Choosing the right payment infrastructure can make or break your digital business. When you’re selling SaaS products, online courses, or digital downloads, you face a critical decision: should you use a Merchant of Record (MoR) or a traditional Payment Processor?

I’ve spent years managing payments for digital products, and the difference between these two approaches isn’t just technical—it’s strategic. Get it wrong, and you’ll spend countless hours on tax compliance, chargeback disputes, and regulatory headaches. Get it right, and you can focus on what actually matters: growing your business.

What Is a Payment Processor?

A payment processor is a service that handles the technical side of credit card transactions. Think Stripe, PayPal, or Square. They move money from your customer’s bank account to yours, but that’s where their responsibility typically ends.

When you use a payment processor, you remain the merchant of record. This means you’re legally responsible for:

- Collecting and remitting sales tax, VAT, and GST in every jurisdiction where you have customers

- Managing PCI DSS compliance and data security

- Handling chargebacks and payment disputes

- Setting up and maintaining merchant accounts

- Navigating international payment regulations

Payment processors typically charge 2.9% + $0.30 per transaction. Sounds affordable, right? But those are just the processing fees. The real cost comes from the operational overhead of managing compliance yourself.

What Is a Merchant of Record?

A Merchant of Record is a legal entity that becomes the seller of record for your transactions. Companies like Fungies, Paddle, and FastSpring act as the MoR, which means they take on the legal and financial responsibilities of selling to your customers.

When a customer buys your product through an MoR, the transaction legally happens between the customer and the MoR—not you. The MoR then pays you the proceeds, minus their fees.

An MoR handles:

- Global tax compliance (VAT, GST, sales tax) automatically calculated and remitted

- PCI DSS compliance and payment security

- Chargeback management and fraud protection

- Merchant account management across multiple regions

- Localized checkout experiences and payment methods

- Invoice generation and regulatory documentation

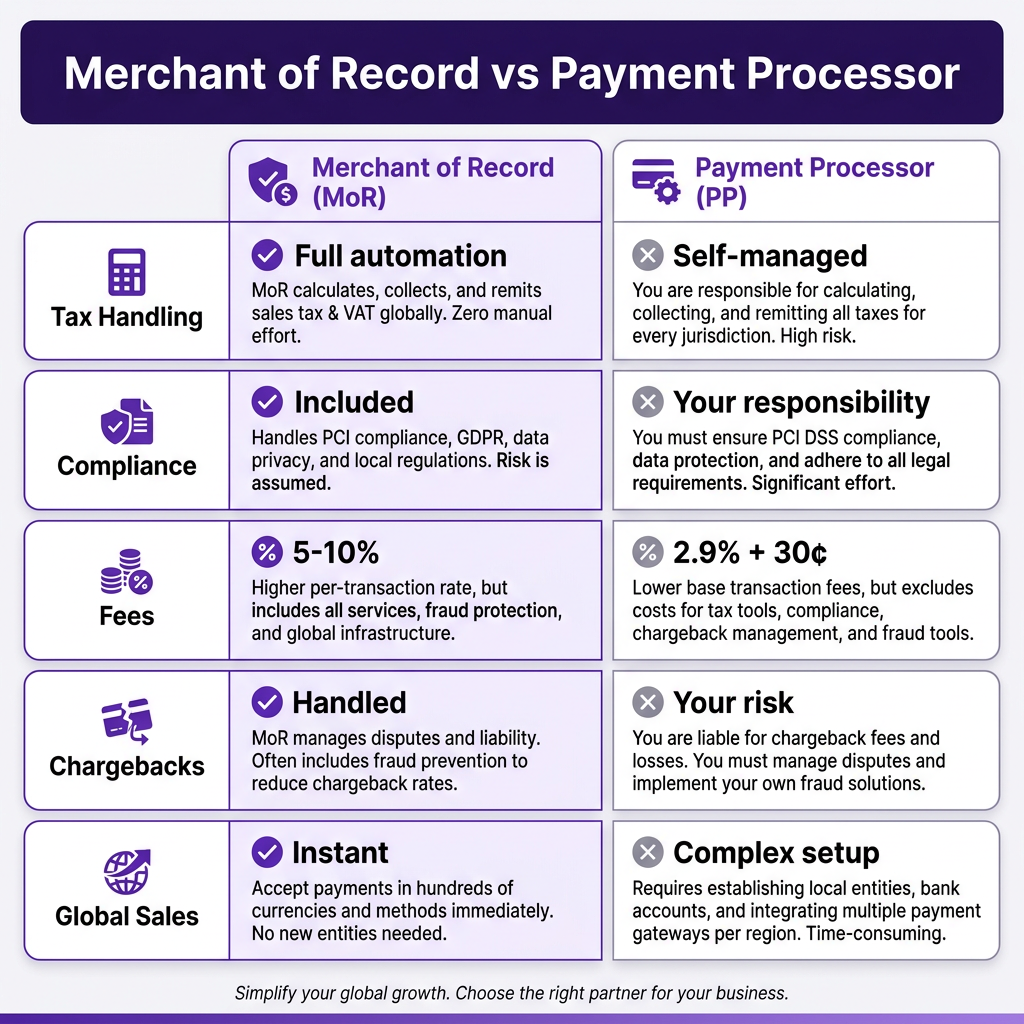

Key Differences at a Glance

Here’s how these two approaches stack up across the dimensions that matter most for digital product sellers:

