The global advertising market is projected to reach a staggering $1.27 trillion in 2026, with digital channels capturing over 73% of total ad spend. For the first time in history, Meta is expected to surpass Google as the world’s largest digital advertising company, claiming 26.8% of global ad spend compared to Google’s 26.4%. These aren’t just numbers—they represent a fundamental shift in how businesses connect with consumers, how budgets are allocated, and how marketing strategies are executed in an AI-first world.

Digital marketing in 2026 is defined by three transformative forces: artificial intelligence that orchestrates entire campaigns from audience discovery through optimization, privacy regulations that have ended the era of third-party cookie tracking, and the rise of new platforms and formats that demand entirely new creative approaches. The marketers who thrive are those who understand not just where the industry stands today, but where it’s headed tomorrow.

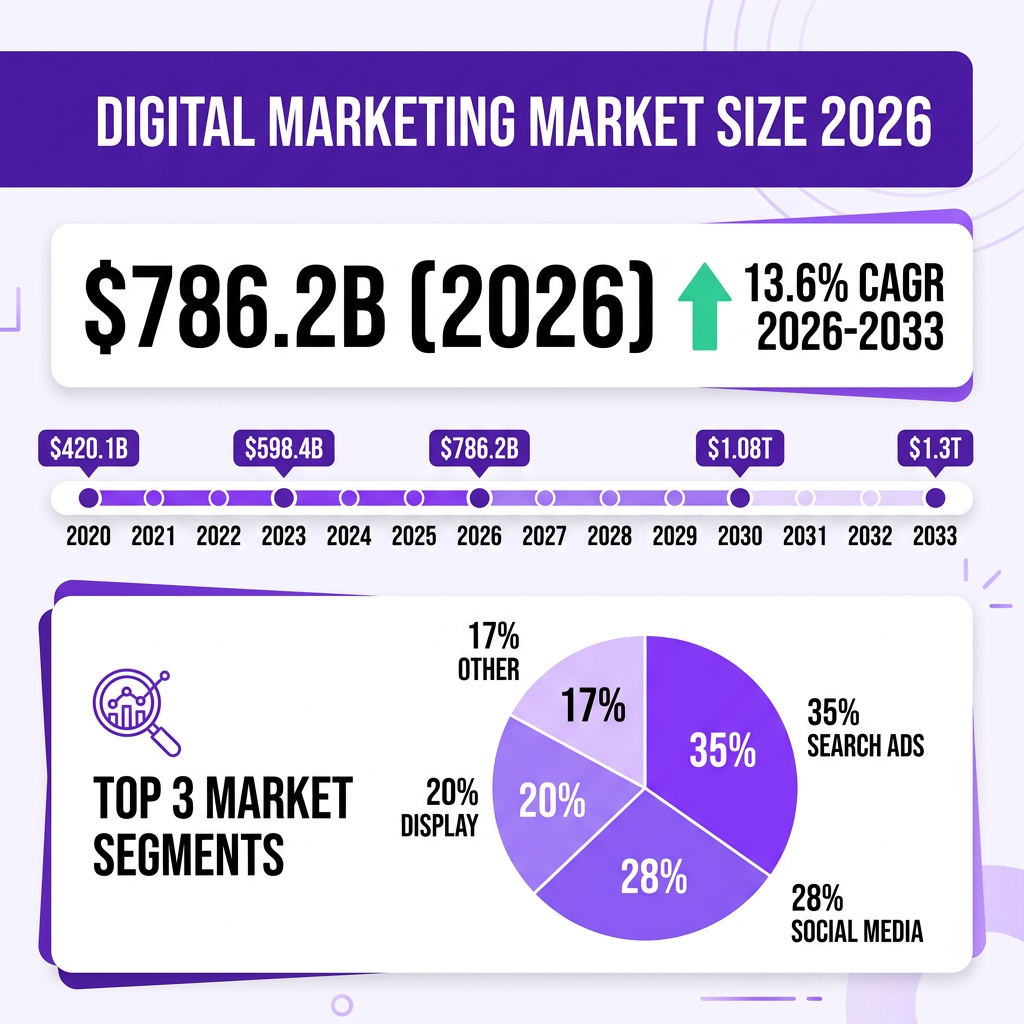

Market Overview: The $786.2 Billion Digital Advertising Ecosystem

The digital marketing landscape in 2026 represents one of the most dynamic and rapidly evolving sectors of the global economy. With global digital advertising spend reaching $786.2 billion this year, the industry has cemented its position as the dominant force in modern commerce. This figure represents a significant jump from the $602 billion recorded in 2023—a 38% increase in just three years that underscores the accelerating shift from traditional to digital channels.

