The European Union is preparing the most significant overhaul of its VAT system in decades. The VAT in the Digital Age (ViDA) reforms, proposed by the European Commission, will fundamentally change how SaaS companies, digital product sellers, and online platforms handle tax compliance across all 27 EU member states. With full implementation scheduled between 2026 and 2030, understanding these changes now is critical for any business selling digital services to European customers.

This comprehensive guide breaks down everything SaaS founders and digital business owners need to know about ViDA — from real-time digital reporting requirements to mandatory e-invoicing and expanded platform liability rules. Whether you’re currently using the One-Stop Shop (OSS) system or handling EU VAT manually, these reforms will impact your operations, compliance costs, and technical requirements.

What Is ViDA? Understanding the VAT in the Digital Age Reforms

ViDA (VAT in the Digital Age) is a comprehensive reform package introduced by the European Commission to modernize the EU’s VAT system for the digital economy. The proposal addresses three critical areas where the current VAT framework, designed decades ago, struggles to keep pace with modern digital commerce:

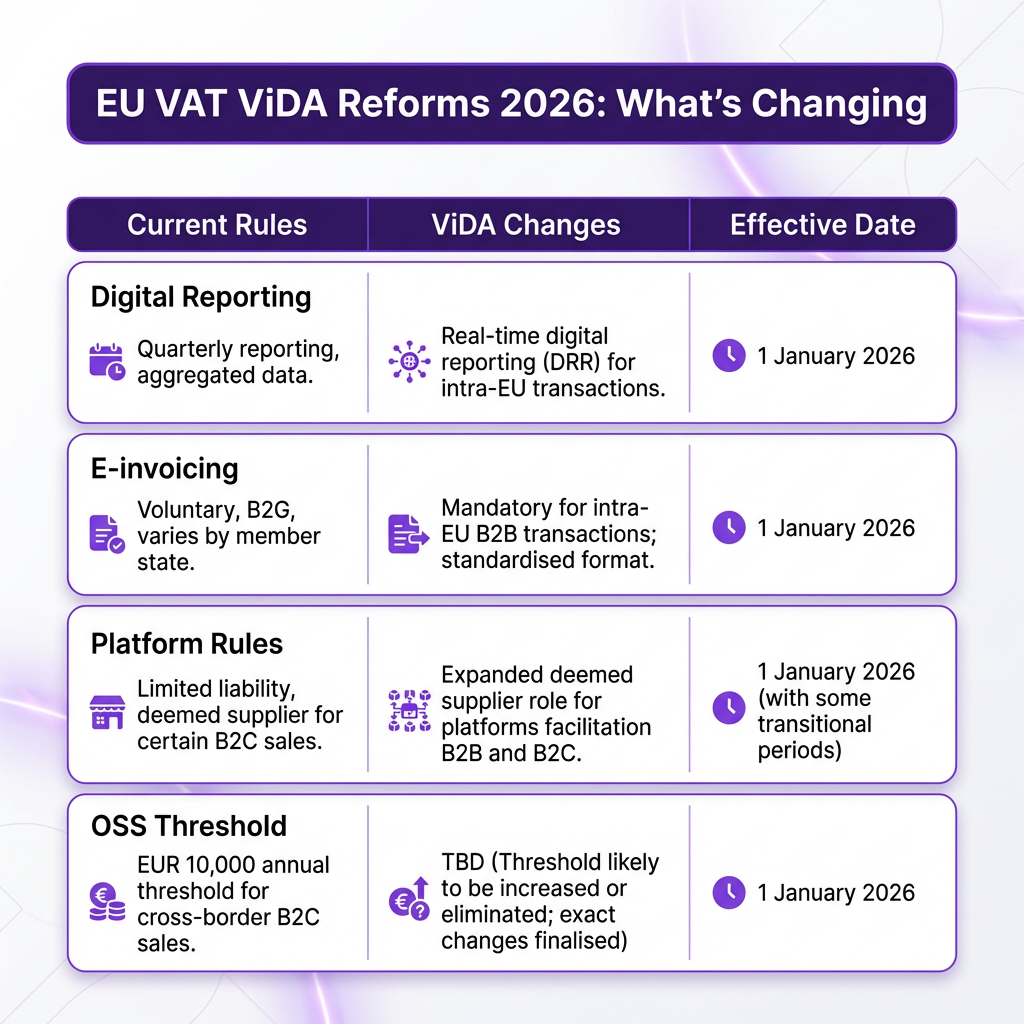

Pillar I: Digital Reporting and E-invoicing — The most significant change for SaaS companies. ViDA mandates structured e-invoices and near real-time transaction reporting for B2B sales across the EU. Instead of quarterly VAT returns, businesses will need to report intra-EU transactions digitally within days of issuance.

Pillar II: Platform Economy and Deemed Supplier Rules — Digital platforms, including SaaS marketplaces and app stores, will face expanded VAT obligations. The reforms strengthen “deemed supplier” rules, making platforms responsible for VAT collection on certain transactions where sellers would otherwise remain unregistered.

