Here’s a number that trips up more founders than it should: you collect $12,000 from a customer in January for an annual SaaS subscription, and your accountant tells you that you only recognized $1,000 in revenue that month. Not $12,000. Just $1,000.

That’s ASC 606 in action — and if you don’t understand it, you’ll misstate your financials, confuse investors, and walk into a Series A due diligence process with clean-up work your team didn’t budget for.

This guide breaks down SaaS revenue recognition under ASC 606 in plain language, with real examples from common pricing models, and explains why a Merchant of Record setup changes the math significantly.

What Is Revenue Recognition (And Why It Matters for SaaS)

Revenue recognition is the accounting principle that determines when you can record money as earned revenue in your financial statements. It sounds simple. It isn’t.

The core rule: you recognize revenue when you deliver the service, not when you collect the cash.

For SaaS companies, this creates a consistent challenge. You often collect payment upfront — monthly, annually, or even multi-year — but you deliver the service over time. That gap between cash in and service delivered is where revenue recognition gets complicated, and where ASC 606 provides the framework.

ASC 606 (Accounting Standards Codification 606) is the U.S. GAAP standard issued by the Financial Accounting Standards Board (FASB) in 2014, fully effective since 2019 for private companies. Its international equivalent is IFRS 15, used across the EU and most other jurisdictions. Both follow the same five-step model.

Getting this right isn’t optional. Investors, acquirers, and lenders use GAAP revenue figures. Misstate them — even accidentally — and you’re looking at restatements, audit flags, and lost trust at the worst possible moment.

