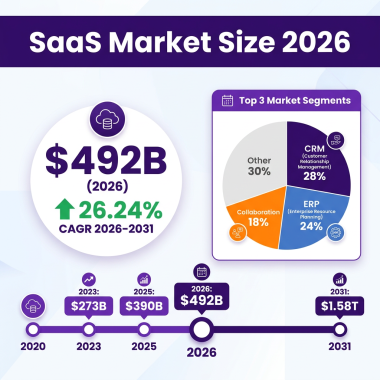

The global Software as a Service (SaaS) market has reached an inflection point in 2026. With the industry now valued at $492.34 billion and projected to nearly triple to $1.58 trillion by 2031, SaaS has evolved from a convenient alternative to on-premise software into the dominant paradigm for enterprise and consumer applications alike. This isn’t just incremental growth—it’s a fundamental restructuring of how software is built, distributed, and consumed across every industry vertical.

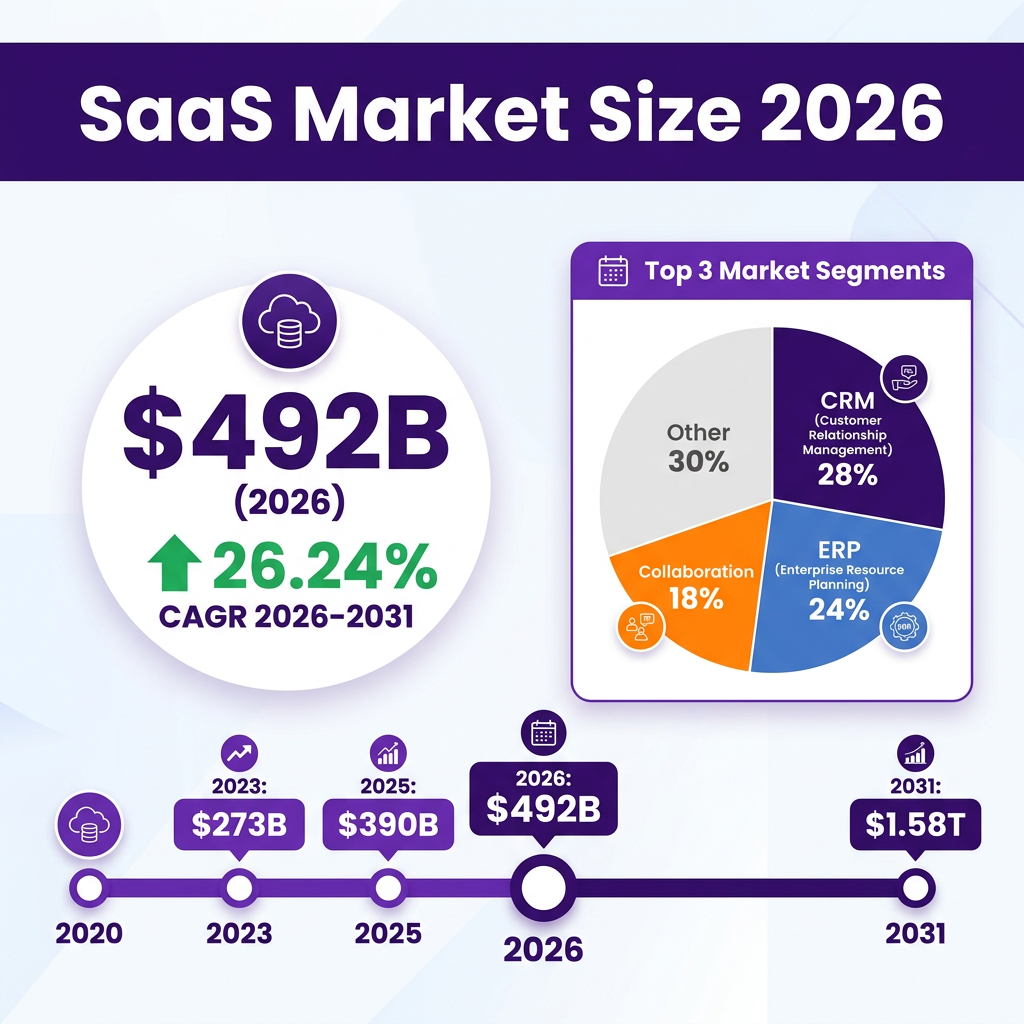

What’s driving this explosive expansion? The convergence of artificial intelligence, cloud infrastructure maturation, and shifting enterprise priorities has created a perfect storm for SaaS adoption. According to Mordor Intelligence, the B2B SaaS market alone is growing at a staggering 26.24% CAGR, making it one of the fastest-growing sectors in the global economy. Meanwhile, AI-native SaaS companies are rewriting the rules of growth—reaching $100M ARR in 18 months, a feat that traditionally took years.