Pillar III: Single VAT Registration — ViDA aims to simplify cross-border compliance by expanding the One-Stop Shop (OSS) system and reducing the need for multiple VAT registrations across EU member states. This pillar offers potential relief for businesses currently managing complex multi-country registrations.

How ViDA Changes Digital Reporting for SaaS Companies

Under current EU VAT rules, SaaS companies file quarterly OSS returns summarizing their B2C sales across all EU member states. While this simplified the pre-2021 system, it still creates a reporting lag that tax authorities argue enables fraud and reduces visibility into cross-border transactions.

ViDA’s digital reporting requirements will fundamentally change this process. By 2030, all B2B transactions between EU member states must be reported through real-time digital systems. Here’s what this means in practice:

Structured E-invoicing Becomes Mandatory: ViDA requires businesses to issue structured e-invoices in a standardized format (likely Peppol BIS 3.0 or EN 16931). These aren’t PDFs — they’re machine-readable XML files that tax authorities can process automatically. For SaaS companies billing other businesses, this means integrating e-invoicing capabilities into your billing system or working with a Merchant of Record that handles this complexity.

Near Real-Time Reporting: Instead of waiting until the end of the quarter to report transactions, ViDA requires reporting within days (potentially 2-5 days) of invoice issuance. This “continuous transaction controls” approach, already used in countries like Italy and Poland, gives tax authorities unprecedented visibility into cross-border trade.

Data Standardization Across the EU: Currently, each EU member state has slightly different reporting requirements. ViDA aims to harmonize these standards, creating a single digital reporting framework across all 27 countries. While this reduces complexity long-term, the transition period will require careful attention to evolving technical specifications.

