The digital seller landscape has undergone a seismic transformation. In 2026, global ecommerce sales are projected to reach $6.3 trillion, representing a compound annual growth rate of 9.4% from 2023. This isn’t just incremental growth—it’s a fundamental restructuring of how commerce happens worldwide. For entrepreneurs, established businesses, and digital-first brands, understanding this market isn’t optional anymore. It’s survival.

What makes 2026 particularly significant? We’re witnessing the convergence of artificial intelligence, social commerce, and mobile-first shopping behaviors creating unprecedented opportunities for digital sellers. The barriers to entry have never been lower, yet the competition has never been fiercer. This comprehensive analysis dives deep into the $6.3 trillion digital seller ecosystem, examining market dynamics, emerging trends, key players, and the strategies that separate thriving sellers from those left behind.

Market Overview: The $6.3 Trillion Digital Seller Ecosystem

The global ecommerce market has evolved from a convenient alternative to brick-and-mortar retail into the dominant force in global commerce. In 2026, digital sales account for over 22% of total global retail sales, up from just 14% in 2019. This shift represents more than a change in consumer preference—it signals a permanent restructuring of the retail landscape that has fundamentally altered how businesses operate and how consumers discover, evaluate, and purchase products.

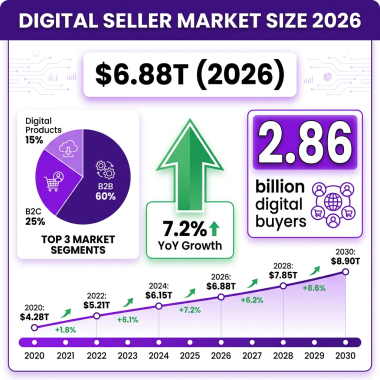

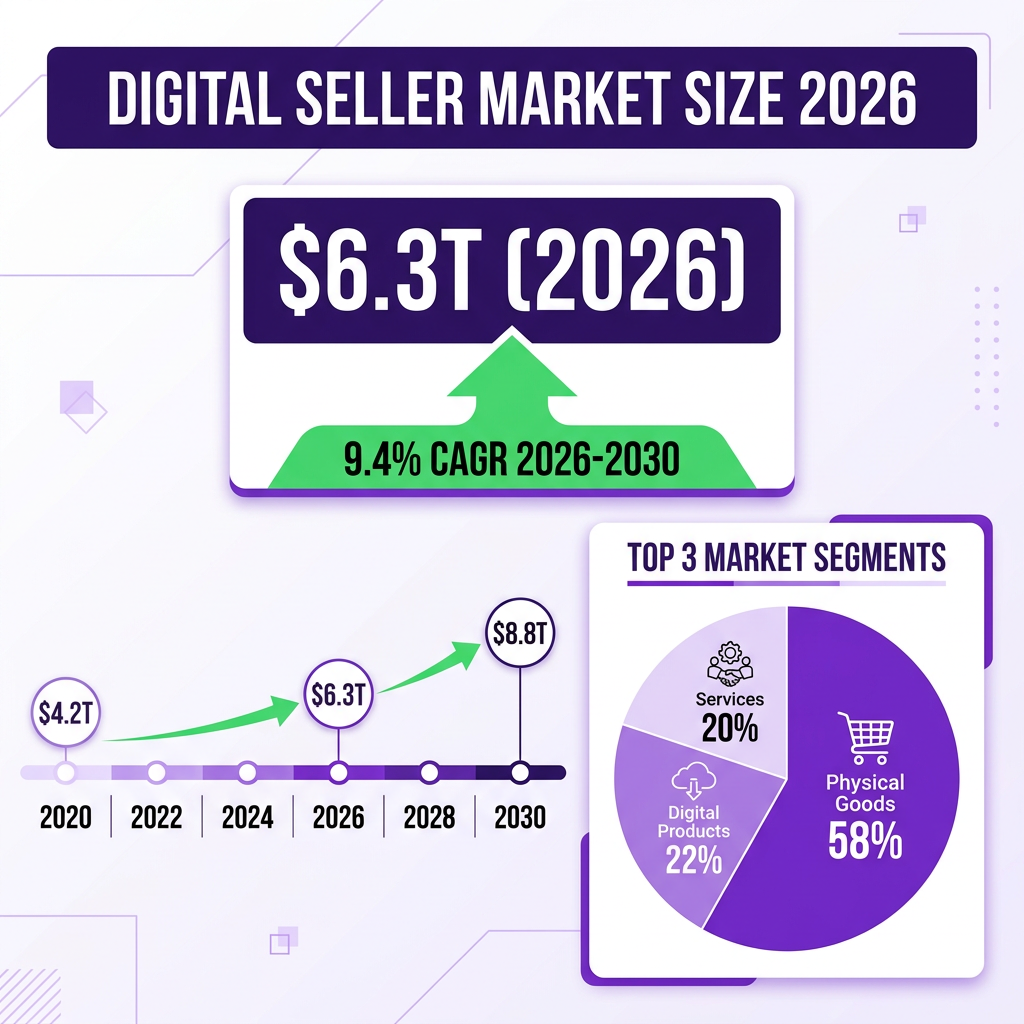

The market’s growth trajectory tells a compelling story of acceleration and maturation. From $4.2 trillion in 2020, the digital seller market expanded to $5.1 trillion in 2023, and is now positioned at $6.3 trillion for 2026. By 2030, analysts project the market will reach $8.8 trillion, maintaining a robust 9.4% CAGR. This sustained growth outpaces traditional retail by a significant margin, with digital channels capturing an increasing share of consumer spending across all categories from fashion and electronics to groceries and industrial supplies.

Breaking down the market composition reveals important insights for digital sellers planning their strategies. Physical goods still dominate, representing approximately 58% of total digital sales, or roughly $3.65 trillion annually. However, digital products—software, courses, templates, digital art, ebooks, virtual goods, and online services—have emerged as the fastest-growing segment, capturing 22% of the market at $1.39 trillion. Services sold through digital platforms, including consulting, freelancing, subscription-based offerings, and professional services, account for the remaining 20% at $1.26 trillion.

Regional distribution shows Asia-Pacific leading with 42% of global digital sales, driven by China’s massive ecommerce ecosystem and rapidly growing markets in Southeast Asia including Indonesia, Vietnam, and the Philippines. North America holds 28% of the market, with the United States remaining the single largest national market at $1.4 trillion in annual digital sales. Europe accounts for 21%, with significant variations between Western European maturity and Eastern European growth markets. Latin America, the Middle East, and Africa collectively represent 9% but show the highest growth rates, with some markets expanding at over 20% annually as digital infrastructure improves and payment systems mature.

