Here’s a stat that should make any SaaS founder’s stomach drop: the EU collected over €1.1 trillion in VAT revenue in 2024, and digital services now account for a rapidly growing share of that. If you’re selling SaaS, software licences, or digital downloads to customers in Europe and you’re not handling EU VAT correctly, you’re not just leaving money on the table — you’re building legal liability.

The problem? EU VAT compliance for digital services is genuinely hard. Twenty-seven countries. Rates ranging from 17% to 27%. A destination-based tax system where the rate depends on where your customer is, not where you are. And a brand new reporting framework — ViDA (VAT in the Digital Age) — that’s rolling out between now and 2030.

This is exactly why EU VAT on digital services is one of the biggest hidden costs for growing SaaS companies — and exactly why a Merchant of Record exists to take that entire problem off your plate.

What EU VAT on Digital Services Actually Means

VAT (Value Added Tax) is a consumption tax. Every EU country charges it. Unlike sales tax in the US, which varies by state and sometimes by product type, EU VAT applies to nearly everything — including SaaS, software downloads, e-books, API access, and digital subscriptions.

The critical rule for digital services is the destination principle, which has been in force since 2015:

- You charge VAT at the rate of your customer’s country, not your own

- This applies whether you’re an EU company or based outside the EU

- For B2C sales (selling to consumers), you’re fully responsible for collection and remittance

- For B2B sales (selling to other businesses), the reverse charge mechanism shifts the VAT obligation to the buyer

Here’s what makes this complex at scale: if you have customers across all 27 EU states, you’re theoretically dealing with 27 different VAT rates, and in some countries, multiple rates depending on product type. An e-book might get a reduced rate; a SaaS subscription gets the standard rate. Always.

