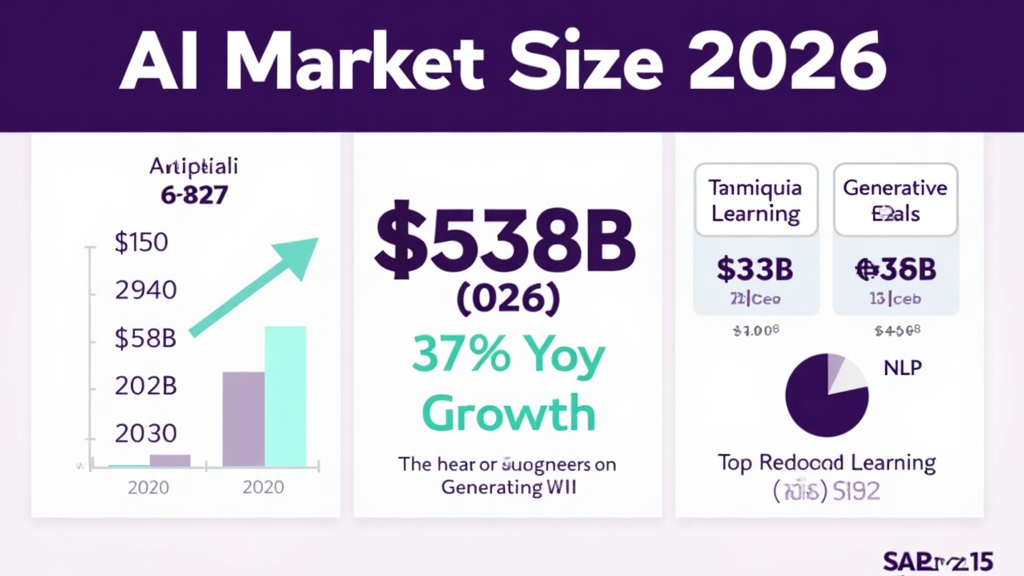

The artificial intelligence market has reached an inflection point in 2026. What started as experimental technology has transformed into a $538 billion global industry, growing at a staggering 37.3% year-over-year rate. For businesses, investors, and technologists, understanding the AI landscape isn’t optional anymore—it’s essential for survival in an increasingly AI-driven economy.

Consider this: in 2024, the global AI market was valued at $244 billion. By 2025, it had grown to $312 billion. Now, in 2026, we’ve nearly doubled that figure. This isn’t gradual growth—it’s an explosion that’s reshaping every industry from healthcare to finance, from manufacturing to creative services. The companies that master AI today will define the business landscape of 2030 and beyond.

The transformation we’re witnessing isn’t just about technology—it’s about the fundamental restructuring of how value is created in the global economy. AI is becoming the new electricity, a general-purpose technology that will touch every aspect of business and society. Organizations that fail to adapt risk becoming obsolete, while those that embrace AI strategically are positioning themselves for unprecedented growth and competitive advantage.

The implications of this growth extend far beyond the technology sector. Every industry is being transformed by AI capabilities. In healthcare, AI is accelerating drug discovery and enabling personalized medicine. In finance, AI powers algorithmic trading, fraud detection, and risk assessment. In manufacturing, AI optimizes supply chains and predicts equipment failures before they happen. In retail, AI personalizes shopping experiences and optimizes inventory management. The pattern is consistent: AI is becoming the competitive advantage that separates market leaders from laggards.

What makes this moment particularly significant is the convergence of several factors. Computing power has reached levels where training massive AI models is economically viable. Data availability has exploded, providing the raw material for AI systems to learn from. Algorithmic breakthroughs, particularly in transformer architectures and reinforcement learning, have dramatically improved AI capabilities. And perhaps most importantly, user interfaces have evolved to make AI accessible to non-technical users. The result is a technology that has moved from research curiosity to practical utility in record time.

Market Overview: The $538 Billion AI Ecosystem

The global artificial intelligence market has evolved from a niche technology sector into one of the most significant economic forces of our time. According to Grand View Research, the AI market reached $390.91 billion in 2025 and is expected to hit $539.45 billion in 2026. Other analysts paint an even more aggressive picture—Noizz.io reports the market has already reached $538 billion with a 37.3% compound annual growth rate.

