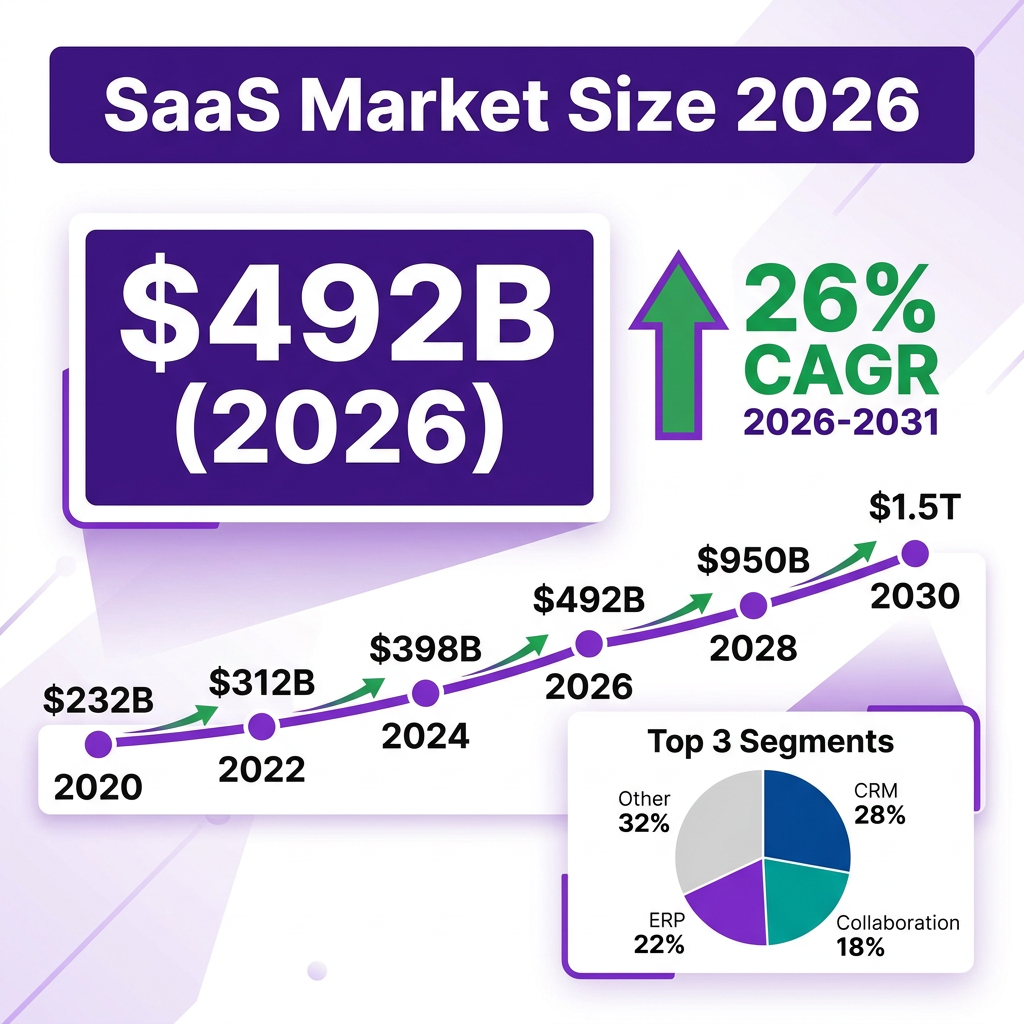

The global Software as a Service (SaaS) market has reached an inflection point in 2026. What started as a niche delivery model for enterprise software has evolved into the dominant paradigm for how businesses consume technology. With the market valued at $492.34 billion in 2026 and projected to grow to $1.58 trillion by 2031 at a compound annual growth rate (CAGR) of 26.24%, SaaS is no longer just a category—it’s the foundation of modern business infrastructure.

This comprehensive analysis draws from over 150 data points across industry reports from Mordor Intelligence, Fortune Business Insights, Precedence Research, OpenView SaaS Benchmarks 2026, and ChartMogul’s Retention Report. We’ll examine market size and growth trajectories, identify the seven trends reshaping the industry, analyze the competitive landscape dominated by tech giants and agile startups, explore the challenges companies face, and forecast where the market is heading through 2030.