The COVID-19 pandemic accelerated digital adoption by an estimated 5 years, but what’s remarkable is how permanent these changes have proven to be. Rather than reverting to pre-pandemic shopping patterns, consumers have doubled down on digital channels, integrating online shopping into their daily routines. The hybrid shopper—someone who researches online before buying in-store, or browses in-store before purchasing online—now represents 73% of all consumers. This behavior has forced traditional retailers to adopt digital-first strategies while creating opportunities for pure-play digital sellers to capture market share from established brick-and-mortar brands.

Mobile commerce deserves special attention as it now drives 73% of all digital sales traffic globally. The smartphone has become the primary shopping device worldwide, with mobile-optimized experiences no longer optional but essential for any serious digital seller. In emerging markets, mobile often represents the only digital access point for consumers, making mobile-first design critical for sellers targeting these high-growth regions. The average mobile transaction value has increased 34% since 2023, indicating growing consumer confidence in mobile purchasing for higher-value items and the improving security and user experience of mobile payment systems.

Key Statistics and Data: Understanding the Digital Seller Landscape

Data-driven decision making separates successful digital sellers from those that struggle to gain traction. Here are the comprehensive statistics that define the 2026 digital seller market across all key dimensions:

Market Size and Growth Metrics: Global ecommerce sales reached $6.3 trillion in 2026, growing from $5.7 trillion in 2025. The year-over-year growth rate of 10.5% demonstrates continued momentum despite economic headwinds and inflationary pressures affecting consumer spending. Cross-border ecommerce now accounts for 22% of all digital transactions, up from 18% in 2023, as sellers increasingly look beyond domestic markets for growth opportunities and consumers become more comfortable purchasing from international merchants.

Consumer Behavior and Shopping Patterns: The average online shopper makes 2.8 purchases per month across various platforms, with an average order value of $84. Cart abandonment rates have improved slightly to 69.8%, down from 71% in 2024, as checkout optimization becomes standard practice across major platforms. Mobile conversion rates have increased to 2.8%, narrowing the gap with desktop conversion at 3.2%. The average customer journey now involves 4.2 touchpoints before purchase, highlighting the importance of omnichannel presence and consistent messaging across platforms.

Platform and Technology Adoption Statistics: Shopify powers over 4.8 million online stores globally, processing $235 billion in gross merchandise value annually. WooCommerce, the WordPress plugin, runs on 6.6 million websites, offering maximum customization for technically capable sellers. Amazon’s third-party seller program includes over 9.7 million sellers worldwide, with 1.9 million actively selling at any given time. Social commerce platforms have seen explosive growth, with TikTok Shop processing over $20 billion in GMV in 2025. Live commerce, popularized in Asia, is gaining traction in Western markets with 28% year-over-year growth as consumers embrace interactive shopping experiences.