Market Overview: The $492 Billion Ecosystem

The SaaS market’s journey from niche technology to mainstream infrastructure has been remarkable. In 2023, the global market was valued at $273.55 billion according to Fortune Business Insights. By 2025, this figure had grown to approximately $390 billion, and 2026 marks another significant milestone with the market reaching $492.34 billion. This represents a compound annual growth rate that outpaces nearly every other technology sector.

The United States continues to dominate the SaaS landscape, accounting for the largest share of global revenue. The U.S. SaaS market alone is valued at approximately $141.06 billion in 2026, driven by technological advancement, increasing demand for cloud-based solutions, and the ongoing digital transformation across industries. North America as a whole represents roughly 45% of global SaaS spending, followed by Europe at 28% and Asia-Pacific at 18%.

Looking at the competitive landscape, the market remains both concentrated at the top and fragmented across verticals. Microsoft leads the enterprise SaaS market, followed by Salesforce, Adobe, Oracle, and SAP. However, the top 10 vendors collectively control less than 40% of the market, leaving significant room for specialized players and emerging challengers. This fragmentation is particularly pronounced in vertical SaaS, where industry-specific solutions often outperform generalist platforms.

The B2B SaaS segment specifically is experiencing unprecedented growth. Valued at $390 billion in 2025, it’s estimated to reach $492.34 billion in 2026 and soar to $1.58 trillion by 2031. This segment is characterized by higher contract values, longer sales cycles, and greater customer lifetime value compared to B2C SaaS. Enterprise customers are increasingly favoring SaaS solutions for critical business functions including CRM, ERP, HCM, and collaboration tools.

Perhaps most telling is the shift in enterprise software spending. According to IDC, SaaS now commands 72% of all enterprise software spending, up from just 35% in 2019. This shift reflects a fundamental change in how organizations think about software ownership, maintenance, and deployment. The subscription model has proven not just viable but preferable for most use cases, offering predictable costs, automatic updates, and scalability that on-premise solutions cannot match.

Key Statistics and Market Data

Understanding the SaaS market requires diving deep into the numbers that define its scale, growth patterns, and economic impact. Here are the critical statistics that every founder, investor, and enterprise buyer should know in 2026:

Market Size and Growth: The global SaaS market reached $492.34 billion in 2026, up from $390 billion in 2025. This represents year-over-year growth of approximately 26%. The B2B SaaS segment specifically is growing at a 26.24% CAGR and is projected to reach $1.58 trillion by 2031. The broader enterprise SaaS market grew 31% year-over-year to reach nearly $15 billion in quarterly revenues according to Synergy Research Group.

Company Count and Distribution: There are now over 42,000 SaaS companies worldwide, with approximately 12,400 based in the United States. The UK and Canada represent the next largest concentrations with roughly 2,000 and 1,500 companies respectively. This global distribution reflects both the borderless nature of SaaS delivery and the concentration of venture capital in major tech hubs.

Revenue Concentration: The top 25% of SaaS businesses with annual run rates between $1M and $30M grew 62.1% in 2022. However, this is slower compared to 2021 when growth was at 78.9%, indicating some normalization after the pandemic-driven acceleration. SaaS businesses with ARR of $1M or less grew an impressive 139.1% from March 2022 to March 2023, showing strong momentum at the early stage.

AI-Native SaaS Explosion: The AI-Created SaaS market is expected to reach $142.02 billion in 2026 and grow to $1.05 trillion by 2033 at a 39.6% CAGR. AI-native SaaS companies are raising at 40% higher valuations than traditional SaaS. Median Series B valuations for AI-powered SaaS hit $175 million in Q3 2025—a 38% year-over-year increase.

Churn and Retention Benchmarks: Net Revenue Retention (NRR) for best-in-class SaaS companies exceeds 120%, meaning existing customers generate more revenue through expansion than is lost through churn. The median gross revenue retention for SaaS companies is approximately 88%, while net revenue retention sits around 105%. Reducing churn by just 5% can increase profits by 125% according to research from Harvard Business School.

Pricing Model Shifts: Usage-based pricing adoption has accelerated dramatically. According to Zylo’s 2026 SaaS Management Index, 78% of IT leaders report unexpected costs from usage-based or AI features. This pricing model now accounts for 35% of new SaaS contracts, up from just 12% in 2020. The shift reflects both customer preference for pay-for-what-you-use and vendor strategies to capture more value from high-usage customers.

Venture Capital Investment: SaaS remains the deepest category for venture capital investment. Over 1,300 active VC firms focus on SaaS and B2B software investments. Notable firms include Andreessen Horowitz, Bessemer Venture Partners, Insight Partners, and Accel. AI-native SaaS companies are seeing median Series A sizes of $22 million versus $15 million for traditional SaaS, with vertical AI SaaS for healthcare, legal, and financial services raising the largest early-stage rounds.

