The global Software as a Service (SaaS) market has reached an inflection point in 2026. With the market valued at $465.03 billion and projected to surge to approximately $1.37 trillion by 2035, SaaS has cemented itself as the dominant software delivery model for businesses worldwide. This represents a compound annual growth rate (CAGR) of 12.85%, signaling robust, sustained expansion across every industry vertical and geography.

What makes 2026 particularly significant is the convergence of multiple transformative forces: artificial intelligence integration, shifting pricing paradigms, and the maturation of vertical SaaS solutions. The industry is no longer just about delivering software over the cloud—it is about intelligent, automated, deeply integrated platforms that fundamentally reshape how businesses operate.

Market Overview: The $465 Billion Ecosystem

The SaaS market’s evolution from a niche delivery model to a $465 billion global powerhouse represents one of the most significant shifts in enterprise technology history. In 2025, the market stood at approximately $408 billion, meaning 2026 marks a year of substantial acceleration with nearly $57 billion in new value creation.

North America continues to dominate the global SaaS landscape, commanding the largest regional market share. The United States alone generates approximately $187 billion in SaaS revenue, driven by a mature cloud infrastructure, high enterprise technology adoption rates, and the presence of industry giants like Salesforce, Microsoft, Adobe, and ServiceNow. Western Europe represents the fastest-growing region, with enterprises accelerating digital transformation initiatives in response to competitive pressures and regulatory requirements.

The Asia-Pacific region, while currently holding approximately 21.4% of the market, is projected to experience the fastest growth trajectory through 2035. Countries like India, Singapore, and South Korea are witnessing explosive SaaS adoption, fueled by a burgeoning startup ecosystem, increasing cloud literacy, and government-led digital transformation programs.

Looking at the deployment models, public cloud SaaS solutions continue to lead with the majority market share, particularly among small and medium enterprises that lack the resources to manage private infrastructure. However, hybrid cloud deployments are gaining significant traction as large enterprises seek to balance the flexibility of cloud solutions with the security and control of on-premises systems. Private cloud SaaS, while representing a smaller segment, remains critical for highly regulated industries such as healthcare, financial services, and government sectors.

The application landscape reveals Customer Relationship Management (CRM) as the dominant segment, accounting for approximately 28% of total SaaS spending. This is followed by Enterprise Resource Planning (ERP) at 22%, and collaboration tools at 18%. The dominance of CRM reflects the universal priority businesses place on customer acquisition and retention, while the substantial ERP share underscores the ongoing migration of core business processes to cloud-native platforms.

By enterprise size, large organizations currently account for 62.3% of SaaS spending, driven by their complex requirements and ability to invest in comprehensive digital transformation initiatives. However, the SME segment is growing rapidly as SaaS vendors increasingly tailor solutions for smaller businesses with simplified pricing, faster implementation timelines, and reduced technical requirements.

Key Statistics and Data Points

The SaaS industry’s scale and impact are best understood through the lens of hard data. Here are the critical statistics defining the market in 2026:

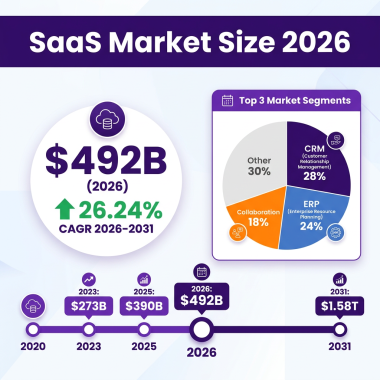

Market Size and Growth: The global SaaS market reached $465.03 billion in 2026, up from $408.21 billion in 2025. The B2B SaaS segment specifically is valued at $492.34 billion in 2026 and is projected to reach $1.58 trillion by 2031, representing a remarkable CAGR of 26.24%. Alternative market sizing from Grand View Research places the 2024 baseline at $399.10 billion, with projections reaching $819.23 billion by 2030 at a 12.0% CAGR.