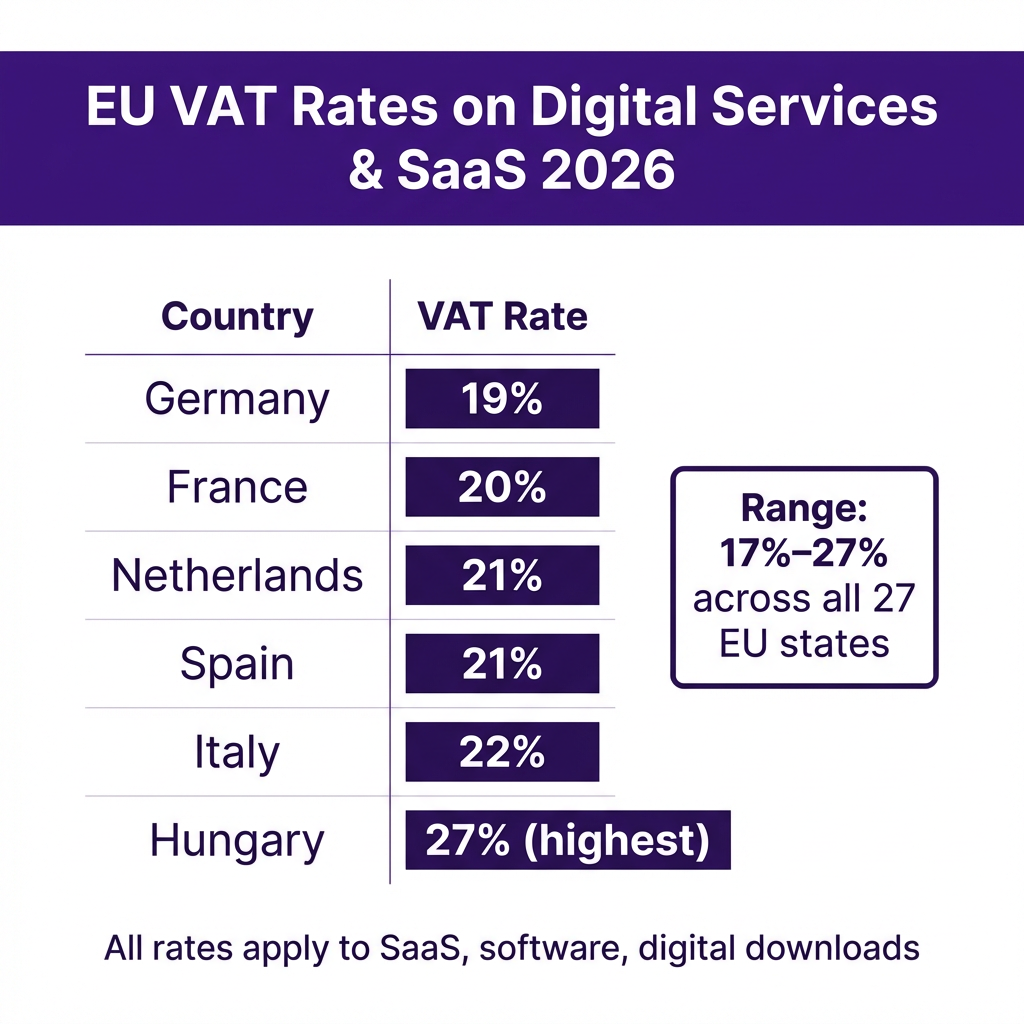

EU VAT Rates for Digital Services in 2026: The Full Breakdown

SaaS and digital services are taxed at each country’s standard VAT rate. There are no reduced rates for software. Here are the key markets:

| Country | Standard VAT Rate | Rate for SaaS/Digital | Notes |

|---|---|---|---|

| 🇱🇺 Luxembourg | 17% | 17% | Lowest in the EU |

| 🇲🇹 Malta | 18% | 18% | Second lowest |

| 🇩🇪 Germany | 19% | 19% | Largest EU economy |

| 🇨🇾 Cyprus | 19% | 19% | Popular for EU company formation |

| 🇫🇷 France | 20% | 20% | E-books get 5.5% reduced rate |

| 🇦🇹 Austria | 20% | 20% | — |

| 🇧🇬 Bulgaria | 20% | 20% | — |

| 🇸🇰 Slovakia | 20% | 20% | — |

| 🇪🇸 Spain | 21% | 21% | Third largest EU economy |

| 🇳🇱 Netherlands | 21% | 21% | Major tech hub |

| 🇧🇪 Belgium | 21% | 21% | E-books at 6% |

| 🇨🇿 Czech Republic | 21% | 21% | Uses Czech koruna |

| 🇱🇻 Latvia | 21% | 21% | — |

| 🇱🇹 Lithuania | 21% | 21% | — |

| 🇵🇹 Portugal | 23% | 23% | — |

| 🇮🇪 Ireland | 23% | 23% | Popular OSS registration country |

| 🇸🇮 Slovenia | 22% | 22% | — |

| 🇮🇹 Italy | 22% | 22% | E-books/e-newspapers at 4% |

| 🇪🇪 Estonia | 22% | 22% | Raised from 20% in Jan 2024 |

| 🇬🇷 Greece | 24% | 24% | — |

| 🇵🇱 Poland | 23% | 23% | — |

| 🇷🇴 Romania | 19% | 19% | — |

| 🇸🇪 Sweden | 25% | 25% | — |

| 🇩🇰 Denmark | 25% | 25% | No reduced rates at all |

| 🇨🇷 Croatia | 25% | 25% | Joined the euro in 2023 |

| 🇫🇮 Finland | 25.5% | 25.5% | Raised from 24% in Sep 2024 |

| 🇭🇺 Hungary | 27% | 27% | Highest VAT rate in the EU |

The range from 17% (Luxembourg) to 27% (Hungary) isn’t academic. On a €100 subscription, that’s the difference between charging €117 and €127. At scale, your pricing strategy and margin calculations have to account for this — unless someone else handles it automatically.

When You Must Register: The €10,000 Threshold and Non-Union OSS

There’s a €10,000 annual revenue threshold that gives small sellers some breathing room. If your total B2C sales to EU customers are below €10,000 per year, you can apply your home country’s VAT rate (if EU-based) instead of tracking destination rates.

Once you cross that threshold — or if you’re a non-EU business selling to EU consumers at all — you need to comply with destination-based VAT rules.

The EU set up the One Stop Shop (OSS) system specifically to simplify this:

- Union OSS — for EU-based businesses. Register once in your home country, file a single quarterly return covering all EU sales, remit to your home tax authority who distributes to other countries.

