The artificial intelligence market has reached a staggering $538 billion in 2026, representing a 37.3% year-over-year growth rate that shows no signs of slowing down. What started as experimental technology in research labs has now become the driving force behind the most significant technological transformation since the internet itself. From healthcare diagnostics to autonomous vehicles, from creative content generation to enterprise automation, AI has permeated every industry vertical and reshaped how businesses operate at a fundamental level.

This comprehensive analysis draws from the latest data from Gartner, McKinsey, Deloitte, IBM, and leading industry research firms to provide you with the most accurate picture of the AI landscape in 2026. Whether you are an investor evaluating opportunities, a business leader planning your AI strategy, or a professional seeking to understand where the industry is heading, this report delivers the data-driven insights you need.

Market Overview: The $538 Billion AI Ecosystem

The global artificial intelligence market has experienced explosive growth over the past decade, evolving from a niche technology sector into a half-trillion-dollar industry that touches virtually every aspect of modern business and daily life. Understanding the current market size, historical trajectory, and future projections is essential for anyone looking to navigate this rapidly evolving landscape.

Current Market Size and Growth Metrics

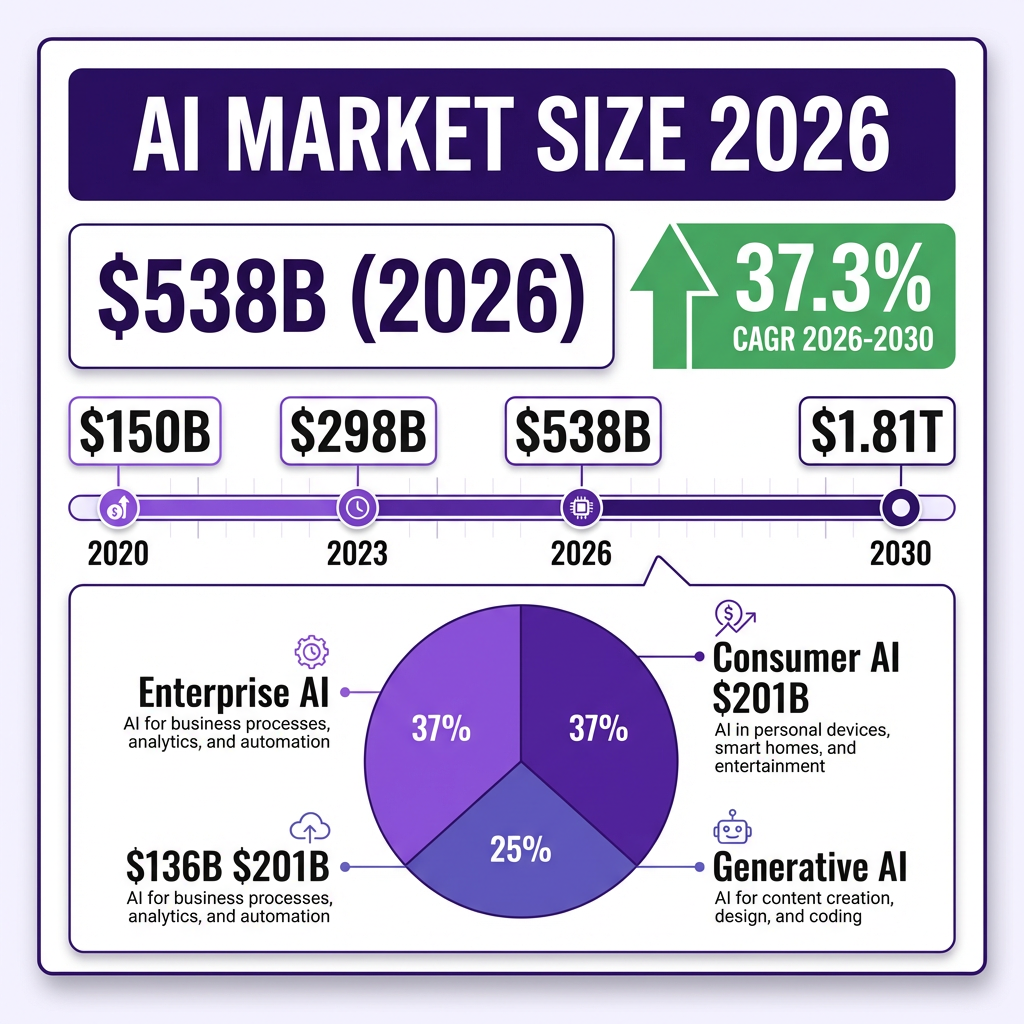

As of 2026, the global AI market stands at $538 billion, according to comprehensive industry analysis. This represents a remarkable 37.3% year-over-year growth rate that significantly outpaces most other technology sectors. The market’s expansion has been fueled by several converging factors: the mainstream adoption of generative AI tools, increased enterprise investment in AI infrastructure, and the proliferation of AI-powered applications across consumer and business markets.

