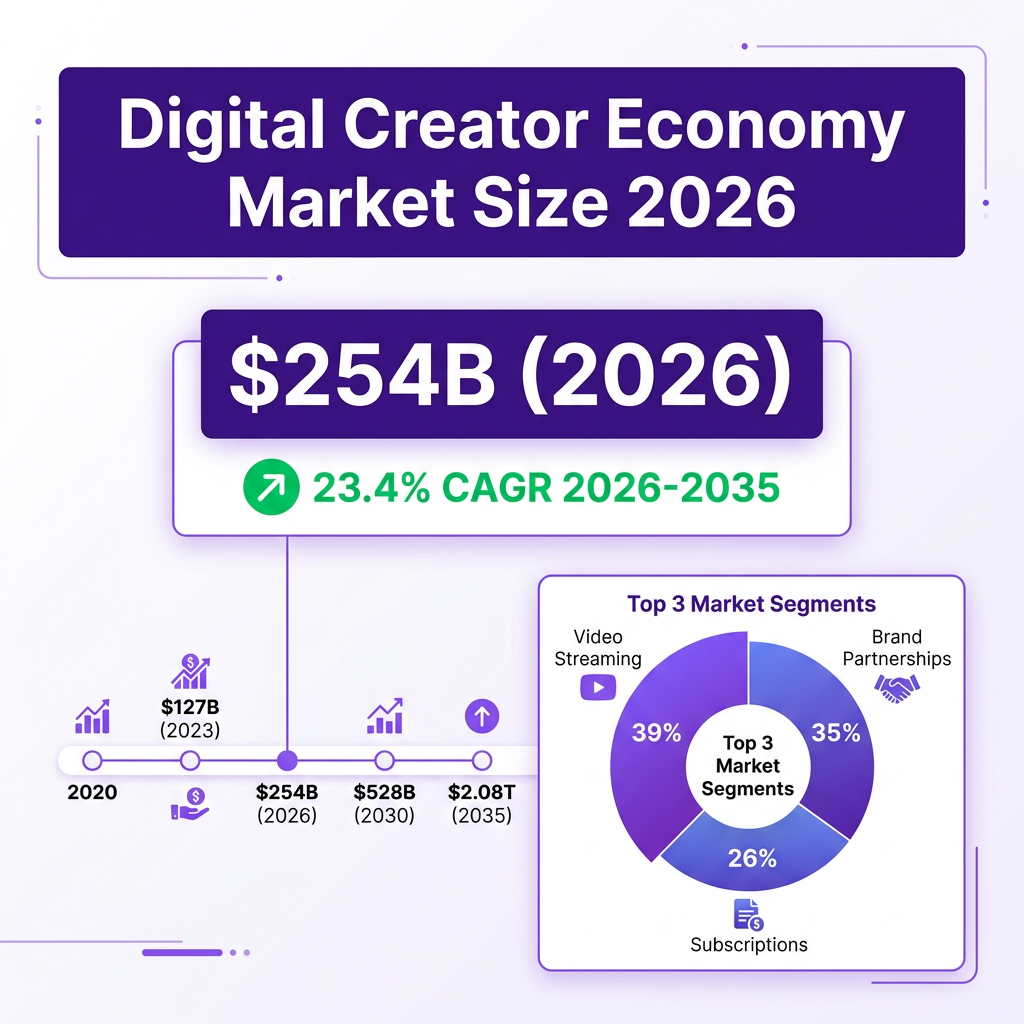

The digital creator economy has evolved from a side-hustle curiosity into a $254 billion global industry that employs over 207 million people worldwide. What started as a handful of YouTube personalities and Instagram influencers has transformed into a sophisticated ecosystem where creators operate as full-stack media companies, complete with diversified revenue streams, professional management teams, and direct-to-consumer business models.

In 2026, the creator economy is entering what industry analysts call “the era of consolidation”—a maturation phase where investment decisions are guided not by experimentation but by proven impact and scalable ROI. The numbers tell a compelling story: the market is projected to reach $528 billion by 2030 and could exceed $2 trillion by 2035, growing at a compound annual growth rate of 22.4% to 23.4%.

Market Overview: The $254 Billion Ecosystem

The creator economy market size has experienced explosive growth over the past decade. According to Research Nester, the market was valued at $178.4 billion in 2025 and is set to exceed $1.35 trillion by 2035. Precedence Research offers even more bullish projections, estimating the market at $254.4 billion in 2025, growing to $313.95 billion in 2026, and potentially reaching $2.08 trillion by 2035.

Goldman Sachs reported that the creator economy could approach half a trillion dollars by 2027, representing a compound annual growth rate of 27.5%. This trajectory places the creator economy among the fastest-growing sectors in the global economy, outpacing traditional media and entertainment industries.

The growth is fueled by several converging factors. First, internet and smartphone penetration has reached unprecedented levels globally, creating an addressable audience of billions. Second, platforms have matured their monetization features, enabling creators to earn through multiple channels simultaneously. Third, the pandemic permanently shifted consumer behavior toward digital content consumption, a trend that has only accelerated.

Looking at the historical trajectory, the creator economy grew from $127.65 billion in 2023 to approximately $205-254 billion in 2026. This represents a doubling in just three years—a growth rate that few industries can match. The market is expected to maintain this momentum, with projections suggesting $480-600 billion by 2028-2030.

The regional distribution of the creator economy reveals interesting patterns. North America and Europe currently dominate in terms of revenue per creator, but Asia-Pacific is experiencing the fastest growth in absolute numbers. India, Southeast Asia, and Latin America are emerging as hotbeds of creator activity, driven by young, mobile-first populations and improving digital infrastructure.

By platform type, video streaming holds the largest share at approximately 39% of total creator economy revenue. This includes YouTube, TikTok, Instagram Reels, and emerging platforms like Twitch. Social commerce platforms, blogging platforms, and podcasting platforms make up the remainder, with each segment showing strong growth trajectories.

The Evolution of Creator Business Models

The business models employed by successful creators have evolved dramatically over the past five years. What began as simple advertising revenue sharing has transformed into sophisticated multi-channel enterprises that rival traditional media companies in complexity and revenue potential.