Digital Products Segment Breakdown: The digital products market has grown to $1.39 trillion, representing 22% of total digital sales. Online courses and educational content generate $350 billion annually, with the creator economy contributing significantly to this figure through platforms like Teachable, Thinkific, and Kajabi. Software and SaaS products sold online account for $480 billion, ranging from productivity tools to enterprise applications. Digital templates, creative assets, and design resources represent a $95 billion market serving designers, marketers, and content creators. NFTs and digital collectibles, after the 2022 hype cycle, have stabilized into a $12 billion market focused on utility and genuine value rather than speculation.

Payment and Financial Data: Digital wallets now account for 49% of all online payments, surpassing credit cards at 21% and demonstrating the shift toward mobile-first payment methods. Buy Now, Pay Later (BNPL) services have grown to a $680 billion transaction volume globally, with 39% of Gen Z and Millennial consumers using BNPL options regularly for purchases ranging from fashion to electronics. Cryptocurrency payments, while still niche at 2% of transactions, have seen 45% growth in merchant adoption as payment processors make integration easier. The average payment processing fee for digital sellers ranges from 2.4% to 3.5% depending on platform, volume, and risk profile.

Marketing and Customer Acquisition Costs: Average customer acquisition cost (CAC) has increased 15% year-over-year to $48 for ecommerce businesses, reflecting increased competition for digital advertising inventory. Facebook and Instagram advertising costs have risen 22%, while TikTok advertising remains 35% cheaper on a CPM basis, driving platform diversification among marketers. Email marketing continues to deliver the highest ROI at $42 for every $1 spent, making it a critical channel for retention and repeat purchases. Organic search drives 33% of all ecommerce traffic, making SEO critical for sustainable growth and reducing dependency on paid acquisition.

Operational and Financial Benchmarks: The average digital seller operates with a 25-35% gross margin, though this varies significantly by category with digital products often achieving 70-90% margins. Inventory turnover for dropshipping businesses averages 12 times per year, while traditional inventory models achieve 6-8 turns depending on category. Customer lifetime value (LTV) averages $168 for first-time buyers who return, with repeat customers representing 41% of revenue for established sellers. The average time to first sale for new digital sellers has decreased to 21 days with modern platform tools and templates.

Logistics and Fulfillment Statistics: Same-day delivery is now available from 67% of major retailers, up from 51% in 2024, setting new consumer expectations for speed. Free shipping expectations have increased, with 75% of consumers expecting free shipping on orders over $50. Return rates for online purchases average 20-30% for fashion categories but drop to 8-12% for electronics and home goods. Fulfillment by Amazon (FBA) handles over 50% of all third-party seller shipments, while Shopify Fulfillment Network has grown to support 15% of Shopify merchants with competitive alternatives.

Sustainability and Environmental Metrics: 68% of consumers consider sustainability when making online purchases, with 52% willing to pay a premium of 10-15% for eco-friendly products and sustainable packaging. Carbon-neutral shipping options are now offered by 43% of major digital sellers as logistics providers expand these services. Packaging waste reduction has become a competitive differentiator, with 38% of consumers citing excessive packaging as a reason for cart abandonment. Sustainable product categories are growing 1.7 times faster than conventional alternatives, indicating a lasting shift in consumer preferences.

Major Trends Shaping Digital Selling in 2026

The digital seller landscape is being fundamentally reshaped by seven major trends that are redefining how products are discovered, evaluated, purchased, and delivered. Understanding these trends is essential for any seller looking to maintain competitive advantage in an increasingly crowded marketplace.

1. AI-Powered Personalization at Scale

Artificial intelligence has moved from novelty to absolute necessity in digital selling. Advanced recommendation engines now drive 35% of Amazon’s revenue and similar percentages for leading retailers across all categories. But AI’s impact extends far beyond product recommendations into every aspect of the selling process. Dynamic pricing algorithms adjust prices in real-time based on demand, competition, inventory levels, and customer segments. Visual search allows customers to find products by uploading images, transforming how discovery happens. Chatbots and virtual assistants handle 68% of customer service inquiries, freeing human agents for complex issues while providing instant responses to common questions.

For digital sellers, AI-powered personalization has demonstrated a 35% lift in conversion rates when properly implemented across the customer journey. Tools that were once enterprise-only—predictive analytics, advanced customer segmentation, automated email personalization, and inventory forecasting—are now accessible to small sellers through platforms like Shopify’s AI suite, third-party apps, and integrated services. The key is using AI to enhance the customer experience without making it feel intrusive or creepy, maintaining transparency about data usage while delivering genuine value through personalization.