- Non-Union OSS — for non-EU businesses. Pick any EU country (Ireland is popular), register there, file quarterly returns covering all EU B2C sales. Ireland tends to be chosen for its English-language administration and business-friendly environment.

Sounds manageable, right? In theory. In practice, here’s what OSS compliance actually requires:

- Collecting and storing customer location evidence (IP address, billing address, bank country — you need at least 2 matching data points)

- Applying the correct VAT rate for each transaction in real time

- Issuing VAT-compliant invoices (specific format requirements per country)

- Filing quarterly OSS returns with accurate country-by-country breakdowns

- Maintaining 10 years of transaction records

- Monitoring for rate changes across 27 countries

For a two-person indie SaaS team, that’s a part-time job. For a growing company, it’s a dedicated hire or an expensive accountant.

ViDA: The Coming Wave of Digital Compliance Requirements

The EU’s VAT in the Digital Age (ViDA) package is the biggest overhaul of EU VAT in decades. Passed in 2024, it’s being phased in through 2030. Here’s what’s coming:

| ViDA Pillar | What It Means | Timeline |

|---|---|---|

| Digital Reporting Requirements (DRR) | Real-time digital reporting for cross-border B2B transactions; e-invoices must be issued within 10 days of the transaction | From January 2027 |

| Platform Economy Rules | Digital platforms (marketplaces) become deemed suppliers responsible for collecting VAT on sales made through their platform | From July 2028 |

| Single VAT Registration | Extension of OSS to cover more transaction types; goal is one registration covering all EU obligations | Phased 2027–2030 |

For platform businesses and SaaS companies selling through marketplaces, ViDA is a fundamental shift. The platform becomes the Merchant of Record in more scenarios. For direct-to-consumer SaaS, it adds e-invoicing obligations and tighter reporting windows.

The practical takeaway: EU VAT compliance is getting more complex, not less. Doing it yourself is going to cost more in compliance infrastructure over time, not less.

What Happens If You Get It Wrong

EU VAT non-compliance isn’t just a paperwork issue. The consequences are concrete:

- Back taxes + interest: You owe the full VAT that should have been collected, even if you didn’t charge it to customers

- Penalties: Country-specific, but commonly 10–150% of the owed tax

- Forced VAT registration: Tax authorities can require registration in specific countries if they detect sales activity

- Audit risk: EU tax authorities now share data under the DAC7 framework — if one country finds you, others may follow

- Blocked payments: Some payment processors and banks will flag accounts discovered to be non-compliant

The classic founder mistake is to think “I’m too small for the EU to care about.” That’s changing fast. EU tax authorities have invested heavily in data-sharing systems, and they’re systematically identifying non-compliant digital sellers — starting with the biggest, but working down the stack.