SaaS Management Market: As SaaS portfolios grow more complex, the SaaS management market is experiencing rapid growth—projected to increase from $4.58 billion in 2025 to $9.37 billion by 2030 at a 15.4% CAGR. This reflects the growing need for tools to manage SaaS sprawl, shadow IT, and compliance risks.

Vertical SaaS Growth: Vertical SaaS—solutions tailored to specific industries—is growing at 45% annually, significantly outpacing horizontal SaaS. Industries like healthcare, agriculture, construction, and legal services are seeing rapid adoption of specialized cloud tools. Veeva Systems (life sciences), Procore Technologies (construction), and Toast (restaurants) exemplify the success of this model.

Major Trends Shaping SaaS in 2026

The SaaS landscape is being fundamentally reshaped by seven major trends that are redefining how software is built, sold, and consumed. Understanding these trends is essential for anyone operating in or evaluating the SaaS market.

1. AI-Native SaaS Becomes the Default

Artificial intelligence is no longer a feature—it is becoming the foundation of modern SaaS products. AI-native SaaS companies are achieving growth rates that were previously unimaginable. Some AI-native software companies reach approximately $3M in annual recurring revenue within their first year and scale to roughly $100M by year four, exceeding typical early-stage SaaS growth timelines. A subset of high-performing AI-native companies achieves approximately $40M in ARR within the first year and exceeds $120M by the second year.

Machine learning represents the largest technology segment in AI-created SaaS, contributing 42.3% of market value in 2026. Natural language processing and computer vision follow, enabling everything from intelligent document processing to automated customer service. The key shift is that AI is moving from experimentation to production-ready platforms—systems that are observable, governable, cost-controlled, and able to operate continuously under real user load.

2. Vertical SaaS Dominates Growth

Vertical SaaS has moved from a niche category to the defining force shaping software growth in 2026. Buyers increasingly demand tools built around the realities of their specific industries rather than generic horizontal solutions. The fastest growth is coming from analog-heavy industries like healthcare, agriculture, construction, legal, and financial services that are rapidly adopting industry-specific cloud tools.

The vertical SaaS model offers several advantages: deeper customer relationships, higher switching costs, embedded fintech opportunities, and better unit economics. Vertical SaaS vendors are also becoming acquirers, expanding within industries by buying complementary tools that deepen critical workflows. This consolidation trend is creating platform companies that serve as operating systems for entire industries.

3. Usage-Based Pricing Goes Mainstream

The shift to usage-based and consumption-based pricing models is one of the most significant changes in SaaS economics. According to Capgemini research, 82% of executives report significant increases in cloud, SaaS, and Gen AI costs tied to these models. While this creates revenue opportunities for vendors, it also introduces cost volatility that replaces the predictable growth of traditional subscription models.

Only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically, creating both a challenge and an opportunity. Vendors who can help customers understand and optimize their usage are winning. This trend is particularly pronounced in AI-powered applications where compute costs scale with usage.

4. AI Agents as Core Product

The most successful SaaS companies in 2026 are not just adding AI features—they are making AI agents the core product. NeuroFlow AI exemplifies this approach, reaching $100M ARR in 18 months by making AI agents the product rather than an add-on. This represents a fundamental shift from software as a tool to software as an autonomous worker.

These AI agents can handle complex workflows, make decisions, and interact with other systems without human intervention. The implications are profound: lower customer effort, higher value delivery, and the potential for entirely new categories of software that were not possible before AI.

5. SaaS Management Becomes Strategic Priority

As SaaS portfolios grow, managing them has become a strategic priority. The rise of SaaS sprawl, Shadow IT, and compliance risks has heightened demand for SaaS spend management, application discovery, and automated access governance. Organizations are transitioning from reactive tracking to proactive SaaS lifecycle management.

Vendors in this space are reporting strong adoption of tools for real-time usage analytics, contract intelligence, and renewal optimization. The SaaS security and governance segment is expected to register the fastest growth with a 24.6% CAGR. This reflects the dual importance of SaaS as both a financial and security consideration.

6. Embedded Fintech Integration

Vertical SaaS companies are increasingly embedding financial services directly into their platforms. This includes payments, lending, insurance, and payroll—creating new revenue streams and deepening customer relationships. The embedded fintech market is growing at 32% CAGR and represents a significant expansion of the traditional SaaS TAM.

For SaaS companies, embedded fintech can increase revenue per customer by 2-5x while improving retention. For customers, it simplifies operations by reducing the number of vendors they need to manage. This trend is particularly strong in vertical SaaS where industry-specific financial workflows can be deeply integrated.