To understand the magnitude of this growth, we need to look at the trajectory. In 2020, the AI market was valued at approximately $150 billion. By 2024, it had grown to $244 billion. The acceleration we’re seeing in 2026 represents a fundamental shift in how businesses and consumers adopt AI technologies. What was once the domain of tech giants and research institutions is now accessible to small businesses, individual developers, and enterprises across every sector.

The market segmentation reveals where the value is being created. Generative AI alone represents $136 billion of the total market—a segment that barely existed three years ago. Machine learning continues to be the backbone of AI applications, while natural language processing has become critical for customer service, content creation, and business intelligence. Computer vision is revolutionizing manufacturing, healthcare diagnostics, and autonomous systems.

Looking ahead, the projections are even more ambitious. Grand View Research forecasts the AI market will reach $3.5 trillion by 2033. This represents a compound annual growth rate that would make AI one of the fastest-growing industries in history. For context, that’s larger than the current GDP of most countries. The AI market isn’t just growing—it’s becoming the economy itself.

Geographic distribution shows the United States maintaining leadership with an estimated market value of $47 billion, according to Exploding Topics. However, China, the European Union, and emerging markets are investing heavily to close this gap. The OECD reports that AI venture capital investments reached $258.7 billion in 2025, representing 61% of all global VC investment—a concentration that shows both the opportunity and the risk in this market.

The regional dynamics of AI development are fascinating. The United States continues to lead in foundational research and venture capital investment, with Silicon Valley remaining the epicenter of AI innovation. However, China is rapidly closing the gap, with massive government investment in AI research and development, and a domestic market that provides enormous amounts of training data. The European Union is taking a different approach, focusing on regulatory frameworks and ethical AI development, which could give European companies a competitive advantage in privacy-conscious markets.

Key Statistics and Data Points

The numbers behind the AI market tell a story of unprecedented growth and transformation. Here are the critical statistics that define the AI landscape in 2026:

Market Size and Growth: The global AI market is valued at $538 billion in 2026, growing at 37.3% year-over-year. The generative AI segment alone reached $136 billion. By 2033, the total AI market is projected to reach $3.5 trillion. The U.S. AI market specifically is worth approximately $47 billion and is projected to reach $851 billion by 2034.

Investment and Funding: AI venture capital investments totaled $258.7 billion in 2025, representing 61% of all global VC investment according to OECD data. Foundation model companies raised $80 billion in 2025 alone, accounting for 40% of global AI funding. AI funding to foundational startups doubled in Q1 2026 compared to all of 2025. AI now represents 35% of NYC VC funding and 30% of UK VC funding.

Adoption and Usage: 35.49% of people now use AI tools every day, according to Exploding Topics research. Nearly 1.8 billion people have used some kind of AI tool. 100% of industries are increasing AI usage according to PwC. 63% of AI users turn to the technology for research and question-answering. Cooking and meal planning is the top “life situation” AI use case.

Enterprise Impact: According to NVIDIA’s State of AI Report 2026, 99% of telecommunications respondents said AI helped improve employee productivity, with a quarter reporting major or significant improvements. AI is driving revenue increases across every industry vertical, with particular strength in financial services, retail, and healthcare. Cost reduction through AI implementation is now measurable and significant across enterprise deployments.

Technology Segments: The generative AI market, valued at $16.87 billion in 2024, is projected to reach $109.37 billion by 2030, growing at a CAGR of 37.9%. Machine learning remains the largest segment by revenue. Natural language processing is the fastest-growing application area. The wearable AI market is expected to reach $303 billion by 2035.

Workforce Transformation: AI is creating new job categories while transforming existing ones. The demand for AI skills has created a talent shortage that companies are addressing through upskilling programs and strategic hiring. AI-related roles command premium salaries, with machine learning engineers, AI researchers, and data scientists among the highest-paid technology professionals.

Industry-Specific Adoption: Healthcare AI is projected to reach $148 billion by 2030, with applications in drug discovery, diagnostics, and personalized medicine. Financial services AI spending reached $29 billion in 2024 and is expected to grow to $144 billion by 2030. Manufacturing AI is driving efficiency gains of 20-30% in early-adopting companies. Retail AI is transforming everything from inventory management to customer personalization.

Consumer Behavior: The adoption of AI tools by consumers has been remarkably rapid. ChatGPT reached 100 million users in just two months—the fastest-growing consumer application in history. This rapid adoption has created a massive market for AI-powered consumer applications, from writing assistants to image generators to personal productivity tools. The consumer AI market is expected to be a major growth driver in the coming years.