Market Overview: The $492 Billion Ecosystem

The SaaS market in 2026 represents one of the most significant technology transformations in business history. According to Mordor Intelligence’s comprehensive analysis, the B2B SaaS market alone was valued at $390 billion in 2025 and has accelerated to $492.34 billion in 2026. This isn’t just incremental growth—it’s a fundamental restructuring of how organizations acquire, deploy, and manage software.

The market’s evolution follows a predictable yet explosive trajectory. Fortune Business Insights reports that the global SaaS market reached $315.68 billion in 2025 and is projected to grow to $375.57 billion by the end of 2026. However, looking at the broader B2B SaaS landscape including specialized vertical solutions and AI-native platforms, the actual addressable market is significantly larger, approaching half a trillion dollars.

What’s driving this growth? Three fundamental shifts are occurring simultaneously. First, enterprise software spending has pivoted decisively toward cloud delivery models. IDC reports that SaaS now commands 72% of all enterprise software spending, up from just 45% in 2020. This represents a permanent shift in procurement preferences that favors subscription-based, cloud-native solutions over traditional on-premise deployments.

Second, the democratization of software development has created an explosion of specialized SaaS solutions targeting narrow verticals. Where enterprises once relied on monolithic ERP systems from SAP or Oracle, they now assemble best-of-breed solutions from dozens of specialized vendors. This fragmentation has expanded the total addressable market while creating opportunities for niche players.

Third, and most significantly, the integration of artificial intelligence into SaaS platforms has created entirely new product categories and expanded use cases. AI-native SaaS companies are raising capital at 40% higher valuations than traditional SaaS, according to VC Mapping data, and AI-powered features are becoming table stakes across every software category.

The geographic distribution of SaaS revenue reveals the market’s maturity curve. The United States remains the dominant market, home to approximately 17,000 SaaS companies and generating an estimated $141.06 billion in SaaS revenue in 2026. North America as a whole accounts for roughly 45% of global SaaS spending, followed by Europe at 28% and Asia-Pacific at 22%. However, emerging markets are growing fastest, with Latin America and Southeast Asia showing 35%+ annual growth rates as digital transformation accelerates.

Looking at the long-term trajectory, Precedence Research forecasts the market reaching $1.37 trillion by 2035, while Mordor Intelligence projects $1.58 trillion by 2031. The difference in these projections reflects varying assumptions about AI adoption rates and the pace of vertical SaaS penetration. What’s consistent across all forecasts is the expectation of sustained high growth—CAGR estimates range from 12.85% to 26.24%, depending on market segment definitions.

Regional Market Analysis

The SaaS market’s growth is not uniform across regions. Understanding geographic variations is essential for companies planning expansion strategies and investors evaluating market opportunities.

North America: The Mature Market Leader

North America, led by the United States, represents the most mature SaaS market globally. With approximately 17,000 SaaS companies and $141.06 billion in projected 2026 revenue, the U.S. accounts for roughly 29% of global SaaS spending. The region’s dominance stems from several factors: early cloud adoption, a robust venture capital ecosystem, and a large base of enterprise customers with sophisticated software needs.

However, maturity brings challenges. Customer acquisition costs in North America are the highest globally, and competition is intense across virtually every software category. Growth for new entrants increasingly depends on vertical specialization or AI-native differentiation rather than horizontal feature competition.

Europe: Privacy-First Innovation

Europe represents approximately 28% of global SaaS spending, with particular strength in privacy-compliant and regulated industry solutions. GDPR and similar regulations have created opportunities for European SaaS companies that build compliance into their core architecture. The Swiss SaaS market alone is projected to reach CHF 4.2 billion by 2026, driven by demand for DSG-compliant AI and localized data residency.

European SaaS companies are also leading in sustainable business practices, with many achieving carbon-neutral operations and incorporating ESG metrics into their reporting. This focus aligns with European corporate values and creates differentiation in the market.

Asia-Pacific: The Growth Engine

Asia-Pacific accounts for 22% of global SaaS spending but is growing at nearly twice the rate of North America. Countries like India, Singapore, and Australia are emerging as significant SaaS markets, while China and Japan represent massive opportunities with unique competitive dynamics.

The region’s growth is driven by rapid digital transformation, increasing cloud adoption among small and medium enterprises, and a growing base of mobile-first users. Mobile SaaS applications are particularly successful in Asia-Pacific, where smartphone penetration exceeds desktop computer usage in many markets.