The generative AI segment alone has reached $136 billion in 2026, demonstrating how quickly this subsector has matured since the launch of ChatGPT in late 2022. What began as a novelty has become a core business tool, with companies across industries deploying generative AI for content creation, code generation, customer service automation, and data analysis.

Gartner’s research provides an even broader perspective, projecting that worldwide AI spending will total $2.5 trillion in 2026 when including all related hardware, software, and services. This figure encompasses not just AI applications themselves but the massive infrastructure investments required to support them—including specialized chips, data centers, cloud computing resources, and professional services.

Historical Growth Trajectory

The AI market’s growth story is one of accelerating adoption curves. In 2020, the global AI market was valued at approximately $150 billion. By 2023, it had more than doubled to $298 billion. The period from 2023 to 2026 has seen the most dramatic expansion, with the market nearly doubling again to reach the current $538 billion valuation.

This growth pattern reflects the transition from AI as an experimental technology to AI as a business imperative. Early adopters in tech-forward industries like finance and e-commerce demonstrated the technology’s value, creating case studies that convinced more conservative sectors to invest. The launch of consumer-facing generative AI tools in 2022-2023 created a watershed moment, familiarizing millions of users with AI capabilities and driving demand for enterprise-grade solutions.

Future Projections: The Path to $1.81 Trillion

Industry analysts project that the AI market will reach $1.81 trillion by 2030, representing a compound annual growth rate (CAGR) of approximately 37.3% from 2026. This projection assumes continued investment in AI infrastructure, ongoing improvements in model capabilities, and the development of new use cases across industries.

Several factors support this optimistic outlook. First, enterprise AI adoption is still in relatively early stages, with significant room for growth as organizations move from pilot projects to production deployments. Second, emerging technologies like autonomous vehicles, robotics, and advanced healthcare diagnostics are expected to create entirely new market segments. Third, the development of more efficient AI models and specialized hardware is making AI accessible to smaller organizations that previously could not afford the infrastructure.

The United States market is projected to reach approximately $851.46 billion by 2034, maintaining its position as the largest single-country AI market. However, growth rates in Asia-Pacific regions, particularly China and India, are expected to outpace North America as these markets mature and local AI ecosystems develop.

Key Statistics and Data Points

Beyond the headline market size figures, a wealth of data points reveals how deeply AI has penetrated global business operations and consumer behavior. These statistics paint a picture of an industry in rapid transition, with significant variation in adoption rates, implementation success, and return on investment across different sectors and organization sizes.

Enterprise Adoption Statistics

Enterprise adoption of AI has reached unprecedented levels in 2026. According to the latest research, 72% of enterprises now report at least one AI deployment in production environments. This marks a significant increase from previous years and indicates that AI has moved beyond the experimental phase for most large organizations.

More impressively, 58% of companies are actively using AI in production workflows, not just pilot projects. This distinction is crucial—it indicates that these organizations have moved past testing and are deriving real operational value from their AI investments. The gap between the 72% with any deployment and the 58% in production suggests that roughly 20% of enterprises are still in the pilot or evaluation phase.

Global organizational adoption has skyrocketed to 78%, representing a staggering 41.8% relative increase since 2023 according to data from McKinsey and Stanford HAI. This growth rate is among the fastest ever recorded for a major enterprise technology, surpassing even the adoption curves of cloud computing and mobile technologies.

Generative AI adoption has been particularly rapid. According to McKinsey’s 2026 research, 65% of organizations are already using generative AI in at least one business function. This represents a remarkable acceleration from 2023, when generative AI was still considered emerging technology by most enterprises.

Investment and Spending Data

Global spending on AI systems is forecast to surpass $300 billion in 2026, up from $223 billion in 2025, according to Gartner. This spending encompasses software, hardware, and services, with the software segment growing fastest as more organizations adopt SaaS-based AI solutions.

