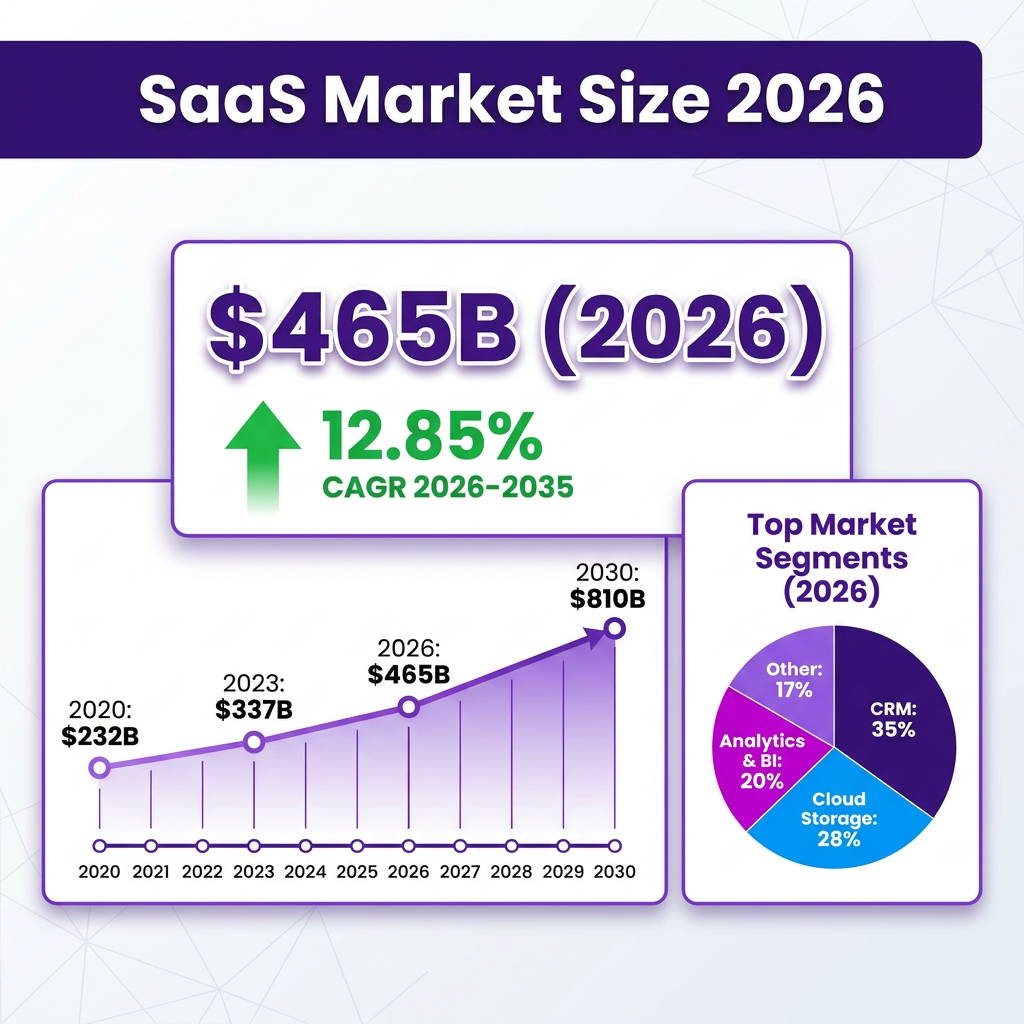

The global Software as a Service (SaaS) market has reached an inflection point in 2026. With a market valuation of $465.03 billion according to Precedence Research, SaaS has evolved from a disruptive technology to the dominant software delivery model worldwide. This represents a significant jump from $408.21 billion in 2025, demonstrating the continued acceleration of cloud adoption across industries.

What is driving this explosive growth? The answer lies in a perfect storm of factors: the widespread shift to remote and hybrid work, the integration of artificial intelligence into core business processes, and the increasing demand for flexible, scalable software solutions. As businesses continue their digital transformation journeys, SaaS has become the foundation upon which modern enterprises are built.