| Feature | Payment Processor | Merchant of Record |

|---|---|---|

| Tax handling | You calculate, collect, and remit | Fully automated |

| Compliance burden | Your responsibility | Handled by MoR |

| Transaction fees | 2.9% + $0.30 | 5-10% all-inclusive |

| Chargeback risk | You bear the risk | MoR manages disputes |

| Global expansion | Complex, multi-vendor setup | Instant worldwide |

| Setup time | Days to weeks | Hours |

| Legal liability | You are the seller | MoR is the seller |

When to Choose a Payment Processor

A traditional payment processor makes sense if:

- You sell primarily in one country — Managing sales tax in a single jurisdiction is manageable

- You have a finance team — Someone can handle tax registration, filing, and compliance

- You want maximum control — Over checkout flow, branding, and customer data

- You sell physical goods — Where tax rules are often simpler than digital products

- Your margins are thin — And you can’t absorb higher MoR fees

Payment processors work best for established businesses with the resources to manage compliance internally. If you’re a startup or small team, the hidden costs of DIY compliance often outweigh the lower transaction fees.

When to Choose a Merchant of Record

An MoR is the better choice if:

- You sell globally — Even a handful of international customers triggers VAT/GST obligations

- You sell digital products — Where tax rules are notoriously complex and vary by jurisdiction

- You’re a startup or small team — Without dedicated finance/legal resources

- You want to launch fast — MoRs get you selling worldwide in hours, not months

- You value peace of mind — Over absolute control of every detail

The MoR model was practically built for SaaS companies and digital product creators. When your customers are spread across 50+ countries, managing tax compliance yourself becomes a full-time job.

Real-World Cost Comparison

Let’s look at a realistic scenario: You’re a SaaS founder selling a $50/month subscription to customers in the US, EU, UK, and Australia.

With a Payment Processor:

- Processing fees: 2.9% + $0.30 = $1.75 per transaction

- Tax software (Avalara/TaxJar): ~$200/month

- Accountant for international compliance: ~$500/month

- Your time managing compliance: 10+ hours/month

- True cost: $700+/month + your time

With a Merchant of Record (e.g., Fungies at 5% + $0.50):

- MoR fees: 5% + $0.50 = $3.00 per transaction

- Tax handling: Included

- Compliance management: Included

- Your time: Minimal

- True cost: $3.00 per transaction

At 100 customers, the payment processor approach costs you $700 + 10 hours of your time monthly. The MoR approach costs $300. The “cheaper” option is actually 2x more expensive when you factor in the hidden costs.

Popular Options in 2026

Payment Processors:

- Stripe — Developer-friendly, extensive customization, but you’re responsible for compliance

- PayPal — Wide customer trust, simple setup, higher fees for international

- Square — Good for omnichannel, strong in-person + online

Merchants of Record:

- Fungies — 5% + $0.50, modern API, built for SaaS and digital products

- Paddle — 5% + $0.50, established player, strong for software

- FastSpring — Custom pricing, enterprise focus, robust features

FAQ

Can I switch from a payment processor to an MoR later?

Yes, but it requires migrating your customers and potentially updating your checkout flow. It’s easier to start with an MoR if you anticipate global growth.

Do MoRs handle refunds?

Yes, MoRs typically handle the entire refund process, including reversing taxes and updating compliance records.

Is my customer data safe with an MoR?

Reputable MoRs are PCI DSS Level 1 compliant and often exceed the security standards of individual businesses. Your customer data is typically safer with an established MoR.

Can I use both?

Some businesses use an MoR for international sales and a payment processor for domestic transactions. However, this adds complexity that most small teams should avoid.

What’s the catch with MoR pricing?

The higher percentage fee can hurt if you have very high transaction volumes (think $1M+/month). At that scale, negotiating custom rates or building in-house compliance might make sense.

Conclusion

The choice between a Merchant of Record and a payment processor comes down to one question: Do you want to build a payments infrastructure company, or do you want to build your product?

If you’re selling digital products globally and don’t have a dedicated finance team, an MoR will save you time, money, and stress. The slightly higher transaction fees are more than offset by the compliance burden you offload.

If you’re selling primarily in one market, have the resources to manage compliance, and want maximum control, a payment processor gives you that flexibility at a lower per-transaction cost.

For most SaaS founders and digital product creators in 2026, the Merchant of Record model is the smarter choice. You didn’t start your business to become a tax compliance expert—let the specialists handle that while you focus on growth.

Ready to Simplify Your Payment Compliance?

Join hundreds of SaaS companies using Fungies.io — automated tax compliance, 50+ payment methods, global Merchant of Record.

No credit card required