The market’s growth trajectory shows no signs of slowing. Industry analysts project the digital marketing market will reach approximately $1.3 trillion by 2033, expanding at a compound annual growth rate (CAGR) of 13.6%. This sustained growth is driven by multiple factors: the continued migration of consumer attention to digital platforms, the development of sophisticated targeting and measurement capabilities, and the integration of artificial intelligence into every aspect of campaign execution.

Breaking down the market by component reveals the diverse ecosystem that makes up digital marketing in 2026. The digital marketing software market alone is projected to grow from $86.3 billion in 2025 to $99.3 billion in 2026, eventually reaching $321.8 billion by 2033 at an impressive CAGR of 18.3%. This software segment encompasses everything from marketing automation platforms and customer relationship management systems to analytics tools and AI-powered creative solutions.

The search engine optimization (SEO) market represents another significant component, valued at $108.28 billion in 2026. SEO services specifically account for $92.74 billion in 2025, with projections indicating growth to $203.83 billion by 2030 at a CAGR of 17.1%. This growth reflects the enduring importance of organic search visibility even as paid channels expand and AI-driven search experiences transform how users discover content.

Programmatic advertising has emerged as the dominant transaction model for digital media, with the market projected to reach $975.1 billion by 2033 at a CAGR of 19.9%. In 2026, more than 91% of all digital display ads are transacted programmatically, representing a fundamental shift from direct sales to automated, data-driven buying. The programmatic advertising market in 2026 is estimated at $720 billion, growing from $650 billion in 2025.

Social media advertising constitutes a major segment within the broader digital marketing landscape. Global social media advertising spending is on track to reach $275.98 billion in 2025 and is projected to hit $480 billion by 2030—a 5.2x increase from the less than $93 billion recorded in 2019. With 5.45 billion social media users worldwide in 2025 (forecast to reach 6.6 billion by 2030), social platforms have become essential channels for reaching consumers at scale.

The Asia-Pacific region continues to lead in digital marketing adoption and spend, driven by massive populations of connected consumers and rapidly growing e-commerce markets. China, India, and Southeast Asian nations represent the fastest-growing markets, with mobile-first strategies dominating due to high smartphone penetration. Meanwhile, North America and Europe remain the most mature markets, with higher per-capita digital ad spending and more sophisticated measurement and attribution capabilities.

Looking at industry verticals, retail and e-commerce continue to dominate digital advertising spend, followed by financial services, technology, and consumer packaged goods. The B2B sector has seen accelerated digital transformation, with companies investing heavily in account-based marketing, content marketing, and lead generation through digital channels. Healthcare and pharmaceutical marketing has also shifted significantly toward digital as regulations evolve and patients increasingly research conditions and treatments online.

Key Statistics and Data: 30 Numbers Defining Digital Marketing in 2026

Understanding the digital marketing landscape requires more than broad market size figures. The following statistics reveal the granular trends, platform dynamics, and consumer behaviors that are shaping strategy in 2026:

Market Size and Growth

- Global digital advertising spend in 2026: $786.2 billion

- Total global advertising market projection for 2026: $1.27 trillion

- Digital’s share of total advertising: 73%

- Digital marketing market value by 2033: $1.3 trillion

- Projected CAGR (2026-2033): 13.6%

- Digital marketing software market 2026: $99.3 billion

- Programmatic advertising market 2026: $720 billion

- SEO services market 2026: $108.28 billion

- Social media advertising spend 2026: $275.98 billion

Platform and Channel Statistics

- Meta’s projected share of global ad spend: 26.8%

- Google’s projected share of global ad spend: 26.4%

- Meta’s estimated ad revenue for 2026: $243.46 billion

- Meta’s year-over-year growth rate: 24.1%

- Google’s year-over-year growth rate: 11.9%

- Combined Meta, Google, and Amazon market share: Over 60%

- Programmatic share of digital advertising revenue: 87%

- Display ads transacted programmatically: 91%

Consumer Behavior and Engagement

- Share of online purchases made on mobile: 57%

- Share of budgets allocated to mobile advertising: 54%

- Share of local searches on Google: 46%

- Social media users worldwide: 5.45 billion (2025)

- Email users worldwide: 4.8 billion (2026)

- TikTok engagement rate compared to Instagram: 8x higher

- TikTok average engagement rate: 7.4% to 8.1%

- Instagram average engagement rate: 1.8%

- Facebook named most important platform by: 36% of marketers

- Facebook highest ROI platform for: 54% of marketers

AI and Technology Adoption

- Organizations regularly using generative AI: 71%

- AI powering marketing activities: 15.1%

- Marketers using AI to scale creative: 46%

- Ad buyers strengthening genAI use: 78% (up from 62%)

- AI video ad spend projection: $9.1 billion (12% of digital video)

- Advertising executives deploying AI in creative: 83%

- Small and medium businesses using AI in marketing: 67%

- Marketers citing content creation as top AI use case: 55%

- Marketers planning to use AI in content creation: 94%

- Writers using AI tools to boost content performance: 50%

ROI and Performance Metrics

- Average email marketing ROI: $45 for every $1 spent (retail/e-commerce)

- Average e-commerce email click-through rate: 2.86%

- Email open rates benchmark: 25-40%

- Email click-through rates benchmark: 1-3%

- Percentage of email revenue from automation flows: 30-50%

- Estimated marketing budget waste: Up to 30%

- Organic traffic reduction due to AI Overviews: 18-47%

Major Trends Shaping Digital Marketing in 2026

The digital marketing landscape of 2026 is being reshaped by seven major trends that are redefining how brands connect with consumers, allocate budgets, and measure success. Understanding these trends is essential for any marketer looking to build effective strategies in this rapidly evolving environment.

1. The Platform Power Shift: Meta Surpasses Google

For the first time in the history of digital advertising, Meta is projected to overtake Google as the world’s largest digital advertising company by the end of 2026. According to eMarketer forecasts, Meta will capture 26.8% of global ad spend, slightly ahead of Google’s 26.4%. This represents a seismic shift in the digital advertising landscape that has been dominated by Google for over two decades.

Meta’s ascendancy is driven by its superior growth rate—projected at 24.1% year-over-year compared to Google’s 11.9%. The company’s advertising business has benefited from several factors: the integration of AI into ad targeting and creative optimization, the continued strength of Instagram as a discovery and shopping platform, and the recovery of digital advertising markets following economic uncertainties.

This shift has profound implications for marketers. While Google Search remains essential for capturing high-intent demand, Meta’s platforms have become increasingly effective for both brand building and direct response. The company’s investments in AI-driven creative tools, shopping features, and measurement capabilities have made it an indispensable channel for advertisers across industries.

The implications extend beyond budget allocation. Meta’s dominance means that understanding its algorithms, creative best practices, and measurement frameworks is now essential for digital marketers. The company’s Advantage+ shopping campaigns, which use AI to automate targeting and creative optimization, have become a model for performance advertising that other platforms are working to replicate.

2. AI-Powered Personalization at Scale

Artificial intelligence has moved from experimental tooling to core marketing infrastructure. By 2026, 71% of organizations regularly use generative AI, and AI now powers 15.1% of all marketing activities. The technology has transformed every stage of the marketing funnel—from audience discovery and creative production to optimization and measurement.

The most significant application of AI in marketing is personalization at scale. Machine learning algorithms can now analyze vast datasets to deliver individualized experiences to millions of users simultaneously. This capability has moved beyond simple demographic targeting to encompass behavioral patterns, contextual signals, and predictive intent modeling.