7. API-First and Composable Architecture

Modern SaaS is built API-first, enabling customers to compose solutions that fit their specific needs. This approach allows for deeper integrations, custom workflows, and the ability to embed SaaS functionality into other applications. The API management market is growing at 23% CAGR, reflecting the importance of this architectural approach.

API-first SaaS companies can serve both end-users and developers, expanding their addressable market. They also benefit from network effects as integrations create switching costs and drive retention. This trend is closely related to the rise of workflow orchestration platforms that connect multiple SaaS tools.

Key Players and Competitive Landscape

The SaaS competitive landscape in 2026 is characterized by established giants, fast-growing challengers, and a long tail of specialized players. Understanding this ecosystem is crucial for strategic positioning and investment decisions.

Market Leaders: Microsoft continues to lead the enterprise SaaS market, leveraging its dominance in productivity software (Office 365, Teams) and cloud infrastructure (Azure). The company’s comprehensive suite approach and enterprise relationships create significant competitive moats. Microsoft is followed by Salesforce, which remains the dominant player in CRM despite increased competition.

Adobe has successfully transitioned from perpetual licenses to SaaS, with its Creative Cloud and Experience Cloud businesses driving consistent growth. Oracle and SAP round out the top five, though both face challenges from cloud-native competitors. Notably, Oracle and Google are among the fastest-growing major SaaS vendors.

Emerging Challengers: ServiceNow has emerged as a major enterprise platform, expanding beyond IT service management into workflow automation across the enterprise. Workday dominates HR and finance SaaS for large enterprises. HubSpot has become the go-to platform for SMB marketing and sales, competing effectively with Salesforce at the lower end of the market.

Zoom, despite post-pandemic normalization, remains a critical communication platform. Shopify powers e-commerce for millions of merchants. Atlassian dominates developer tools and team collaboration. These companies have built strong positions in specific domains and are expanding horizontally.

Vertical SaaS Leaders: Veeva Systems has built a $40+ billion business serving the life sciences industry with specialized CRM and data solutions. Procore Technologies dominates construction management software. Toast has revolutionized restaurant operations with its integrated platform. These companies demonstrate the power of vertical focus.

AI-Native Disruptors: A new generation of AI-native SaaS companies is challenging incumbents across categories. Companies like Jasper (AI writing), Copy.ai (marketing content), and Gong (revenue intelligence) have achieved significant scale by leading with AI capabilities. These companies are often reaching $100M ARR faster than their traditional SaaS predecessors.

Market Fragmentation: Despite the concentration at the top, the SaaS market remains highly fragmented. Different vendors lead each major segment: Salesforce in CRM, Workday in HCM, ServiceNow in ITSM, Zoom in video conferencing, Slack in team messaging. This fragmentation creates opportunities for both consolidation and specialized solutions.

Geographic Distribution: While the U.S. dominates SaaS, significant players have emerged from other regions. Europe has produced companies like SAP (Germany), Spotify (Sweden), and UiPath (Romania). Israel is a hotbed of cybersecurity SaaS. Australia has produced Atlassian and Canva. This global distribution reflects both the borderless nature of SaaS and regional strengths in specific domains.

Challenges and Pain Points

Despite the impressive growth, the SaaS industry faces significant challenges that both vendors and customers must navigate. Understanding these pain points is essential for sustainable success.

1. Customer Churn and Retention

Churn remains the existential threat for SaaS businesses. Unlike traditional software where customers made large upfront investments, SaaS customers can cancel with minimal friction. B2B SaaS churn tends to occur at renewal cycles, making losses more strategic and costly given long sales cycles and deep relationship investment.

A SaaS solution with ARR of $10M to $15M can only stay in business for 7.5 months (median) based on current cash reserves if growth stalls. This highlights the importance of maintaining strong retention while scaling. Reducing churn requires excellence across product, customer success, and value demonstration.

2. Rising Customer Acquisition Costs

As the SaaS market matures, customer acquisition costs (CAC) have risen dramatically. Increased competition, platform saturation, and privacy changes have made traditional growth channels more expensive. SaaS companies must now achieve greater efficiency in their go-to-market motions or find alternative acquisition strategies.

Product-led growth (PLG) has emerged as a response to high CAC, allowing companies to acquire customers through free trials and freemium offerings. However, PLG requires significant product investment and does not work for all categories. The most successful companies often combine PLG with sales-assisted and enterprise sales motions.

3. SaaS Sprawl and Management Complexity

Enterprises now use an average of 130+ SaaS applications, creating significant management challenges. SaaS sprawl leads to security vulnerabilities, redundant spending, and compliance risks. Shadow IT—unsanctioned SaaS usage—complicates governance further.

Only 2% of organizations have holistic FinOps teams covering cloud, SaaS, and Gen AI, leaving most companies without adequate visibility and control. This complexity creates opportunities for SaaS management platforms but also represents a barrier to further SaaS adoption in some organizations.