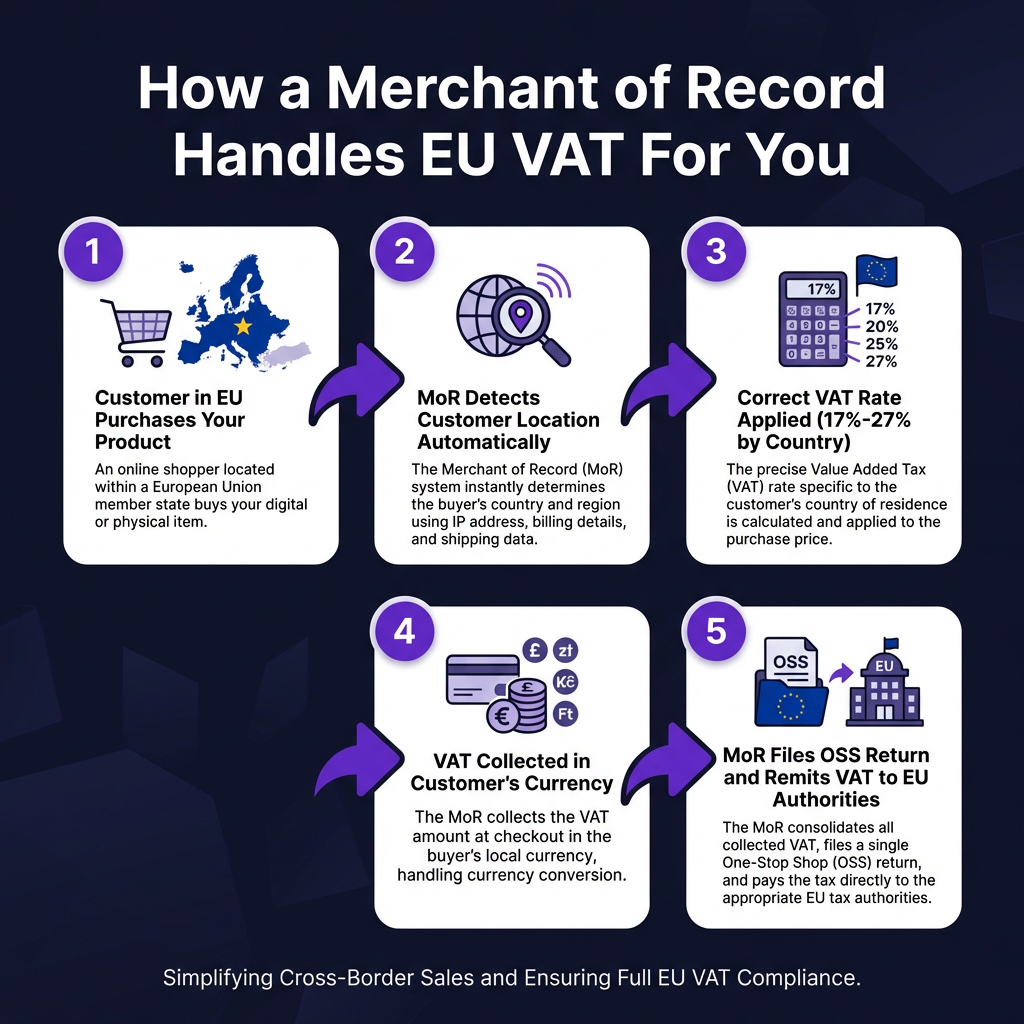

How a Merchant of Record Eliminates EU VAT Complexity

A Merchant of Record (MoR) is a company that acts as the legal seller of record for your product. They buy it from you (at wholesale) and resell it to your customer. Because they’re the seller, they’re responsible for:

- VAT collection and remittance in every jurisdiction

- Tax compliance and registration

- Invoicing requirements

- Chargebacks and payment disputes

For EU VAT specifically, this means:

- The MoR detects your customer’s location automatically (IP + billing data)

- The correct VAT rate gets applied at checkout — no manual rate table

- VAT-compliant invoices are issued automatically

- The MoR files OSS returns quarterly and remits to EU authorities

- You never touch EU VAT filings, registrations, or audits

When ViDA’s e-invoicing requirements kick in (2027), a good MoR will handle those too. The compliance burden scales with the MoR’s infrastructure, not yours.