In the early days of the creator economy, business models were straightforward. YouTube creators earned through AdSense revenue sharing. Bloggers relied on display advertising and occasional sponsored posts. Instagram influencers charged flat fees for sponsored content. These models were simple but fragile—dependent on single platforms and subject to algorithmic whims.

Today’s successful creator businesses operate on what industry analysts call the “hub and spoke” model. The hub consists of owned assets—email lists, private communities, and proprietary products. The spokes are discovery platforms—YouTube, TikTok, Instagram, LinkedIn—that drive traffic to the hub. This model provides both reach and resilience.

Subscription-based models have emerged as particularly powerful. Patreon pioneered the space, but platforms like Substack, beehiiv, and Circle have expanded the possibilities. Creators can now offer tiered memberships with varying levels of access, community features, and exclusive content. The predictability of recurring revenue transforms creator businesses from feast-or-famine operations into stable enterprises.

Digital products represent another evolution in creator monetization. Rather than trading time for money through sponsored posts, creators develop products that can be sold infinitely without additional effort. Courses, templates, ebooks, and software tools enable creators to scale their impact and income simultaneously. The most successful creators now generate the majority of their revenue from products rather than services.

The emergence of creator-led commerce has added physical products to the mix. Creators are launching merchandise lines, beauty brands, and consumer products that leverage their audience relationships. This vertical integration—owning the product, the marketing, and the distribution—offers margins that traditional brand partnerships cannot match.

Licensing and IP deals represent the highest tier of creator business models. Established creators license their content, likeness, and intellectual property for use by media companies, brands, and platforms. Netflix’s deals with creators like Ms. Rachel and Mark Rober exemplify this trend. As the creator economy matures, IP ownership will become increasingly important for long-term value creation.

Regional Variations in the Creator Economy

While the creator economy is global in scope, significant regional variations exist in terms of market maturity, platform preferences, monetization approaches, and regulatory environments. Understanding these differences is essential for creators and brands operating internationally.

North America remains the largest creator economy market by revenue, driven by high advertising rates, mature monetization infrastructure, and a culture that celebrates entrepreneurship. The United States alone accounts for a significant portion of global influencer marketing spend, with brands allocating $37.1 billion annually to creator partnerships. American creators benefit from established legal frameworks, robust payment systems, and a large domestic audience.

Europe presents a more fragmented landscape. The European Union’s regulatory environment, including GDPR privacy regulations and the Digital Services Act, creates compliance challenges for creators and platforms. However, European audiences show strong engagement with creator content, and cities like London, Berlin, and Paris have emerged as creator economy hubs. The EU AI Act will further shape how AI-generated content is created and disclosed.

Asia-Pacific represents the fastest-growing region in terms of creator numbers. India alone has millions of active creators across platforms like YouTube, Instagram, and regional apps like ShareChat and Moj. Southeast Asian markets—Indonesia, Thailand, Vietnam—are experiencing explosive growth in mobile-first content consumption. The region’s young demographics and improving digital infrastructure suggest continued expansion.

China operates as a distinct ecosystem due to platform restrictions and regulatory differences. While Western platforms are largely inaccessible, domestic alternatives like Douyin (TikTok’s Chinese version), Xiaohongshu (Little Red Book), and Bilibili have created thriving creator economies. Chinese creators often lead in live commerce and social shopping innovations that later spread to Western markets.

Latin America and the Middle East represent emerging markets with significant potential. Brazil, Mexico, and Argentina have vibrant creator communities, while Gulf states are investing heavily in digital content as part of economic diversification efforts. These markets often leapfrog traditional media development, moving directly to creator-driven content consumption.

The Role of Platforms in Shaping the Creator Economy

Platforms are not neutral infrastructure—they actively shape the creator economy through algorithmic decisions, policy choices, and monetization feature development. Understanding platform dynamics is essential for creator success.

YouTube’s Partner Program remains the gold standard for creator monetization. The platform shares 55% of ad revenue with creators, providing transparent metrics and predictable income. YouTube’s algorithm favors watch time and session duration, incentivizing longer, more engaging content. The platform’s investment in Shorts, memberships, and shopping features demonstrates its commitment to creator monetization.

TikTok has revolutionized content discovery through its “For You Page” algorithm, which can catapult unknown creators to viral fame overnight. However, the platform’s monetization features lag behind its discovery capabilities. The Creativity Program Beta offers revenue sharing, but creators often report lower earnings per view compared to YouTube. TikTok Shop represents the platform’s bet on social commerce as a monetization pathway.

Instagram has evolved from a photo-sharing app to a comprehensive creator platform. Reels competes directly with TikTok for short-form video attention, while Shopping features enable direct commerce. Meta’s Creator Fast Track program, paying $1,000-$3,000 monthly to qualifying creators, signals serious investment in retention. However, Instagram’s algorithm changes have historically disrupted creator businesses, highlighting platform dependency risks.

LinkedIn’s emergence as a creator platform represents a significant development. The professional network’s focus on knowledge sharing and career development has created opportunities for B2B creators who would struggle on entertainment-focused platforms. LinkedIn’s revenue-sharing programs and CapCut integration demonstrate its commitment to the creator economy.

Emerging platforms like Twitch, Discord, and Telegram offer specialized environments for community building and monetization. Twitch dominates live streaming, particularly in gaming. Discord enables private community spaces with subscription capabilities. Telegram’s channel features support large-scale broadcast messaging. These platforms serve specific creator needs that mainstream social media cannot address.

Regulatory Landscape and Compliance

As the creator economy matures, regulatory scrutiny has increased. Creators and brands must navigate complex legal requirements around advertising disclosure, data privacy, intellectual property, and emerging AI regulations.

The Federal Trade Commission (FTC) in the United States requires clear disclosure of material connections between creators and brands. Sponsored content must be labeled with hashtags like #ad or #sponsored. Failure to comply can result in fines and reputational damage. The FTC has increased enforcement actions against both creators and brands for inadequate disclosure.

The European Union’s General Data Protection Regulation (GDPR) affects how creators collect and process audience data. Email list building, analytics tracking, and personalized advertising all fall under GDPR requirements. Creators targeting European audiences must implement compliant data practices or risk significant penalties.