Enterprise Adoption: The average company now uses 106 SaaS applications, down slightly from 112 in 2023, indicating a trend toward consolidation. However, this consolidation rate has dropped from 14% to just 5% year-over-year, suggesting that while companies are mindful of sprawl, they continue adopting specialized tools. Organizations currently deploy an average of 7.3 SaaS applications with AI functionality, representing 7% of total SaaS apps.

AI Investment Surge: Spending on AI-native SaaS applications increased by 108% year-over-year. According to the State of FinOps 2025 Report, 63% of organizations now manage AI spend, with adoption projected to reach 96% by the end of 2026. AI-powered SaaS companies command valuation premiums of 40% compared to traditional SaaS businesses.

Revenue Retention Benchmarks: The median Net Revenue Retention (NRR) for private B2B SaaS companies stands at 101%, with bootstrapped companies achieving a median of 104%. Top performers push NRR above 120% through proactive customer success and expansion strategies. Gross Revenue Retention (GRR) benchmarks range from 85-95%, with the median at 91% for bootstrapped companies in the $3M-$20M ARR range.

Growth Rates: The median revenue growth rate for bootstrapped SaaS companies with $3M-$20M ARR is 15% annually, while companies in the 90th percentile achieve 42.3% growth. VC-backed SaaS companies show higher growth rates but also higher burn rates, with sales and marketing representing 47% of revenue compared to 33% for PE-backed companies.

Customer Acquisition: The average B2B SaaS Customer Acquisition Cost (CAC) sits at $1,200, though this varies significantly by company size and market segment. SEO delivers a remarkable 702% ROI for B2B SaaS companies with a break-even time of just 7 months. Email marketing remains the most effective revenue channel, with 59% of B2B marketers naming it their top performer.

Churn and Retention: Reducing churn by just 5% can increase profits by 125%. The median annual B2B SaaS retention rate sits around 88-90%, meaning there is significant room for improvement. Monthly churn rates below 1% (annualized below 5%) are considered good, while top performers achieve even lower rates.

Valuation Multiples: The median EV/Revenue multiple for SaaS companies stands at 3.4x as of March 2026. Public SaaS companies trade at a median ARR multiple of 6.7x. AI-native SaaS companies at Series B stage command median valuations of $175 million, representing a 38% year-over-year increase.

Expansion Revenue: Expansion ARR now represents 40% of total new ARR for SaaS companies, a 5% increase from 2024. For companies exceeding $50M ARR, expansion revenue represents over 50% of total new ARR, highlighting the critical importance of land-and-expand strategies.

R&D Investment: Private SaaS companies invest 34% of revenue in R&D compared to 23% for public SaaS companies, reflecting the ongoing innovation race and the need to differentiate in crowded markets.

Major Trends Shaping SaaS in 2026

The SaaS landscape is being fundamentally reshaped by seven major trends that will define the industry through the remainder of the decade:

1. AI-Native SaaS Becomes the Default

Artificial intelligence is no longer a differentiator—it is an expectation. The AI-Created SaaS market is expected to reach $142.02 billion in 2026 and surge to $1.05 trillion by 2033, representing a staggering 39.6% CAGR. Machine learning leads this segment with a 42.3% market share, followed by natural language processing and computer vision applications.

What distinguishes 2026 from previous years is the shift from AI as a feature to AI as the core product architecture. Companies like NeuroFlow AI exemplify this trend, achieving $100M ARR in just 18 months by making AI agents the product rather than an add-on. The viral freemium model—where users can create basic agents for free but unlock collaborative features by inviting team members—has proven particularly effective for AI-native platforms.

2. Vertical SaaS Dominates New Entrants

Horizontal SaaS platforms are facing increasing competition from vertical solutions purpose-built for specific industries. Vertical AI SaaS companies in healthcare, legal, and financial services raised the largest early-stage rounds, with median Series A sizes of $22 million compared to $15 million for traditional horizontal SaaS.

