Here’s a stat that should wake you up: SaaS companies lose an average of 4.3% of revenue to sales tax liabilities alone. Add chargebacks, compliance headaches, and the operational cost of managing payments across borders, and you’re looking at a significant drain on resources that could be going toward growth.

If you’re building a SaaS business and trying to figure out whether you need a payment gateway or a merchant of record, you’re not alone. Most founders I talk to conflate the two or assume they’re interchangeable. They’re not. The choice you make here will impact everything from your tax obligations to your chargeback liability to how fast you can expand globally.

In this guide, I’ll break down exactly what each model does, where they differ, and how to choose the right approach for your business stage. No fluff, just the practical details you need to make an informed decision.

What Is a Payment Gateway?

A payment gateway is the technology layer that securely captures and transmits payment information between your customer, your business, and the financial institutions processing the transaction. Think of it as the digital equivalent of a card reader at a physical store.

When a customer enters their credit card details on your checkout page, the payment gateway:

- Encrypts the data using tokenization to replace sensitive card information with secure tokens

- Routes the transaction to the appropriate payment processor or acquiring bank

- Handles authorization by communicating with the customer’s issuing bank to verify funds

- Returns the response — approved, declined, or requiring additional verification like 3D Secure

Popular payment gateways include Stripe, PayPal, Braintree, and Adyen. They integrate with your application via APIs and handle the technical complexity of moving money securely.

Here’s the critical part: a payment gateway does NOT assume legal responsibility for the transaction. You remain the merchant of record. That means you’re on the hook for tax compliance, chargeback disputes, fraud liability, and regulatory requirements in every jurisdiction where you sell.

What Is a Merchant of Record?

A Merchant of Record (MoR) is a legal entity that becomes the seller of record for your transactions. When customers buy your product, they’re technically buying from the MoR, not from you. The MoR then pays you the proceeds minus their fees.

This might sound like a subtle distinction, but it’s transformative. By becoming the legal seller, the MoR assumes:

- Tax compliance liability — calculating, collecting, and remitting VAT, GST, and sales tax in every jurisdiction

- Chargeback management — handling disputes, providing evidence, and absorbing losses

- Fraud prevention — implementing detection systems and covering fraudulent transaction costs

- Regulatory compliance — ensuring adherence to PCI DSS, GDPR, and local financial regulations

- Payment method relationships — negotiating rates with banks and processors globally

Companies like Fungies, Paddle, FastSpring, and Lemon Squeezy operate as merchants of record. When you integrate with them, you’re essentially outsourcing the entire financial and legal infrastructure of selling online.

Merchant of Record vs Payment Gateway: The Key Differences

Let’s cut through the confusion with a direct comparison of what each model actually handles:

| Responsibility | Payment Gateway | Merchant of Record |

|---|---|---|

| Payment processing | ✓ Yes | ✓ Yes |

| Data encryption & security | ✓ Yes | ✓ Yes |

| Tax calculation & remittance | ✗ No (you handle this) | ✓ Yes |

| Chargeback management | ✗ No (you handle disputes) | ✓ Yes |

| Fraud liability | ✗ You absorb losses | ✓ MoR absorbs losses |

| PCI compliance | Partial (shared responsibility) | ✓ Full MoR responsibility |

| Global entity requirements | ✗ You need local entities | ✓ Not required |

| Legal seller of record | ✗ You remain seller | ✓ MoR is the seller |

| Pricing model | Transaction fees only | Higher fee, all-inclusive |

The fundamental difference is liability. With a payment gateway, you retain all legal and financial responsibility for transactions. With a merchant of record, you outsource that liability in exchange for higher per-transaction fees.

The Hidden Costs of Payment Gateways

Payment gateways advertise low transaction fees — typically 2.9% + $0.30 per transaction. But that number is misleading. Here’s what you’re not seeing:

Tax Compliance Costs

According to Anrok’s 2025 Global Tax Compliance Report, SaaS companies waste over 30 hours monthly on manual tax compliance work. If you’re selling globally, you need to:

- Track nexus thresholds in every US state (SaaS is taxable in 30+ states)

- Register for VAT in the EU, UK, and other jurisdictions

- Calculate correct tax rates based on customer location

- File returns monthly, quarterly, or annually depending on jurisdiction

- Remit collected taxes to the appropriate authorities

Get this wrong and you’re facing penalties, interest, and in some cases, criminal liability. Most SaaS founders I know underestimate the complexity here until they’re scrambling to clean up a compliance mess.