Market Overview: The $465 Billion Ecosystem

The SaaS market trajectory has been nothing short of remarkable. From humble beginnings in the early 2000s to becoming a nearly half-trillion-dollar industry, the growth curve shows no signs of flattening. According to multiple industry analysts, the market is projected to reach $887.05 billion by 2030 and an astounding $1.37 trillion by 2035, representing a compound annual growth rate (CAGR) of 12.85% from 2026 to 2035.

This growth is not uniform across all segments. The B2B SaaS market specifically is experiencing even more aggressive expansion, with Mordor Intelligence projecting growth from $492.34 billion in 2026 to $1.58 trillion by 2031 at a CAGR of 26.24%. This divergence highlights how enterprise software needs are driving disproportionate value creation in the sector.

The United States continues to dominate the global SaaS landscape, hosting approximately 17,000 of the world SaaS companies. The US SaaS market alone is valued at $187 billion, serving as both the innovation hub and primary revenue center for the industry. However, growth is increasingly global, with significant expansion in Europe, Asia-Pacific, and emerging markets.

Looking at the deployment models, public cloud continues to lead adoption, particularly among small and medium enterprises that lack the resources to manage private infrastructure. However, hybrid cloud deployments are gaining traction as larger enterprises seek to balance flexibility with security and compliance requirements. Private cloud SaaS still commands the largest revenue share, driven by enterprise demand for controlled environments.

The application landscape within SaaS reveals interesting patterns. Customer Relationship Management (CRM) solutions maintain the largest market share at approximately 20%, followed by Enterprise Resource Planning (ERP) at 18%, and collaboration tools at 15%. Human Capital Management (HCM), Business Intelligence and Analytics, and content management systems round out the major categories, each capturing significant portions of the market.

Key Statistics and Data Points

Understanding the SaaS market requires diving deep into the numbers that define its scale, growth patterns, and operational benchmarks. Here are the critical statistics that every SaaS founder, investor, and industry observer should know in 2026:

Market Size and Growth Metrics

- Global SaaS market size (2026): $465.03 billion (Precedence Research)

- Alternative market estimate: $512.27 billion (Statista)

- B2B SaaS market (2026): $492.34 billion

- Projected market size (2030): $887.05 billion

- Long-term projection (2035): $1.37 trillion

- CAGR (2026-2035): 12.85%

- B2B SaaS CAGR (2026-2031): 26.24%

- US market share: $187 billion

- Number of SaaS companies globally: Over 30,000

- SaaS companies in the US: 17,000

Adoption and Usage Statistics

- Organizations using SaaS: 99% of companies worldwide

- Average SaaS applications per business: 305+ tools

- Public SaaS companies (enterprise): Average 1,500 customers

- Public SaaS companies (mid-market): Average 13,000 customers

- AI adoption in SaaS: 75% of companies embedding AI by end of 2026

Revenue and Growth Benchmarks

- Median private SaaS growth rate: 25% year-over-year

- Bootstrapped SaaS growth (median): 15% annually ($3M-$20M ARR range)

- Equity-backed SaaS growth (median): 30% annually

- 90th percentile bootstrapped growth: 42.3%

- Target ARR growth for healthy SaaS: 40%+ annually

- Companies with flat/negative growth: 6.9% (up from 5.3% in 2023)

Retention and Churn Benchmarks

- Net Revenue Retention (NRR) target: 106%

- Best-in-class NRR: 120-130%

- Median NRR (bootstrapped): 103%

- 90th percentile NRR: 117.9%

- Gross Revenue Retention (GRR) target: 85-95%

- Median GRR (bootstrapped): 91%

- Annual churn target: Under 5%

- Monthly churn (good): Under 1%

- Average monthly churn: 5-7%

Customer Acquisition and Efficiency Metrics

- Average B2B SaaS CAC: $1,200

- CAC payback period target: Under 12 months

- Excellent CAC payback: 12-15 months

- Sales efficiency (Magic Number) target: Greater than 1.0

- Best-in-class CAC efficiency: $1 ARR for every $0.50-0.75 spend

- Expansion revenue target: ~40% of new ARR

Marketing and ROI Statistics

- SEO ROI for B2B SaaS: 702%

- SEO break-even time: 7 months

- Content marketing ROI: 420% (highest of any sector)