This trend reflects a maturation of the SaaS market. As general-purpose tools become commoditized, value creation shifts toward deep industry expertise, specialized workflows, and regulatory compliance built into the software DNA. Companies that understand the nuances of their target vertical—from HIPAA compliance in healthcare to SEC reporting requirements in finance—are commanding premium valuations and achieving faster customer acquisition.

3. Usage-Based Pricing Goes Mainstream

The traditional per-seat subscription model is giving way to consumption-based pricing that aligns vendor success with customer value realization. This shift is accelerating as AI capabilities increase software consumption unpredictably—customers want to pay for outcomes, not access.

Usage-based pricing creates natural expansion revenue as customers grow, reduces friction in the sales process by lowering initial commitment, and better serves the long tail of occasional users who were previously priced out of seat-based models. However, it also introduces new challenges in revenue predictability and requires sophisticated billing infrastructure.

4. API-First and Embedded SaaS

The most successful SaaS companies of 2026 are those that disappear into the background. API-first architectures allow SaaS functionality to be embedded directly into customer applications and workflows, creating invisible infrastructure that powers experiences rather than standalone products that require context switching.

This trend is particularly pronounced in categories like payments, communications, and analytics, where the best SaaS is the one users never know they are using. The rise of embedded finance—where banking, lending, and insurance capabilities are woven into non-financial software—exemplifies this shift toward invisible infrastructure.

5. Workflow Orchestration Becomes Mandatory

As SaaS portfolios expand, the ability to orchestrate workflows across multiple applications becomes critical. Reliable AI at scale requires control planes and execution layers, not isolated features. Companies are demanding unified platforms that can automate complex, multi-step processes spanning CRM, ERP, HR, and specialized tools.

This trend favors platforms with robust integration ecosystems, open APIs, and native workflow automation capabilities. It also creates opportunities for pure-play orchestration vendors that can sit above the application layer and coordinate activity across a company’s entire SaaS stack.

6. Data as Infrastructure and Product

Clean, versioned, and governed data has become both the foundation for AI performance and a monetizable product in its own right. SaaS companies are increasingly recognizing that the data flowing through their platforms may be as valuable as the software itself.

This realization is driving investments in data platforms, integration layers, and ownership models that treat data as a strategic asset. Companies that can offer unique datasets—anonymized and aggregated—are creating new revenue streams while improving their core products through machine learning.

7. Privacy-First and Agentic Governance

As AI agents gain autonomy and access to sensitive systems, governance and trust frameworks become competitive differentiators. The March 2026 acquisition of BetterCloud by CoreStack to create a unified Agentic Governance OS signals the market’s direction—companies need visibility, automation, policy enforcement, and compliance across cloud, SaaS, and AI systems.

Privacy-first data practices are emerging as key differentiators, particularly in European markets with strict GDPR enforcement and in enterprise segments with complex compliance requirements. SaaS vendors that can demonstrate robust data governance are winning deals against competitors with more cavalier approaches.

Key Players and Competitive Landscape

The SaaS market remains highly fragmented, with different vendors leading each major segment. However, several companies have established dominant positions that shape competitive dynamics across the industry:

Microsoft leads the overall enterprise SaaS market, leveraging its Office 365 and Azure ecosystems to drive comprehensive platform adoption. The company’s strategy of integrating AI capabilities across its entire product suite through Copilot has created a formidable competitive moat. Microsoft’s collaboration tools, particularly Teams, have achieved dominant market share, making it the default choice for enterprise communication.

Salesforce remains the undisputed leader in CRM, with its platform approach extending into marketing automation, customer service, and analytics. The company’s acquisition strategy—most notably the $27.7 billion purchase of Slack—has created an integrated ecosystem that competes directly with Microsoft’s offerings. Salesforce’s AppExchange marketplace, with thousands of third-party integrations, reinforces its platform lock-in.