4. AI Cost Volatility

While AI presents enormous opportunities, it also introduces cost volatility that challenges traditional SaaS unit economics. Usage-based AI pricing means costs can spike unexpectedly based on customer behavior. 78% of IT leaders report unexpected costs from usage-based or AI features, creating both customer frustration and vendor margin pressure.

Vendors must develop pricing models that balance accessibility with profitability while helping customers understand and control their costs. This is particularly challenging for AI-native companies where inference costs represent a significant portion of COGS.

Opportunities and Growth Strategies

Despite the challenges, significant opportunities exist for SaaS companies that can execute effectively. Here are the key growth strategies defining success in 2026:

1. Vertical Expansion with Embedded Fintech

The combination of vertical SaaS and embedded fintech represents one of the largest opportunities in software. By adding payments, lending, and other financial services to industry-specific platforms, SaaS companies can dramatically expand their revenue per customer while deepening relationships.

Toast exemplifies this approach, generating significant revenue from payments processed through its restaurant platform. Shopify’s merchant services business now rivals its subscription revenue. This model works across verticals—construction, healthcare, professional services, and more.

2. AI-First Product Development

Companies that lead with AI capabilities rather than bolting them on are capturing disproportionate value. This requires rethinking product architecture, user interfaces, and value propositions around AI capabilities. The most successful AI-native SaaS companies treat AI as the product, not a feature.

Key success factors include: proprietary data that improves AI performance, workflows that improve with AI assistance, and pricing models that capture AI value. Companies like Gong (conversation intelligence) and Copy.ai (content generation) demonstrate this approach.

3. International Expansion

While the U.S. remains the largest SaaS market, significant growth opportunities exist internationally. Europe, Asia-Pacific, and Latin America represent underserved markets with growing SaaS adoption. Companies that can navigate localization, compliance, and go-to-market challenges can capture significant value.

International expansion requires investment in localization, regional sales and support, and compliance with local regulations (GDPR in Europe, data residency requirements in various countries). However, the payoff can be substantial—many successful SaaS companies generate 30-50% of revenue from international markets.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes possible in the SaaS market. Here are three case studies from 2026:

Case Study 1: NeuroFlow AI – From $0 to $100M ARR in 18 Months

NeuroFlow AI achieved one of the fastest growth trajectories in SaaS history by making AI agents the core product rather than a feature. Starting with $500K in seed funding, the company reached $100M ARR in just 18 months.

Their product-led growth engine launched with a viral freemium tier: any user could create a basic agent for free, but sharing it with 3+ team members unlocked collaborative features. This drove organic growth while demonstrating value. The company focused on autonomous workflow execution, allowing AI agents to handle complex business processes without human intervention.

Key success factors: AI as the product (not a feature), viral distribution mechanics, and solving high-value workflows autonomously. NeuroFlow demonstrates the growth potential for AI-native SaaS when execution aligns with market timing.

Case Study 2: EcoTrack Analytics – Bootstrapped to $20M ARR

EcoTrack Analytics demonstrates that venture funding is not required for SaaS success. The company bootstrapped to $20M ARR by weaponizing community-driven customer acquisition in the sustainability niche.

Rather than competing for expensive paid acquisition channels, EcoTrack built a passionate community of sustainability professionals who became advocates and distribution. The company focused on a specific vertical (carbon tracking and ESG reporting), creating deep functionality that horizontal tools could not match.

Key success factors: vertical focus, community-led growth, and capital efficiency. EcoTrack proves that bootstrapped SaaS can achieve significant scale with the right market and execution.

Case Study 3: Vanta – Compliance Automation at Scale

Vanta has built a $300M ARR business (up 69% year-over-year) with 16,000 customers by automating security compliance. The company recognized that SOC 2, ISO 27001, and other compliance frameworks were becoming table stakes for SaaS vendors, creating a massive market opportunity.

Vanta’s platform automates the evidence collection, monitoring, and reporting required for compliance, reducing what previously took months to weeks. The company has expanded from SOC 2 to cover multiple frameworks and use cases, increasing customer lifetime value.

Key success factors: regulatory tailwinds, workflow automation, and expansion across compliance frameworks. Vanta demonstrates how SaaS can capture value from increasing regulatory complexity.

Future Outlook and Predictions (2026-2030)

The SaaS market’s trajectory through 2030 will be shaped by technological advancement, evolving customer expectations, and macroeconomic factors. Here is what to expect:

Market Size Projections: The global SaaS market is projected to reach $819.23 billion by 2030 according to Grand View Research, representing a 12.0% CAGR from 2025. However, more aggressive projections from Mordor Intelligence suggest the B2B SaaS market alone could reach $1.58 trillion by 2031. The AI-Created SaaS market is expected to grow from $142 billion in 2026 to over $1 trillion by 2033.