However, the rise of AI in marketing comes with challenges. Research indicates that marketers should reduce organic traffic expectations by 18-47% as Google AI Overviews answer user queries directly without requiring clicks. This shift is forcing marketers to rethink their search strategies and explore new approaches to visibility and engagement.

The integration of AI into marketing workflows has also raised questions about the future of marketing roles. While some fear displacement, the reality is that AI is augmenting human capabilities rather than replacing them. The most successful marketers are those who can effectively collaborate with AI tools, using them to automate routine tasks while focusing on strategy, creativity, and relationship building.

3. Programmatic Advertising Dominance

Programmatic advertising has achieved near-total dominance in digital display, with 91% of all digital display ads transacted programmatically in 2026. The programmatic advertising market is projected to reach $975.1 billion by 2033, growing at a CAGR of 19.9%.

This growth is driven by three primary factors: the accelerating adoption of artificial intelligence and machine learning technologies that enhance targeting precision and optimize bidding strategies in real time; the fundamental shift in consumer media consumption toward streaming platforms and connected TV environments; and the escalating demand from retailers and enterprises for measurable, performance-driven advertising solutions.

Programmatic advertising now extends far beyond traditional display to encompass video, connected TV, digital out-of-home, and audio. The technology has enabled advertisers to reach audiences across an increasingly fragmented media landscape with unprecedented efficiency and precision.

The rise of programmatic has also transformed the relationship between advertisers and publishers. Real-time bidding has created a more efficient marketplace, but it has also put pressure on publisher revenues and raised concerns about brand safety and ad fraud. These challenges have driven investment in verification technologies and private marketplace deals that offer more control and transparency.

4. Video-First Content Strategy

Video has become the dominant content format across all digital marketing channels. Short-form video, pioneered by TikTok and adopted by Instagram Reels and YouTube Shorts, has transformed how brands create and distribute content. TikTok’s engagement rates—averaging 7.4% to 8.1%—are roughly eight times higher than Instagram’s, demonstrating the format’s power to capture and hold audience attention.

AI-generated video has emerged as a significant trend, with global AI video ad spend projected at $9.1 billion in 2026—roughly 12% of all digital video advertising. This represents a dramatic shift from just three years ago when AI-generated video was effectively nonexistent in advertising.

The economics of video production have been transformed by AI tools that can produce comparable creative at 70-90% lower costs in hours instead of weeks. Traditional ad production costs $10,000 to $50,000 for a 30-second commercial, while AI tools enable brands to create high-quality video content at a fraction of the cost and time.

Live video has also emerged as a powerful format, with platforms investing heavily in live shopping experiences and real-time engagement features. The authenticity and immediacy of live content creates unique opportunities for brands to connect with audiences in ways that pre-recorded content cannot match.

5. Privacy-First Marketing

The deprecation of third-party cookies and the standardization of global privacy regulations have fundamentally changed how marketers collect, use, and protect consumer data. The industry is shifting from a “data rental” model to a new era of “asset building” focused on first-party data.

This shift has accelerated investment in customer data platforms, consent management systems, and privacy-enhancing technologies. Marketers are increasingly focused on building direct relationships with consumers and creating value exchanges that encourage voluntary data sharing.

The key to success in this new environment is no longer simply “buying traffic,” but rather “building assets + verifying authenticity + achieving automation.” Brands that can simultaneously strengthen their first-party data, AI infrastructure, and compliance capabilities will be best positioned to succeed.

Contextual targeting has experienced a renaissance as cookie-based targeting becomes less viable. Rather than tracking individuals across the web, contextual advertising uses the content of a page to determine ad relevance. Advances in natural language processing have made contextual targeting more sophisticated and effective than ever before.

6. Social Commerce Expansion

Social commerce—the integration of shopping experiences directly into social media platforms—has become a major growth driver. With 26% of marketers planning to explore selling products directly on social media in 2026, platforms like Instagram, TikTok, and Facebook have invested heavily in native commerce capabilities.

The convergence of content and commerce has shortened the path from discovery to purchase. Users can now discover, research, and buy products without leaving their favorite social apps. This trend is particularly pronounced among younger consumers who increasingly use social platforms as their primary discovery and shopping channels.