- Email marketing effectiveness: 59% of B2B marketers name it most effective channel

- Average sales cycle (Series A): 78 days

Major Trends Shaping SaaS in 2026

The SaaS landscape is undergoing a fundamental transformation driven by technological innovation, changing customer expectations, and evolving business models. Here are the seven major trends defining the industry in 2026:

1. Native AI Integration

Artificial intelligence is no longer a bolt-on feature—it is becoming the core of modern SaaS products. By the end of 2026, 75% of SaaS companies are expected to embed AI-driven automation in at least one core process. The AI SaaS market segment alone is projected to exceed $200 billion.

This shift from “AI-enhanced” to “AI-native” represents a fundamental change in how software is built and delivered. Companies that merely retrofit AI features onto existing products face what industry experts call “innovation debt,” while those built with AI at their core are capturing disproportionate market share.

However, this trend comes with challenges. Compute costs for large language models can inflate expenses by 30-110%, creating “invoice shock” if not properly managed through dynamic pricing models. Successful AI-native SaaS companies are those that have figured out how to deliver AI value while maintaining sustainable unit economics.

2. The Rise of Vertical SaaS

Horizontal SaaS—tools designed for broad applicability across industries—is facing increasing competition from vertical solutions built for specific industries. Healthcare, agriculture, construction, and other traditionally analog-heavy sectors are rapidly adopting industry-specific cloud tools.

Vertical SaaS vendors are becoming acquirers themselves, expanding within industries by purchasing complementary tools that deepen critical workflows. This consolidation creates comprehensive platforms that are difficult for horizontal competitors to displace. The trend is driven by buyer demand for software that understands the unique realities of their specific industries.

Investors have taken notice. Annual funding volumes for vertical SaaS show consistent growth, with late-stage funding rounds growing larger as investor confidence in the scalability of mature vertical SaaS companies increases.

3. Agentic AI and Autonomous Software

The next evolution beyond AI integration is “agentic” software—SaaS products that do not just assist users but act autonomously on their behalf. Instead of users learning complex software interfaces, AI agents understand goals and execute tasks independently.

This represents a paradigm shift from software as a tool to software as a partner. Modern SaaS is becoming proactive rather than reactive, anticipating user needs and taking action without explicit instruction. The implications for user experience and productivity are profound.

Early implementations are already showing promise in areas like customer support, where AI agents handle routine inquiries end-to-end, and in sales, where agents can research prospects, craft personalized outreach, and even schedule meetings.

4. Flexible and Usage-Based Pricing

The traditional per-seat subscription model is under pressure as customers demand pricing that better aligns with value received. Usage-based pricing, outcome-based models, and hybrid approaches are gaining traction across the industry.

This shift is particularly important for AI-enhanced SaaS, where compute costs can vary dramatically based on usage. Companies that implement dynamic pricing models can better manage cost volatility while providing transparency to customers.

The most sophisticated SaaS companies are moving toward pricing models that grow with customer success—capturing more revenue as customers derive more value, rather than charging purely for access.

5. API-First Architecture and Ecosystem Integration

With the average business using 305+ SaaS applications, integration has become critical. API-first SaaS companies are winning because they fit seamlessly into existing tech stacks rather than requiring customers to change their workflows.

This trend extends beyond simple data exchange to deep workflow integration. The most successful SaaS products are those that become invisible infrastructure—powering business processes without creating friction or requiring constant user attention.

The ecosystem approach is becoming a competitive moat. SaaS companies with robust integration marketplaces and partner ecosystems create switching costs that make customer retention easier and acquisition more efficient.

6. Embedded Fintech

Financial services are increasingly being embedded directly into SaaS platforms. Payment processing, lending, insurance, and payroll are becoming native features rather than integrations with third-party providers.

For vertical SaaS in particular, embedded fintech represents a massive revenue expansion opportunity. A construction management platform that can also handle payments, insurance, and equipment financing captures significantly more value per customer than one that merely manages projects.