Adobe dominates creative and document workflows through its Creative Cloud and Document Cloud offerings. The company’s successful transition from perpetual licenses to subscription models serves as a blueprint for traditional software vendors. Adobe’s AI initiatives, particularly Firefly for generative AI in creative workflows, position it well for the next generation of creative tools.

ServiceNow has established itself as the leader in IT service management and is expanding into HR, customer service, and workflow automation. The company’s focus on enterprise-grade solutions for complex organizations has created high switching costs and strong retention metrics.

Snowflake and Datadog represent the new generation of data-focused SaaS leaders. Snowflake’s data cloud platform has become the standard for enterprise data warehousing and analytics, while Datadog’s observability platform dominates monitoring and analytics for cloud-native applications. Both companies demonstrate the power of usage-based pricing models aligned with customer data growth.

HubSpot has emerged as the leading SMB-focused CRM and marketing platform, successfully competing with Salesforce in the mid-market through simpler pricing, easier implementation, and strong inbound marketing practices. The company’s freemium model has proven highly effective at capturing early-stage companies that grow into significant accounts.

Zoom, despite post-pandemic normalization, remains the default video conferencing solution for businesses worldwide. The company’s expansion into phone systems, contact center, and AI-powered meeting assistants represents its strategy to become a comprehensive communications platform.

CrowdStrike leads the cybersecurity SaaS segment, with its cloud-native endpoint protection platform achieving dominant market share. The company’s threat intelligence network creates a data flywheel that improves protection for all customers as the network grows.

Emerging challengers include Notion for workplace collaboration, Figma for design (now part of Adobe), Canva for democratized design, and a host of AI-native startups challenging incumbents with specialized, intelligent solutions. The market’s fragmentation means there is no single dominant player—rather, a constellation of leaders across different categories and customer segments.

Challenges and Pain Points

Despite the industry’s robust growth, SaaS companies face significant challenges that are intensifying as the market matures:

1. The AI Valuation Trap

SaaS valuations hit decade-plus lows in Q1 2026 as markets priced AI as an existential threat to traditional software. Growth-adjusted multiples reveal potential lingering vulnerability, and the market is painting all SaaS companies with the same brush rather than distinguishing potential winners from losers.

Companies without clear AI strategies face valuation discounts, while those with AI narratives may find expectations difficult to meet. The median ARR multiple for public SaaS companies has compressed significantly, creating a challenging environment for fundraising and M&A.

2. Customer Acquisition Cost Inflation

The New CAC Ratio for new customers continues to rise—14% higher in 2024—and shows no signs of reversing. As competition intensifies and digital advertising costs increase, acquiring new customers becomes progressively more expensive. This dynamic favors companies with strong organic growth engines, established brands, and effective product-led growth strategies.

The Blended CAC Ratio was down 10% due to the increase in Expansion ARR to New ARR mix, highlighting the importance of customer success and expansion in maintaining efficient growth. Companies that can grow through existing customers are weathering the CAC inflation storm better than those dependent on new logo acquisition.

3. SaaS Sprawl and Consolidation Pressure

With companies using an average of 106 SaaS applications, managing this sprawl has become a critical mandate for both IT and finance teams. The rise of SaaS management platforms reflects the need for visibility, automation, policy enforcement, compliance, and spend optimization across complex portfolios.

While the consolidation rate has dropped to just 5% year-over-year, pressure is mounting for rationalization. Vendors that cannot demonstrate clear, differentiated value face replacement by broader platforms or point solutions with stronger ROI.

4. Retention and Churn Challenges

With median Net Revenue Retention at just 101%, retaining and expanding existing customers is becoming more challenging. The silent killer of recurring revenue—churn—remains a persistent threat, particularly in competitive categories with low switching costs.

Multiple interactions and channels make it essential to deliver consistent, high-quality experiences across all touchpoints. Customers engage with products through onboarding, support, product updates, and community forums—any breakdown in this experience can trigger churn.