Latin America and Emerging Markets

Latin America, Southeast Asia, and Africa represent the fastest-growing SaaS regions, with annual growth rates exceeding 35%. These markets are leapfrogging traditional software deployment models, moving directly to cloud-native solutions without the legacy infrastructure that constrains adoption in mature markets.

The key challenge in these markets is payment infrastructure and pricing sensitivity. SaaS companies succeeding in emerging markets typically offer localized pricing, mobile payment options, and freemium models that allow users to derive value before committing to paid subscriptions.

Key Statistics and Data: 25 Numbers That Define SaaS in 2026

Understanding the SaaS market requires diving into the metrics that matter. Here are 25 critical statistics that paint a complete picture of where the industry stands in 2026:

Market Size and Growth

- $492.34 billion — Global B2B SaaS market size in 2026 (Mordor Intelligence)

- $315.68 billion — Global SaaS market size in 2025 (Fortune Business Insights)

- $375.57 billion — Projected SaaS market size for end of 2026 (Fortune Business Insights)

- $1.58 trillion — Projected market size by 2031 (Mordor Intelligence)

- 26.24% CAGR — Growth rate 2026-2031 for B2B SaaS (Mordor Intelligence)

- 18.7% CAGR — Growth rate 2026-2034 (Fortune Business Insights)

- 12.85% CAGR — Conservative growth estimate 2026-2035 (Precedence Research)

- 72% — Share of enterprise software spending now going to SaaS (IDC)

- 17,000 — Number of SaaS companies in the United States

- $141.06 billion — U.S. SaaS revenue projected for 2026

Company Performance Benchmarks

- 26% — Median revenue growth rate for private B2B SaaS companies (OpenView 2026)

- 15% — Median growth rate for bootstrapped SaaS ($3M-$20M ARR) (SaaS Capital 2026)

- 42.3% — 90th percentile growth rate for bootstrapped SaaS (SaaS Capital 2026)

- 101% — Median Annual Net Revenue Retention (NRR) across all private B2B SaaS

- 103% — Median NRR for bootstrapped SaaS companies (SaaS Capital)

- 117.9% — 90th percentile NRR for bootstrapped SaaS

- 91% — Median Gross Revenue Retention (GRR) for bootstrapped SaaS

- 18 months — Median blended CAC payback for $5M-$25M ARR SaaS

- 6.7x — Median public SaaS ARR multiple (SaaS Capital Index, June 2025)

- 3.4x — Median EV/Revenue for SaaS M&A (March 2026)

Churn and Retention

- 3.5% — Median monthly churn rate for B2B SaaS (Artisan Strategies 2026)

- 2.6% — Voluntary cancellation component of median churn

- 0.8-0.9% — Billing failure component of median churn

- 5-7% — Monthly churn for early-stage startups (<$1M ARR)

- 0.5-1% — Monthly churn for enterprise SaaS with large contracts

- 1.8% — Infrastructure SaaS median monthly churn (lowest category)

- 9.6% — EdTech median monthly churn (highest category)

Product-Led Growth Metrics

- 9% — Median free-to-paid conversion across all PLG models

- 12% — Median conversion for freemium products

- 48.8% — Conversion for opt-out free trials (credit card required)

- 280%+ — Increase in enterprise AI adoption (Salesforce CIO Survey)

These numbers reveal a market in transition. Growth rates remain healthy but have normalized from the pandemic-era peaks. The focus has shifted from pure growth to sustainable unit economics, with investors scrutinizing NRR, CAC payback periods, and gross margins more closely than ever. The companies thriving in 2026 are those that have achieved product-market fit, demonstrated efficient customer acquisition, and built durable competitive moats.

Seven Major Trends Shaping SaaS in 2026

The SaaS landscape of 2026 bears little resemblance to the market of even three years ago. Seven interconnected trends are reshaping how software is built, sold, and consumed. Understanding these trends is essential for anyone operating in or evaluating the SaaS space.

The Shift from Growth-at-All-Costs to Efficient Growth

Before diving into the seven trends, it’s important to understand the macroeconomic context that shaped them. The 2021-2022 period of near-zero interest rates and abundant venture capital created a “growth-at-all-costs” mentality where SaaS companies prioritized ARR growth above all other metrics. This era saw companies raising massive rounds at eye-watering valuations based on growth multiples that assumed infinite capital availability.