Regional Market Distribution: North America leads the global AI market with approximately 40% market share, driven by significant investments from tech giants and a robust startup ecosystem. The Asia-Pacific region is the fastest-growing market, with China investing heavily in AI research and development as part of its national strategy. Europe represents about 20% of the global market, with strong adoption in manufacturing, automotive, and financial services. Emerging markets in Latin America, Middle East, and Africa are showing accelerating adoption, though from a smaller base.

AI Infrastructure Investment: Data center construction for AI workloads reached $150 billion globally in 2025. Cloud providers invested $80 billion in AI-specific infrastructure. NVIDIA’s data center revenue grew to $60 billion annually. Custom AI chip development attracted $20 billion in venture funding. Energy consumption for AI training and inference has become a significant concern, with major providers committing to renewable energy sources for their AI operations.

Major Trends Shaping AI in 2026

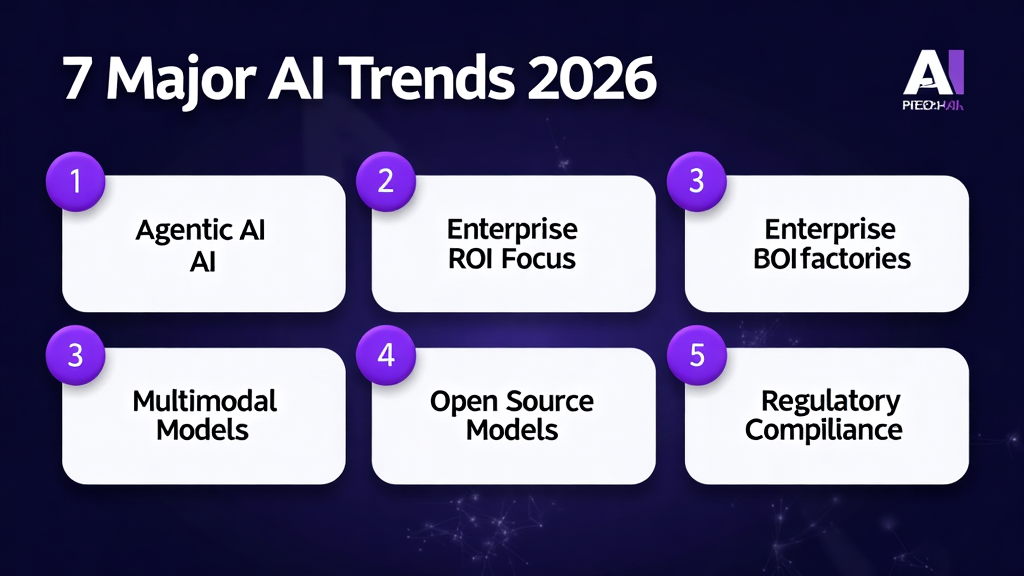

The AI landscape is being reshaped by seven major trends that will define the industry through the remainder of this decade:

1. The Rise of Agentic AI: Agentic AI—systems that can autonomously plan, reason, and execute complex tasks—is moving from research labs to production environments. According to IBM’s 2026 AI predictions, agentic AI and non-human identities will outnumber human users in organizations significantly. These systems don’t just respond to prompts; they take initiative, make decisions, and complete multi-step workflows with minimal human oversight.

The implications of agentic AI are profound. Imagine AI systems that can manage your calendar, book travel, conduct research, draft reports, and coordinate with other AI agents to complete complex projects. This isn’t science fiction—it’s the direction the technology is heading. Companies like Adept, Inflection, and others are building AI agents that can interact with software interfaces, browse the web, and complete tasks that previously required human intervention.

2. Enterprise ROI Focus: The era of AI experimentation is ending. As David Lanstein, CEO of Atolio, told IBM Think: “The most significant trend we see emerging is the shift from AI experimentation and excitement to private and secure deployments with real ROI expectations within enterprises.” Companies are no longer asking “What can AI do?” but “What will AI deliver for our bottom line?”

This shift is changing how AI projects are evaluated and funded. CIOs and CFOs are demanding clear metrics, pilot programs with defined success criteria, and phased rollouts that demonstrate value before major investments. The “vibe coding” era of AI experimentation is giving way to disciplined, ROI-focused implementations.