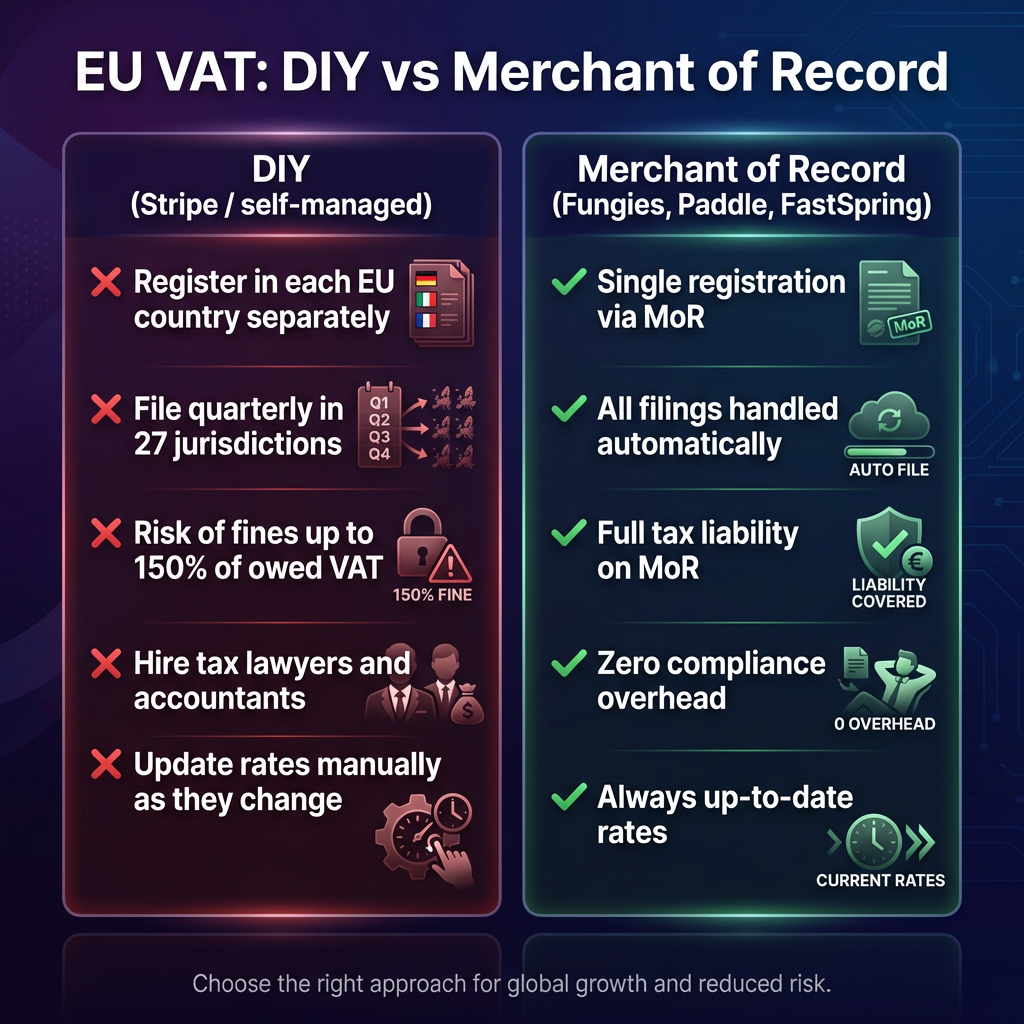

MoR Comparison: EU VAT Handling

| Feature | Fungies | Paddle | FastSpring | Gumroad | DIY (Stripe) |

|---|---|---|---|---|---|

| Full MoR for EU VAT | ✅ Yes | ✅ Yes | ✅ Yes | ⚠️ Partial | ❌ No |

| OSS Filing Handled | ✅ Yes | ✅ Yes | ✅ Yes | ⚠️ Partial | ❌ Your responsibility |

| Destination VAT rate auto-applied | ✅ Yes | ✅ Yes | ✅ Yes | ⚠️ Limited | ❌ Build it yourself |

| B2B reverse charge support | ✅ Yes | ✅ Yes | ✅ Yes | ❌ No | ❌ Build it yourself |

| VAT invoices auto-generated | ✅ Yes | ✅ Yes | ✅ Yes | ⚠️ Basic | ❌ Build it yourself |

| ViDA-ready (2027+) | ✅ Yes | ✅ Yes | ✅ Yes | ❌ Unknown | ❌ Your problem |

| Monthly fee | $0 | $0 | $0 | $0 | $0 + compliance cost |

| Transaction fee | ~5% | 5%+ | 8.9%+ or $500/mo | 10% | 2.9% + tax lawyer fees |

The hidden cost of DIY is real. Between Stripe fees, a tax compliance tool like Avalara or TaxJar (typically $100–$500/month), and the accounting overhead, most companies end up paying more than MoR fees — without the liability protection.

B2B vs B2C: The Rule That Saves You Money

Not every EU sale triggers a VAT obligation on your end. The reverse charge mechanism applies to B2B transactions:

- If your customer is a registered EU business and provides their VAT number, they handle the VAT via reverse charge

- You issue a zero-VAT invoice noting “reverse charge applies”

- No VAT remittance needed from your side

This matters practically: SaaS companies selling to other businesses (SMBs, enterprises, developers) may find that a large portion of their EU revenue is B2B — which simplifies compliance significantly. The complication is accurately distinguishing B2B from B2C at checkout and validating EU VAT numbers in real time via the VIES system.

A good MoR handles VIES validation automatically. DIY means building the integration or paying for a service that does it.