AI-enhanced compliance SaaS for SMBs is one standout example, with platforms saving customers $12,000 annually in regulated niches like finance and achieving $50M+ ARR by combining software with embedded financial services.

7. Privacy-First and Compliance Automation

With increasing regulatory complexity—GDPR in Europe, state-level privacy laws in the US, and industry-specific regulations—compliance has become a major pain point for businesses. SaaS companies that can automate compliance are finding strong product-market fit.

This trend goes beyond mere compliance checklists to proactive privacy management. Modern SaaS platforms are building in privacy by design, with automated data classification, consent management, and regulatory reporting.

The market is rewarding SaaS companies that can turn compliance from a cost center into a competitive advantage—enabling customers to enter new markets faster and with less risk.

Key Players and Competitive Landscape

The SaaS market is dominated by a mix of established technology giants and specialized innovators. Understanding the competitive landscape is essential for anyone looking to enter or compete in this space.

The Big Three: Microsoft, Salesforce, and Adobe

Microsoft continues to be the dominant force in SaaS through its Office 365 and Azure platforms. With comprehensive productivity, collaboration, and cloud infrastructure offerings, Microsoft has built an ecosystem that is deeply embedded in enterprise workflows worldwide.

Salesforce remains the CRM leader with $41.5 billion in FY2026 revenue and 20.7% of the global CRM market according to IDC. The company CRM revenue alone exceeds that of Microsoft, Oracle, Adobe, and SAP combined. Salesforce platform approach, with extensive customization and integration capabilities, has created significant switching costs for its enterprise customers.

Adobe has successfully transitioned from packaged software to SaaS through its Creative Cloud and Document Cloud offerings. The company focus on creative professionals and digital experience management has created a loyal customer base with strong retention characteristics.

Emerging Leaders and Specialized Players

Beyond the giants, several companies are defining specific SaaS categories:

- ServiceNow: Dominating IT service management and expanding into workflow automation across the enterprise

- Snowflake: Leading the data warehouse and analytics space with a cloud-native approach

- Datadog: Setting the standard for cloud monitoring and observability

- CrowdStrike: Defining modern cybersecurity with its cloud-native endpoint protection

- Zoom: Despite post-pandemic normalization, remaining a critical communication infrastructure

- HubSpot: Leading the inbound marketing and sales automation space, particularly for SMBs

- Workday: Dominating HR and financial management for large enterprises

- Shopify: Powering e-commerce for millions of merchants worldwide

The Long Tail: 30,000+ SaaS Companies

While the giants capture headlines and significant market share, the long tail of SaaS companies—numbering over 30,000 globally—represents the true diversity of the industry. These companies serve niche markets, specific use cases, and regional needs that larger players cannot address effectively.

The United States hosts approximately 17,000 SaaS companies, but significant innovation is emerging from Europe, Israel, India, and other technology hubs. This geographic diversity is creating a rich ecosystem of solutions for virtually every business need.

Interestingly, 31.4% of Salesforce deployments belong to companies with 10 or fewer employees, demonstrating that even enterprise-grade SaaS has found traction in the SMB market. This democratization of enterprise software is a defining characteristic of the modern SaaS landscape.

Challenges and Pain Points

Despite the impressive growth and opportunity in SaaS, the industry faces significant challenges that founders, operators, and investors must navigate carefully.

1. Intensifying Competition and Market Saturation

The barrier to entry for SaaS has never been lower. With “vibe coding” and AI-assisted development tools, building a SaaS product requires less technical expertise than ever before. While this democratization is positive for innovation, it has created intense competition in virtually every category.

Investors are increasingly selective, with many declaring they will not fund SaaS concepts anymore—they want to see traction, revenue, and clear differentiation. The average sales cycle for Series A SaaS startups has risen to 78 days, reflecting more cautious buyer behavior and increased scrutiny of new vendors.

SaaS valuations hit decade-plus lows in Q1 2026 as markets priced in AI as an existential threat. The market is painting all SaaS companies with the same brush rather than distinguishing potential winners from losers, creating both risk and opportunity.