3. AI Superfactories: Microsoft predicts the rise of flexible, global AI systems—linked AI “superfactories” that will drive down costs and improve efficiency. These massive data center complexes, connected by high-speed networks, represent the infrastructure layer that will make advanced AI accessible at consumer price points.

The scale of these investments is staggering. Microsoft, Google, Amazon, and others are investing tens of billions of dollars in AI infrastructure. These aren’t just data centers—they’re specialized facilities designed specifically for AI training and inference, with custom chips, high-bandwidth networking, and massive power requirements.

4. Multimodal AI Models: The boundaries between text, image, audio, and video AI are dissolving. Leading models now seamlessly work across modalities, enabling applications that were science fiction just two years ago. This convergence is creating entirely new product categories and user experiences.

GPT-4V, Gemini, and Claude can now process and generate content across text, images, and code. This enables applications like automated video editing, intelligent document processing, and creative tools that understand context across media types. The next generation of AI applications will be inherently multimodal.

5. Open Source AI Revolution: Open-source models like DeepSeek-R1 and Meta’s Llama series are challenging proprietary systems. This democratization is accelerating innovation while creating new competitive dynamics. Companies can now deploy state-of-the-art AI without paying premium API fees.

The open-source movement is particularly significant for enterprises concerned about data privacy and vendor lock-in. By running open-source models on their own infrastructure, companies can maintain control over their data while still benefiting from cutting-edge AI capabilities.

6. AI Workforce Integration: AI is becoming a standard tool across all job functions, not just technical roles. From marketing to legal, from finance to HR, professionals are expected to have AI literacy. This is creating a divide between AI-enabled workers and those being left behind.

The transformation of work is perhaps the most profound impact of AI. Tasks that once required hours of human effort can now be completed in minutes with AI assistance. This is changing job descriptions, performance expectations, and career trajectories across every industry.

7. Regulatory Compliance: The EU AI Act and similar regulations worldwide are creating a new compliance layer for AI deployment. Companies must now navigate safety requirements, transparency obligations, and liability frameworks. This is increasing costs but also creating competitive moats for compliant organizations.

The regulatory landscape is complex and evolving. The EU AI Act categorizes AI systems by risk level, with different requirements for each category. High-risk AI systems, such as those used in healthcare, transportation, and criminal justice, face the strictest requirements. Companies operating globally must navigate a patchwork of regulations.

Key Players and Competitive Landscape

The AI market is dominated by a select group of companies that combine technological expertise with massive computational resources and data access. Understanding this competitive landscape is essential for anyone looking to invest in, partner with, or compete against these players.

NVIDIA: The undisputed leader in AI infrastructure, NVIDIA’s GPUs power the majority of AI training and inference workloads. The company’s revenue has exploded alongside the AI boom, with data center revenue becoming its primary business. NVIDIA isn’t just selling chips—it’s building an ecosystem of software, libraries, and developer tools that create switching costs for customers.

NVIDIA’s competitive position is remarkably strong. The company’s CUDA platform has become the standard for AI development, creating a massive moat around its hardware business. Competitors like AMD and Intel are trying to break through, but NVIDIA’s software ecosystem gives it a significant advantage.

Microsoft: Through its strategic partnership with OpenAI and integration of AI across its product suite, Microsoft has positioned itself as the leading enterprise AI provider. Azure’s AI services, GitHub Copilot, and Microsoft 365 Copilot are generating significant revenue while locking customers into the Microsoft ecosystem. The company is investing billions in AI infrastructure, including the development of AI superfactories.

Microsoft’s partnership with OpenAI has been transformative for both companies. Microsoft gets access to cutting-edge AI models, while OpenAI gets the compute resources and distribution channels it needs to scale. This partnership has put Microsoft at the center of the AI revolution.

Alphabet (Google): Google’s DeepMind and Google AI research divisions continue to produce breakthrough models. The company’s advantage in search and advertising data, combined with its cloud infrastructure, makes it a formidable competitor. Google’s Gemini models are competitive with OpenAI’s offerings, and the company’s Android platform provides a massive distribution channel for AI applications.

Google’s position is paradoxical. The company has some of the best AI research in the world, but it’s also the most threatened by AI disruption. If AI chatbots replace search, Google’s core business is at risk. The company is racing to integrate AI into its products while defending its search dominance.