AI Integration Deepens: By 2030, AI will be embedded in virtually every SaaS application. The distinction between AI-native and traditional SaaS will blur as AI becomes table stakes. Autonomous agents will handle increasingly complex workflows, potentially replacing entire job categories. The companies that win will be those that can deliver AI value reliably and cost-effectively.

Vertical Consolidation: Vertical SaaS platforms will continue consolidating, creating industry operating systems that handle an increasing share of business workflows. These platforms will embed not just software but financial services, marketplaces, and AI capabilities. Winners in each vertical will capture disproportionate value.

Pricing Model Evolution: Usage-based pricing will become the dominant model for infrastructure and AI-heavy applications, while seat-based pricing will persist for collaboration tools. Hybrid models that combine base subscriptions with usage components will emerge as a best practice. Pricing transparency and predictability will become competitive advantages.

Geographic Expansion: SaaS adoption will accelerate in emerging markets as internet infrastructure improves and digital transformation initiatives expand. Asia-Pacific will be the fastest-growing region, though North America will remain the largest market. Localization and compliance capabilities will be critical for international success.

Sustainability Focus: Environmental considerations will increasingly influence SaaS purchasing decisions. Carbon footprint of cloud infrastructure, sustainable development practices, and ESG reporting capabilities will become differentiators. SaaS companies will need to demonstrate environmental responsibility to win enterprise contracts.

SaaS Business Model Evolution

The SaaS business model has undergone significant evolution since its inception. What began as a simple subscription model has fragmented into multiple variations, each optimized for different customer segments and use cases. Understanding this evolution is crucial for both building and evaluating SaaS businesses in 2026.

Pure Subscription Model: The original SaaS model charges a fixed monthly or annual fee per user or organization. This model provides predictable revenue and simple unit economics but may not capture the full value delivered to high-usage customers. It remains dominant in collaboration tools, CRM, and HR software where value correlates with team size.

Usage-Based Pricing: Increasingly popular for infrastructure and AI-heavy applications, this model charges based on consumption—API calls, compute hours, data processed, or similar metrics. While it better aligns pricing with value, it introduces revenue volatility and requires sophisticated customer education. Companies like AWS, Snowflake, and OpenAI have proven this model at scale.

Freemium and Product-Led Growth: The freemium model offers a free tier with paid upgrades for advanced features or higher limits. When combined with product-led growth strategies, this model can drive viral adoption and efficient customer acquisition. Slack, Dropbox, and Notion exemplify successful freemium execution.

Hybrid Models: Many successful SaaS companies now combine elements of multiple models—a base subscription plus usage-based overages, or tiered subscriptions with feature gates. This approach balances predictability with value capture but requires careful pricing architecture to avoid customer confusion.

Regional Market Analysis

The SaaS market exhibits significant regional variation in adoption rates, competitive dynamics, and growth opportunities. Understanding these differences is essential for global expansion strategies.

North America: The United States remains the world’s largest SaaS market, accounting for approximately 45% of global spending. The region benefits from mature cloud infrastructure, high enterprise IT budgets, and a concentration of both vendors and customers. Canada represents a smaller but growing market with particular strength in AI and fintech SaaS.

Europe: Europe accounts for roughly 28% of global SaaS spending, with the UK, Germany, and France leading adoption. GDPR compliance has created both challenges and opportunities—vendors that can demonstrate robust data protection have a competitive advantage. The European market shows particular strength in privacy-focused and regulated industry solutions.

Asia-Pacific: Growing at the fastest rate of any region, Asia-Pacific represents 18% of global SaaS spending and climbing. China has developed its own SaaS ecosystem largely separate from Western markets, while India, Japan, and Australia are major adopters of global SaaS solutions. Mobile-first SaaS has particular traction in Southeast Asia.

Latin America and Emerging Markets: These regions represent the next frontier for SaaS expansion. While current penetration is lower, digital transformation initiatives and improving internet infrastructure are driving rapid adoption. Local payment methods, language support, and mobile optimization are critical success factors.

Technology Stack Evolution

The technology underlying SaaS has evolved dramatically, enabling new capabilities while reducing barriers to entry. Modern SaaS architecture reflects lessons learned from two decades of cloud computing.

Cloud-Native Architecture: Leading SaaS companies have embraced cloud-native principles—microservices, containerization, and serverless computing. This architecture enables scalability, resilience, and rapid deployment. Kubernetes has become the de facto standard for container orchestration, while serverless functions handle variable workloads efficiently.

Multi-Tenancy Models: SaaS architecture must balance resource efficiency with isolation and customization. Modern multi-tenant systems use sophisticated data partitioning, tenant-aware caching, and configurable business logic to serve diverse customers from shared infrastructure while maintaining security boundaries.