Venture capital investment in AI has reached historic levels. In Q1 2026 alone, AI startups raised record-breaking funding as the AI boom pushed global venture funding to new heights. The top 5 VC firms captured 73% of total AI deal value in Q1 2026, indicating market concentration around the most promising companies. PitchBook data shows that more than 80% of global private investment in AI flowed to US AI firms over the prior year.

Big Tech’s AI spending has become a major economic force. Meta, Microsoft, Alphabet, and Amazon have collectively committed approximately $650 billion to AI infrastructure and development. Microsoft alone is running a $145 billion annual run-rate on AI-related investments, driven by its Azure cloud platform and OpenAI partnership. Meta projects $115-135 billion in AI spending, focusing on its Llama models and AI-powered advertising infrastructure.

ROI and Value Creation Metrics

Despite widespread adoption, AI ROI remains a challenge for many organizations. According to PwC’s 2026 CEO Survey, 56% of CEOs report neither increased revenue nor decreased costs from their AI investments in the last 12 months. This finding highlights the implementation gap between adopting AI technology and successfully integrating it into business processes to create measurable value.

However, the 44% of organizations that are seeing returns are achieving significant results. Research from Unframe AI’s 2026 benchmarks, based on surveys of 255 enterprise leaders, reveals that successful AI implementations deliver measurable gains in productivity, cost reduction, and revenue growth. The key differentiator appears to be not just adoption but the depth of integration—organizations that embed AI deeply into workflows see better results than those using it for isolated tasks.

Only 25% of AI initiatives deliver expected returns, making budget approval and continued investment difficult for many organizations. This statistic underscores the importance of strategic planning and realistic goal-setting when implementing AI solutions.

User and Consumer Statistics

The global daily active user base for generative AI technology ranges between 115 million and 180 million as of early 2026, according to Master of Code Global research. This represents substantial growth from 2023-2024 figures and indicates mainstream consumer adoption of AI tools.

Enterprise AI usage patterns show that 52% of employees are already using AI agents in their daily work, according to WRITER’s 2026 Enterprise AI Adoption Survey. This finding suggests that AI is becoming as commonplace in the workplace as email or spreadsheets were in previous decades.

Customer service has emerged as a leading use case, with a significant percentage of enterprises using AI for customer service and support automation. Klarna’s widely-cited AI implementation, powered by OpenAI GPT integration, has become a benchmark for what is possible when AI is deployed at scale in customer-facing applications.