The interest rate environment of 2023-2024 fundamentally changed this dynamic. As capital became more expensive, investors shifted focus to capital efficiency, path to profitability, and sustainable unit economics. The median public SaaS ARR multiple compressed from 15x+ in 2021 to 6.7x in mid-2025, forcing companies to adapt their strategies.

This shift has had profound implications for how SaaS companies operate. Sales and marketing budgets have been scrutinized, with CAC payback periods becoming a critical metric. Product teams have been tasked with driving expansion revenue from existing customers rather than relying solely on new customer acquisition. And the bar for raising venture capital has risen significantly, with investors requiring clear evidence of product-market fit and efficient growth before committing capital.

The seven trends that follow all reflect this new reality. They represent strategies that work in a capital-constrained environment where efficiency matters as much as growth. Companies that have adapted to this reality are thriving; those that haven’t are struggling to survive.

1. AI-Native Architecture Becomes Default

The most significant shift in SaaS is the transition from “AI-powered” features to AI-native architectures. In 2026, leading SaaS products aren’t adding AI as a bolt-on capability—they’re being built from the ground up with artificial intelligence as the core processing layer. This represents a fundamental architectural change comparable to the shift from desktop to cloud.

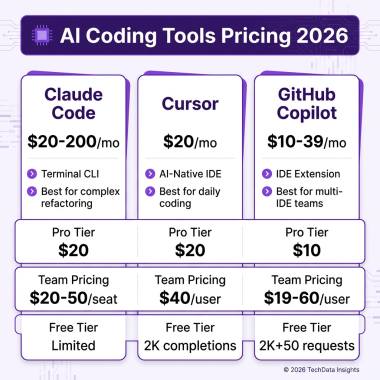

Salesforce’s CIO Survey reveals that enterprise AI adoption has jumped over 280%, with “agentic” AI—multi-agent systems that can act autonomously rather than just respond to prompts—identified as a core 2026 priority. Companies like Cursor, the AI code editor from Anysphere, exemplify this trend. Cursor crossed $500 million ARR by mid-2025 and hit $2 billion ARR by February 2026, making it the fastest SaaS company to reach those milestones.

The implications are profound. AI-native SaaS companies are raising capital at 40% higher valuations than traditional SaaS, according to VC Mapping data. Median Series B valuations for AI-powered SaaS hit $175 million in Q3 2025—a 38% year-over-year increase. For incumbent vendors, this creates an existential challenge: retrofit AI into legacy architectures or risk displacement by native competitors.

2. Vertical SaaS Reaches Critical Mass

Horizontal SaaS—products designed to serve any industry—still dominates by revenue, but vertical SaaS—solutions built for specific industries—is growing twice as fast. The vertical SaaS market is projected to reach $157.4 billion by 2025 with a 23.9% CAGR, roughly double the pace of many horizontal segments.

This trend reflects a maturation of the market. As generic solutions have saturated common use cases, opportunities have emerged in specialized domains. Healthcare vertical SaaS leads with 28% projected year-over-year growth, driven by AI-driven telemedicine platforms and regulatory compliance tools. Other hot verticals include construction, legal services, agriculture, and logistics.

The Swiss market illustrates this trend clearly. Scalemetrics reports that 60% of Swiss SMEs now adopt vertical SaaS solutions tailored to specific industries like MedTech and Engineering, with CHF 4.2 billion projected Swiss SaaS market value by 2026. Vertical solutions offer deeper functionality, better compliance, and more relevant workflows than their horizontal counterparts.

3. Product-Led Growth Evolves Into Full-Stack GTM

Product-led growth (PLG) has evolved beyond the simple “freemium” or “free trial” models of the early 2020s. In 2026, the most successful SaaS companies operate full-stack go-to-market engines that combine self-serve product adoption with sales-assisted motions, AI-driven onboarding, and usage-based expansion.

The data supports this evolution. Median free-to-paid conversion sits around 9% across all PLG models, but there’s significant variation: freemium products convert at 12%, while opt-in free trials convert at 18.2% and opt-out trials (requiring credit card) at 48.8%. The winning strategy isn’t choosing one model—it’s orchestrating multiple pathways based on customer segment and use case complexity.