Live shopping, popularized in Asian markets, has gained traction globally. Brands and creators host live streams where viewers can purchase featured products in real-time. This format combines entertainment, social proof, and instant gratification in a way that traditional e-commerce cannot replicate.

7. Generative AI Creative Production

Generative AI has transformed creative production, with 83% of advertising executives deploying AI in their creative process as of 2026—up from 60% just two years earlier. The technology is being used for everything from copywriting and image generation to video production and personalization.

The most common use cases for AI in marketing include content creation (50%), reporting and analytics (39%), creative ideation (37%), market research (35%), and marketing automation (33%). Non-AI blog creation has dropped from 65% to 5%, indicating how rapidly AI has been adopted for content production.

However, the rise of AI-generated content has also raised concerns about authenticity, quality control, and maintaining brand voice. The most effective AI-generated ads start with strong brand inputs: quality product images, clear brand guidelines, and defined audience segments.

The quality of AI-generated creative has improved dramatically, but human oversight remains essential. The best results come from collaborative workflows where AI handles production and iteration while humans provide strategic direction and quality control.

Key Players and Competitive Landscape

The digital marketing ecosystem is dominated by a handful of technology giants, but the competitive landscape is evolving rapidly as new entrants challenge incumbents and traditional boundaries between platforms blur.

The Triopoly: Meta, Google, and Amazon

Meta, Google, and Amazon together account for over 60% of the global digital advertising market. This concentration of market power has significant implications for advertisers, publishers, and the broader digital economy.

Meta has emerged as the dominant force in social advertising, with projected ad revenue of $243.46 billion in 2026. The company’s platforms—including Facebook, Instagram, Messenger, and WhatsApp—reach billions of users worldwide. Meta’s strength lies in its sophisticated targeting capabilities, AI-driven optimization, and the integration of commerce features that enable seamless shopping experiences.

Google remains the leader in search advertising and maintains significant positions in display (through Google Display Network), video (YouTube), and programmatic (Display & Video 360). While the company is projected to lose its position as the top digital advertising company to Meta in 2026, its search business continues to generate massive revenue from high-intent queries.

Amazon has built a formidable advertising business by leveraging its e-commerce platform and first-party purchase data. The company’s advertising revenue has grown rapidly as brands recognize the value of reaching consumers at the point of purchase intent.

Emerging Platforms and Challengers

Beyond the triopoly, several platforms are gaining significant traction. TikTok has emerged as a major force in digital advertising, with engagement rates that dwarf those of competitors. The platform’s algorithm-driven content discovery has made it particularly effective for reaching younger audiences and driving viral content.

LinkedIn dominates B2B advertising, offering unique access to professional audiences and decision-makers. The platform’s advertising business has grown as B2B marketers increasingly shift budgets to digital channels.

Microsoft has strengthened its position in digital advertising through its partnership with OpenAI and the integration of AI capabilities into its search and advertising products. The company’s acquisition of Xandr has also bolstered its programmatic advertising capabilities.

Apple has taken a different approach, emphasizing privacy while building its advertising business through App Store ads and Apple News. The company’s privacy-focused positioning has resonated with consumers concerned about data tracking.

Ad Tech and MarTech Ecosystem

The advertising technology and marketing technology ecosystems include thousands of companies providing specialized solutions for targeting, measurement, creative optimization, and customer data management. Key categories include:

- Demand-Side Platforms (DSPs): Enable advertisers to buy inventory programmatically across multiple sources, with leading players including The Trade Desk, Google Display & Video 360, and Amazon DSP

- Supply-Side Platforms (SSPs): Help publishers manage and monetize their ad inventory, with major providers including Google Ad Manager, Magnite, and PubMatic

- Customer Data Platforms (CDPs): Unify customer data from multiple sources to enable personalization, with Segment, mParticle, and Tealium leading the category

- Marketing Automation Platforms: Automate marketing workflows across email, social, and other channels, with HubSpot, Marketo, and Salesforce Marketing Cloud as major players

- Analytics and Attribution: Measure campaign performance and attribute conversions across touchpoints, with Google Analytics, Adobe Analytics, and specialized attribution providers

The ad tech landscape has undergone significant consolidation as privacy changes and platform restrictions have made independent targeting more difficult. Companies that can offer first-party data solutions, privacy-enhancing technologies, or specialized vertical expertise have fared better than those dependent on third-party cookies.