OpenAI: The creator of ChatGPT and the GPT model series, OpenAI has become synonymous with generative AI. Despite being a relatively young company, its models power millions of applications and its API business is growing rapidly. The company’s challenge is maintaining its technical lead while scaling its business operations.

OpenAI’s trajectory has been remarkable. From a research lab to a $80+ billion company in just a few years, OpenAI has defined the generative AI category. The company’s challenge now is to convert its technical leadership into sustainable business advantage.

Amazon (AWS): Amazon’s cloud platform offers the broadest suite of AI services, from foundational models to specialized applications. AWS’s market leadership in cloud computing gives it a natural advantage in AI deployment. The company’s Bedrock platform allows enterprises to access multiple foundation models through a single API.

Amazon’s approach is to be the “everything store” for AI. Rather than betting on a single model or approach, AWS offers customers choice and flexibility. This strategy has made AWS the platform of choice for enterprises that want to avoid vendor lock-in.

Meta: While Meta’s AI investments are less visible than some competitors, the company’s open-source Llama models have been downloaded hundreds of millions of times. Meta’s AI research is focused on applications for its social platforms, including content recommendation, moderation, and creation tools.

Meta’s open-source strategy is a clever competitive move. By releasing high-quality open-source models, Meta is commoditizing the foundation model layer and shifting competition to applications and distribution—areas where Meta has advantages.

Anthropic: Founded by former OpenAI researchers, Anthropic has positioned itself as the safety-focused AI company. Its Claude models are competitive with GPT-4 and are particularly strong in reasoning and safety. The company has raised billions in funding and is focused on enterprise applications.

Anthropic’s focus on AI safety and constitutional AI has resonated with enterprises concerned about the risks of AI deployment. The company’s Claude models are known for being helpful, harmless, and honest—a positioning that differentiates it from competitors.

IBM: IBM’s Watson platform and AI consulting services make it a significant player in enterprise AI deployment. The company’s focus is on practical AI applications for large organizations, particularly in regulated industries like healthcare and finance.

IBM’s approach is to focus on the “boring” but valuable applications of AI—document processing, customer service automation, and business process optimization. This pragmatic approach has made IBM a trusted partner for enterprises navigating AI adoption.

Challenges and Pain Points

Despite the tremendous growth and opportunity, the AI industry faces significant challenges that could slow adoption or create risks for businesses and society.

Data Quality and Management: AI systems are only as good as the data they’re trained on. Poor data quality, biased training sets, and data governance failures are leading causes of AI project failures. Organizations struggle to clean, label, and manage the massive datasets required for modern AI systems. According to S3Corp, data management breakdowns are one of the five recurring patterns of enterprise AI failure.

The data challenge is multifaceted. Organizations need to collect the right data, clean it, label it, and ensure it’s representative of the real-world scenarios the AI will encounter. This process is time-consuming, expensive, and often underestimated in AI project planning.

AI Talent Shortage: There simply aren’t enough qualified AI engineers, data scientists, and ML operations specialists to meet demand. This talent gap is driving up costs and slowing deployment timelines. Companies are competing fiercely for a limited pool of experienced AI professionals, with salaries reaching unprecedented levels.

The talent shortage is particularly acute for specialized roles like AI infrastructure engineers, ML operations specialists, and AI safety researchers. Universities are ramping up AI programs, but it will take years for the supply of talent to catch up with demand.

Security and Privacy Risks: AI systems introduce new attack surfaces and vulnerabilities. Data privacy concerns are particularly acute in regulated industries. The risk of AI systems being manipulated, poisoned, or exploited is a growing concern for security professionals. Model theft and intellectual property protection are emerging as critical issues.

AI security is a new frontier. Traditional security practices don’t address the unique risks of AI systems, such as adversarial attacks, data poisoning, and model inversion. Organizations need to develop new security capabilities to protect their AI assets.

Integration and Scalability: Moving AI from pilot projects to production-scale deployment is proving difficult for many organizations. Legacy systems, data silos, and organizational resistance create friction. The “last mile” of AI deployment—integrating models into existing workflows—often takes longer than building the models themselves.

The integration challenge is often underestimated. AI models that work well in controlled environments may fail when deployed in complex, real-world systems. Organizations need to invest in ML operations (MLOps) capabilities to manage the AI lifecycle.

Ethical and Bias Concerns: AI systems can perpetuate and amplify existing biases. Hallucinations—confident falsehoods generated by AI—remain a significant problem. The lack of explainability in many AI systems creates accountability challenges. Regulatory frameworks are still evolving, creating compliance uncertainty.