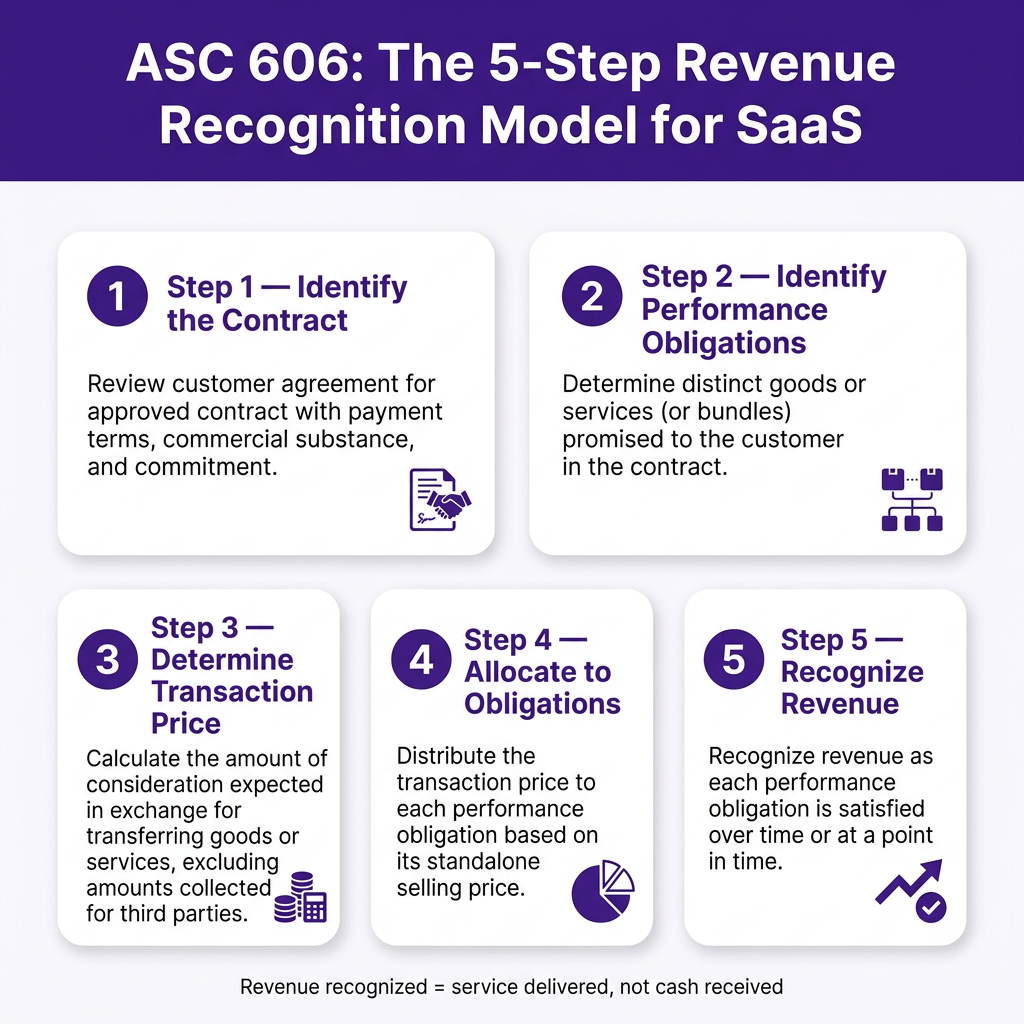

The ASC 606 Five-Step Model, Applied to SaaS

Every dollar of revenue your SaaS business recognizes must flow through this framework:

Step 1: Identify the Contract

For SaaS, this is usually the moment a customer accepts your Terms of Service and a subscription agreement is executed — whether that’s a digital click-wrap, a signed order form, or a self-serve checkout. The contract establishes the commercial relationship and the rights and obligations of both parties.

Step 2: Identify Performance Obligations

A performance obligation is a distinct promise to transfer a good or service. For most SaaS products, the primary obligation is access to the hosted software over the subscription period. But watch out for bundled promises — if you also offer implementation services, dedicated support, or training as part of the deal, those might be separate performance obligations that need to be accounted for independently.

Step 3: Determine the Transaction Price

The transaction price is what you expect to receive in exchange for satisfying your performance obligations. For a simple $99/month plan, that’s $99. For variable pricing (usage-based, overage charges), it gets more nuanced — you’ll need to estimate the likely amount using either an expected value or most-likely-amount approach.

Step 4: Allocate the Transaction Price

If you have multiple performance obligations, you allocate the total price to each based on their standalone selling price. If you sell a subscription for $1,200/year that includes onboarding services you’d normally charge $300 for separately, you allocate roughly 80% ($960) to subscription access and 20% ($240) to onboarding — then recognize each piece on its own timeline.

Step 5: Recognize Revenue as Obligations Are Satisfied

This is the payoff step. You recognize revenue either at a point in time (when control is transferred, like a one-time software license) or over time (like SaaS subscriptions). For subscriptions, revenue is recognized ratably — evenly over the subscription period — because you’re continuously delivering access to the software.

SaaS Revenue Recognition by Pricing Model

The five-step model plays out differently depending on how you price. Here’s how the most common SaaS models work in practice:

| Pricing Model | Example | Revenue Recognition Treatment | Deferred Revenue? |

|---|---|---|---|

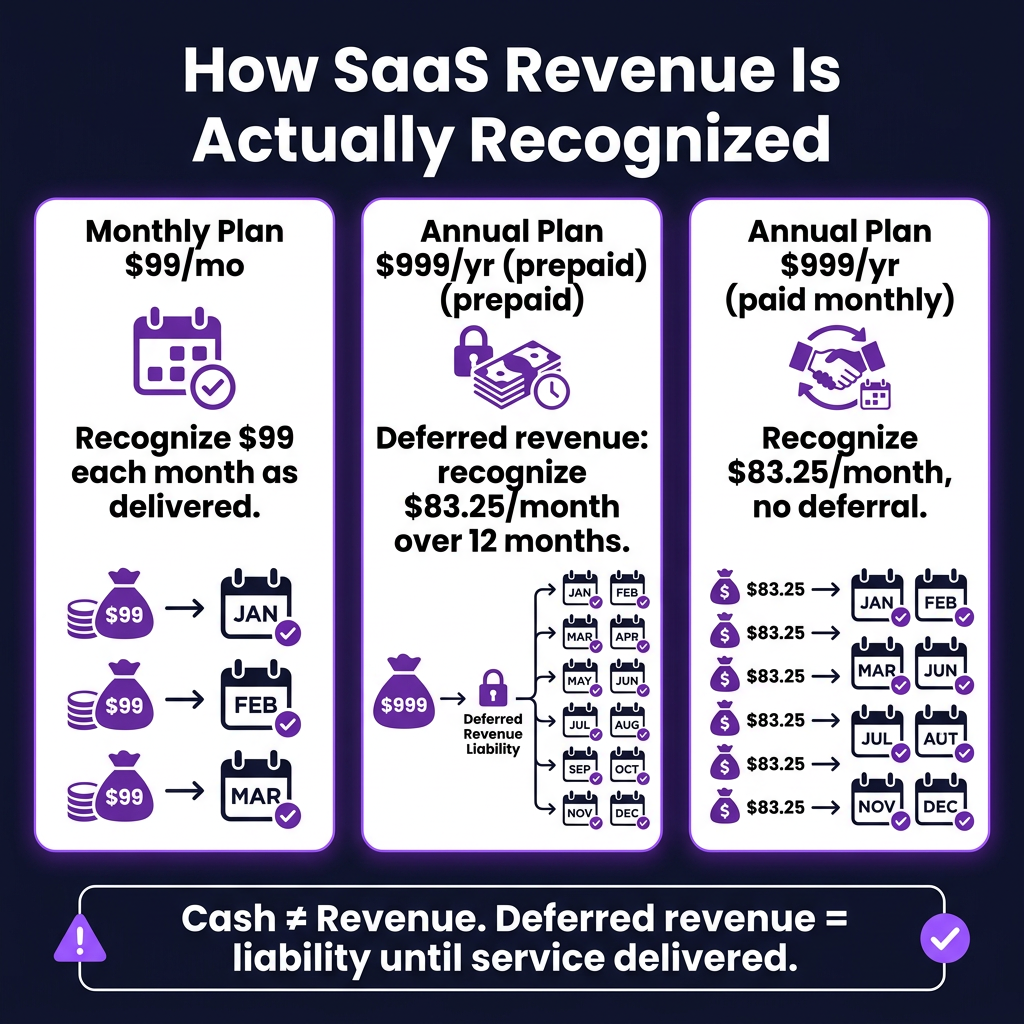

| Monthly subscription | $99/month | Recognize $99 each month as the month passes | No |

| Annual prepaid | $999/year upfront | Recognize $83.25/month over 12 months | Yes — $999 starts as deferred revenue |

| Annual paid monthly | $83.25/month (annual commitment) | Recognize $83.25 each month | No |

| Multi-year deal | $30,000 / 3 years upfront | Recognize $833.33/month over 36 months | Yes — large deferred balance |

| Usage-based | $0.01 per API call | Recognize in period usage occurs | Sometimes — depends on billing cycle |

| Freemium + upgrade | $0 → $49/month mid-month | Recognize pro-rated amount for days of paid service | No |

The annual prepaid model is where most founders trip up. When $11,988 hits your bank account in January, your instinct is to celebrate $11,988 in January revenue. But under ASC 606, that cash is a liability on your balance sheet — called deferred revenue — until you deliver the service each month.

Deferred Revenue: The Liability You’re Glad to Have

Deferred revenue is one of those accounting concepts that feels counterintuitive but makes complete sense once you internalize ASC 606’s logic.

When a customer pays you $999 for a year upfront, you’ve received cash but haven’t yet earned it. You owe them 12 months of software access. Until you deliver those months, the $999 sits on your balance sheet as a current liability under “Deferred Revenue.”

Each month, as you deliver service, you recognize $83.25 as earned revenue and reduce the deferred revenue balance accordingly. By month 12, the deferred revenue balance hits zero and the full $999 has flowed through your income statement.

This matters practically in two scenarios:

- If a customer cancels: You may owe them a refund for the unearned portion — which is exactly what the deferred revenue balance represents. Good accounting makes refund calculations trivial.

- During M&A due diligence: Acquirers look at deferred revenue carefully. A large deferred revenue balance signals committed future revenue — it’s actually a positive signal if the churn is low. But it also signals near-term service delivery obligations they’re buying.