With 81% of B2B buyers making vendor decisions before engaging sales teams, according to Rev-Geni research, the product experience has become the primary marketing channel. Companies are investing heavily in product analytics, in-app guidance, and self-service enablement to capture this demand.

4. Usage-Based Pricing Goes Mainstream

The subscription model that defined SaaS for two decades is being supplemented—and in some cases replaced—by usage-based pricing. Customers increasingly prefer to pay for what they consume rather than commit to fixed recurring fees. This trend is particularly strong in infrastructure, API-based services, and AI-powered tools where consumption can vary dramatically.

Dynamic pricing in SaaS billing is more popular than ever, according to Tridens Technology’s industry analysis. Companies are implementing sophisticated metering, tiered pricing, and hybrid models that combine base subscriptions with usage overages. This flexibility improves conversion rates and reduces churn by aligning costs with value received.

The challenge for vendors is building billing infrastructure capable of handling complex usage calculations, real-time metering, and flexible pricing models. This has created a sub-market of billing infrastructure SaaS companies that serve other SaaS vendors.

5. API-First and Embedded Platforms

The line between SaaS and infrastructure is blurring as more companies expose their core functionality through APIs. API-first SaaS products are designed to be embedded within other applications rather than used as standalone tools. This “SaaS as infrastructure” model enables developers to add sophisticated capabilities—payments, communications, analytics, AI—without building from scratch.

This trend is accelerating the fragmentation of the SaaS market. Instead of buying monolithic suites, companies are assembling best-of-breed solutions through APIs. The result is a more dynamic competitive landscape where switching costs are lower and innovation cycles are faster.

6. Embedded Finance and Fintech Integration

Financial services are being embedded directly into SaaS platforms across every industry. Whether it’s payments, lending, insurance, or banking, SaaS companies are finding ways to incorporate financial products into their core offerings. This trend, often called “embedded finance,” represents a significant revenue expansion opportunity.

For B2B SaaS specifically, this means offering payment processing, revenue-based financing, or expense management as part of the core product. Companies like Stripe, Mercury, and Brex have built substantial businesses around this model, and traditional SaaS vendors are following suit.

7. Capital Efficiency Over Growth-at-All-Costs

The venture capital environment of 2026 looks very different from 2021. Investors have shifted focus from pure growth to capital efficiency and path to profitability. GP Bullhound’s survey of 100+ European SaaS companies reveals that €50M+ ARR leaders are hitting 28% EBITDA margins while sub-€25M cohorts accelerate growth—signaling disciplined scaling over expansion-at-all-costs.

This shift has profound implications for SaaS operators. The “blitzscaling” playbook of raising massive rounds to fund aggressive customer acquisition has been replaced by a focus on unit economics, sustainable growth rates, and efficient capital deployment. Companies that can demonstrate strong NRR, reasonable CAC payback periods, and clear paths to profitability command premium valuations.

Key Players and Competitive Landscape

The SaaS competitive landscape in 2026 is characterized by a few dominant platform players, a growing ecosystem of vertical specialists, and an increasingly crowded mid-market. Understanding the competitive dynamics requires examining both the established giants and the emerging challengers reshaping the industry.

The Platform Giants

Microsoft maintains its position as the overall leader in enterprise SaaS, leveraging its dominance in productivity (Microsoft 365), collaboration (Teams), and cloud infrastructure (Azure). The company’s comprehensive platform strategy—integrating SaaS applications with infrastructure and AI capabilities—creates powerful network effects that are difficult for competitors to overcome.

Salesforce remains the dominant force in CRM, generating $41.5 billion in FY2026 revenue and holding 20.7% of the global CRM market according to IDC. The company’s CRM revenue alone—$21.6 billion—exceeds the combined CRM revenue of Microsoft, Oracle, Adobe, and SAP. Salesforce’s strategy of expanding beyond CRM into platform services, AI (Einstein), and industry clouds has created a formidable ecosystem.

Adobe has successfully transitioned from perpetual license software to SaaS, with its Creative Cloud and Experience Cloud businesses driving consistent growth. Oracle and SAP, while slower to embrace cloud delivery, remain significant players particularly in enterprise ERP and database markets. Both companies are investing heavily in AI to modernize their offerings.

Google continues to build its SaaS presence through Google Workspace and Google Cloud Platform, though it trails Microsoft in enterprise adoption. Workday dominates HR and finance SaaS for large enterprises, while ServiceNow has established itself as the platform of choice for IT service management and workflow automation.