Chargeback and Fraud Expenses

Global chargeback volume is projected to reach 337 million cases by 2026, up 42% from 2023. Worldwide chargeback losses are expected to climb from $33.79 billion in 2025 to $41.69 billion by 2028.

When you use a payment gateway, you’re responsible for:

- The disputed transaction amount (refunded to the customer)

- Chargeback fees ($15-$100 per dispute)

- Time spent gathering evidence and responding to disputes

- Potential placement on monitoring programs if your chargeback rate exceeds 1%

First-party fraud (friendly fraud) now accounts for roughly 45% of merchant dispute volume. That’s customers disputing legitimate charges — and you’re eating the cost.

Operational Overhead

Beyond direct costs, payment gateways require you to build and maintain:

- Subscription management logic (upgrades, downgrades, prorations)

- Dunning management for failed payments

- Tax calculation integrations

- Multi-currency support

- Compliance monitoring and reporting

Every hour your engineering team spends on billing infrastructure is an hour not spent on your core product.

When to Choose a Payment Gateway

Despite the added responsibilities, payment gateways make sense in specific scenarios:

1. You’re Early Stage with Simple Needs

If you’re pre-revenue or making your first sales, a payment gateway gets you started fast. Stripe can be integrated in a day. You don’t need complex tax compliance yet if you’re only selling domestically or in limited markets.

2. You Have In-House Finance and Legal Teams

Enterprise SaaS companies with dedicated tax, legal, and finance teams can handle compliance internally. If you have the resources to manage global tax obligations and chargeback disputes, the lower transaction fees of a gateway may pencil out.

3. You Need Maximum Customization

Payment gateways offer more control over the checkout experience, custom pricing logic, and integration flexibility. If your billing model is highly unique — say, complex usage-based pricing with custom enterprise contracts — you might need the granular control a gateway provides.

4. You’re Primarily B2B with Invoicing

If your customers are large enterprises paying via invoice and wire transfer rather than credit card, the benefits of a merchant of record diminish. Your transaction volume is lower, and the compliance burden is reduced.

When to Choose a Merchant of Record

Here’s where an MoR becomes the obvious choice:

1. You’re Selling Globally

The moment you start accepting payments from multiple countries, tax complexity explodes. The EU has 27 different VAT regimes. US states each have their own sales tax rules. Canada has GST, HST, and QST depending on the province.

An MoR handles all of this automatically. They calculate the correct tax based on customer location, collect it at checkout, and remit it to the appropriate authorities. You receive net proceeds without touching tax compliance.

2. You Want to Focus on Product, Not Payments

Every hour spent on billing infrastructure is an hour not spent improving your product. An MoR gives you a complete payments stack out of the box: checkout, subscriptions, tax compliance, fraud prevention, and dispute management.

For small teams, this is often the difference between shipping features and drowning in payment operations.

3. You’re Risk-Averse

If the thought of a surprise $50,000 tax bill or a wave of chargebacks keeps you up at night, an MoR provides peace of mind. They absorb the liability. They handle the disputes. They ensure compliance.

4. You Need to Move Fast

Want to start selling in Japan tomorrow? With a payment gateway, you’d need to understand Japanese consumption tax, register with local authorities, and set up local payment methods. With an MoR, you flip a switch and you’re live.

This speed-to-market advantage is why most successful indie makers and micro-SaaS founders choose MoRs.