Challenges and Pain Points

Despite the tremendous growth and opportunity in digital marketing, the industry faces significant challenges that are reshaping how marketers operate and allocate resources.

1. Privacy Regulations and Signal Loss

The deprecation of third-party cookies, implementation of privacy regulations like GDPR and CCPA, and platform restrictions on data sharing have created a “signal loss” crisis for marketers. Up to 30% of marketing budgets are wasted, according to most marketers, due to inefficient targeting and measurement challenges.

Marketers are struggling to maintain targeting precision and attribution accuracy in an environment where traditional identifiers are disappearing. This has increased the importance of first-party data strategies, contextual targeting, and privacy-enhancing technologies.

The regulatory landscape continues to evolve, with new privacy laws being enacted globally. Marketers must navigate a complex patchwork of regulations while maintaining effective targeting and measurement capabilities.

2. AI-Driven Search Disruption

The integration of generative AI into search engines—particularly Google’s AI Overviews—is fundamentally changing how users discover information. With AI providing direct answers to queries, marketers face reduced organic traffic expectations of 18-47%.

This shift requires new approaches to search visibility, including optimization for AI-generated answers, increased focus on brand presence in AI responses, and diversification beyond traditional SEO tactics.

The emergence of Generative Engine Optimization (GEO) and Answer Engine Optimization (AEO) represents a new frontier in search marketing. Rather than optimizing for blue links, marketers must now optimize for inclusion in AI-generated summaries and answers.

3. Content Saturation and Attention Competition

The proliferation of AI-generated content has created a saturation problem, making it increasingly difficult for brands to stand out. Consumers are bombarded with content across multiple platforms, and attention spans continue to decline.

Marketers must now compete not just with other brands, but with an endless stream of user-generated content, entertainment, and algorithmically recommended media. This has raised the bar for content quality and authenticity.

The challenge is compounded by algorithm changes that prioritize engagement over reach. Platforms are increasingly showing content from accounts users don’t follow if the algorithm determines it will drive engagement, making it harder for brands to maintain consistent visibility with their audiences.

4. Measurement and Attribution Complexity

As the customer journey becomes more complex and privacy restrictions limit tracking capabilities, accurate measurement and attribution have become increasingly difficult. Marketers struggle to understand which touchpoints are driving conversions and how to optimize their media mix.

This has driven renewed interest in marketing mix modeling (MMM) and other privacy-safe measurement approaches. However, these methods require significant data and expertise, putting them out of reach for many smaller advertisers.

Opportunities and Growth Strategies

Amidst the challenges, significant opportunities exist for marketers who can adapt to the new landscape and leverage emerging capabilities.

1. First-Party Data Advantage

Brands that invest in building direct relationships with customers and collecting first-party data are gaining a significant competitive advantage. This data—collected with consent through owned channels like websites, apps, and email—provides a foundation for personalization and targeting that is not dependent on third-party cookies.

Successful strategies include creating value exchanges that encourage data sharing, implementing customer data platforms to unify data sources, and using zero-party data (information customers intentionally share) to enhance personalization.

Loyalty programs, exclusive content, and personalized experiences can all incentivize customers to share their data willingly. The key is to be transparent about how data will be used and to deliver clear value in exchange.

2. AI-Augmented Creativity

Rather than replacing human creativity, AI is augmenting it. Marketers are using AI to accelerate creative production, test variations at scale, and personalize content for different audience segments. The combination of human strategic thinking and AI execution is proving more effective than either alone.

Opportunities include using AI for rapid creative iteration, generating personalized content variations, and optimizing creative performance in real-time based on engagement data.

Dynamic creative optimization (DCO) has become increasingly sophisticated, with AI enabling real-time assembly of creative elements based on audience signals. This allows for personalization at a scale that would be impossible with manual production.