2. The Churn Challenge

Customer churn remains the silent killer of SaaS businesses. The average SaaS company loses 5-7% of its customer base every month. At 6% monthly churn, a company is essentially replacing its entire customer base every 14 months—not growing, but running on a treadmill.

The math is brutal: with $50,000 in monthly recurring revenue and 6% churn, a company loses $3,000 every 30 days. Reducing churn from 10% to 8% annually can create 20%+ revenue impact over 3-5 years through improved retention economics.

Churn comes in two forms: voluntary (customers choosing to leave) and involuntary (payment failures). While voluntary churn is a product and value problem, involuntary churn is almost entirely recoverable with the right retry logic and dunning sequences. Yet many SaaS companies underinvest in payment recovery systems.

3. Technical Debt and Integration Complexity

With the average business using 305+ SaaS applications, integration has become both a requirement and a challenge. Too many tools lead to technical debt: outdated software, siloed data, and frustrated employees struggling with systems that do not talk to each other.

SaaS companies must invest heavily in integration capabilities, API development, and ecosystem partnerships. Those that do not become isolated islands in the enterprise tech stack, vulnerable to replacement by more connected competitors.

The challenge is particularly acute for older SaaS companies that built their architectures before API-first design became standard. Retrofitting connectivity into legacy systems is expensive and time-consuming.

Opportunities and Growth Strategies

Despite the challenges, significant opportunities exist for SaaS companies that can execute effectively. Here are the key growth strategies that are working in 2026:

1. Vertical Expansion and Industry Specialization

The most significant opportunity in SaaS is verticalization. Industry-specific solutions command premium pricing, achieve higher retention rates, and face less direct competition than horizontal alternatives.

Vertical SaaS platforms are increasingly leveraging AI and embedded fintech to automate complex, industry-specific workflows. This combination of deep domain expertise and modern technology creates powerful competitive moats.

Investors continue to pour significant capital into vertical SaaS startups, with late-stage funding rounds growing larger as confidence in the scalability of mature vertical SaaS companies increases. The fastest growth is coming from analog-heavy industries like healthcare, agriculture, and construction that are rapidly adopting industry-specific cloud tools.

2. AI-Native Product Development

Building AI into products from the ground up—rather than retrofitting it—is creating significant competitive advantages. AI-native SaaS companies are capturing market share from legacy players by delivering fundamentally different user experiences.

The key is moving beyond simple automation to true intelligence—software that learns, adapts, and improves over time. Companies that can deliver personalized experiences at scale through AI are seeing dramatic improvements in engagement and retention.

However, success requires managing compute costs effectively. The companies winning in AI SaaS are those that have figured out how to deliver AI value while maintaining sustainable unit economics through efficient model selection, caching strategies, and dynamic pricing.

3. Ecosystem and Platform Strategies

The most successful SaaS companies are becoming platforms—enabling third-party developers to build on their infrastructure and create value for their customers. This ecosystem approach creates network effects that make platforms increasingly valuable as they grow.

Platform strategies require significant investment in developer experience: comprehensive APIs, clear documentation, sandbox environments, and support resources. But the payoff is a vibrant ecosystem that extends the platform capabilities far beyond what any single company could build.

Companies like Salesforce, Shopify, and Slack have demonstrated the power of platform strategies. Their success is inspiring a new generation of SaaS companies to think platform-first from day one.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes that are possible in the SaaS market. Here are three case studies that demonstrate different paths to success:

Case Study 1: Salesforce—Platform Ecosystem Dominance

Salesforce journey from a simple CRM to a $41.5 billion enterprise software giant offers lessons in platform strategy and ecosystem development. By opening its platform to third-party developers early, Salesforce created an AppExchange marketplace that now hosts thousands of applications.

The company success stems from understanding that CRM is not just a software category but a platform for customer engagement. By enabling developers to extend its capabilities, Salesforce created switching costs that make it difficult for customers to leave—even as competitors offer lower prices.

Key metrics: 20.7% global CRM market share, $21.6 billion in CRM revenue alone, and a platform that processes over 1 trillion transactions per quarter.

