market Size 2026-2035 (digital commerce market projections)

- Tax Foundation — VAT Rates in Europe 2026 (EU VAT rates by country)

- Numeral — EU VAT Rates by Country 2026 Guide (EU VAT thresholds and rules)

- Double Point Accountancy — Ultimate Guide to VAT on Digital Services (UK VAT rules post-Brexit)

- Anrok — Australia GST Guide for Digital Businesses (Australia GST rates and thresholds)

- TaxCloud — Sales Tax Nexus by State Chart (US economic nexus thresholds)

- Anrok — SaaS Sales Tax by State 2026 (US SaaS taxability by state)

- Paddle — VAT Penalties Guide for SaaS and App Companies (EU VAT penalties and fines)

- Vertex — VAT Non-Compliance Penalties (Germany late filing penalties)

- European Commission — VAT Gap Report (EU VAT compliance gap statistics)

- Fungies.io — Paddle vs FastSpring vs Lemon Squeezy Comparison 2026 (MOR pricing comparison)

- Avalara — Global VAT and GST on Digital Services (global digital tax rates and thresholds)