5. AI Integration Complexity

While AI presents enormous opportunities, integrating AI capabilities into existing products is technically complex and resource-intensive. Companies must invest in data infrastructure, model training, and governance frameworks while maintaining core product quality.

The shift from AI experimentation to production-ready platforms requires observable, governable, cost-controlled systems that can operate continuously under real user load. Many companies are discovering that AI features that demo well struggle to deliver consistent value at scale.

Opportunities and Growth Strategies

Amidst these challenges, significant opportunities exist for SaaS companies that execute the right strategies:

1. AI-Powered Personalization at Scale

AI-powered personalization, now accessible to mid-market companies, can boost conversion rates by 202%. The key is moving beyond basic recommendation engines to truly intelligent systems that adapt to individual user behavior, preferences, and contexts.

Companies that can deliver personalized experiences without requiring extensive user configuration will capture significant market share. The goal is software that feels like it was built specifically for each user, automatically.

2. Product-Led Growth with AI Assistants

Product-led growth models that let the product sell itself are being enhanced by AI assistants that guide users to value faster. With 81% of B2B buyers making vendor decisions before engaging sales teams, the product experience is increasingly the primary sales channel.

AI agents in SaaS marketing function as autonomous team members rather than simple tools. They can qualify leads, provide personalized demos, and even handle initial onboarding—scaling customer acquisition without proportional increases in headcount.

3. Vertical Market Deepening

The success of vertical SaaS companies demonstrates the value of deep industry expertise. Opportunities exist in virtually every vertical—from construction and agriculture to legal and healthcare—where general-purpose tools fail to address industry-specific workflows and compliance requirements.

The playbook is clear: identify a vertical with sufficient market size, build deep functionality that horizontal players cannot easily replicate, and establish category leadership before competitors recognize the opportunity.

4. Ecosystem and Partnership Strategies

Ecosystem partnerships extend reach without expanding headcount. Companies that can integrate seamlessly with the tools their customers already use—becoming part of a larger workflow rather than an isolated application—achieve higher retention and faster growth.

The most successful SaaS companies of 2026 are those that have built robust integration ecosystems, making their platforms the central hub for business operations. This creates powerful network effects and high switching costs.

Case Studies and Success Stories

Real-world examples illustrate the strategies driving SaaS success in 2026:

Case Study 1: NeuroFlow AI – $0 to $100M ARR in 18 Months

NeuroFlow AI transformed $500K in seed funding into $100M ARR in just 18 months by making AI agents the core product rather than a feature. Their strategy centered on a viral freemium tier: any user could create a basic agent for free, but sharing it with 3+ team members unlocked collaborative features.

This approach created organic network effects within organizations, as individual users became advocates for broader adoption. The product-led growth engine was enhanced by AI-powered onboarding that personalized the first-use experience based on user role and industry.

Key lesson: When AI is the product, not a feature, distribution models must change. Traditional sales processes are too slow for AI-native products that demonstrate value immediately.

Case Study 2: EcoTrack Analytics – Bootstrapped to $20M ARR

EcoTrack Analytics achieved $20M ARR without venture capital by weaponizing community-driven customer acquisition in the sustainability niche. Rather than competing for expensive paid advertising keywords, they built a passionate community of sustainability professionals who became product advocates.

The company’s content strategy focused on educational resources that helped sustainability professionals advance their careers, creating goodwill and brand authority. This community-first approach generated high-quality referrals at minimal cost.

Key lesson: In crowded markets, community-driven acquisition can outperform paid channels while building durable competitive advantages.

Case Study 3: Slack – From Internal Tool to $27.7B Acquisition

While Slack’s acquisition by Salesforce occurred before 2026, its growth trajectory remains instructive. The company transformed team collaboration by creating a centralized hub for messaging, file sharing, and app integrations. By connecting with tools like Google Drive and Trello, Slack became the “command center” for productivity.

The integration ecosystem was critical to Slack’s success—users didn’t just adopt a chat tool, they adopted a platform that connected their entire workflow. This created powerful lock-in as teams built their operations around Slack channels and integrations.