The EU AI Act introduces new requirements for AI-generated content. Creators using AI tools must disclose when content is artificially generated. Virtual influencers face specific labeling requirements. These regulations will shape how AI is integrated into creator workflows and how audiences perceive AI-generated content.

Copyright and intellectual property issues remain persistent challenges. Creators must navigate fair use doctrines when incorporating third-party content. Music licensing, in particular, creates friction for video creators. Platforms have implemented content ID systems to manage copyright claims, but these systems often generate disputes and demonetization.

Tax compliance adds complexity for creators earning income across multiple jurisdictions. International creators may owe taxes in multiple countries. The rise of digital nomad creators further complicates tax residency questions. Professional creators increasingly require accounting and legal support to manage compliance obligations.

Key Statistics and Data Points

The creator economy is defined by numbers that would have seemed impossible just a decade ago. With over 207 million active creators worldwide, this represents a significant portion of the global workforce. To put this in perspective, if the creator economy were a country, it would rank among the top 10 most populous nations on Earth.

Influencer marketing spend has become a critical metric for understanding the creator economy’s scale. In 2026, global influencer marketing spend exceeded $32 billion, with U.S. annual creator economy ad spend alone reaching $37.1 billion according to the IAB. This represents a fundamental shift in how brands allocate marketing budgets—moving from traditional advertising to creator partnerships.

Creator income statistics reveal a bifurcated market. While the average content creator earns $61,980 per year, the distribution is highly skewed. According to Influencer Marketing Hub, the average creator earns only 2-3% of their audience size as annual revenue. Breaking this down by follower tiers: creators with 1,000-10,000 followers typically earn $100-$1,000 per month, while those with larger audiences can command significantly higher rates.

A critical finding from recent research is the importance of revenue diversification. Creators with three or more revenue streams earned $75,000 more on average than those relying on a single source in 2025. This statistic underscores a fundamental shift in how successful creators approach their businesses—they are no longer dependent on a single platform or monetization method.

Platform-specific statistics paint a detailed picture of where creators focus their efforts. YouTube leads with 61.8 million creators globally, followed by Instagram and TikTok with significant but smaller creator bases. Each platform offers different monetization potential: YouTube’s revenue share model through the Partner Program remains the gold standard for sustainable creator income, while TikTok and Instagram excel at brand partnership facilitation.

Brand partnerships remain the dominant revenue source, with approximately 68.8% of creators citing brand deals as their primary income stream. However, this dependency is declining as more creators move into subscriptions, affiliate marketing, and owned products. Survey data from Circle shows that 88% of creators now prioritize paid memberships as a monetization strategy, with 53% selling courses and 51% offering coaching or services.

The rise of community-centric monetization is particularly noteworthy. According to Circle’s research, 69% of creators now prioritize member transformation as their primary driver of retention and growth. This represents a shift from vanity metrics (views, likes) to value metrics (member outcomes, retention rates).

AI adoption among creators has reached mainstream levels. A remarkable 84% of creators already use AI tools in their workflow, whether for content generation, editing, analytics, or audience engagement. This technological adoption is reshaping what it means to be a creator, blurring the lines between human and AI-generated content.

Platform demographics reveal that the 25-34 age group is now the largest audience segment across platforms, representing the prime earning and spending years. This demographic shift has significant implications for the types of content that succeed and the products creators can effectively promote.

Major Trends Shaping the Digital Creator Economy in 2026

The creator economy in 2026 is defined by seven transformative trends that are reshaping how creators build audiences, monetize content, and structure their businesses. Understanding these trends is essential for anyone looking to enter or succeed in this space.

1. AI-Powered Content Creation at Scale

Artificial intelligence has moved from experimental tool to essential infrastructure for creators. With 84% of creators already using AI tools, the technology is enabling unprecedented levels of productivity. Creators who use AI aren’t working less—they’re publishing 10x more content, reaching wider audiences, and building bigger personal brands.

The AI creator tools market has attracted significant venture capital, with $1.2 billion raised by AI content creation startups in 2025 alone. Companies like Runway, Synthesia, and emerging players are providing professional-grade AI video generation, image creation, and text generation tools that were previously accessible only to large media companies.

However, AI adoption comes with challenges. While 76% of consumers report trusting virtual influencers for product recommendations, nearly half view AI-generated content as a potential trust liability. This tension between efficiency and authenticity will define the AI era of content creation.

2. Diversified Revenue Streams as Survival Strategy

The era of relying on a single platform or monetization method is over. Successful creators in 2026 operate diversified business models that include brand partnerships, affiliate marketing, digital products, courses, coaching, memberships, and merchandise.

The data is clear: creators with three or more revenue streams earn $75,000 more annually than those with a single source. This diversification isn’t just about maximizing income—it’s about building resilience against platform algorithm changes, policy shifts, and market volatility.

Monetization method preferences have shifted significantly. While brand sponsorships remain important (cited by 18% as a primary method), paid memberships lead at 88%, followed by selling courses (53%) and offering coaching or services (51%). Affiliate revenue and digital products round out the typical creator revenue mix.

3. The Rise of Owned Audiences

Perhaps the most significant trend in 2026 is the migration from rented platforms to owned channels. Creators are increasingly building direct relationships with their audiences through email lists, private communities, and owned platforms—reducing dependency on algorithmic social media.

This trend is exemplified by the growth of platforms like Substack, beehiiv, and Circle. Substack took the spotlight in 2025 as creators sought alternatives to social media algorithms. beehiiv raised $33 million in Series B funding in April 2024, signaling strong investor confidence in newsletter-based creator businesses.

The distinction between “discovery platforms” (TikTok, Instagram, YouTube) and “revenue platforms” (communities, memberships, courses) has become a fundamental framework for creator strategy. Discovery platforms are where attention is captured; revenue platforms are where value is monetized.

4. From URL to IRL: In-Person Creator Events

The URL to IRL (In Real Life) movement represents a counter-trend to digital saturation. Creators are increasingly hosting in-person events, meetups, conferences, and experiences that transform online communities into real-world connections.

This trend is driven by audience demand for authentic, face-to-face interactions. According to the Influencer Marketing Factory’s Creators IRL Survey, people want to go from online to offline and meet their favorite creators in person. This movement is creating new revenue opportunities through ticket sales, sponsorships, and exclusive experiences.