Case Study 2: Snowflake—Data Cloud Innovation

Snowflake rise in the data warehouse market demonstrates the power of cloud-native architecture and consumption-based pricing. By separating compute from storage and enabling seamless data sharing between organizations, Snowflake created a fundamentally different approach to data management.

The company success highlights several key strategies: technical differentiation through architecture innovation, pricing alignment with value (customers pay for what they use), and network effects through the Data Marketplace where customers can share and monetize data.

Snowflake growth trajectory—reaching billions in revenue in less than a decade—shows that even in markets dominated by giants like Amazon and Google, innovative startups can capture significant market share through superior product design.

Case Study 3: Bootstrapped SaaS—Sustainable Growth

While venture-backed SaaS companies grab headlines, bootstrapped SaaS represents a significant portion of the market. According to SaaS Capital 2026 survey of over 1,000 private B2B SaaS companies, bootstrapped companies with $3M to $20M in ARR show median revenue growth of 15%, Net Revenue Retention of 103%, and Gross Revenue Retention of 91%.

The 90th percentile of bootstrapped SaaS companies are growing by 42.3% annually with NRR of 117.9%. These companies demonstrate that sustainable, profitable growth is possible without venture capital—though the path requires disciplined capital efficiency and customer focus.

Key lessons: focus on profitability from day one, prioritize customer retention over growth at all costs, and build products that solve specific, high-value problems.

Future Outlook and Predictions

The SaaS market trajectory through 2030 and beyond will be shaped by technological innovation, evolving customer expectations, and macroeconomic factors. Here is what industry analysts and experts predict:

Market Size Projections

By 2030, the global SaaS market is projected to reach $887 billion, nearly doubling from 2026 levels. The long-term outlook to 2035 suggests a $1.37 trillion market, representing sustained growth at a 12.85% CAGR.

The B2B SaaS segment may grow even faster, with projections suggesting $1.58 trillion by 2031 at a 26.24% CAGR. This divergence reflects the increasing enterprise reliance on cloud software and the expanding scope of SaaS into mission-critical business functions.

Technology Trends

AI will continue to be the dominant technology trend, with expectations that by 2027, mainstream deployment of enterprise AI agents will become standard. The distinction between “AI-enhanced” and “AI-native” SaaS will become irrelevant as AI becomes table stakes for all software categories.

Blockchain integration for specific use cases—trade finance, provenance tracking, digital identity—is expected to reach mainstream deployment by 2027, though likely as backend infrastructure rather than user-facing features.

Edge computing will become increasingly important for SaaS applications requiring low latency, particularly in IoT, autonomous systems, and real-time analytics. SaaS architectures will evolve to distribute compute between cloud and edge seamlessly.

Market Structure Predictions

Consolidation is likely to accelerate as larger SaaS companies acquire smaller players to fill product gaps and enter new markets. Vertical SaaS companies, in particular, are becoming acquirers, expanding within industries by buying complementary tools.

The number of SaaS companies is expected to double from current levels, driven by lower barriers to entry and the proliferation of niche opportunities. However, the gap between successful platforms and struggling point solutions will widen.

Operating margins will be a key metric to watch. As the industry matures, the question of whether SaaS returns to prioritizing growth or maintains focus on profitability will determine the strategies of public companies and their private counterparts.

Regional Expansion

While the US will remain the largest single market, growth rates in Asia-Pacific, Latin America, and Africa will outpace mature markets. SaaS companies that can navigate localization challenges—including payment methods, compliance requirements, and cultural differences—will capture significant value.

The rise of regional SaaS champions—companies that dominate specific geographies rather than competing globally—will create both opportunities and challenges for international expansion.

Key Takeaways

- The SaaS market reached $465 billion in 2026 and is projected to nearly double to $887 billion by 2030, making it one of the fastest-growing sectors in the global economy.

- AI integration is no longer optional—75% of SaaS companies will embed AI in core processes by end of 2026, with AI-native companies capturing disproportionate market share.

- Vertical SaaS represents the biggest opportunity—industry-specific solutions command premium pricing, achieve higher retention, and face less competition than horizontal alternatives.