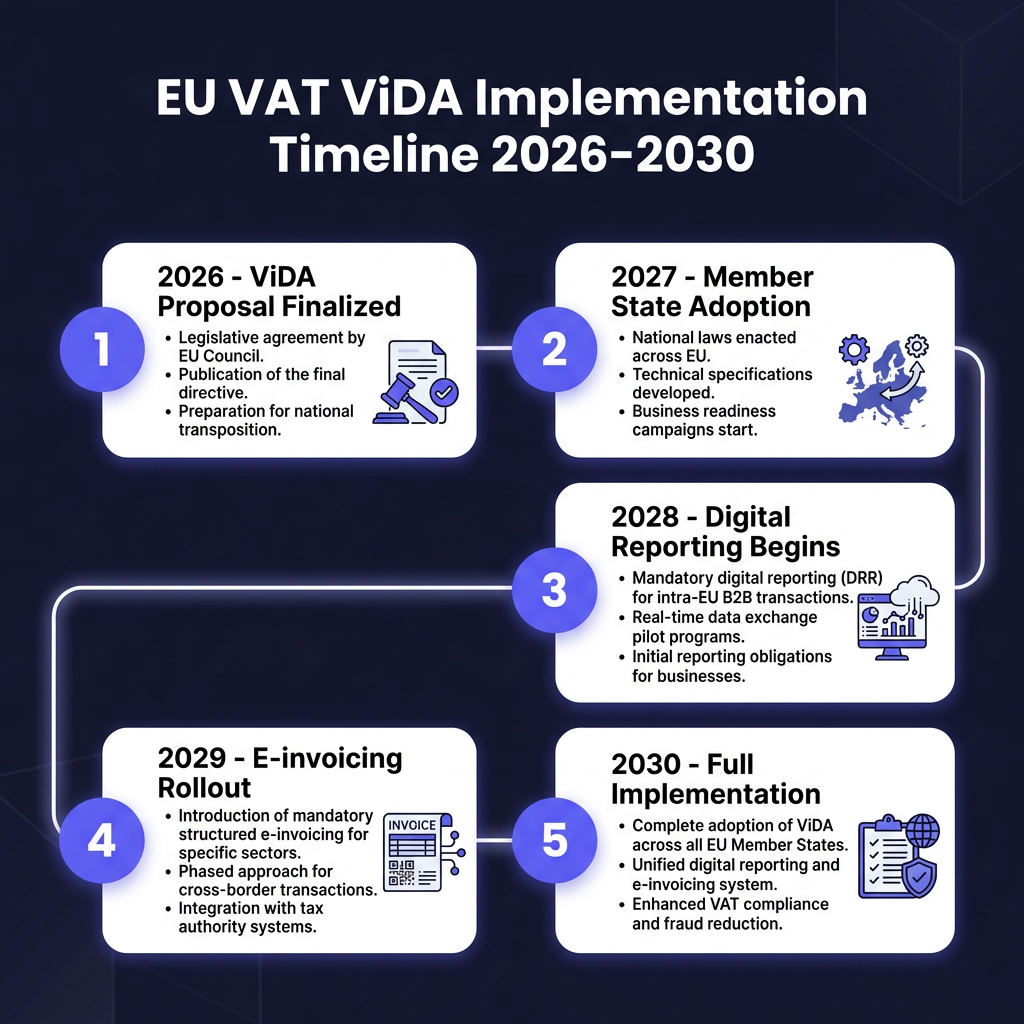

The ViDA Implementation Timeline: When These Changes Take Effect

ViDA isn’t happening overnight. The European Commission has proposed a phased implementation to give businesses and member states time to adapt their systems and processes. Here’s the current expected timeline:

2026-2027: Legislative Adoption — The ViDA proposals must be approved by the European Parliament and Council. Member states then need to transpose the directives into national law. During this period, technical specifications for digital reporting and e-invoicing standards will be finalized.

2028: Digital Reporting Requirements Begin — The first major obligation kicks in. Large enterprises (those above certain turnover thresholds) will need to begin real-time digital reporting for intra-EU B2B transactions. SaaS companies above these thresholds should prepare their systems during 2027.

2029: E-invoicing Rollout — Mandatory structured e-invoicing begins for B2B transactions. This is likely the biggest technical challenge for most SaaS companies, requiring integration with e-invoicing networks like Peppol or working with compliant billing providers.

2030: Full Implementation — All ViDA requirements apply to businesses of all sizes. The expanded OSS system, enhanced platform rules, and complete digital reporting framework become mandatory across the EU.

Platform Economy Rules: What Changes for SaaS Marketplaces

If you operate a SaaS platform that enables third-party sellers — think app stores, plugin marketplaces, or software distribution platforms — ViDA’s platform economy rules directly impact your VAT obligations. The reforms expand “deemed supplier” rules that make platforms responsible for VAT collection in specific scenarios:

Domestic Deemed Supplier Rules: Currently, platforms are only deemed suppliers for cross-border transactions. ViDA extends this to domestic sales when the underlying seller is unregistered for VAT. If your platform enables non-VAT-registered developers to sell to customers in the same country, you may become responsible for collecting and remitting that VAT.