Key lesson: Simplicity and integration are key to SaaS success. The best products solve real problems while seamlessly connecting with the tools users already rely on.

Future Outlook and Predictions (2027-2030)

The SaaS market’s trajectory through 2030 will be shaped by several converging forces:

Market Size Projections

By 2030, the global SaaS market is projected to reach between $819 billion and $1.37 trillion, depending on the forecasting methodology. The most aggressive projections suggest the market could approach $1.58 trillion by 2031, representing a nearly fourfold increase from 2026 levels.

This growth will be driven by continued cloud adoption in emerging markets, the proliferation of AI-native applications, and the expansion of SaaS into new categories previously served by on-premises software or manual processes.

The AI Transformation

By 2027, AI capabilities will be table stakes rather than differentiators. The question will not be whether a SaaS product uses AI, but how effectively it applies AI to solve customer problems. Companies that have built AI-native architectures will have significant advantages over those retrofitting AI into legacy codebases.

Agentic AI—systems that can autonomously perform complex tasks—will move from experimental to production-ready, fundamentally changing how businesses operate. SaaS platforms will increasingly function as autonomous team members rather than tools requiring human operation.

Market Consolidation

The fragmented SaaS landscape will see significant consolidation as larger players acquire specialized solutions to round out their platforms. The SaaS management market alone is projected to grow from $4.58 billion in 2025 to $9.37 billion by 2030, reflecting the need for governance across sprawling SaaS portfolios.

Private equity will play an increasingly important role, taking public SaaS companies private to restructure for long-term profitability rather than growth-at-all-costs. This shift will prioritize sustainable unit economics over top-line growth.

Regional Shifts

While North America will remain the largest market, Asia-Pacific will capture an increasing share of global SaaS spending. India, in particular, is emerging as both a major market and a hub for SaaS innovation, with domestic companies expanding globally.

European markets will continue growing rapidly, driven by digital transformation mandates and increasing comfort with cloud solutions among traditionally conservative industries.

Key Takeaways

- The global SaaS market reached $465.03 billion in 2026 and is projected to grow to $1.37 trillion by 2035 at a 12.85% CAGR

- AI-native SaaS is becoming the default, with the AI-Created SaaS segment growing at 39.6% CAGR and reaching $1.05 trillion by 2033

- Vertical SaaS solutions are commanding premium valuations, with median Series A sizes of $22M compared to $15M for horizontal SaaS

- Usage-based pricing is going mainstream as customers demand to pay for outcomes rather than access

- Customer acquisition costs continue rising (up 14% year-over-year), making retention and expansion critical for efficient growth

- The average company uses 106 SaaS applications, creating opportunities for consolidation and orchestration platforms

- Top performers achieve Net Revenue Retention above 120% through proactive customer success and expansion strategies

- North America leads in absolute terms, but Asia-Pacific is the fastest-growing region with 21.4% market share

Sources and Citations

- Precedence Research – Software As A Service (SaaS) Market Size, Share, and Trends 2026 to 2035: https://www.precedenceresearch.com/software-as-a-service-market

- The Business Research Company – Software As A Service Global Market Report 2026: https://www.thebusinessresearchcompany.com/report/software-as-a-service-global-market-report

- Mordor Intelligence – B2B SaaS Market Size & Share Analysis: https://www.mordorintelligence.com/industry-reports/b2b-saas-market

- Zylo – 175+ Unmissable SaaS Statistics for 2026: https://zylo.com/blog/saas-statistics

- BetterCloud – 147 SaaS Statistics for 2026: https://www.bettercloud.com/monitor/saas-statistics

- SaaS Capital – 2026 Benchmarking Metrics for Bootstrapped SaaS Companies: https://www.saas-capital.com/blog-posts/benchmarking-metrics-for-bootstrapped-saas-companies

- Coherent Market Insights – AI Created SaaS Market Trends: https://www.coherentmarketinsights.com/industry-reports/ai-created-saas-market

- Synergy Research Group – Microsoft Leads in SaaS

Deep Dive: Regional SaaS Market Analysis

Understanding the global SaaS market requires examining regional dynamics that shape adoption patterns, competitive landscapes, and growth trajectories. Each major region presents unique opportunities and challenges for SaaS vendors.