Emerging Challengers and AI-Native Players

While the giants dominate by revenue, the most interesting competitive dynamics are occurring at the edges. AI-native companies like Cursor, Anthropic, and OpenAI are creating entirely new categories and threatening to disrupt established players. Cursor’s trajectory from launch to $2 billion ARR in under two years demonstrates the potential for AI-native products to achieve unprecedented growth rates.

Vertical SaaS specialists are also gaining ground. Companies like Toast (restaurants), Shopify (e-commerce), and Veeva (life sciences) have demonstrated that deep industry focus can create more valuable businesses than broad horizontal approaches. These companies benefit from higher switching costs, better unit economics, and stronger expansion revenue within their target industries.

Market Fragmentation and Consolidation

The SaaS market remains surprisingly fragmented despite the presence of giants. According to Synergy Research Group, no single vendor dominates across all segments, with different leaders in collaboration, CRM, ERP, HCM, and other categories. This fragmentation creates both opportunity and challenge—opportunity for specialized vendors to carve out profitable niches, challenge for buyers trying to manage complex SaaS portfolios.

Consolidation is occurring simultaneously. Private equity firms are actively rolling up smaller SaaS companies, particularly in fragmented verticals. The median EV/Revenue multiple for SaaS M&A has stabilized around 3.4x as of March 2026, down from the peaks of 2021 but still representing healthy valuations for quality assets.

Challenges and Pain Points

Despite the market’s growth, SaaS companies face significant challenges in 2026. These pain points represent both risks for operators and opportunities for vendors building solutions to address them.

The SaaS Valuation Reset and Its Implications

The most significant challenge facing SaaS companies in 2026 is the valuation reset that occurred between 2022 and 2025. During the pandemic-era boom, SaaS companies traded at median revenue multiples of 15-20x, with high-growth companies commanding 30x+ multiples. These valuations assumed perpetual low interest rates and unlimited capital availability.

As interest rates normalized, these assumptions proved faulty. The median public SaaS ARR multiple compressed to 6.7x by June 2025, and while multiples have recovered slightly to around 8-9x in early 2026, they remain well below peak levels. This compression has had cascading effects across the ecosystem.

For public companies, lower multiples mean less valuable equity for acquisitions and employee compensation. For private companies, the public market reset has flowed downstream to venture valuations, making fundraising more difficult and dilutive. And for employees holding stock options, the promise of SaaS wealth creation has dimmed considerably.

The companies navigating this reset most successfully are those that adapted quickly to the new reality. They cut burn rates, focused on path to profitability, and demonstrated that their businesses could generate returns at lower valuation multiples. Companies that clung to the old playbook of growth-at-all-costs have faced existential crises.

1. Customer Retention and Churn

Churn remains the existential threat to SaaS businesses. With median monthly churn at 3.5% for B2B SaaS, companies are losing over a third of their customers annually if they can’t improve retention. The problem is more acute for early-stage companies, with those under $1M ARR experiencing 5-7% monthly churn.

The cost of churn extends beyond lost revenue. High churn rates signal product-market fit problems, increase customer acquisition costs (as you must replace churned revenue before growing), and depress valuations. Companies with NRR above 130% trade at 15-20x forward revenue, while those below 100% struggle at 3-5x multiples.

Addressing churn requires a multi-faceted approach: improving onboarding to accelerate time-to-value, implementing proactive customer success programs, addressing billing failures (which account for 0.8-0.9% of monthly churn), and continuously enhancing product value. The companies winning in 2026 treat retention as a product discipline, not just a customer success function.

2. Rising Customer Acquisition Costs

The median blended CAC payback period for $5M-$25M ARR SaaS companies is 18 months—flat versus Q3 2025 but up from 15 months in 2023. This trend reflects increased competition for attention, higher advertising costs, and more sophisticated buyers who conduct extensive research before engaging vendors.

For companies with long sales cycles or low ACVs, extended CAC payback periods create cash flow challenges. The capital required to fund customer acquisition grows as payback periods extend, making efficient growth more difficult. This dynamic favors companies with strong product-led growth motions that can acquire customers at lower costs.

3. AI Disruption and Competitive Pressure

The rapid pace of AI innovation creates both opportunity and threat. Incumbent SaaS companies face disruption from AI-native competitors who can offer superior capabilities at lower costs. At the same time, integrating AI into existing products requires significant investment and technical expertise.