2. The Social Commerce Explosion

Social commerce has evolved from simple influencer marketing to full-fledged shopping experiences embedded within social platforms. TikTok Shop, Instagram Shopping, Facebook Marketplace, and Pinterest Shopping have created new sales channels that blur the line between content consumption and purchasing. In 2026, social commerce is projected to reach $1.2 trillion globally, representing 19% of total digital sales and growing faster than traditional ecommerce.

The mechanics of social commerce are fundamentally different from traditional search-based shopping. Discovery happens through algorithmic feeds rather than search intent, requiring sellers to create content that resonates with platform algorithms. Purchase decisions are influenced by social proof, viral trends, authentic creator recommendations, and FOMO rather than detailed product comparisons. The path from discovery to purchase has been compressed to seconds, with in-app checkout removing friction that previously caused abandonment. For digital sellers, this means building presence where customers spend their time—not just optimizing for Google search but creating engaging content for TikTok, Instagram, and emerging platforms.

Live commerce, combining live streaming with instant purchasing, has gained significant traction beyond its Asian origins. Western markets are now embracing the format, with conversion rates for live commerce events averaging 10-15%, significantly higher than traditional ecommerce. Digital sellers who can authentically engage audiences through live content, demonstrations, and limited-time offers are capturing outsized returns and building loyal communities.

3. Mobile-First and App-First Shopping

With 73% of ecommerce traffic coming from mobile devices, mobile-first design is no longer optional—it’s the default. But the trend is evolving beyond responsive websites to app-first experiences that leverage native device capabilities. Progressive Web Apps (PWAs) offer native app functionality without app store friction, faster load times, and offline capabilities. Super apps—platforms that combine shopping, payments, social, and services—are gaining ground, particularly in Asian markets where WeChat and similar platforms dominate.

Mobile optimization now means more than screen adaptation. It requires thumb-friendly navigation, one-tap checkout through mobile wallets, biometric authentication, and seamless mobile payment integration. Voice commerce through mobile assistants is growing 35% annually, with 27% of smartphone users having made a voice purchase. For digital sellers, mobile performance directly correlates with revenue—every 100ms of load time improvement increases conversion by 1%, making technical optimization a business-critical priority.

4. Sustainability as a Competitive Differentiator

Environmental consciousness has become a purchasing factor for the majority of consumers across all demographics. Digital sellers are responding with carbon-neutral shipping options, sustainable packaging materials, transparent supply chains, and product lifecycle programs that address end-of-life disposal. 68% of consumers consider sustainability in their purchase decisions, and 52% are willing to pay a 10-15% premium for environmentally responsible products from brands that demonstrate authentic commitment.

This trend extends beyond physical products to digital goods as well. Digital sellers are highlighting the environmental benefits of digital delivery over physical shipping, reducing carbon footprints through elimination of logistics. Carbon calculators at checkout show the impact of shipping choices, empowering consumers to make informed decisions. Circular economy models—resale, refurbishment, recycling—are being integrated into digital seller strategies, with platforms like ThredUp and Poshmark demonstrating the viability of second-hand commerce at scale. Brands that authentically commit to sustainability are building stronger customer loyalty, commanding price premiums, and attracting talent who share these values.

5. Buy Now, Pay Later (BNPL) Mainstream Adoption

BNPL has transitioned from alternative financing to standard payment option expected by consumers at checkout. Services like Klarna, Afterpay, Affirm, and PayPal Pay in 4 are now integrated into most major ecommerce platforms and increasingly available to smaller sellers through platform partnerships. The $680 billion BNPL market in 2026 represents 11% of digital transaction value and continues growing at 25% annually. For digital sellers, offering BNPL increases average order value by 45% and conversion rates by 20-30%, particularly for higher-priced items.

The demographic appeal of BNPL extends beyond cash-constrained consumers to include affluent shoppers who use these services to manage cash flow, try products before fully committing, and avoid credit card interest. The trend is driving changes in how sellers price and position products—subscription models, trial periods, and flexible payment terms are becoming standard expectations rather than premium offerings. However, regulatory scrutiny is increasing globally, with new consumer protection requirements emerging in major markets to ensure transparency and prevent overextension.

6. Cross-Border Commerce Simplification

International selling has become accessible to businesses of all sizes through platform improvements and service provider innovation. Ecommerce platforms now handle currency conversion, tax compliance, localized payment methods, and shipping logistics automatically. Cross-border sales grew 28% in 2025, with 22% of all digital transactions now crossing borders. For digital product sellers, the opportunity is even greater—digital delivery removes shipping complexities entirely, making global expansion nearly frictionless.

Key enablers include automated VAT and sales tax calculation through services like Avalara and TaxJar, multi-currency pricing with localized payment methods through Stripe and Adyen, and AI-powered translation for product listings that maintains brand voice across languages. Markets like Southeast Asia, Latin America, and Eastern Europe are seeing explosive growth in cross-border purchasing as digital payment infrastructure matures. Digital sellers who localize experiences—language, currency, payment methods, cultural preferences, and customer support—capture disproportionate market share in these high-growth regions.