North America: The Mature Market Leader

North America, particularly the United States, remains the epicenter of the global SaaS industry. With approximately $187 billion in annual SaaS revenue, the region accounts for roughly 40% of global spending. This dominance stems from several factors: early cloud adoption, a mature venture capital ecosystem, and the headquarters location of most major SaaS vendors.

The U.S. market is characterized by high enterprise maturity, with organizations using an average of 110+ SaaS applications. Competition is fierce across all categories, with established players defending market share against well-funded challengers. The region leads in AI adoption, with 68% of enterprises reporting active AI initiatives within their SaaS portfolios.

Canada represents a smaller but significant market, with particular strength in fintech SaaS and AI research. Canadian companies benefit from proximity to U.S. markets while operating in a more favorable regulatory environment for data privacy.

Europe: Regulatory-Driven Growth

Western Europe is the fastest-growing major SaaS market, driven by digital transformation mandates and regulatory requirements. The General Data Protection Regulation (GDPR) has created both challenges and opportunities—vendors that can demonstrate robust compliance capabilities command premium pricing and win enterprise deals.

The European market values data sovereignty, creating opportunities for regional cloud providers and SaaS vendors with European data centers. Countries like Germany, the UK, France, and the Netherlands lead in enterprise adoption, while Eastern European markets show strong growth potential as digital infrastructure improves.

European SaaS buyers prioritize security, compliance, and vendor stability over cutting-edge features. This preference favors established vendors and creates barriers for new entrants lacking enterprise credibility.

Asia-Pacific: The Growth Engine

Asia-Pacific represents the future of SaaS growth. Currently holding 21.4% of global market share, the region is projected to grow at nearly double the rate of North America through 2035. India, in particular, is emerging as both a major market and a global SaaS innovation hub.

India’s SaaS ecosystem has produced global leaders like Zoho, Freshworks, and BrowserStack, demonstrating the region’s capability to build world-class software. The country’s large English-speaking workforce, strong engineering talent, and growing domestic market create ideal conditions for SaaS innovation.

Southeast Asian markets including Singapore, Indonesia, and Vietnam show explosive growth as mobile-first economies leapfrog traditional software adoption patterns. These markets favor SaaS solutions designed for mobile devices and low-bandwidth environments.

China presents a unique case—a massive market largely closed to Western SaaS vendors due to regulatory restrictions and local competition. Chinese SaaS companies like DingTalk, Feishu, and Tencent Meeting dominate domestically while beginning to expand internationally.

Latin America and Middle East: Emerging Opportunities

Latin America is experiencing rapid SaaS adoption as digital payments infrastructure matures and internet penetration increases. Brazil and Mexico lead the region, with particular strength in fintech and e-commerce SaaS. The region’s young, mobile-first population creates opportunities for innovative SaaS solutions.

The Middle East, particularly the UAE and Saudi Arabia, is investing heavily in digital transformation as part of economic diversification efforts. Government initiatives and sovereign wealth fund investments are accelerating SaaS adoption across public and private sectors.

SaaS Pricing Evolution: From Seats to Value

The SaaS pricing landscape is undergoing its most significant transformation since the shift from perpetual licenses to subscriptions. The traditional per-seat model, while still dominant, is increasingly supplemented or replaced by alternative pricing approaches better aligned with customer value.

Usage-Based Pricing Models

Usage-based pricing aligns vendor revenue with customer success. Rather than charging for access, vendors charge for actual consumption—API calls, data processed, transactions handled, or compute resources consumed. This model reduces friction in the sales process by lowering initial commitment and creates natural expansion revenue as customers grow.