The “AI wrapper” gold rush of 2024-2025 has officially ended, according to industry observers. Simple AI add-ons are no longer sufficient differentiation. Companies must build genuine AI-native capabilities that deliver unique value to survive.

Opportunities and Growth Strategies

For SaaS companies navigating the challenges of 2026, several high-impact growth strategies have emerged. These approaches leverage current market dynamics to drive sustainable expansion.

1. Land-and-Expand with Product-Led Growth

The most successful SaaS companies in 2026 combine product-led acquisition with sales-assisted expansion. The land-and-expand model—acquiring customers through self-serve channels, then growing revenue through usage expansion, seat upgrades, and cross-sells—delivers superior unit economics compared to traditional sales-led approaches.

Expansion revenue now represents approximately 40% of new ARR for leading SaaS companies. This revenue is more profitable than new customer revenue (no acquisition cost) and signals strong product-market fit. Companies should design their products and pricing to encourage natural expansion as customers derive more value.

2. Vertical Specialization

As horizontal markets saturate, vertical specialization offers a path to differentiation and higher margins. Vertical SaaS companies benefit from deeper customer relationships, higher switching costs, and the ability to charge premium prices for industry-specific functionality.

The playbook is well-established: identify a large but underserved vertical, build deep functionality for that industry’s specific workflows, and expand within the vertical through network effects and industry-specific integrations. Healthcare, construction, legal, and agriculture remain attractive verticals with significant SaaS penetration potential.

3. AI-Native Product Development

Companies that successfully integrate AI into their core product architecture can achieve dramatic improvements in user outcomes and operational efficiency. The key is moving beyond superficial AI features to genuine AI-native capabilities that transform how users work.

Examples include AI agents that can complete entire workflows autonomously, predictive analytics that anticipate user needs, and natural language interfaces that eliminate complexity. Companies should evaluate every product interaction for AI enhancement potential.

Case Studies: SaaS Success Stories from 2026

Real-world examples illustrate how successful SaaS companies are navigating the 2026 landscape. These case studies highlight different strategies for growth, retention, and competitive positioning.

The Common Threads of SaaS Success

Before examining individual case studies, it’s worth identifying the common characteristics that distinguish successful SaaS companies in 2026. Across the winners, several patterns emerge: genuine product-market fit demonstrated by strong NRR, efficient customer acquisition with CAC payback under 18 months, clear differentiation from competitors, and leadership teams that adapted quickly to changing market conditions.

The companies profiled below represent different paths to success—AI-native disruption, capital-efficient bootstrapping, and vertical specialization. Each offers lessons applicable to SaaS operators at various stages and in different market segments.

Case Study 1: Cursor — AI-Native Disruption

Cursor, the AI code editor from Anysphere, represents the most dramatic SaaS success story of 2025-2026. The company crossed $500 million ARR by mid-2025 and reached $2 billion ARR by February 2026—making it the fastest SaaS company to achieve those milestones.

Cursor’s success stems from genuine AI-native architecture. Unlike competitors who added AI features to existing code editors, Cursor was built around AI assistance from the ground up. The product uses large language models to understand code context, predict developer intent, and generate relevant suggestions.

The company’s PLG strategy amplified this product advantage. A viral freemium tier allowed any user to create a basic AI agent for free, with collaborative features unlocked by sharing with team members. This viral loop drove rapid adoption while the product’s genuine utility converted free users to paid plans.

Case Study 2: NeuroFlow AI — From Seed to $100M ARR in 18 Months

NeuroFlow AI demonstrates how AI-native SaaS can achieve extraordinary growth with limited initial capital. The company turned $500,000 in seed funding into $100 million ARR in just 18 months by making AI agents the core product rather than a feature.

NeuroFlow’s strategy focused on a specific use case—automating repetitive business workflows—and delivered measurable ROI from day one. Customers could deploy AI agents to handle tasks like data entry, customer support triage, and report generation, with immediate productivity gains.

The company’s PLG motion included a viral freemium tier that allowed users to create basic agents for free, with advanced features unlocked through team invites. This approach minimized CAC while driving rapid user acquisition.

Case Study 3: EcoTrack Analytics — Bootstrapped Success

Not every SaaS success requires venture capital. EcoTrack Analytics, a bootstrapped sustainability-focused SaaS company, reached $20 million ARR without raising external funding. The company achieved this by weaponizing community-driven customer acquisition in the sustainability niche.