7. Omnichannel Integration and Unified Commerce

The distinction between online and offline retail has effectively dissolved. Customers expect seamless experiences across all channels—buy online, pick up in-store; return online purchases to physical locations; consistent pricing and inventory visibility everywhere; unified customer profiles that remember preferences regardless of touchpoint. Unified commerce platforms that integrate all channels into single systems of record are becoming the standard for serious retailers.

For pure-play digital sellers, this trend manifests as marketplace expansion—selling through Amazon, eBay, Etsy, Walmart, and social platforms while maintaining direct-to-consumer channels. Inventory synchronization, consistent branding, centralized customer data, and unified fulfillment become critical capabilities. The goal is meeting customers wherever they prefer to shop while maintaining profitability across channels and building direct relationships that reduce platform dependency over time.

Key Players and Competitive Landscape

The digital seller ecosystem comprises multiple layers of platforms, service providers, and marketplaces that enable commerce at every scale. Understanding the competitive landscape helps sellers choose the right partners and identify opportunities for differentiation in crowded markets.

Ecommerce Platforms: Shopify remains the dominant independent platform, powering over 4.8 million online stores with $235 billion in annual GMV. Their ecosystem of apps, themes, and partners creates significant stickiness and enables customization for virtually any use case. WooCommerce, the WordPress plugin, runs on 6.6 million websites, offering maximum customization for technically capable sellers who want complete control. BigCommerce has positioned itself as the enterprise alternative to Shopify, while Squarespace and Wix compete for the small business segment with integrated website and commerce tools that prioritize ease of use.

Adobe Commerce (formerly Magento) and Salesforce Commerce Cloud serve large enterprises with complex requirements, multi-store architectures, and advanced B2B functionality. Emerging platforms like Shopware (strong in Europe) and VTEX (popular in Latin America) are gaining regional market share by addressing local needs. For digital product sellers specifically, platforms like Gumroad, LemonSqueezy, Podia, and Teachable offer specialized features for digital delivery, license management, and creator monetization that general-purpose platforms lack.

Marketplaces: Amazon dominates with $600+ billion in third-party seller GMV, though increasing fees, intense competition, and platform control make profitability challenging for many sellers. eBay remains relevant for used goods, collectibles, automotive parts, and auction formats. Etsy has carved out the handmade, vintage, and craft supplies niche with 96 million active buyers seeking unique items. Walmart Marketplace has emerged as a viable Amazon alternative, particularly for US-based sellers, with lower competition, less fee pressure, and a growing customer base seeking alternatives to Amazon.

Regional marketplaces hold significant power in their home territories: Mercado Libre in Latin America, Rakuten in Japan, Ozon in Russia, Allegro in Poland, and Flipkart in India. For digital sellers, creative marketplaces like Creative Market, Envato, Shutterstock, and Adobe Stock provide access to designer and developer audiences. App stores—Apple’s App Store and Google Play—represent massive marketplaces for software sellers, though with significant platform control, review processes, and 15-30% fees that impact margins.

Social Commerce Platforms: TikTok Shop has exploded onto the scene, processing over $20 billion in GMV in 2025 with aggressive expansion into Western markets and creator incentive programs. Instagram Shopping and Facebook Marketplace leverage Meta’s massive user base, though conversion rates lag dedicated ecommerce platforms. Pinterest has successfully pivoted to shopping, with users showing high purchase intent for home, fashion, and DIY products. YouTube Shopping integrates with Google’s ecosystem, offering unique advantages for video-centric products and tutorial-based selling.

Payment Processors and Financial Services: Stripe powers millions of online businesses with developer-friendly APIs, comprehensive features, and global coverage. PayPal remains ubiquitous for consumer trust, particularly in cross-border transactions and for older demographics. Square dominates in-person payments but has expanded online with competitive offerings. Adyen serves enterprise clients with global payment coverage and unified commerce capabilities. For digital sellers specifically, platforms like Fungies.io offer merchant-of-record services that handle tax compliance, fraud prevention, global payment methods, and regulatory requirements in integrated solutions that reduce operational burden.

Logistics and Fulfillment Providers: Amazon FBA sets the standard for fulfillment speed and reliability, though at increasing cost and with inventory restrictions. Shopify Fulfillment Network offers an alternative with competitive pricing and deeper integration with Shopify stores. ShipBob, Deliverr (now Amazon), ShipMonk, and similar 3PLs serve mid-market sellers with flexible options. For digital products, delivery is instant through download links, cloud access, or license keys—eliminating logistics complexity but requiring robust infrastructure for file hosting, access control, and digital rights management.