- Churn remains the critical challenge—with average monthly churn of 5-7%, SaaS companies must prioritize retention as much as acquisition to achieve sustainable growth.

- Platform strategies create lasting competitive advantage—companies that build ecosystems rather than just products benefit from network effects that are difficult to replicate.

Sources and Citations

- Precedence Research – Software as a Service (SaaS) Market Size and Share Report 2026-2035

- Statista – Software as a Service Market Forecast Worldwide 2026

- Mordor Intelligence – B2B SaaS Market Size and Share Analysis 2026-2031

- Quantumrun – SaaS Industry Growth Statistics 2026

- DemandSage – SaaS Statistics 2026 (Market Size and Industry Report)

- SaaS Capital – 2026 Benchmarking Metrics for Bootstrapped SaaS Companies

- Eagle Rock CFO – SaaS Business Metrics Benchmarks 2026

- Prospeo – SaaS Revenue Growth 2026 Benchmarks

- TechnologyChecker.io – Salesforce Statistics and Market Share 2026

- Flippa – Top SaaS Companies in the USA 2026 Guide

- SaaS Capital Index – SaaS Valuations and Growth Analysis Q1 2026

- Best SEO Webtech – 7 SaaS Trends in 2026

- Taboola – 8 SaaS Marketing Trends for 2026

- HiringThing – 2026 Vertical SaaS Trends

- Oliver Munro – 60+ SaaS Marketing Statistics and Benchmarks for 2026

The Evolution of SaaS: From Niche to Necessity

The Software as a Service model has undergone a remarkable transformation since its inception. What began as a novel approach to delivering software over the internet has become the default method for enterprise and consumer applications alike. Understanding this evolution provides crucial context for where the industry stands today and where it is headed.

In the early 2000s, SaaS was viewed with skepticism by enterprise IT departments concerned about security, reliability, and data ownership. Salesforce pioneering of the model in CRM was initially dismissed by established players like Siebel Systems. Yet the advantages of cloud delivery—automatic updates, lower upfront costs, and accessibility from anywhere—proved irresistible to businesses of all sizes.

The 2010s saw explosive growth as broadband became ubiquitous and mobile devices created demand for software that worked across platforms. Companies like Dropbox, Slack, and Zoom became household names by solving specific problems with elegant, cloud-native solutions. The COVID-19 pandemic accelerated adoption further, as remote work made cloud-based collaboration tools essential rather than optional.

Today, SaaS has matured into a sophisticated ecosystem. The focus has shifted from convincing businesses to adopt cloud software to helping them manage the complexity of hundreds of SaaS applications. Integration platforms, SaaS management tools, and unified analytics have emerged to address the challenges of SaaS sprawl.

Regional Market Analysis

The SaaS market is not uniform across geographies. Different regions exhibit distinct characteristics in terms of adoption rates, preferred vendors, and growth trajectories.

North America

The United States remains the epicenter of the SaaS industry, with Silicon Valley, Seattle, and New York hosting the headquarters of the world largest cloud software companies. The US market alone represents over $187 billion in annual SaaS revenue, with an average of 305+ SaaS applications deployed per business.

American SaaS companies benefit from deep capital markets, a large domestic customer base, and a culture that embraces early technology adoption. The presence of major cloud infrastructure providers—Amazon Web Services, Microsoft Azure, and Google Cloud Platform—creates a supportive ecosystem for SaaS development.

Europe

Europe represents the second-largest SaaS market, with particular strength in fintech, privacy-focused solutions, and enterprise software. The General Data Protection Regulation (GDPR) has created both challenges and opportunities—compliance requirements favor SaaS solutions that can handle data governance automatically.

European SaaS companies often emphasize data sovereignty and privacy as competitive differentiators. The region has produced notable successes in areas like team collaboration (Spotify, though now public, started with SaaS principles), project management, and financial software.

Asia-Pacific

The Asia-Pacific region is experiencing the fastest SaaS growth rates, albeit from a smaller base. China, India, Japan, and Southeast Asian countries are rapidly adopting cloud software, driven by digital transformation initiatives and the proliferation of mobile-first business models.