Major Trends Shaping AI in 2026

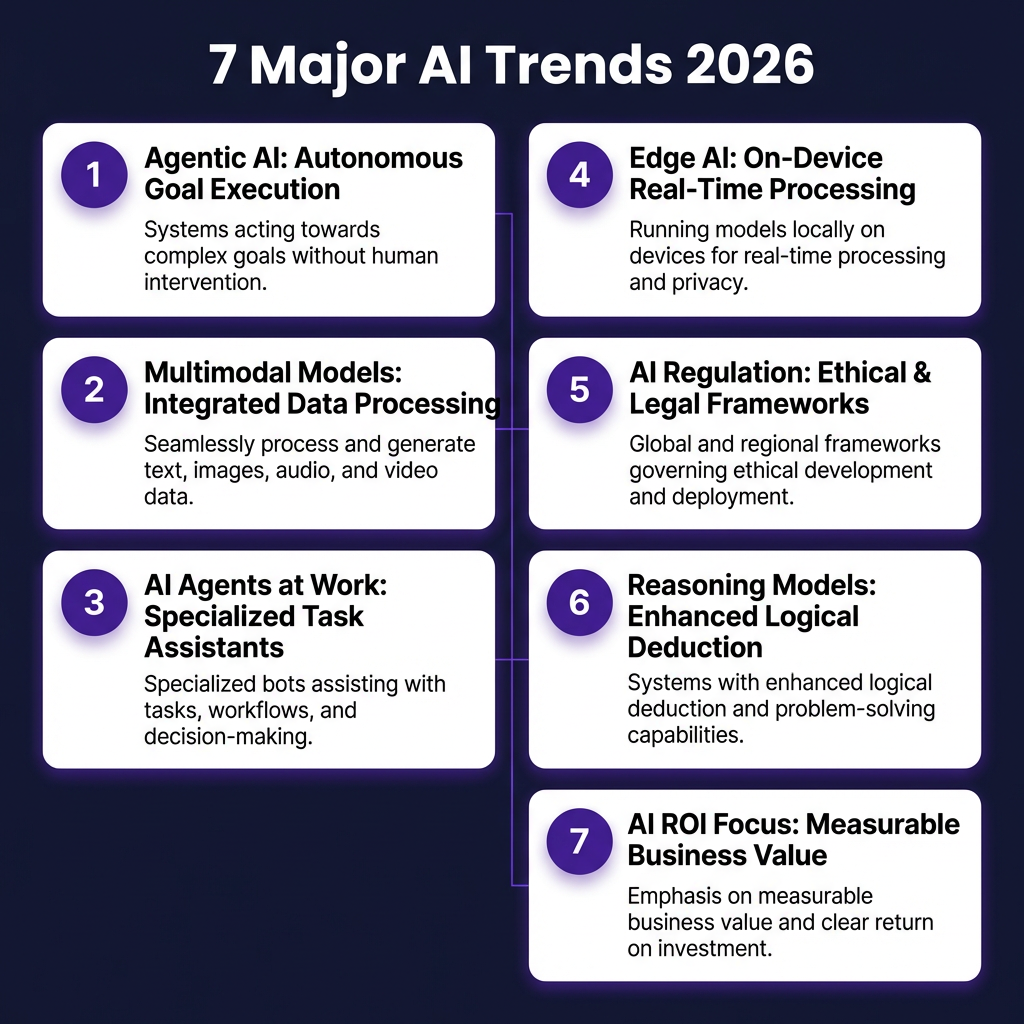

The AI landscape in 2026 is defined by seven major trends that are reshaping how organizations develop, deploy, and benefit from artificial intelligence. Understanding these trends is essential for anyone looking to build or invest in AI capabilities.

1. Agentic AI: From Tools to Autonomous Agents

The most significant trend emerging in 2026 is the shift from AI experimentation to AI industrialization, specifically through agentic AI systems. Unlike traditional AI tools that respond to individual prompts, agentic AI can autonomously plan, execute multi-step tasks, and make decisions with minimal human oversight.

According to IBM’s 2026 AI trends analysis, reasoning models from frontier labs like DeepSeek-R1 have taken the world by storm, demonstrating capabilities that seemed impossible just a year ago. These models can handle complex reasoning tasks, break down problems into steps, and maintain context across extended interactions.

Nearly all executives (97%) report that their companies deployed AI agents in the past year, according to WRITER’s research. This widespread adoption indicates that agentic AI is moving from experimental technology to standard business infrastructure. The implications are profound—business processes that previously required human coordination can now be handled by AI systems working autonomously.

2. Multimodal AI Models

AI systems are increasingly capable of processing and generating multiple types of content—text, images, audio, and video—within a single model. This multimodal capability is opening new use cases that were not possible with single-modal systems.

Microsoft’s 2026 AI trends report highlights how multimodal AI is enabling more natural human-computer interaction. Users can now upload a photo and ask questions about it, dictate voice commands that the AI understands in context, or request video content generated from text descriptions. This flexibility is making AI accessible to users who may not be comfortable with text-only interfaces.

The business applications of multimodal AI are extensive. Retailers can use it for visual search and product recommendations. Healthcare providers can analyze medical imaging alongside patient records. Content creators can generate multimedia assets from simple text prompts. As these models improve, the distinction between different types of AI tools is blurring.

3. AI Agents in the Workplace

Beyond general agentic AI, 2026 has seen the emergence of specialized AI agents designed for specific workplace functions. These agents can handle tasks ranging from scheduling meetings and drafting emails to analyzing financial reports and managing customer relationships.

Deloitte’s State of AI in the Enterprise report emphasizes how AI agents are becoming embedded in core business workflows. Rather than replacing human workers, these agents are augmenting capabilities—handling routine tasks while humans focus on strategic decision-making and creative work.

The productivity implications are significant. Organizations report that AI agents can handle 60-80% of routine administrative tasks, freeing up employee time for higher-value activities. However, successful implementation requires careful attention to change management and employee training.

4. Edge AI and Distributed Computing

As AI models become more efficient, there is growing interest in running AI workloads on edge devices rather than in centralized data centers. Edge AI enables real-time processing without latency, reduces bandwidth costs, and addresses privacy concerns by keeping data local.