Expanded Platform Categories: The reforms clarify that SaaS marketplaces, software distribution platforms, and digital service intermediaries fall under platform economy rules. If you’re unsure whether your business model qualifies, consult a VAT specialist — the penalties for non-compliance are substantial.

Enhanced Record-Keeping: Platforms will need to maintain detailed records of transactions, seller identities, and VAT treatments. ViDA requires platforms to share this data with tax authorities upon request, creating additional compliance overhead for marketplace operators.

Preparing Your SaaS Business for ViDA Compliance

The technical and operational requirements of ViDA will challenge many SaaS companies, particularly those with custom billing systems or limited compliance resources. Here’s a practical preparation checklist:

Audit Your Current Billing Infrastructure: Can your system generate structured e-invoices in XML format? Does it support real-time reporting APIs? If you’re using Stripe, Paddle, or a Merchant of Record like Fungies.io, verify their ViDA compliance roadmap. Most major providers are already preparing for these requirements.

Review Your EU Customer Base: ViDA’s B2B reporting requirements apply to transactions between EU businesses. If you sell primarily B2C, your immediate obligations may be lighter, but platform rules and OSS changes still matter. Map your customer base by VAT registration status to understand your specific exposure.

Evaluate Your VAT Registration Strategy: ViDA’s expanded OSS system may reduce the need for multiple EU VAT registrations. However, if you have significant B2B sales to specific countries, local registration might still offer advantages. Consult with a VAT advisor to optimize your structure before 2028.

Plan for E-invoicing Integration: Even if you use a third-party billing provider, understand how e-invoice delivery will work. Will invoices be sent through Peppol? Direct API connections? Email with structured attachments? Your enterprise customers will have preferences and requirements.

Simplify Your Global Tax Compliance

Fungies.io handles EU VAT, US sales tax, and 100+ countries automatically — so you can focus on building your SaaS or game.

No credit card required • Merchant of Record included

FAQ: EU VAT ViDA Reforms for SaaS Companies

Does ViDA replace the OSS system?

No, ViDA expands and enhances the One-Stop Shop system. The OSS will remain the primary mechanism for non-EU sellers to handle EU VAT, but with expanded coverage and potentially simplified procedures.

Do ViDA rules apply to non-EU SaaS companies?

Yes. If you sell digital services to EU customers, ViDA’s platform rules and digital reporting requirements apply regardless of where your business is headquartered. Non-EU sellers using the OSS will see expanded reporting obligations.

What happens if I don’t comply with ViDA requirements?

Member states are implementing significant penalties for non-compliance. Late reporting, incorrect e-invoicing, and failure to use approved digital systems can result in fines ranging from €50 to €500 per invoice, plus potential loss of VAT deduction rights for your customers.

Will ViDA increase my compliance costs?

Initially, yes. The technical requirements for e-invoicing and real-time reporting require system upgrades or switching to compliant billing providers. However, the harmonized standards across the EU should reduce long-term complexity compared to managing 27 different national requirements.

How does ViDA affect my existing VAT registrations?

ViDA’s expanded OSS aims to reduce the need for multiple VAT registrations. If you currently hold registrations in several EU countries purely for B2C digital services, you may be able to consolidate these into a single OSS registration. However, B2B transactions with local VAT obligations may still require local registration.

Conclusion: Act Now to Prepare for ViDA

The EU VAT ViDA reforms represent the biggest change to European digital taxation since the introduction of the OSS system in 2021. While full implementation stretches to 2030, the technical requirements — particularly around e-invoicing and real-time reporting — demand preparation starting now.

For SaaS companies, the key decisions center on billing infrastructure and VAT management strategy. Working with a Merchant of Record that handles ViDA compliance automatically can eliminate much of this complexity, allowing you to focus on product development rather than tax technicalities.

Whether you handle VAT in-house or through a provider, start the conversation about ViDA preparation today. The businesses that adapt early will avoid the compliance scrambles and technical debt that inevitably come with waiting until deadlines approach.