AI and Machine Learning Infrastructure: Integrating AI capabilities requires new infrastructure patterns—model serving, feature stores, vector databases, and specialized compute resources. SaaS companies must manage the complexity of ML operations while delivering reliable, cost-effective AI features to customers.

Edge Computing: For latency-sensitive applications, SaaS vendors are increasingly deploying processing at the edge—closer to end users. Content delivery networks have evolved into edge computing platforms, enabling real-time personalization, video processing, and IoT data ingestion with minimal latency.

Security and Compliance: Modern SaaS must meet stringent security standards—SOC 2, ISO 27001, GDPR, HIPAA, and industry-specific requirements. Zero-trust architecture, encryption at rest and in transit, and comprehensive audit logging are table stakes. Automated compliance monitoring and evidence collection have become competitive advantages.

Customer Success and Retention Strategies

In the SaaS model, customer success is not a department—it is a fundamental business strategy. Because customers can churn with minimal friction, delivering ongoing value is essential for sustainable growth.

Onboarding Excellence: The first 30 days determine whether a customer will become long-term. Best-in-class SaaS companies invest heavily in onboarding—personalized setup, in-app guidance, and proactive outreach. Time-to-value (TTV) is a critical metric, with leading companies achieving first value within hours rather than weeks.

Health Scoring and Predictive Analytics: Leading SaaS companies use data to predict churn before it happens. Health scores combine product usage, support tickets, NPS responses, and business context to identify at-risk accounts. Predictive models can flag churn risk weeks or months in advance, enabling proactive intervention.

Expansion Revenue: The most successful SaaS companies generate more revenue from existing customers than they lose to churn. Expansion strategies include seat expansion, feature upgrades, usage increases, and cross-selling complementary products. Net Revenue Retention (NRR) above 120% indicates a healthy expansion engine.

Customer Communities: Building community around a SaaS product creates network effects, reduces support burden, and increases switching costs. User forums, certification programs, and customer advisory boards deepen relationships while generating product feedback. Community-led growth is emerging as a powerful acquisition and retention strategy.

Proactive Support: Rather than waiting for customers to report issues, leading SaaS companies monitor for problems and reach out proactively. In-app messaging, automated check-ins, and customer success managers for high-value accounts ensure issues are resolved before they drive churn.

SaaS Metrics and Benchmarks

Understanding SaaS metrics is essential for evaluating performance, comparing against benchmarks, and making strategic decisions. The SaaS business model has spawned a unique vocabulary of metrics that capture the dynamics of recurring revenue businesses.

Annual Recurring Revenue (ARR): The most fundamental SaaS metric, ARR represents the predictable, recurring revenue from subscriptions normalized to a one-year period. It excludes one-time fees and professional services. ARR growth rate is the primary indicator of business momentum, with top-quartile companies growing 60%+ annually at scale.

Monthly Recurring Revenue (MRR): Similar to ARR but measured monthly, MRR provides more granular visibility into growth trends. MRR can be broken down into new MRR (from new customers), expansion MRR (from existing customers), contraction MRR (downgrades), and churned MRR (cancellations).

Customer Acquisition Cost (CAC): The total cost to acquire a new customer, including sales and marketing expenses. CAC payback period—the time to recover acquisition costs through gross margin—should typically be under 12 months for healthy unit economics. Rising CAC across the industry has made efficient growth a top priority.

Lifetime Value (LTV): The total revenue expected from a customer relationship. LTV:CAC ratio should exceed 3:1 for sustainable growth. LTV calculations require assumptions about churn rates, expansion revenue, and gross margins—making accurate measurement challenging but critical.

Net Revenue Retention (NRR): The percentage of recurring revenue retained from existing customers, including expansion, contraction, and churn. Best-in-class SaaS companies achieve NRR above 120%, meaning growth from existing customers more than offsets any losses. Public SaaS companies with NRR above 130% command premium valuations.

Gross Revenue Retention (GRR): Similar to NRR but excluding expansion revenue, GRR measures the core stickiness of the product. GRR above 85% is considered strong, with top performers exceeding 90%. The gap between NRR and GRR indicates expansion opportunity.

Magic Number: A measure of sales efficiency calculated as the net new ARR generated in a quarter divided by the previous quarter’s sales and marketing spend. A Magic Number above 0.75 indicates efficient growth, while above 1.0 is exceptional.

Rule of 40: The principle that a SaaS company’s growth rate plus profit margin should exceed 40%. This balances growth and profitability, with high-growth companies allowed lower margins and mature companies expected to deliver profits. The Rule of 40 has become a key valuation benchmark for SaaS businesses.

The Role of APIs and Ecosystems

Modern SaaS is increasingly interconnected, with APIs enabling data flow and workflow automation across applications. The API economy has become a defining characteristic of the SaaS landscape.