Challenges and Pain Points for Digital Sellers

Despite the massive opportunity, digital selling is not without significant challenges that can derail even promising businesses. Understanding these pain points helps sellers prepare, plan, and differentiate through superior execution.

1. Customer Acquisition Cost (CAC) Inflation

The cost of acquiring customers online has increased dramatically across all channels. Facebook and Instagram CPMs have risen 22% year-over-year as competition for ad inventory intensifies. Google’s cost-per-click for competitive keywords continues climbing, particularly in high-value categories. The iOS privacy changes have made attribution more difficult, forcing sellers to spend more to achieve the same measurable results. Average CAC now stands at $48 for ecommerce businesses, up from $35 in 2023, with some categories seeing even steeper increases.

This challenge is particularly acute for new sellers without established audiences, organic traffic, or brand recognition. The pay-to-play nature of digital marketing means significant upfront investment before proving product-market fit, creating cash flow challenges for bootstrapped businesses. Sellers are responding by focusing on retention and lifetime value rather than one-time transactions, building communities that generate organic growth, and investing in owned channels like email marketing where acquisition costs are lower and margins are higher.

2. Platform Dependency and Fee Pressure

Selling through Amazon, Etsy, app stores, or other marketplaces means accepting platform control over customer relationships, pricing visibility, search rankings, and policy enforcement. Amazon’s fees now average 30-40% of revenue for many sellers when including advertising costs, fulfillment fees, and referral commissions. App store fees of 15-30% significantly impact software and digital product margins. Platform policy changes can destroy businesses overnight, as seen when Amazon suspends seller accounts or Apple changes App Store guidelines.

The solution is diversification—maintaining direct-to-consumer channels alongside marketplace presence to reduce dependency. Building email lists, social media followings, and communities creates assets that platforms can’t take away. However, this requires additional investment in technology, marketing, and operations that not all sellers can afford, particularly in early stages. The tension between marketplace reach and independence remains a central strategic challenge for digital sellers.

3. Tax Compliance Complexity

Selling globally means navigating a patchwork of tax regulations that vary by country, region, and product type. VAT in Europe (with different rates across member states), GST in Australia and Canada, sales tax in the US (with thousands of jurisdictions each with their own rules), and consumption taxes in other markets create significant compliance burdens. Digital products face additional complexity with different rules for software, courses, ebooks, templates, and other categories. Penalties for non-compliance can be severe, including back taxes, fines, and blocked market access.

Automated tax solutions have emerged to address this challenge. Platforms like Avalara, TaxJar, and merchant-of-record services handle calculation, collection, and remittance automatically. However, these services add cost (typically 0.5-2% of revenue), and sellers remain responsible for proper setup, ongoing compliance monitoring, and accurate product categorization. For small sellers, the complexity often forces a choice between limiting sales to domestic markets or accepting the costs of compliance solutions.

Opportunities and Growth Strategies for Digital Sellers

Within the challenges lie significant opportunities for digital sellers who execute strategically and leverage their unique advantages in the digital economy.

1. The Digital Product Advantage

Digital products offer margins that physical goods simply cannot match. No inventory costs, no shipping logistics, no returns handling, no warehouse fees, and infinite scalability with near-zero marginal costs. The $1.39 trillion digital products market is growing faster than physical ecommerce, driven by the creator economy expansion, remote work tools demand, software-as-a-service adoption, and consumer comfort with digital ownership.

Successful digital sellers focus on solving specific, painful problems for defined audiences. Online courses that teach in-demand skills, templates that save professionals hours of work, software that automates tedious tasks, digital art that enables creative expression—all command premium pricing when value is clear and immediately demonstrable. The key is packaging expertise into scalable products, building systems for continuous delivery and updates, and creating communities around products that drive retention and word-of-mouth growth.

2. Subscription and Recurring Revenue Models

Subscription models provide predictable revenue, higher lifetime value, and more valuable business multiples. Software, content, communities, and even physical products are being repositioned as subscriptions. The subscription ecommerce market has grown to $120 billion, with consumers increasingly comfortable with recurring payments for products and services that deliver ongoing value.

For digital sellers, subscriptions align incentives—ongoing value delivery rather than one-time transactions creates better customer relationships. Successful subscription businesses focus on retention through continuous product improvement, community building that increases switching costs, and excellent customer support that prevents churn. Churn management becomes as important as acquisition, with successful sellers achieving negative churn through expansion revenue from existing customers.

3. Global Expansion Through Digital Channels

Digital selling removes geographical constraints that previously limited business growth. A solo creator in Poland can sell to customers worldwide without local presence, physical infrastructure, or local employees. Emerging markets represent massive growth opportunities—Southeast Asia’s digital economy is growing 20% annually, Latin America’s ecommerce penetration is accelerating as payment infrastructure improves, and African markets are leapfrogging traditional retail straight to mobile commerce.