Local players often dominate due to language, regulatory, and cultural factors. However, global SaaS companies are increasingly investing in localization to capture this high-growth market. The region unique characteristics—such as super-app ecosystems in Southeast Asia and mobile payment prevalence in China—are driving innovation in SaaS business models.

Industry-Specific SaaS Adoption

SaaS adoption varies significantly across industries, with some sectors embracing cloud software enthusiastically while others lag due to regulatory, security, or cultural factors.

Technology and Professional Services

Unsurprisingly, technology companies are the heaviest adopters of SaaS, often using 400+ applications across their organizations. Professional services firms—consulting, legal, accounting—have also embraced SaaS for project management, time tracking, and client collaboration.

These industries value the flexibility and scalability of SaaS, as their needs fluctuate with project pipelines and client demands. The ability to add or remove licenses quickly aligns costs with revenue, making SaaS economically attractive.

Healthcare

Healthcare has been slower to adopt SaaS due to strict HIPAA compliance requirements and concerns about data security. However, the pandemic accelerated cloud adoption as telehealth became essential. Electronic Health Record (EHR) systems, practice management software, and patient engagement platforms are increasingly delivered via SaaS models.

Vertical SaaS solutions designed specifically for healthcare workflows—such as dental practice management, mental health platforms, and specialty EHRs—are seeing strong growth as they address industry-specific needs that horizontal solutions cannot meet.

Financial Services

Banks, insurance companies, and investment firms have historically been cautious about cloud software due to regulatory scrutiny and security concerns. However, the rise of fintech has forced traditional institutions to modernize, and SaaS solutions for compliance, risk management, and customer engagement are gaining traction.

Embedded fintech—where SaaS platforms incorporate financial services directly—is blurring the lines between software and banking. This trend is particularly strong in vertical SaaS for industries like construction, real estate, and healthcare, where payment processing and lending are natural extensions of workflow software.

Manufacturing and Logistics

Traditional industries like manufacturing and logistics are undergoing digital transformation, with SaaS solutions for supply chain management, inventory optimization, and predictive maintenance gaining adoption. The Industrial Internet of Things (IIoT) is creating demand for SaaS platforms that can process and analyze data from connected equipment.

These industries represent significant growth opportunities for vertical SaaS, as their specific workflows and regulatory requirements are poorly served by horizontal solutions. Companies that understand the nuances of manufacturing or logistics can build highly sticky products with strong competitive moats.

The Economics of SaaS: Unit Economics and Profitability

Understanding the economics of SaaS is essential for founders, investors, and operators. The subscription model creates unique financial dynamics that differ fundamentally from traditional software or services businesses.

The Rule of 40

The Rule of 40—a metric that adds growth rate and profit margin, with the sum ideally exceeding 40%—has become a benchmark for SaaS health. A company growing 50% annually with -10% margins meets the rule, as does a company growing 20% with 20% margins.

This framework acknowledges that SaaS companies face a trade-off between growth and profitability. Early-stage companies typically prioritize growth, investing heavily in sales and marketing to capture market share. As companies mature, the focus shifts toward profitability and operational efficiency.

Customer Lifetime Value and CAC

The ratio of Customer Lifetime Value (LTV) to Customer Acquisition Cost (CAC) is a critical metric for SaaS businesses. Healthy SaaS companies maintain LTV:CAC ratios of 3:1 or higher, meaning the lifetime value of a customer is at least three times the cost to acquire them.

CAC payback period—the time required to recover acquisition costs from a customer margin—is equally important. Best-in-class SaaS companies achieve payback in under 12 months, while 12-15 months is considered excellent. Longer payback periods strain cash flow and increase risk if churn is higher than expected.

Gross Margin Considerations

SaaS gross margins are typically high—70-80% or more—because the cost of delivering software to additional customers is minimal. However, AI-enhanced SaaS is changing this dynamic. The compute costs of running large language models can reduce gross margins significantly if not managed carefully.

Companies must balance the value delivered by AI features against the costs of providing them. Dynamic pricing, efficient model selection, and caching strategies are essential for maintaining healthy margins in the AI era.