Contract Modifications: The Messy Real-World Scenarios

SaaS customers upgrade, downgrade, add seats, remove seats, and negotiate custom deals mid-contract. Each of these creates what ASC 606 calls a contract modification — and they each require different accounting treatment.

| Scenario | ASC 606 Treatment | Revenue Impact |

|---|---|---|

| Customer upgrades from $99 to $199/mo mid-month | Prospective modification — treat as new contract for remaining term | Recognize pro-rated $199 from upgrade date |

| Annual customer adds 5 seats at $10/seat/mo | Separate performance obligation at standalone price — add-on | Recognize $50/month for new seats from add date |

| Annual customer downgrades to lower tier | Cumulative catch-up or prospective — depends on whether distinct | Adjust recognized amount and deferred revenue balance |

| Enterprise customer renegotiates pricing | Assess if modification or new contract — often treated as combined | Reallocate remaining transaction price |

Most SaaS billing systems handle proration automatically at the operational level. The accounting entries still need to flow correctly into your general ledger — which is why dedicated revenue recognition software becomes critical at scale.

ASC 606 vs IFRS 15: What Changes If You’re Selling Globally

If you’re selling to customers in the EU, UK, or other markets outside the US, the relevant standard is IFRS 15 rather than ASC 606. The good news: they’re largely aligned. Both use the same five-step model and were developed as a joint project by FASB and IASB.

The meaningful differences are narrow but worth knowing:

| Area | ASC 606 (US GAAP) | IFRS 15 (International) |

|---|---|---|

| Variable consideration constraint | Highly probable not to reverse (75–80% threshold) | Highly probable not to reverse (50%+ threshold) |

| Sales with right of return | Recognize expected net amount; refund liability for expected returns | Similar, with some disclosure differences |

| Licenses of IP | More prescriptive bright-line tests for functional vs symbolic IP | More principle-based judgment |

| Practical expedients | Several optional expedients available | Slightly fewer expedients |

| Disclosure requirements | Detailed quantitative disclosures required | Similar but with some differences in disaggregation |

For most SaaS founders doing straightforward subscription billing, these differences won’t materially change how you recognize revenue. They matter more for software companies with complex licensing arrangements or variable consideration at scale.

How a Merchant of Record Simplifies Revenue Recognition

Here’s where things get interesting from a Fungies perspective: the way you accept payments directly affects your revenue recognition complexity.

When you use Stripe directly (or any direct payment processor), you are the merchant of record. That means:

- Every transaction is yours, including chargebacks and refunds

- You must collect and remit VAT/sales tax in every applicable jurisdiction

- Deferred revenue, tax liabilities, and chargeback reserves all sit on your balance sheet

- Your revenue recognition must account for tax gross-ups and then back out tax amounts

When you use a Merchant of Record (MoR) like Fungies.io, the MoR becomes the merchant in each transaction. This creates a meaningfully different accounting picture:

- You receive net proceeds (after fees, tax) from the MoR — cleaner revenue line

- Tax compliance (VAT, GST, sales tax) is the MoR’s responsibility, not yours

- Chargebacks are the MoR’s primary liability — you’re insulated

- Revenue recognition is simpler: you recognize the net amount received as revenue when service is delivered

This doesn’t eliminate ASC 606 compliance — you still need to recognize revenue over the service period, handle contract modifications, and maintain deferred revenue accounting. But it removes entire categories of complexity around tax accounting and payment risk, which typically translates to meaningful reductions in accounting overhead for early-stage companies.