Startups like Sweatpals, which sits at the intersection of the creator economy and IRL socializing, have attracted venture capital interest. Patron co-led Sweatpals’ seed round, recognizing the potential of combining digital influence with physical experiences.

5. Creator-Led Commerce and Social Shopping

Social commerce has blurred the lines between creators and retailers. Creators are no longer just advertisers—they’re becoming extensions of retail strategies, with direct shopping integrations, affiliate links, and even their own product lines.

Platforms have responded by building sophisticated commerce features. TikTok Shop, Instagram Shopping, and YouTube’s shopping integrations allow creators to sell products directly through their content. This trend is particularly strong in beauty, fashion, and consumer packaged goods.

The data shows that creators are building real businesses, not just chasing brand deals. Many successful creators now operate multi-layer business models that include physical products, digital goods, and services—essentially functioning as media companies with diversified revenue streams.

6. The B2B Creator Emergence

While consumer-facing creators dominate headlines, a significant trend is the rise of B2B creators—professionals who build audiences around business expertise, industry knowledge, and professional development. LinkedIn has become the breakout platform for this segment.

LinkedIn’s integration with CapCut and its revenue-sharing programs for top B2B creators signal the platform’s commitment to this space. The professional networking site is tapping into a pool of subject matter experts who can monetize their knowledge through courses, consulting, and corporate partnerships.

This trend reflects a broader shift in how businesses consume content. Decision-makers increasingly trust individual experts over traditional corporate messaging, creating opportunities for knowledgeable professionals to build influential personal brands.

7. AI Virtual Influencers and Synthetic Media

The synthetic influencer market has emerged as a distinct segment within the creator economy, valued at $15.9 billion in 2026. AI-generated virtual influencers like Lil Miquela have demonstrated that computer-generated personas can build real audiences and secure brand partnerships.

By 2030, the synthetic talent market is estimated to be worth tens of billions. Companies like Synthesia, valued at $4 billion, help brands build fleets of synthetic social media accounts that can post content, respond to comments, and engage with customers across platforms.

This trend raises important questions about authenticity, disclosure, and the future of human creativity. The EU AI Act and FTC guidelines are beginning to address AI disclosure requirements, but the regulatory landscape remains evolving.

The Evolution of Creator Business Models

The business models employed by successful creators have evolved dramatically over the past five years. What began as simple advertising revenue sharing has transformed into sophisticated multi-channel enterprises that rival traditional media companies in complexity and revenue potential.

In the early days of the creator economy, business models were straightforward. YouTube creators earned through AdSense revenue sharing. Bloggers relied on display advertising and occasional sponsored posts. Instagram influencers charged flat fees for sponsored content. These models were simple but fragile—dependent on single platforms and subject to algorithmic whims.

Today’s successful creator businesses operate on what industry analysts call the “hub and spoke” model. The hub consists of owned assets—email lists, private communities, and proprietary products. The spokes are discovery platforms—YouTube, TikTok, Instagram, LinkedIn—that drive traffic to the hub. This model provides both reach and resilience.

Subscription-based models have emerged as particularly powerful. Patreon pioneered the space, but platforms like Substack, beehiiv, and Circle have expanded the possibilities. Creators can now offer tiered memberships with varying levels of access, community features, and exclusive content. The predictability of recurring revenue transforms creator businesses from feast-or-famine operations into stable enterprises.

Digital products represent another evolution in creator monetization. Rather than trading time for money through sponsored posts, creators develop products that can be sold infinitely without additional effort. Courses, templates, ebooks, and software tools enable creators to scale their impact and income simultaneously. The most successful creators now generate the majority of their revenue from products rather than services.

The emergence of creator-led commerce has added physical products to the mix. Creators are launching merchandise lines, beauty brands, and consumer products that leverage their audience relationships. This vertical integration—owning the product, the marketing, and the distribution—offers margins that traditional brand partnerships cannot match.

Licensing and IP deals represent the highest tier of creator business models. Established creators license their content, likeness, and intellectual property for use by media companies, brands, and platforms. Netflix’s deals with creators like Ms. Rachel and Mark Rober exemplify this trend. As the creator economy matures, IP ownership will become increasingly important for long-term value creation.

Regional Variations in the Creator Economy

While the creator economy is global in scope, significant regional variations exist in terms of market maturity, platform preferences, monetization approaches, and regulatory environments. Understanding these differences is essential for creators and brands operating internationally.

North America remains the largest creator economy market by revenue, driven by high advertising rates, mature monetization infrastructure, and a culture that celebrates entrepreneurship. The United States alone accounts for a significant portion of global influencer marketing spend, with brands allocating $37.1 billion annually to creator partnerships. American creators benefit from established legal frameworks, robust payment systems, and a large domestic audience.

Europe presents a more fragmented landscape. The European Union’s regulatory environment, including GDPR privacy regulations and the Digital Services Act, creates compliance challenges for creators and platforms. However, European audiences show strong engagement with creator content, and cities like London, Berlin, and Paris have emerged as creator economy hubs. The EU AI Act will further shape how AI-generated content is created and disclosed.

Asia-Pacific represents the fastest-growing region in terms of creator numbers. India alone has millions of active creators across platforms like YouTube, Instagram, and regional apps like ShareChat and Moj. Southeast Asian markets—Indonesia, Thailand, Vietnam—are experiencing explosive growth in mobile-first content consumption. The region’s young demographics and improving digital infrastructure suggest continued expansion.

China operates as a distinct ecosystem due to platform restrictions and regulatory differences. While Western platforms are largely inaccessible, domestic alternatives like Douyin (TikTok’s Chinese version), Xiaohongshu (Little Red Book), and Bilibili have created thriving creator economies. Chinese creators often lead in live commerce and social shopping innovations that later spread to Western markets.

Latin America and the Middle East represent emerging markets with significant potential. Brazil, Mexico, and Argentina have vibrant creator communities, while Gulf states are investing heavily in digital content as part of economic diversification efforts. These markets often leapfrog traditional media development, moving directly to creator-driven content consumption.

The Role of Platforms in Shaping the Creator Economy

Platforms are not neutral infrastructure—they actively shape the creator economy through algorithmic decisions, policy choices, and monetization feature development. Understanding platform dynamics is essential for creator success.