Snowflake pioneered usage-based pricing in the data warehouse category, charging by compute consumption rather than data storage. This approach has proven highly successful, with the company achieving $3 billion in annual revenue and demonstrating that customers will embrace variable pricing when it aligns with value.

Challenges with usage-based pricing include revenue predictability, customer anxiety about runaway costs, and the need for sophisticated metering infrastructure. Vendors must provide clear cost visibility and controls to prevent bill shock and maintain customer trust.

Outcome-Based Pricing

The most customer-aligned pricing model charges for outcomes rather than usage. A sales automation platform might charge per meeting booked. A recruiting tool might charge per hire made. A marketing platform might charge per qualified lead generated.

Outcome-based pricing requires vendors to have confidence in their product’s ability to deliver results and the measurement infrastructure to track those results accurately. When executed well, it creates perfect alignment between vendor and customer interests.

Hybrid and Freemium Models

Most successful SaaS companies now employ hybrid pricing that combines elements of multiple models. A typical structure might include a free tier for individual users, a seat-based tier for small teams, and usage-based pricing for enterprise customers with variable needs.

Freemium remains a powerful acquisition strategy, with companies like Notion, Figma, and Slack using free tiers to drive viral adoption and organic growth. The key is designing free tiers that provide genuine value while creating clear upgrade paths to paid features.

The Role of AI in SaaS: Beyond the Hype

Artificial intelligence has moved from marketing buzzword to core infrastructure in SaaS products. However, the reality of AI integration is more nuanced than the hype suggests. Understanding where AI creates genuine value versus where it adds complexity is critical for SaaS strategy.

AI-Native vs. AI-Enhanced

AI-native SaaS companies build their entire product architecture around AI capabilities. These products cannot function without AI and leverage it for core functionality. Examples include AI coding assistants, generative design tools, and autonomous customer service platforms.

AI-enhanced SaaS adds AI capabilities to existing products—smart email sorting in a CRM, predictive churn scoring in a customer success platform, or automated transcription in a meeting tool. These enhancements improve user experience and productivity but do not fundamentally change the product’s core value proposition.

The market is rewarding AI-native companies with premium valuations—40% higher than traditional SaaS—but these companies also face higher expectations and technical complexity.

Agentic AI: The Next Frontier

Agentic AI refers to systems that can autonomously perform complex, multi-step tasks rather than simply responding to individual prompts. These agents can plan, execute, and adapt based on changing conditions—functioning more like autonomous team members than tools.

Early applications include autonomous sales development representatives that can research prospects, craft personalized outreach, and manage follow-up sequences without human intervention. Customer service agents that can resolve complex issues by accessing multiple systems and executing actions on behalf of users.

The technical challenges of agentic AI are significant—ensuring reliability, maintaining security, and providing appropriate human oversight. However, the potential impact on productivity and labor costs is transformative.

Conclusion: Navigating the SaaS Landscape in 2026

The SaaS market in 2026 presents both unprecedented opportunities and significant challenges. The $465 billion market is projected to nearly triple by 2035, creating enormous value for companies that can navigate the evolving landscape successfully.

Success requires balancing multiple imperatives: integrating AI capabilities without losing focus on core value, managing rising customer acquisition costs through retention and expansion, and differentiating in an increasingly crowded market. Companies that execute well on these dimensions will capture disproportionate value in the growing market.

For SaaS buyers, the abundance of options creates both opportunity and complexity. The key is building integrated technology stacks that deliver genuine productivity improvements while managing costs and risks. The rise of SaaS management platforms reflects the growing recognition that technology portfolio management is a core competency for modern businesses.

As we look toward 2030, the SaaS industry will continue evolving. AI will become table stakes, vertical solutions will capture increasing share, and new pricing models will align vendor success with customer outcomes. The companies that thrive will be those that adapt to these changes while maintaining focus on delivering genuine value to their customers.