3. Emerging Platform Growth

New platforms and formats continue to emerge, offering first-mover advantages for early adopters. Connected TV, digital audio, and immersive formats like augmented reality represent significant growth opportunities.

Connected TV ad spend is forecast to grow 13.8% in the US in 2026, with AI-generated creative enabling long-tail advertisers to participate in premium video advertising for the first time.

Retail media networks—advertising platforms operated by retailers—have emerged as a major new category. Amazon pioneered the model, but Walmart, Target, and other major retailers have followed suit. These platforms offer unique access to shoppers at the point of purchase intent, with closed-loop attribution that proves ROI.

4. Influencer and Creator Partnerships

The creator economy has matured into a significant marketing channel. The global influencer marketing platform market was valued at $20.24 billion in 2026 and is projected to grow to $70.86 billion by 2032.

Nano-influencers (creators with smaller but highly engaged followings) consistently outperform larger creators in engagement rates. With 75.9% of Instagram’s influencer base in the nano category, brands have unprecedented access to authentic, high-performing partnerships.

Long-term ambassador relationships are replacing one-off sponsored posts as brands recognize the value of sustained partnerships. These relationships build authentic connections with audiences and generate content that can be repurposed across channels.

Case Studies and Success Stories

Case Study 1: AI-Powered Creative Optimization

A leading e-commerce brand implemented AI-powered creative optimization across its Meta and Google campaigns, resulting in a 40% improvement in return on ad spend (ROAS) within three months. The brand used generative AI to create hundreds of creative variations, which were then tested and optimized using machine learning algorithms. The key success factor was maintaining strong brand guidelines while allowing AI to optimize for performance.

The brand started by feeding its best-performing creative assets into an AI system that generated variations of headlines, images, and calls-to-action. These variations were tested across different audience segments, with the algorithm automatically allocating budget to the best-performing combinations. Within weeks, the system had identified creative approaches that outperformed the brand’s previous best ads by significant margins.

Case Study 2: First-Party Data Transformation

A B2B software company transformed its marketing performance by building a comprehensive first-party data strategy. By creating valuable content and tools that encouraged registration, the company grew its first-party database by 300% in 12 months. This data foundation enabled personalized nurture campaigns that increased conversion rates by 45% and reduced customer acquisition costs by 30%.

The company invested in interactive tools—calculators, assessments, and configurators—that provided immediate value to prospects while capturing valuable data about their needs and interests. This data was used to personalize follow-up communications and route leads to the appropriate sales channels based on their characteristics and behavior.

Case Study 3: TikTok Viral Campaign

A consumer packaged goods brand achieved viral success on TikTok by partnering with micro-influencers to create authentic, entertaining content. The campaign generated 50 million views and a 200% increase in sales during the campaign period. The key insight was that TikTok’s algorithm rewards engaging content regardless of follower count, enabling smaller creators to drive significant reach.

Rather than working with a few large influencers, the brand partnered with dozens of micro-creators who had authentic connections to the product category. The creators were given creative freedom to develop content that would resonate with their specific audiences, resulting in a diverse range of content that felt native to the platform rather than overtly promotional.

Future Outlook and Predictions (2027-2030)

Looking beyond 2026, several trends will shape the future of digital marketing:

Market Projections

- Global digital advertising market will reach $1.3 trillion by 2033

- Programmatic advertising will approach $1 trillion by 2033

- Social media users will reach 6.6 billion by 2030

- Social media ad spend will hit $480 billion by 2030

- Digital will capture nearly 65% of global ad spend by 2030

- Influencer marketing will grow to $70.86 billion by 2032

Technology Evolution

AI will continue to transform marketing, with predictive forecasting, automated channel mix decisions, and real-time creative adaptation becoming standard capabilities. The integration of AI agents into marketing workflows will enable autonomous optimization of campaigns across channels.

Immersive technologies like augmented reality and virtual reality will create new advertising formats and consumer experiences. As these technologies mature, they will open entirely new categories of digital marketing.