YouTube’s Partner Program remains the gold standard for creator monetization. The platform shares 55% of ad revenue with creators, providing transparent metrics and predictable income. YouTube’s algorithm favors watch time and session duration, incentivizing longer, more engaging content. The platform’s investment in Shorts, memberships, and shopping features demonstrates its commitment to creator monetization.

TikTok has revolutionized content discovery through its “For You Page” algorithm, which can catapult unknown creators to viral fame overnight. However, the platform’s monetization features lag behind its discovery capabilities. The Creativity Program Beta offers revenue sharing, but creators often report lower earnings per view compared to YouTube. TikTok Shop represents the platform’s bet on social commerce as a monetization pathway.

Instagram has evolved from a photo-sharing app to a comprehensive creator platform. Reels competes directly with TikTok for short-form video attention, while Shopping features enable direct commerce. Meta’s Creator Fast Track program, paying $1,000-$3,000 monthly to qualifying creators, signals serious investment in retention. However, Instagram’s algorithm changes have historically disrupted creator businesses, highlighting platform dependency risks.

LinkedIn’s emergence as a creator platform represents a significant development. The professional network’s focus on knowledge sharing and career development has created opportunities for B2B creators who would struggle on entertainment-focused platforms. LinkedIn’s revenue-sharing programs and CapCut integration demonstrate its commitment to the creator economy.

Emerging platforms like Twitch, Discord, and Telegram offer specialized environments for community building and monetization. Twitch dominates live streaming, particularly in gaming. Discord enables private community spaces with subscription capabilities. Telegram’s channel features support large-scale broadcast messaging. These platforms serve specific creator needs that mainstream social media cannot address.

Regulatory Landscape and Compliance

As the creator economy matures, regulatory scrutiny has increased. Creators and brands must navigate complex legal requirements around advertising disclosure, data privacy, intellectual property, and emerging AI regulations.

The Federal Trade Commission (FTC) in the United States requires clear disclosure of material connections between creators and brands. Sponsored content must be labeled with hashtags like #ad or #sponsored. Failure to comply can result in fines and reputational damage. The FTC has increased enforcement actions against both creators and brands for inadequate disclosure.

The European Union’s General Data Protection Regulation (GDPR) affects how creators collect and process audience data. Email list building, analytics tracking, and personalized advertising all fall under GDPR requirements. Creators targeting European audiences must implement compliant data practices or risk significant penalties.

The EU AI Act introduces new requirements for AI-generated content. Creators using AI tools must disclose when content is artificially generated. Virtual influencers face specific labeling requirements. These regulations will shape how AI is integrated into creator workflows and how audiences perceive AI-generated content.

Copyright and intellectual property issues remain persistent challenges. Creators must navigate fair use doctrines when incorporating third-party content. Music licensing, in particular, creates friction for video creators. Platforms have implemented content ID systems to manage copyright claims, but these systems often generate disputes and demonetization.

Tax compliance adds complexity for creators earning income across multiple jurisdictions. International creators may owe taxes in multiple countries. The rise of digital nomad creators further complicates tax residency questions. Professional creators increasingly require accounting and legal support to manage compliance obligations.

Key Players and Competitive Landscape

The creator economy ecosystem comprises multiple layers, from platforms that host content to tools that enable creation, management, and monetization. Understanding the competitive landscape is essential for creators choosing where to invest their time and for brands seeking partnership opportunities.

Major Platforms

YouTube remains the dominant platform for creator monetization, with its Partner Program setting the standard for revenue sharing. The platform’s combination of ad revenue, channel memberships, Super Chat, and shopping features provides creators with multiple income streams. YouTube’s 61.8 million creators represent the largest creator base of any single platform.

TikTok has revolutionized short-form video and become essential for reaching younger demographics. The platform’s Creativity Program Beta, live gifting, and TikTok Shop provide monetization pathways, though creators often report lower direct earnings compared to YouTube. TikTok’s strength lies in discovery and viral potential.

Instagram continues to evolve, with Reels competing directly with TikTok and Shopping features enabling creator commerce. Meta’s Creator Fast Track program now pays $1,000-$3,000 monthly to creators with 100,000+ followers, signaling serious investment in creator retention.

LinkedIn has emerged as the breakout platform for B2B creators, with professional content gaining significant traction. The platform’s focus on knowledge sharing and professional development has created opportunities for subject matter experts to build influential audiences.

Creator Economy Infrastructure

Beyond platforms, a robust infrastructure of tools and services has emerged to support creator businesses. These include:

Content Creation Tools: Runway provides professional-grade AI video generation. Synthesia offers AI-powered video creation for businesses and creators. CapCut, now integrated with LinkedIn, provides accessible video editing.

Monetization Platforms: Patreon pioneered creator subscriptions and continues to lead the space. Substack dominates newsletter monetization. Gumroad enables digital product sales. Stan Store and similar platforms provide all-in-one creator storefronts.

Creator Management: Agentio raised $40 million in Series B funding for its YouTube creator marketplace, connecting brands with creators at scale. ShopMy secured $26.5 million for its affiliate marketing platform. Passes raised $40 million for its creator monetization tools.

Analytics and Discovery: HypeAuditor provides creator analytics and fraud detection. ThoughtLeaders offers data-driven creator discovery and campaign management. CreatorIQ’s State of Creator Marketing report has become an industry benchmark.

Venture Capital and Investment

The creator economy raised over $1.5 billion in 2024, with 2025 and 2026 showing continued strong investment activity. Key investors include Benchmark, Lightspeed Venture Partners, Bond Capital, New Enterprise Associates, and AlleyCorp.

Notable funding rounds include Substack’s $100 million Series C in July 2025, beehiiv’s $33 million Series B, and multiple eight-figure rounds for AI-powered creator tools. The investment focus has shifted toward infrastructure and monetization tools rather than new platforms.

Harlem Capital and other firms specifically focus on supporting minority and women creators, recognizing the untapped potential in diverse creator communities. This focus on equity and inclusion represents a maturation of the creator economy investment thesis.

Challenges and Pain Points

Despite its growth and potential, the creator economy faces significant challenges that creators, platforms, and brands must navigate. Understanding these pain points is essential for sustainable success.