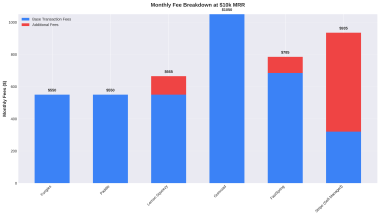

Cost Comparison: The Real Math

Let’s run the numbers for a hypothetical SaaS company doing $50,000 MRR with customers in the US, EU, and UK:

| Cost Category | Payment Gateway | Merchant of Record |

|---|---|---|

| Transaction fees | 2.9% + $0.30 per transaction | 5% + $0.50 per transaction |

| Monthly cost (est.) | ~$1,450 | ~$2,500 |

| Tax compliance software | $300-$500/month | Included |

| Chargeback costs | $500-$2,000/month (variable) | Included |

| Fraud prevention tools | $200-$500/month | Included |

| Engineering time | 20-40 hours/month | 2-5 hours/month |

| Finance/legal time | 30+ hours/month | 5-10 hours/month |

| Total effective cost | $2,450-$4,450+ + labor | ~$2,500 flat |

When you factor in the fully-loaded cost of engineering and finance time, the MoR often comes out cheaper — or at least comparable — while eliminating risk and compliance headaches.

Popular Merchant of Record Providers

If you’re leaning toward an MoR, here are the leading options:

Fungies

Best for: SaaS and digital product creators who want simplicity

Fungies offers a flat 5% + $0.50 per transaction with no monthly fees. It handles global tax compliance, chargebacks, and fraud prevention out of the box. The developer experience is Stripe-like with simple API integration and pre-built checkout components.

Paddle

Best for: Established SaaS companies with higher volumes

Paddle has been around since 2012 and serves thousands of software companies. They offer more advanced features like usage-based billing and deeper analytics. Pricing is custom based on volume.

FastSpring

Best for: Software and digital goods companies

FastSpring focuses on software, SaaS, and video game companies. They offer strong localization features and have been in the MoR space for over a decade.

Lemon Squeezy

Best for: Indie makers and small digital product sellers

Lemon Squeezy gained popularity in the indie maker community for its simple setup and clean UI. They charge 5% + $0.50 per transaction. Note that they were acquired by Stripe in 2024, so their long-term roadmap may evolve.

FAQ: Merchant of Record vs Payment Gateway

Can I switch from a payment gateway to a merchant of record later?

Yes, but it’s not trivial. You’ll need to migrate customer payment methods (if the MoR supports imports), update your checkout integration, and potentially re-collect tax information from customers. Most companies make this switch when they hit $10K-$20K MRR and the compliance burden becomes unsustainable.

Do merchants of record support usage-based billing?

Most modern MoRs support hybrid models combining subscription and usage-based billing. Fungies, Paddle, and FastSpring all offer metered billing capabilities. Check with your provider for specific implementation details.

What happens to my existing customers if I switch to an MoR?

Most MoRs can import existing subscriptions, though the process varies. Customers typically don’t need to take any action — their billing continues seamlessly. You may need to communicate the change for transparency, but from the customer’s perspective, nothing changes.

Is an MoR more expensive than a payment gateway?

Per-transaction fees are higher, but total cost of ownership is often lower when you factor in tax compliance software, fraud tools, chargeback costs, and engineering time. Run the math for your specific situation.

Can I use both a payment gateway and an MoR?

Generally no — you choose one model per transaction. Some companies use an MoR for self-serve customers and a gateway for enterprise deals invoiced separately, but this adds complexity.

Conclusion: Making the Right Choice

The payment gateway vs merchant of record decision comes down to three factors: your growth stage, your risk tolerance, and how much you value focus.

If you’re just starting out, selling only domestically, and have more time than money, a payment gateway like Stripe is a fine choice. You’ll learn a lot about payments infrastructure, and your transaction costs will be lower.

But if you’re selling globally, want to eliminate compliance risk, or would rather focus your team on product development than billing operations, a merchant of record is the smarter long-term play. The higher per-transaction fee is insurance against tax penalties, chargeback losses, and operational headaches.

Personally? I’ve seen too many SaaS founders get blindsided by tax audits or drown in chargeback disputes. For most software companies, the MoR model pays for itself many times over.

If you’re ready to simplify your payments and go global without the compliance headache, get started with Fungies. One integration, global tax compliance handled, and you can focus on what actually matters: building a great product.

Sources

- Anrok End-of-Year Sales Tax and VAT Report 2025

- Chargeflow Chargeback Statistics 2025

- Sift Q4 2025 Digital Trust Index

- Merchant Risk Council 2025 Global eCommerce Payments and Fraud Report

- Stripe: What Is a Merchant of Record?

- FastSpring: What Is a Merchant of Record?

- Paddle: What is a merchant of record?