Voice interfaces will become increasingly important as smart speakers and voice assistants proliferate. Marketers will need to develop strategies for voice search optimization and audio advertising.

Regulatory Landscape

Privacy regulations will continue to expand globally, with more countries implementing comprehensive data protection frameworks. Marketers will need to build privacy-centric strategies that deliver personalization without compromising consumer trust.

The regulatory focus may shift from data collection to algorithmic transparency, with potential requirements to explain how AI systems make decisions about content distribution and ad targeting.

Key Takeaways

- The global digital advertising market will reach $786.2 billion in 2026, representing 73% of total ad spend

- Meta is projected to surpass Google as the largest digital advertising company for the first time, with 26.8% market share

- AI has become core marketing infrastructure, with 71% of organizations regularly using generative AI

- Programmatic advertising dominates with 91% of digital display ads transacted programmatically

- Video is the dominant content format, with AI-generated video ad spend reaching $9.1 billion

- Privacy regulations have ended the third-party cookie era, making first-party data strategies essential

- Email marketing continues to deliver the highest ROI at $45 for every $1 spent

- The market is projected to reach $1.3 trillion by 2033, growing at 13.6% CAGR

Sources and Citations

- eMarketer – Meta to Surpass Google in Digital Ad Revenues Forecast (2026)

- Grand View Research – Digital Marketing Software Market Size Report (2026-2033)

- Hostinger – 47 Essential Digital Marketing Statistics for 2026

- Incremys – Digital Marketing 2026 Statistics

- Persistence Market Research – Programmatic Advertising Market Forecast

- Renub Research – Programmatic Advertising Market Outlook 2026

- SearchLab – Programmatic Advertising Statistics 2026

- The Business Research Company – SEO Services Market Report 2026

- HubSpot – 2026 Marketing Statistics, Trends & Data

- Smartly.io – 2026 Digital Advertising Trends Report

- Improvado – 7 AI Marketing Trends Reshaping Strategy in 2026

- TechnologyChecker – AI in Marketing Statistics 2026

- Morphed – AI Advertising Statistics 2026

- The Influencer Marketing Factory – TikTok vs Instagram Engagement 2026

- Metricool – 25 TikTok Statistics in 2026

- Digital Applied – Content Marketing Statistics 2026

- MarkNtel Advisors – Digital Marketing Market Research Report

Regional Market Analysis

The digital marketing landscape varies significantly across regions, with different markets at different stages of maturity and facing unique challenges and opportunities.

North America

North America remains the most mature digital advertising market, with the highest per-capita ad spending and most sophisticated measurement capabilities. The United States alone accounts for a significant portion of global digital ad spend, with major platforms and ad tech companies headquartered in the region.

The region leads in adoption of emerging technologies like AI-powered marketing tools and connected TV advertising. However, it also faces the most stringent privacy regulations, with state-level laws in California, Virginia, and other states adding complexity to compliance.

Europe

Europe’s digital marketing landscape is shaped by the General Data Protection Regulation (GDPR), which has set the global standard for privacy protection. The Digital Markets Act (DMA) and Digital Services Act (DSA) are further reshaping the competitive landscape by imposing new obligations on large platforms.

Despite regulatory challenges, Europe remains a significant market with high digital penetration and sophisticated consumers. The region has seen strong growth in privacy-preserving advertising technologies and first-party data strategies.

Asia-Pacific

Asia-Pacific is the fastest-growing region for digital marketing, driven by massive populations of connected consumers and rapidly expanding e-commerce markets. China, India, and Southeast Asian nations represent enormous opportunities, though each market has unique characteristics and platform ecosystems.

Mobile-first strategies dominate in the region, with many consumers accessing the internet primarily through smartphones. Social commerce and live shopping are particularly advanced in Asian markets, offering a preview of trends that are likely to spread globally.

Latin America and Middle East/Africa

These emerging markets represent significant growth opportunities as internet penetration increases and digital payments become more accessible. While current ad spend is lower than in mature markets, the growth rates are among the highest globally.

Challenges include infrastructure limitations, payment friction, and in some cases, political instability. However, brands that establish early presence in these markets can build significant competitive advantages as they develop.