Success in global markets requires localization beyond simple translation. Understanding local payment preferences (cash on delivery remains popular in some markets, mobile wallets dominate others), cultural nuances that affect marketing messaging, pricing expectations that vary by market, and regulatory requirements for data privacy and consumer protection is essential. Partners that handle tax compliance, local payment methods, currency conversion, and regulatory requirements reduce barriers to entry significantly, enabling sellers to test markets before major investment.

Case Studies and Success Stories

Real-world examples demonstrate what’s possible in the digital seller market when strategy, execution, and timing align.

Case Study 1: Notion Template Creator

A solo creator developed productivity templates for Notion, initially selling through Gumroad for $15-25 per template. By building an audience on Twitter and YouTube through free educational content, they grew to $50,000 monthly revenue within 18 months. Key strategies included: offering free templates to build email lists, creating template bundles for higher average order value, implementing affiliate partnerships with Notion influencers, and continuously expanding the template library based on customer feedback. The business now includes a template marketplace with 40+ creators, generating $1.2 million annually with minimal overhead and high margins.

Case Study 2: Shopify App Developer

A development team of three identified a gap in email marketing automation for Shopify stores—existing solutions were either too simple or too complex for mid-market merchants. Building a focused app that solved one problem exceptionally well, they launched on the Shopify App Store with a freemium model that allowed stores to try before buying. Within two years, they reached 15,000 active merchants and $85,000 monthly recurring revenue. The app was eventually acquired for $4.2 million by a larger software company, demonstrating the value of focused digital products in large ecosystems and the viability of the Shopify partner ecosystem for building valuable businesses.

Case Study 3: Digital Course Creator

An industry expert with 15 years of experience packaged their knowledge into a comprehensive online course teaching specialized professional skills, initially selling through their own website using Teachable. By combining strategic paid advertising with organic content marketing, podcast appearances, and strategic partnerships with complementary businesses, they generated $2.3 million in first-year revenue. The course price point of $997 positioned it as premium, with a 4% refund rate indicating strong product-market fit and quality delivery. Ongoing updates, community access, and live Q&A sessions drive 40% of revenue from existing customers through upsells and referrals.

Future Outlook and Predictions (2026-2030)

The digital seller market will continue evolving rapidly through 2030, shaped by technological innovation, regulatory changes, and shifting consumer expectations. Here are the key predictions that will define the next phase of digital commerce:

Market Growth Projections: The global digital seller market will reach $8.8 trillion by 2030, maintaining the 9.4% CAGR that has characterized the past decade. Digital products will grow to represent 28% of the market as the creator economy expands, software continues eating the world, and consumers become increasingly comfortable with digital ownership. Cross-border commerce will account for 30% of transactions as logistics networks improve, payment infrastructure globalizes, and trust in international purchasing increases.

Technology Evolution: Artificial intelligence will become fully integrated into every aspect of digital selling—from product development and pricing optimization to marketing personalization and customer service automation. Augmented reality will enable virtual try-before-you-buy experiences for physical products, while virtual goods in metaverse environments will create entirely new product categories. Voice commerce will reach 15% of transactions as smart speakers and voice assistants proliferate in homes and vehicles.

Regulatory Changes: Data privacy regulations will continue expanding globally, requiring sellers to be more transparent and careful with customer data collection and usage. Tax compliance will be increasingly automated, with real-time reporting becoming standard across jurisdictions. Platform regulation may limit the power of major marketplaces, potentially opening opportunities for independent sellers and reducing fee pressure. Sustainability reporting requirements will become mandatory for larger sellers.

Consumer Behavior Shifts: Sustainability will move from differentiator to baseline expectation, with consumers expecting transparency about environmental impact. Instant gratification will drive same-day delivery to become standard in major markets, requiring sellers to optimize logistics or partner with fulfillment networks. Subscription fatigue may emerge in some categories, requiring sellers to demonstrate ongoing value more clearly. The line between content and commerce will blur further as social platforms become primary shopping destinations.

Digital Seller Best Practices for 2026

Beyond understanding market trends and competitive dynamics, successful digital sellers in 2026 follow specific best practices that maximize their chances of success. These practices span technology, marketing, operations, and customer experience.

Technology Stack Optimization: Modern digital sellers need integrated technology stacks that connect seamlessly. This means choosing an ecommerce platform that integrates with your email marketing tool, CRM, analytics, accounting software, and fulfillment solutions. API-first platforms provide the flexibility to build custom workflows as your business grows. Investing in headless commerce architectures allows sellers to deliver content-rich experiences while maintaining robust backend systems.