Country-Specific Wrinkles That Will Catch You Off Guard

Even with OSS, some situations require direct country registration:

- You hold inventory in a warehouse in Germany or France → separate VAT registration required regardless of OSS

- You sell B2C in France above certain thresholds → French-specific invoicing rules may apply

- You have employees or a fixed establishment in Poland → you may be considered locally established, affecting OSS eligibility

- Hungary → has mandatory e-invoicing (Online Számla system) that predates ViDA, with its own integration requirements

- Italy → Sistema di Interscambio (SdI) for e-invoicing is already live and mandatory for B2B; increasingly relevant for cross-border

These edge cases are exactly where you need either a local tax advisor or a MoR that’s already navigated them across thousands of customers.

Key Takeaways

- EU VAT applies to you from your first EU sale if you’re non-EU; if you’re EU-based, it applies after €10,000 in EU B2C revenue annually

- Rates range from 17% to 27% and SaaS always gets the standard rate — never reduced

- OSS simplifies multi-country compliance but still requires significant ongoing operational effort: location tracking, invoice generation, quarterly filing

- ViDA is coming: mandatory e-invoicing and real-time digital reporting arrive between 2027 and 2030 — compliance complexity is increasing, not decreasing

- A Merchant of Record eliminates all of this: they’re the legal seller, they collect and remit VAT, they handle invoicing, they file OSS returns — you get a net revenue payment and zero EU tax exposure

FAQ

Do I need to register for EU VAT if I’m based outside the EU?

Yes — if you’re selling digital services (SaaS, software, digital downloads) to EU consumers (B2C), you must comply with EU VAT rules from your very first sale. There’s no minimum threshold for non-EU businesses selling digital services. You register via the Non-Union OSS scheme in any EU member state of your choice.

What counts as “digital services” for EU VAT purposes?

SaaS subscriptions, software licences and downloads, e-books and digital publications, online courses (when pre-recorded and automated), cloud storage, API access, streaming services (video, music, games), website hosting, and digital templates. Essentially any product or service delivered electronically with minimal human intervention.

Does using a Merchant of Record remove my EU VAT liability completely?

Yes. Because the MoR is the legal seller of record, they bear full tax liability. You’re not collecting VAT from customers, so you have no registration, collection, or remittance obligations. The MoR receives the full amount from the customer (including VAT), remits the VAT to tax authorities, and pays you the net amount. Any audit or compliance issue is the MoR’s problem.

How do I know if my EU customers are B2B or B2C?

The standard method is to ask for a VAT number at checkout. If the customer provides a valid EU VAT number (verifiable in real time via the EU’s VIES system), treat them as B2B and apply reverse charge — zero VAT on your invoice. If no VAT number is provided, treat as B2C and apply destination-country VAT. A good MoR or checkout tool handles VIES validation automatically.

Don’t Let EU VAT Be the Compliance Tax You Pay Forever

EU VAT on digital services isn’t going away and it’s not getting simpler. ViDA is adding new reporting layers. Tax authorities are getting better at detecting non-compliant sellers. The cost of DIY compliance — in time, money, and legal risk — keeps rising.

The founders who move fast in Europe are the ones who’ve delegated this entirely. They signed up with a Merchant of Record, embedded the checkout in an afternoon, and spent zero hours on OSS filings. Their competitors are still updating spreadsheets.

If you’re selling digital products or SaaS to EU customers, start with Fungies — zero monthly fees, full MoR coverage including EU VAT, and a checkout that handles location detection, rate application, and invoice generation automatically. You focus on the product; we handle the tax authorities.

References

- EU VAT Rates 2026: Complete Guide to All 27 Countries for Digital Services — PayTaxFast

- European VAT 2026: What Digital Cross-Border Businesses Need to Know — Nexway

- VAT OSS Schemes: Simplify EU Compliance & Grow Faster 2026 — Hellotax

- Digital Services VAT Rules Tighten Globally from 2026 — Global VAT Compliance

- VAT in the Digital Age (ViDA) — European Commission

- EU’s ViDA in Motion — VATupdate

- Global VAT & GST on Digital Services: Complete Guide — Fonoa

- Do I Need to Register for EU OSS? A Complete Guide (2026) — Toolbox Lab