EcoTrack’s strategy focused on building a passionate user community around sustainability reporting and carbon tracking. By providing genuine value through free educational content and community resources, the company built trust and credibility that translated into paid subscriptions.

The case demonstrates that capital-efficient growth remains possible in 2026. With median growth of 15% for bootstrapped SaaS companies, patient founders can build substantial businesses without dilution or the pressure for hypergrowth that comes with VC funding.

Future Outlook and Predictions: 2026-2030

Looking beyond 2026, the SaaS market is positioned for continued transformation. Several key developments will shape the industry through 2030. The next five years will likely see more change than the previous decade, as AI capabilities mature, new delivery models emerge, and the competitive landscape continues to evolve.

For SaaS founders and operators, the key to navigating this future is maintaining adaptability while building durable competitive advantages. The companies that will thrive are those that can balance innovation with execution, growth with efficiency, and ambition with pragmatism.

Market Size Projections

By 2030, the global SaaS market is projected to reach $819.23 billion according to Grand View Research, while Mordor Intelligence’s more aggressive forecast predicts $1.58 trillion by 2031. The difference reflects varying assumptions about AI adoption and vertical SaaS penetration, but all projections indicate sustained high growth.

The market will likely bifurcate into two tiers: AI-native platforms that command premium valuations and traditional SaaS that faces commoditization pressure. Companies that successfully integrate AI into their core architecture will capture disproportionate value, while those that don’t risk margin compression.

Technology Evolution

By 2030, AI agents will handle the majority of routine software interactions. Users will increasingly interact with SaaS platforms through natural language rather than traditional interfaces, with AI systems handling the complexity of underlying functionality. This shift will favor platforms built with AI-native architectures over those retrofitted with AI capabilities.

Edge computing and 5G will enable new categories of SaaS applications that require low latency and real-time processing. Industries like manufacturing, logistics, and healthcare will see particular benefit from edge-enabled SaaS solutions that can process data locally while maintaining cloud connectivity.

Market Structure Changes

Consolidation will accelerate as private equity firms and strategic buyers acquire smaller SaaS companies. The fragmented nature of the market creates opportunities for roll-up strategies, particularly in vertical segments with many small vendors.

At the same time, the barrier to entry for new SaaS companies will continue to fall. Low-code platforms, AI-assisted development, and cloud infrastructure make it easier than ever to launch SaaS products. This dynamic will ensure continued innovation and competitive pressure even as consolidation occurs.

Key Takeaways

- The SaaS market reached $492.34 billion in 2026 and is projected to grow to $1.58 trillion by 2031 at a 26.24% CAGR, representing one of the largest technology market opportunities.

- AI-native architecture is now the default for competitive SaaS products, with AI-native companies raising capital at 40% higher valuations than traditional SaaS.

- Vertical SaaS is growing twice as fast as horizontal, with industry-specific solutions offering deeper functionality and better unit economics.

- Product-led growth has evolved into full-stack GTM engines combining self-serve, sales-assisted, and AI-driven expansion motions.

- Capital efficiency has replaced growth-at-all-costs as the primary investor focus, with NRR, CAC payback, and path to profitability commanding premium valuations.

Sources and Citations

- Mordor Intelligence — B2B SaaS Market Size & Share Analysis 2026-2031

- Fortune Business Insights — Software as a Service (SaaS) Market Report 2026-2034

- Precedence Research — Software As A Service (SaaS) Market Analysis 2026-2035

- OpenView SaaS Benchmarks 2026 — Survey of 1,941 private B2B SaaS companies

- SaaS Capital — 2026 Benchmarking Metrics for Bootstrapped SaaS Companies

- Artisan Strategies — SaaS Churn Rate Benchmarks 2026 (500+ companies)

- Digital Applied — SaaS Marketing Statistics 2026: 150+ Data Points

- Synergy Research Group — Enterprise SaaS Market Rankings Q2 2026

- IDC — Global CRM Market Share Report 2026

- GP Bullhound — European SaaS Survey 2026

- VC Mapping — SaaS Investors & Venture Capital Firms 2026

- Scalemetrics — Top European SaaS Trends 2026

- Tridens Technology — Top 6 SaaS Industry Trends for 2026