Revenue Recognition Software: What You Need at Each Stage

Spreadsheets work until they don’t. Here’s the honest breakdown of when to graduate to dedicated tooling:

| ARR Stage | Recommended Approach | Tools | Monthly Cost (Est.) |

|---|---|---|---|

| < $500K ARR | Spreadsheet-based deferred revenue schedule | Excel / Google Sheets + QuickBooks | $50–200 |

| $500K–$2M ARR | Light automation with billing system integration | Chargebee, Maxio (starter), Stripe Revenue Recognition | $200–800 |

| $2M–$10M ARR | Dedicated RevRec module with audit trail | Maxio, Chargebee RevRec, LedgerUp | $800–3,000 |

| $10M+ ARR / Pre-IPO | Enterprise-grade RevRec with ASC 606 attestation | Zuora Revenue, NetSuite ARM, Workday Revenue | $3,000–15,000+ |

The transition from spreadsheets to tooling isn’t just about saving time — it’s about creating an audit trail that satisfies external auditors. Series B investors and acquirers will request revenue schedules going back multiple years. If those were built in spreadsheets with manual entries, expect a painful (and expensive) cleanup process.

5 Key Takeaways

- Cash ≠ revenue. Annual prepayments create deferred revenue — a balance sheet liability that converts to earned revenue as you deliver service each month.

- The five-step ASC 606 model applies to every customer contract. Identify the contract, obligations, price, allocate it, then recognize as you perform.

- Contract modifications are the hardest part. Upgrades, downgrades, and seat changes each require careful accounting treatment — automate this as early as possible.

- IFRS 15 and ASC 606 are nearly identical for standard SaaS subscriptions — the differences matter mainly for complex licensing or high-volume variable consideration.

- Merchant of Record simplifies the picture. Using an MoR like Fungies.io removes tax accounting complexity and payment risk, letting you focus on recognizing net revenue correctly rather than managing a tangle of gross-to-net tax adjustments.

Frequently Asked Questions

When does ASC 606 apply to my SaaS startup?

ASC 606 applies to all U.S. entities under GAAP, including private companies. If you’re reporting GAAP financials — which investors and lenders typically require — ASC 606 governs how you recognize revenue. Even if you’re not yet audited, building ASC 606-compliant books from the start saves enormous cleanup costs later.

How does SaaS revenue recognition work with free trials?

Free trials with no payment obligation don’t create a contract for revenue recognition purposes — no money changes hands, so there’s no revenue to recognize or defer. If you offer a free trial that auto-converts to a paid plan (with a credit card on file), revenue recognition begins on the conversion date, not the trial start date.

What’s the difference between MRR and GAAP revenue for SaaS?

MRR (Monthly Recurring Revenue) is an operational metric, not a GAAP number. MRR normalizes all subscription revenue to a monthly figure, regardless of billing frequency. GAAP revenue is what you actually recognize in a given period under ASC 606 — for annual prepaid customers, GAAP revenue for a month equals 1/12 of the annual contract value, which often matches MRR. The difference shows up in multi-year deals, discounts, and variable components.

Does a Merchant of Record change how I recognize revenue?

Yes, meaningfully. With an MoR, you recognize the net amount received (after MoR fees) as revenue when service is delivered. You don’t gross up for taxes because the MoR handles tax collection — they’re the taxpayer, not you. This simplifies your revenue line and removes the need to track and remit VAT/GST in dozens of jurisdictions independently.

Start with the Right Financial Infrastructure

Revenue recognition might not be the most exciting topic in SaaS, but it’s one of the highest-leverage things to get right early. Investors price companies on revenue multiples. Acquirers verify revenue schedules. Lenders base credit facilities on revenue quality.

Getting your ASC 606 setup right — with clean deferred revenue accounting, a traceable recognition schedule, and simplified payment infrastructure — isn’t just accounting hygiene. It’s a competitive advantage when you’re raising or exiting.

If you’re selling software or digital products globally and want to skip the tax complexity that comes with being your own merchant of record, get started with Fungies.io — we handle the payment infrastructure so you can focus on building product and cleaning books you’re proud of.

References

- Maxio — SaaS Revenue Recognition Under ASC 606

- Chargebee — Ultimate Guide to SaaS Revenue Recognition 2026

- Beancount — ASC 606 for SaaS Startups: Five-Step Model & Deferred Revenue

- Trullion — ASC 606 vs IFRS 15: Key Differences

- DualEntry — SaaS Revenue Recognition: A Complete Guide

- FASB — Comparison of Topic 606 and IFRS 15