Bias in AI is a particularly thorny issue. AI systems trained on historical data can perpetuate historical biases. Addressing this requires careful attention to training data, model design, and ongoing monitoring—but even with these measures, eliminating bias entirely may be impossible.

Cost and Resource Constraints: Training large AI models requires massive computational resources, putting cutting-edge AI development out of reach for all but the best-funded organizations. Inference costs can scale unpredictably with usage. The energy consumption of AI data centers is creating sustainability concerns.

The cost of AI development is staggering. Training a large language model can cost tens of millions of dollars in compute alone. This concentration of resources among a few large players raises concerns about competition and innovation.

Opportunities and Growth Strategies

For businesses looking to capitalize on the AI boom, several strategic approaches are proving successful:

Process Optimization: The most immediate ROI from AI comes from automating existing processes. Companies are using AI to analyze vast datasets, identify inefficiencies, and streamline operations. From supply chain optimization to customer service automation, the productivity gains are measurable and significant. According to NetCom Learning, process optimization is one of the primary drivers of AI adoption in 2026.

The key to successful process optimization is identifying the right use cases. Not every process is suitable for AI automation. The best candidates are high-volume, repetitive tasks with clear inputs and outputs—exactly the kind of work that AI excels at.

Customer Experience Transformation: AI-powered personalization, predictive support, and intelligent automation are enabling companies to deliver superior customer experiences at scale. AI can analyze customer interactions to identify trends, predict needs, and proactively address issues. This leads to higher satisfaction, increased loyalty, and improved lifetime value.

Customer experience is a natural fit for AI because it involves processing large amounts of unstructured data—customer interactions, feedback, and behavior patterns. AI can extract insights from this data that would be impossible to find manually.

New Product Development: AI is enabling entirely new categories of products and services. From AI-powered creative tools to intelligent automation platforms, companies are building businesses that wouldn’t have been possible five years ago. The key is identifying problems that AI can solve uniquely well, rather than simply adding AI to existing products.

The most successful AI-native products solve problems that were previously unsolvable or uneconomical to address. They’re not just faster or cheaper versions of existing solutions—they’re fundamentally different approaches.

Strategic Partnerships: Given the complexity and cost of AI development, partnerships are becoming essential. Companies are partnering with AI providers, cloud platforms, and specialized consultancies to accelerate their AI initiatives. The right partnership can provide access to technology, talent, and best practices that would take years to develop internally.

Partnerships can take many forms—from simple API integrations to joint ventures to strategic investments. The key is finding partners whose strengths complement your own and whose interests align with yours.

Workforce Upskilling: The most successful AI implementations are accompanied by comprehensive training programs. Companies that invest in AI literacy across their workforce see better adoption and more innovative use cases. This isn’t just about technical training—it’s about helping employees understand how AI can augment their work.

Upskilling is particularly important because AI is changing the nature of work itself. Employees need to learn how to work alongside AI systems, how to supervise AI outputs, and how to identify opportunities for AI augmentation.

Case Studies and Success Stories

Real-world implementations demonstrate the transformative potential of AI when deployed effectively:

Nasdaq: The global stock exchange built an AI platform using NVIDIA technology to optimize internal operations and enhance external products. The system improves functionality and user experience while streamlining internal work processes. This demonstrates how traditional financial institutions can leverage AI to maintain competitive advantage.

Nasdaq’s implementation shows that AI isn’t just for tech companies. Even established financial institutions can leverage AI to improve operations and create new products. The key is starting with clear objectives and building the right team.

AXA: The insurance giant developed AXA Secure GPT, a platform powered by Azure OpenAI Service that empowers employees to leverage generative AI while maintaining the highest levels of data safety. This approach shows how regulated industries can adopt AI responsibly.

AXA’s approach to AI governance is a model for other regulated industries. By creating a secure, controlled environment for AI use, the company is enabling innovation while managing risk.

UBS: The investment bank leveraged Azure OpenAI Service and Azure AI Search to develop the Legal AI Assistant (LAIA), enabling employees to quickly find information and boosting productivity. This is a prime example of how AI can augment knowledge work in professional services.

UBS’s LAIA system addresses a common pain point in professional services—finding relevant information in vast document repositories. By making this information instantly accessible, AI is transforming how knowledge workers operate.