1. Platform Dependency and Algorithm Volatility

The single greatest risk for creators is platform dependency. Algorithm changes can decimate reach overnight, policy updates can demonetize content, and platform bans can destroy years of audience building. The 2025 TikTok ban discussions in the U.S. highlighted this vulnerability for millions of creators.

Creators are responding by building owned audiences through email lists and private communities, but this requires significant additional effort and expertise. The tension between platform reach and audience ownership remains unresolved.

2. Income Inequality and Sustainability

The creator economy exhibits extreme income inequality. While top creators earn millions, the majority struggle to make sustainable incomes. Research indicates that nearly half of creators still earn under $10,000 annually, and the $15,000 annual earnings threshold separates creators who struggle from those positioned to scale.

This inequality creates a “winner-take-all” dynamic that can discourage new entrants and limit the diversity of voices in the creator economy. The challenge for platforms and tools is to democratize success and provide pathways for mid-tier creators to build sustainable businesses.

3. Content Saturation and Discovery

With 207 million creators producing content, standing out has never been more difficult. Content saturation means that even high-quality work can go unnoticed without algorithmic favor or significant promotion budgets.

The average creator earns only 2-3% of their audience size as annual revenue—a stark reminder of how challenging monetization remains for most. Breaking through requires not just creativity but strategic understanding of platform algorithms, SEO, and audience psychology.

4. Burnout and Mental Health

The pressure to consistently produce content, engage with audiences, and stay relevant takes a significant toll on creator mental health. The always-on nature of social media, combined with public scrutiny and algorithmic pressure, contributes to high rates of burnout.

Creators report feeling trapped in content treadmills, unable to take breaks without losing momentum. The lack of traditional employment benefits—health insurance, retirement plans, paid time off—adds to the stress of creator life.

5. Brand Partnership Complexity

While brand deals remain the primary revenue source for most creators, securing and managing partnerships is complex and time-consuming. Negotiating contracts, ensuring FTC compliance, maintaining authenticity, and managing brand relationships requires skills that many creators lack.

The rise of creator management agencies and platforms like Agentio addresses this challenge, but these services typically take significant cuts of creator earnings. The power imbalance between brands and individual creators remains a persistent issue.

Opportunities and Growth Strategies

Despite the challenges, the creator economy offers unprecedented opportunities for those who approach it strategically. Here are the key growth strategies that successful creators are employing in 2026.

1. Niche Specialization and Authority Building

The days of generalist creators are fading. The most successful creators in 2026 are those who dominate specific niches, building authority that commands premium pricing and loyal audiences. Whether it’s B2B SaaS marketing, sustainable fashion, or vintage watch restoration, deep expertise trumps broad appeal.

This specialization enables creators to charge premium rates for courses, consulting, and partnerships. It also creates defensible moats—generalist content can be replicated, but deep expertise cannot.

2. Community-First Business Models

The most sustainable creator businesses are built around communities rather than content alone. Paid memberships, private groups, and cohort-based courses create recurring revenue and deeper audience relationships.

Survey data shows that 69% of creators prioritize member transformation as their primary growth driver. This community-centric approach creates value that extends beyond individual pieces of content, building businesses that can weather algorithm changes and platform shifts.

3. AI-Augmented Workflows

Creators who embrace AI tools gain significant competitive advantages. AI can handle research, drafting, editing, thumbnail creation, and analytics—freeing creators to focus on strategy, creativity, and community building.

The key is using AI as an amplifier rather than a replacement. The most successful creators maintain their unique voices and perspectives while leveraging AI to increase output and quality.

4. Cross-Platform Presence with Owned Audiences

Successful creators maintain presence across multiple platforms while building owned audiences through email lists and private communities. This strategy maximizes reach while minimizing platform risk.

The framework is clear: use discovery platforms (TikTok, Instagram, YouTube) to attract attention, then convert that attention to owned channels (email, communities, courses) where monetization is more effective and relationships are deeper.

5. Strategic Brand Partnerships

While brand deals remain important, the nature of partnerships is evolving. Long-term ambassadorships are replacing one-off sponsored posts, and creators are increasingly selective about brand alignments.

Creators are also building their own affiliate programs, creating passive income streams that don’t require ongoing content creation. This shift from active to passive revenue is a hallmark of mature creator businesses.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes possible in the creator economy. These case studies represent different paths to success.

Case Study 1: The B2B Creator Pivot

A former marketing executive built a LinkedIn following of 500,000+ by sharing tactical B2B marketing advice. Rather than pursuing traditional brand deals, this creator launched a cohort-based course generating $2 million annually, a newsletter with 100,000 subscribers, and a consulting practice serving enterprise clients.

The key insight: B2B audiences have higher lifetime value and are willing to pay premium prices for professional development. By positioning as an industry expert rather than an influencer, this creator built a seven-figure business with just a mid-sized audience.

Case Study 2: The Community-First Approach

A fitness creator with 200,000 Instagram followers shifted focus from content to community, launching a paid membership program through Circle. Within 18 months, 5,000 members at $30/month generated $1.8 million in annual recurring revenue—far exceeding what brand deals would have provided.

The creator now employs a team of coaches and community managers, transforming a personal brand into a scalable business. The membership model provides predictable revenue and deeper member transformation than free content ever could.

Case Study 3: The AI-Enhanced Creator

A technology educator leveraged AI tools to 10x content output without sacrificing quality. Using AI for research, script drafting, and video editing, this creator publishes daily across YouTube, TikTok, and Instagram while maintaining a newsletter and course business.

The result: 2 million combined followers, multiple seven-figure revenue streams, and a team of just three people. AI didn’t replace this creator’s expertise—it amplified their ability to share it.

Future Outlook and Predictions (2026-2030)

The creator economy will look radically different by 2030. Based on current trends and expert projections, here are the key developments to expect.

Market Size Projections

By 2030, the creator economy is projected to reach $528-600 billion, with some estimates suggesting it could exceed $2 trillion by 2035. This growth will be driven by continued platform innovation, expanding global internet access, and the normalization of creator careers.

The number of professional creators—those earning sustainable full-time incomes—will increase significantly, though income inequality will likely persist. The $15,000 threshold that currently separates hobbyists from professionals may rise as the bar for entry increases.