Integration Platforms: Tools like Zapier, Workato, and MuleSoft have made it possible for non-technical users to connect SaaS applications without writing code. These platforms have become essential infrastructure, with thousands of pre-built integrations enabling workflow automation across the SaaS stack.

Embedded Integrations: Leading SaaS vendors are embedding integration capabilities directly into their products. Rather than requiring customers to use third-party tools, they offer native connections to popular complementary applications. This reduces friction and increases product stickiness.

Platform Ecosystems: The largest SaaS companies have evolved into platforms that support third-party developers. Salesforce’s AppExchange, Slack’s app directory, and Shopify’s app store demonstrate how platforms can extend functionality while capturing value from ecosystem participants.

API-First Business Models: Some SaaS companies lead with their APIs rather than user interfaces, targeting developers as primary customers. Stripe (payments), Twilio (communications), and SendGrid (email) built massive businesses by making complex infrastructure accessible through simple APIs.

Data Synchronization: The challenge of keeping data consistent across multiple SaaS applications has created opportunities for synchronization platforms and data warehouses. Tools like Fivetran, Stitch, and Segment enable centralized data management while maintaining SaaS application functionality.

SaaS Security and Compliance Landscape

As SaaS has become critical infrastructure, security and compliance requirements have intensified. Enterprise customers demand rigorous security practices, while regulations like GDPR and industry-specific frameworks create compliance obligations.

SOC 2 Compliance: The SOC 2 framework has become the standard for SaaS security assurance. Developed by the AICPA, SOC 2 evaluates vendors across five trust service criteria: security, availability, processing integrity, confidentiality, and privacy. SOC 2 Type II reports, covering operational effectiveness over time, are increasingly required for enterprise sales.

GDPR and Data Privacy: The European Union’s General Data Protection Regulation has global implications for SaaS companies. Requirements include data minimization, purpose limitation, consent management, and the right to erasure. SaaS vendors must implement privacy by design and maintain detailed records of processing activities.

Industry-Specific Frameworks: Healthcare SaaS must comply with HIPAA in the United States, requiring business associate agreements and specific safeguards for protected health information. Financial services SaaS faces PCI DSS requirements for payment data and SOC 1 for financial reporting. FedRAMP authorization is required for U.S. government contracts.

Zero Trust Architecture: Modern SaaS security assumes breach and verifies every access request. Zero trust principles include least-privilege access, micro-segmentation, and continuous authentication. SaaS vendors are implementing zero trust both internally and as features for customers.

Supply Chain Security: SaaS applications depend on complex supply chains of open-source libraries, third-party APIs, and cloud infrastructure. Supply chain attacks have highlighted the need for software composition analysis, dependency scanning, and vendor security assessment.

Key Takeaways

- The SaaS market reached $492.34 billion in 2026 and is projected to grow to $1.58 trillion by 2031, representing one of the largest and fastest-growing sectors in technology.

- AI-native SaaS is the dominant growth category, with companies achieving $100M ARR in 18 months and raising at 40% higher valuations than traditional SaaS.

- Vertical SaaS is outpacing horizontal growth at 45% annually, as industry-specific solutions capture value that generic platforms cannot.

- Usage-based pricing has gone mainstream, now accounting for 35% of new contracts, but introduces cost volatility that both vendors and customers must manage.

- Customer retention remains the critical challenge—reducing churn by 5% can increase profits by 125%, making it the highest-leverage activity for SaaS companies.

Sources and Citations

- Mordor Intelligence – B2B SaaS Market Size & Share Analysis (2026-2031): https://www.mordorintelligence.com/industry-reports/b2b-saas-market

- Fortune Business Insights – Software as a Service [SaaS] Market Size Report: https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222

- Precedence Research – Software As A Service (SaaS) Market Size and Trends: https://www.precedenceresearch.com/software-as-a-service-market

- Zylo – 175+ Unmissable SaaS Statistics for 2026: https://zylo.com/blog/saas-statistics

- Email Vendor Selection – 71+ SaaS Statistics, Trends, and Benchmarks: https://www.emailvendorselection.com/saas-statistics

- Synergy Research Group – Microsoft Leads in SaaS Market Analysis: https://www.srgresearch.com/articles/microsoft-leads-saas-market-salesforce-adobe-oracle-and-sap-follow

- Coherent Market Insights – AI Created SaaS Market Size and Trends: https://www.coherentmarketinsights.com/industry-reports/ai-created-saas-market

- Grand View Research – Software As A Service Market Size Report: https://www.grandviewresearch.com/industry-analysis/saas-market-report

- SaaS Fourm – Case Studies: SaaS Success Stories from 2026: https://www.saasfourm.com/case-studies-saas-success-stories-from-lessons-from-explosive-growth

- Innovecs – Top SaaS Trends in 2026: https://innovecs.com/blog/the-top-7-saas-trends