Sandvik: The engineering company created the Manufacturing Copilot, built with Azure OpenAI and Azure AI Search, to provide easy access to years of product documentation. This demonstrates AI’s potential to unlock institutional knowledge and improve operational efficiency in manufacturing.

Sandvik’s implementation shows how AI can capture and make accessible the tacit knowledge that exists in organizations. This is particularly valuable in manufacturing, where expertise is often concentrated in the minds of experienced workers.

CoreWeave: Using Cohere’s AI platform, CoreWeave transformed its customer support operations in just 90 days. This case shows how quickly AI can deliver results when implemented with clear objectives and the right technology partners.

CoreWeave’s rapid implementation demonstrates that AI projects don’t have to take years. With the right approach and the right partners, companies can see results in months.

Notion: The productivity platform enhanced its workspace search capabilities with Cohere Rerank, demonstrating how AI can improve existing products without requiring complete rebuilds. This approach of incremental AI enhancement is accessible to companies of all sizes.

Notion’s approach shows that AI doesn’t have to be a massive, disruptive project. Incremental improvements using AI can deliver significant value with lower risk.

Future Outlook and Predictions

The trajectory of AI development suggests we’re in the early stages of a transformation that will reshape society over the next decade. Here are the key predictions for AI through 2030:

2027: The Year of AI Agents: By early 2027, AI systems will achieve superhuman coding capabilities according to forecasts from the AI 2027 project. By mid-2027, agentic AI will handle complex multi-step workflows autonomously. This will fundamentally change how software is developed and how businesses operate.

The implications of agentic AI are difficult to overstate. When AI systems can autonomously complete complex tasks, the nature of work changes fundamentally. Knowledge workers will shift from doing work to supervising AI agents, reviewing their outputs, and handling exceptions.

Market Growth: The AI market is projected to reach $757.58 billion by 2026 according to AIStatistics.ai, with some analysts predicting even higher figures. By 2030, the generative AI market alone could reach $109.37 billion. The U.S. AI market is projected to reach $851 billion by 2034.

These projections, if accurate, would make AI one of the largest industries in the world. The economic impact would be comparable to the rise of the internet or mobile computing—but potentially larger and faster.

Enterprise Adoption: By 2027, AI will move from experimental deployments to core business infrastructure for most Fortune 500 companies. The “massive middle of the enterprise bell curve” will transition from experimentation to production-grade systems, according to Tomás Hernando Kofman of Not Diamond.

This transition will be driven by competitive pressure. As early adopters demonstrate the value of AI, laggards will be forced to follow or risk being left behind. The result will be a rapid acceleration of AI adoption across the enterprise landscape.

Workforce Transformation: AI will augment rather than replace most jobs, but the nature of work will change dramatically. Roles will shift toward AI supervision, creative direction, and complex problem-solving. The gap between AI-enabled workers and those without AI skills will widen, creating economic and social challenges.

The workforce transformation will require massive investment in education and training. Governments, educational institutions, and employers will need to work together to ensure workers have the skills they need to thrive in an AI-driven economy.

Regulatory Evolution: By 2030, comprehensive AI regulations will be in place in most major economies. The EU AI Act is just the beginning. These regulations will create compliance costs but also establish standards that enable broader adoption by addressing safety and liability concerns.

The regulatory landscape will continue to evolve as the technology develops. Regulators will need to balance the need for safety and accountability with the need to enable innovation. Getting this balance right will be critical for the continued development of the AI industry.

Technological Convergence: AI will increasingly integrate with other emerging technologies—quantum computing, biotechnology, robotics, and the Internet of Things. This convergence will create capabilities that are difficult to predict from today’s vantage point but will likely include autonomous systems, personalized medicine, and intelligent infrastructure.

The convergence of AI with other technologies will create entirely new industries and transform existing ones. The boundaries between technology sectors will blur as AI becomes a foundational capability across all domains.

AI Safety and Alignment: As AI systems become more capable, safety and alignment research is receiving increased attention and funding. Major AI labs are investing billions in safety research. Governments are establishing AI safety institutes. The AI safety field is evolving from academic research to practical engineering discipline. By 2030, AI safety is expected to be a standard component of AI development, similar to how cybersecurity became standard for software development.