Platform Evolution

Platforms will continue converging, with social media, commerce, and entertainment becoming indistinguishable. TikTok is reportedly developing a revamped TV app focused on higher-quality, long-form content. Instagram has launched a dedicated TV experience on Amazon Fire TV. Netflix is licensing creator content and partnering with Spotify for video podcasts.

The distinction between traditional media and creator content will blur further. We’re already seeing creators like Ms. Rachel and Mark Rober sign Netflix deals—a trend that will accelerate as platforms compete for proven talent.

AI and Synthetic Media

By 2030, AI influencers and synthetic media will represent a significant portion of the creator economy. The synthetic talent market alone is projected to be worth tens of billions. Creators will increasingly license their likenesses to AI companies, creating passive income from AI-generated content.

However, regulatory frameworks will evolve to address disclosure requirements and consumer protection. The EU AI Act and FTC guidelines are just the beginning of a complex regulatory landscape that will shape how AI is used in content creation.

Creator Business Maturation

The era of the solo creator will give way to creator-led media companies. Successful creators will build teams, develop IP, and create diversified businesses that extend far beyond social media content. The creator economy will increasingly resemble the traditional media industry—but with lower barriers to entry and more democratic distribution.

Management agencies will evolve from deal facilitators to operating partners, providing strategic guidance, business development, and infrastructure support. The most successful creator businesses will be those that professionalize operations while maintaining authentic audience connections.

The Evolution of Creator Business Models

The business models employed by successful creators have evolved dramatically over the past five years. What began as simple advertising revenue sharing has transformed into sophisticated multi-channel enterprises that rival traditional media companies in complexity and revenue potential.

In the early days of the creator economy, business models were straightforward. YouTube creators earned through AdSense revenue sharing. Bloggers relied on display advertising and occasional sponsored posts. Instagram influencers charged flat fees for sponsored content. These models were simple but fragile—dependent on single platforms and subject to algorithmic whims.

Today’s successful creator businesses operate on what industry analysts call the “hub and spoke” model. The hub consists of owned assets—email lists, private communities, and proprietary products. The spokes are discovery platforms—YouTube, TikTok, Instagram, LinkedIn—that drive traffic to the hub. This model provides both reach and resilience.

Subscription-based models have emerged as particularly powerful. Patreon pioneered the space, but platforms like Substack, beehiiv, and Circle have expanded the possibilities. Creators can now offer tiered memberships with varying levels of access, community features, and exclusive content. The predictability of recurring revenue transforms creator businesses from feast-or-famine operations into stable enterprises.

Digital products represent another evolution in creator monetization. Rather than trading time for money through sponsored posts, creators develop products that can be sold infinitely without additional effort. Courses, templates, ebooks, and software tools enable creators to scale their impact and income simultaneously. The most successful creators now generate the majority of their revenue from products rather than services.

The emergence of creator-led commerce has added physical products to the mix. Creators are launching merchandise lines, beauty brands, and consumer products that leverage their audience relationships. This vertical integration—owning the product, the marketing, and the distribution—offers margins that traditional brand partnerships cannot match.

Licensing and IP deals represent the highest tier of creator business models. Established creators license their content, likeness, and intellectual property for use by media companies, brands, and platforms. Netflix’s deals with creators like Ms. Rachel and Mark Rober exemplify this trend. As the creator economy matures, IP ownership will become increasingly important for long-term value creation.

Regional Variations in the Creator Economy

While the creator economy is global in scope, significant regional variations exist in terms of market maturity, platform preferences, monetization approaches, and regulatory environments. Understanding these differences is essential for creators and brands operating internationally.

North America remains the largest creator economy market by revenue, driven by high advertising rates, mature monetization infrastructure, and a culture that celebrates entrepreneurship. The United States alone accounts for a significant portion of global influencer marketing spend, with brands allocating $37.1 billion annually to creator partnerships. American creators benefit from established legal frameworks, robust payment systems, and a large domestic audience.

Europe presents a more fragmented landscape. The European Union’s regulatory environment, including GDPR privacy regulations and the Digital Services Act, creates compliance challenges for creators and platforms. However, European audiences show strong engagement with creator content, and cities like London, Berlin, and Paris have emerged as creator economy hubs. The EU AI Act will further shape how AI-generated content is created and disclosed.

Asia-Pacific represents the fastest-growing region in terms of creator numbers. India alone has millions of active creators across platforms like YouTube, Instagram, and regional apps like ShareChat and Moj. Southeast Asian markets—Indonesia, Thailand, Vietnam—are experiencing explosive growth in mobile-first content consumption. The region’s young demographics and improving digital infrastructure suggest continued expansion.

China operates as a distinct ecosystem due to platform restrictions and regulatory differences. While Western platforms are largely inaccessible, domestic alternatives like Douyin (TikTok’s Chinese version), Xiaohongshu (Little Red Book), and Bilibili have created thriving creator economies. Chinese creators often lead in live commerce and social shopping innovations that later spread to Western markets.

Latin America and the Middle East represent emerging markets with significant potential. Brazil, Mexico, and Argentina have vibrant creator communities, while Gulf states are investing heavily in digital content as part of economic diversification efforts. These markets often leapfrog traditional media development, moving directly to creator-driven content consumption.

The Role of Platforms in Shaping the Creator Economy

Platforms are not neutral infrastructure—they actively shape the creator economy through algorithmic decisions, policy choices, and monetization feature development. Understanding platform dynamics is essential for creator success.

YouTube’s Partner Program remains the gold standard for creator monetization. The platform shares 55% of ad revenue with creators, providing transparent metrics and predictable income. YouTube’s algorithm favors watch time and session duration, incentivizing longer, more engaging content. The platform’s investment in Shorts, memberships, and shopping features demonstrates its commitment to creator monetization.

TikTok has revolutionized content discovery through its “For You Page” algorithm, which can catapult unknown creators to viral fame overnight. However, the platform’s monetization features lag behind its discovery capabilities. The Creativity Program Beta offers revenue sharing, but creators often report lower earnings per view compared to YouTube. TikTok Shop represents the platform’s bet on social commerce as a monetization pathway.