Data-Driven Decision Making: The most successful digital sellers measure everything. They track customer acquisition costs by channel, monitor lifetime value by cohort, analyze conversion rates at each funnel stage, and use A/B testing to optimize continuously. Dashboards that provide real-time visibility into key metrics enable rapid response to market changes and early identification of opportunities or problems.

Customer Experience Excellence: In a world of infinite choice, customer experience is the ultimate differentiator. This means fast-loading pages, intuitive navigation, transparent pricing, flexible payment options, proactive communication, and hassle-free returns. Sellers who invest in customer experience see higher conversion rates, better reviews, more referrals, and lower acquisition costs through improved word-of-mouth.

Content Marketing Investment: Organic traffic through content marketing provides the highest ROI of any acquisition channel. Successful digital sellers invest in SEO-optimized blog content, video tutorials, social media presence, and email newsletters that provide value before asking for sales. This builds authority, trust, and audience that compounds over time, reducing dependency on paid advertising.

Community Building: The most valuable digital sellers don’t just have customers—they have communities. Whether through Facebook Groups, Discord servers, membership programs, or events, building community around your brand creates switching costs, generates feedback, drives referrals, and provides a moat against competitors. Community members become advocates who market your products for free.

Agile Operations: The digital seller landscape changes rapidly. Successful sellers maintain agile operations that can pivot quickly in response to platform changes, market shifts, or competitive threats. This means maintaining diversified revenue streams, testing new channels continuously, and avoiding over-dependence on any single platform or strategy.

The Rise of the Creator Economy and Digital Products

A significant driver of digital seller market growth is the explosive expansion of the creator economy. In 2026, the creator economy is valued at $250 billion, with over 50 million people worldwide identifying as creators who monetize their skills, knowledge, or audience through digital products and services.

This trend represents a fundamental shift in how value is created and captured. Individuals with specialized knowledge can now package that expertise into scalable digital products—courses, templates, software, ebooks, and memberships—that generate passive income. The barriers that previously prevented individuals from becoming sellers—technical complexity, distribution challenges, payment processing—have been eliminated by modern platforms.

For the broader digital seller market, the creator economy represents both competition and opportunity. Competition because millions of new sellers have entered the market. Opportunity because these creators need tools, platforms, and services to run their businesses. The infrastructure supporting creators—payment processing, email marketing, course platforms, community tools—has become a massive market in itself.

The most successful creators think like businesses from day one. They invest in branding, build email lists, diversify revenue streams, and systematize their operations. They understand that audience is the ultimate asset and focus on building genuine relationships rather than extracting maximum short-term revenue. This approach creates sustainable businesses that can weather platform changes and algorithm updates.

Key Takeaways

- The digital seller market reached $6.3 trillion in 2026, growing at 9.4% CAGR with no signs of slowing as digital commerce becomes the default

- Digital products represent the fastest-growing segment at 22% of the market, offering superior margins of 70-90% and infinite scalability

- AI-powered personalization, social commerce, and mobile-first experiences are the defining trends reshaping digital selling in 2026

- Cross-border selling has become accessible to businesses of all sizes, opening global opportunities in high-growth emerging markets

- Customer acquisition costs are rising, making retention, community building, and owned channels critical for sustainable growth

- Tax compliance complexity remains a major challenge, driving adoption of automated solutions and merchant-of-record services

- Subscription models and recurring revenue provide predictability, higher lifetime value, and more valuable business multiples

- Sustainability has become a competitive differentiator with 68% of consumers considering environmental impact in purchase decisions

- The market will reach $8.8 trillion by 2030, with digital products and cross-border commerce driving the next wave of growth

- Success requires balancing platform diversification with focused execution on solving specific customer problems

Sources and Citations

- eMarketer Global Ecommerce Forecast 2026 – https://www.emarketer.com/content/global-ecommerce-forecast

- Statista Digital Commerce Report 2026 – https://www.statista.com/topics/871/online-shopping/

- Shopify Annual Commerce Report 2025 – https://news.shopify.com/annual-merchant-solutions-report

- Amazon Seller Report 2026 – https://sell.amazon.com/learn/seller-reports

- McKinsey & Company: The Future of Digital Commerce – https://www.mckinsey.com/industries/retail/our-insights

- Digital Commerce 360: Top 1000 Online Retailers – https://digitalcommerce360.com/article/top-1000-online-retailers/

- Grand View Research: E-commerce Market Size Report – https://www.grandviewresearch.com/industry-analysis/e-commerce-market

- Payment Cards Network: Global Payments Report 2026 – https://paymentsjournal.com/global-payments-report/

- HubSpot: State of Marketing 2026 – https://www.hubspot.com/state-of-marketing

- Klarna: Buy Now Pay Later Consumer Insights – https://www.klarna.com/uk/press/consumer-insights/