Economic Impact Projections: McKinsey estimates that AI could add $13 trillion to global GDP by 2030. PwC projects that AI will contribute $15.7 trillion to the global economy by 2030. The World Economic Forum predicts that AI will create 97 million new jobs while displacing 85 million, resulting in a net positive of 12 million jobs. These projections suggest that AI will be one of the most significant drivers of economic growth in the coming decade.

Democratization of AI: By 2030, AI capabilities that today require specialized expertise and significant resources will be accessible to small businesses and individual developers. Low-code and no-code AI platforms will enable non-technical users to build AI-powered applications. Open-source models will continue to improve, narrowing the gap with proprietary systems. This democratization will drive innovation across all sectors of the economy.

Key Takeaways

- The global AI market has reached $538 billion in 2026, growing at 37.3% year-over-year, making it one of the fastest-growing industries in history.

- Enterprise AI is shifting from experimentation to ROI-focused deployment, with companies demanding measurable business outcomes from AI investments.

- Agentic AI, multimodal models, and AI superfactories are the key technological trends shaping the industry in 2026.

- NVIDIA, Microsoft, Google, OpenAI, and Amazon dominate the competitive landscape, but open-source alternatives are democratizing access to AI technology.

- Data quality, talent shortage, security risks, and integration challenges remain the primary barriers to AI adoption for most organizations.

- By 2030, AI is projected to be a $3.5 trillion market, fundamentally transforming how businesses operate and how work is performed.

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- Noizz.io – AI Market Size 2026: https://noizz.io/statistics/ai-market-size-2026

- Thunderbit – AI Growth in 2026: 80 Key Statistics: https://thunderbit.com/blog/ai-growth-key-statistics

- AIStatistics.ai – 70+ AI Statistics 2026: https://aistatistics.ai

- OECD – Venture Capital Investments in AI Through 2025: https://www.oecd.org/en/publications/venture-capital-investments-in-artificial-intelligence-through-2025

- IBM – The Trends That Will Shape AI and Tech in 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- Microsoft – What’s Next in AI: 7 Trends to Watch in 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026

- NVIDIA – State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026

- Exploding Topics – 45+ NEW Artificial Intelligence Statistics: https://explodingtopics.com/blog/ai-statistics

- MarketsandMarkets – US Artificial Intelligence Market: https://www.marketsandmarkets.com/ResearchInsight/us-artificial-intelligence-companies.asp

- Statista – Artificial Intelligence Market Leaders: https://www.statista.com/topics/13788/artificial-intelligence-ai-market-leaders

- AI 2027 – AI Forecast Predictions: https://ai-2027.com

Key Takeaways

- The global AI market has reached $538 billion in 2026, growing at 37.3% year-over-year, making it one of the fastest-growing industries in history.

- Enterprise AI is shifting from experimentation to ROI-focused deployment, with companies demanding measurable business outcomes from AI investments.

- Agentic AI, multimodal models, and AI superfactories are the key technological trends shaping the industry in 2026.

- NVIDIA, Microsoft, Google, OpenAI, and Amazon dominate the competitive landscape, but open-source alternatives are democratizing access to AI technology.

- Data quality, talent shortage, security risks, and integration challenges remain the primary barriers to AI adoption for most organizations.

- By 2030, AI is projected to be a $3.5 trillion market, fundamentally transforming how businesses operate and how work is performed.

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- Noizz.io – AI Market Size 2026: https://noizz.io/statistics/ai-market-size-2026

- Thunderbit – AI Growth in 2026: 80 Key Statistics: https://thunderbit.com/blog/ai-growth-key-statistics

- AIStatistics.ai – 70+ AI Statistics 2026: https://aistatistics.ai

- OECD – Venture Capital Investments in AI Through 2025: https://www.oecd.org/en/publications/venture-capital-investments-in-artificial-intelligence-through-2025

- IBM – The Trends That Will Shape AI and Tech in 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- Microsoft – What’s Next in AI: 7 Trends to Watch in 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026

- NVIDIA – State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026

- Exploding Topics – 45+ NEW Artificial Intelligence Statistics: https://explodingtopics.com/blog/ai-statistics

- MarketsandMarkets – US Artificial Intelligence Market: https://www.marketsandmarkets.com/ResearchInsight/us-artificial-intelligence-companies.asp

- Statista – Artificial Intelligence Market Leaders: https://www.statista.com/topics/13788/artificial-intelligence-ai-market-leaders

- AI 2027 – AI Forecast Predictions: https://ai-2027.com