Instagram has evolved from a photo-sharing app to a comprehensive creator platform. Reels competes directly with TikTok for short-form video attention, while Shopping features enable direct commerce. Meta’s Creator Fast Track program, paying $1,000-$3,000 monthly to qualifying creators, signals serious investment in retention. However, Instagram’s algorithm changes have historically disrupted creator businesses, highlighting platform dependency risks.

LinkedIn’s emergence as a creator platform represents a significant development. The professional network’s focus on knowledge sharing and career development has created opportunities for B2B creators who would struggle on entertainment-focused platforms. LinkedIn’s revenue-sharing programs and CapCut integration demonstrate its commitment to the creator economy.

Emerging platforms like Twitch, Discord, and Telegram offer specialized environments for community building and monetization. Twitch dominates live streaming, particularly in gaming. Discord enables private community spaces with subscription capabilities. Telegram’s channel features support large-scale broadcast messaging. These platforms serve specific creator needs that mainstream social media cannot address.

Regulatory Landscape and Compliance

As the creator economy matures, regulatory scrutiny has increased. Creators and brands must navigate complex legal requirements around advertising disclosure, data privacy, intellectual property, and emerging AI regulations.

The Federal Trade Commission (FTC) in the United States requires clear disclosure of material connections between creators and brands. Sponsored content must be labeled with hashtags like #ad or #sponsored. Failure to comply can result in fines and reputational damage. The FTC has increased enforcement actions against both creators and brands for inadequate disclosure.

The European Union’s General Data Protection Regulation (GDPR) affects how creators collect and process audience data. Email list building, analytics tracking, and personalized advertising all fall under GDPR requirements. Creators targeting European audiences must implement compliant data practices or risk significant penalties.

The EU AI Act introduces new requirements for AI-generated content. Creators using AI tools must disclose when content is artificially generated. Virtual influencers face specific labeling requirements. These regulations will shape how AI is integrated into creator workflows and how audiences perceive AI-generated content.

Copyright and intellectual property issues remain persistent challenges. Creators must navigate fair use doctrines when incorporating third-party content. Music licensing, in particular, creates friction for video creators. Platforms have implemented content ID systems to manage copyright claims, but these systems often generate disputes and demonetization.

Tax compliance adds complexity for creators earning income across multiple jurisdictions. International creators may owe taxes in multiple countries. The rise of digital nomad creators further complicates tax residency questions. Professional creators increasingly require accounting and legal support to manage compliance obligations.

Key

Takeaways

- The digital creator economy has matured into a $254 billion industry employing over 207 million people worldwide, with projections suggesting it could exceed $2 trillion by 2035.

- Revenue diversification is essential: creators with three or more income streams earn $75,000 more annually than those relying on a single source.

- AI adoption has reached mainstream levels with 84% of creators using AI tools, enabling 10x content output and new forms of synthetic media.

- The migration from rented platforms to owned audiences through email lists, memberships, and communities represents the most significant strategic shift in the creator economy.

- B2B creators are emerging as a distinct and lucrative segment, with LinkedIn becoming the breakout platform for professional content creators.

- While brand deals remain the primary revenue source (68.8% of creators), paid memberships (88%), courses (53%), and coaching (51%) are gaining ground.

- The creator economy faces significant challenges including platform dependency, income inequality, content saturation, and creator burnout that must be addressed for sustainable growth.

Sources and Citations

- Research Nester – Creator Economy Market Size & Share | Forecast Report 2026-2035: https://www.researchnester.com/reports/creator-economy-market/5691

- Precedence Research – Creator Economy Market Size to Hit USD 2084.57 Billion by 2035: https://www.precedenceresearch.com/creator-economy-market

- Goldman Sachs – The creator economy could approach half-a-trillion dollars by 2027: https://www.goldmansachs.com/insights/articles/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027

- Exploding Topics – Creator Economy Market Size (2025-2030): https://explodingtopics.com/blog/creator-economy-market-size

- Archive.com – 25 Creator Economy Market Size Statistics Every Brand Should Track in 2026: https://archive.com/blog/creator-economy-market-size

- Companies History – Creator Economy Statistics And Market Size 2026: https://www.companieshistory.com/creator-economy-market-size/

- The Influencer Marketing Factory – The 2026 Creator Economy Report: https://theinfluencermarketingfactory.com/creator-economy/

- Circle Blog – Creator Economy Statistics for 2026: https://circle.so/blog/creator-economy-statistics

- LinkedIn (Lindsey Gamble) – Creator Economy: Key Trends from 2025 & Predictions for 2026: https://www.linkedin.com/pulse/creator-economy-key-trends-from-2025-predictions-2026-lindsey-gamble-2hk2e

- Stan Store – 8 Trends That Will Define the Creator Economy in 2026: https://stan.store/blog/creator-economy-trends-2026/

- Forbes – The Creator Economy In 2026: The Era Of Consolidation: https://www.forbes.com/sites/jasondavis/2026/01/26/the-creator-economy-in-2026—the-era-of-consolidation/

- Business Insider – 17 creator-economy startups to watch in 2026, according to VCs: https://www.businessinsider.com/creator-economy-ai-startups-to-watch-according-vc-investors-2026-3

- Ellty – 15 Creator Economy Investors Funding Content Startups 2026: https://www.ellty.com/blog/creator-economy-investors

- Visible.vc – Top Creator Economy Startups and the VCs That Fund Them in 2026: https://visible.vc/blog/creator-economy-vcs/

- Playbella – The 2026 Global Report on Synthetic Influence: https://playbella.org/blog/2026-ai-influencer-landscape-report

- Metricool – Virtual & AI Influencers in 2026: https://metricool.com/ai-virtual-influencers/

- Uscreen – Content Creator Income in 2026: Average Salaries and Tips: https://www.uscreen.tv/blog/content-creator-income/

- DemandSage – 41+ Creator Economy Statistics 2026: https://www.demandsage.com/creator-economy-statistics/

- IAB – Brands in the Creator Economy Are Proving Performance: https://www.iab.com/blog/brands-in-the-creator-economy-are-proving-performance/

- LA Times – The Creator Economy in Los Angeles, 2026: A New Frontier: https://www.latimes.com/b2b/entertainment/story/2026-03-22/los-angeles-creator-economy-2026-trends