The MIT Sloan Management Review has documented practical AI implementation success stories that leverage edge computing for applications like manufacturing quality control, autonomous vehicles, and healthcare monitoring. These use cases require split-second decision-making that cloud-based AI cannot provide.

Hardware advances are making edge AI increasingly feasible. Specialized chips designed for AI inference are becoming smaller, cheaper, and more energy-efficient. This trend is democratizing AI by enabling capabilities on devices that do not have cloud connectivity or cannot afford the latency of round-trip API calls.

5. AI Regulation and Governance

As AI capabilities advance, regulatory frameworks are evolving to address concerns about safety, privacy, bias, and accountability. The European Union’s AI Act has set a global precedent, classifying AI systems by risk level and imposing requirements on high-risk applications.

Forbes reports on overcoming barriers to AI adoption in 2026, noting that governance and compliance have become top priorities for enterprise AI deployments. Organizations are investing in AI governance frameworks, bias detection tools, and audit trails to ensure their AI systems meet regulatory requirements and ethical standards.

The regulatory landscape is still evolving, with different jurisdictions taking different approaches. This creates complexity for global organizations that must navigate multiple regulatory regimes. However, the trend is clear: AI is moving from an unregulated frontier to a governed technology sector with established rules and accountability mechanisms.

6. Reasoning and Chain-of-Thought Models

A year ago, AI models struggled with tasks like counting the number of “r”s in “strawberry.” Today, reasoning models from Chinese frontier labs and Western developers have demonstrated remarkable improvements in logical reasoning, mathematical problem-solving, and step-by-step analysis.

IBM’s analysis highlights how open-source reasoning agents have taken the world by storm, making advanced reasoning capabilities accessible to developers worldwide. These models can break down complex problems, consider multiple approaches, and explain their reasoning processes—capabilities that are essential for high-stakes applications in fields like medicine, law, and engineering.

The development of reasoning models represents a qualitative shift in AI capabilities. Rather than simply pattern matching, these systems can engage in forms of structured thinking that more closely resemble human cognition. This opens possibilities for AI applications that require genuine understanding rather than statistical approximation.

7. Focus on AI ROI and Business Value

After years of AI hype and experimentation, 2026 has brought a renewed focus on measurable business value. Organizations are no longer satisfied with AI pilots that demonstrate technical feasibility—they want proof of financial returns.

This trend is driven by the sobering statistic that 56% of CEOs report no revenue increase or cost reduction from AI investments. Boards and investors are demanding accountability for AI spending, which has reached hundreds of billions of dollars globally. The organizations that succeed are those that can connect AI initiatives to specific business outcomes.

Best practices are emerging for AI ROI measurement. Leading organizations are establishing clear metrics before deployment, tracking usage and outcomes rigorously, and being willing to shut down projects that do not deliver value. This disciplined approach is separating successful AI implementations from expensive experiments.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a mix of established technology giants, well-funded startups, and emerging players from around the world. Understanding the competitive landscape is essential for identifying partnership opportunities, competitive threats, and investment prospects.

The Big Tech Dominance

Microsoft, Alphabet (Google), Amazon, and Meta remain the dominant forces in AI, collectively controlling the majority of cloud AI infrastructure, foundational model development, and consumer AI applications. Their combined AI spending of approximately $650 billion in 2026 dwarfs the investment capacity of smaller competitors.

Microsoft’s strategic partnership with OpenAI has given it a leading position in generative AI through the integration of GPT models into Microsoft 365, Azure, and Bing. The company’s Copilot products have become the standard for AI-assisted productivity, with millions of enterprise users. Microsoft’s $145 billion AI run-rate reflects both infrastructure investment and the revenue potential of AI-integrated software.

Alphabet has leveraged its deep research capabilities and vast data resources to develop competitive AI models, including the Gemini family of large language models. Google’s integration of AI into Search, Ads, and Cloud services represents a massive deployment of AI at scale. The Motley Fool reports that Alphabet is quietly winning the AI race in certain segments, particularly in AI-powered advertising and cloud services.

Amazon’s AI strategy centers on AWS, where it provides the infrastructure that powers a significant portion of the world’s AI workloads. Amazon Bedrock has become a popular platform for building generative AI applications, offering access to multiple foundation models through a single API. The company’s investment in AI chips through its Trainium and Inferentia processors represents a strategic move to reduce dependence on NVIDIA.

Meta has taken a different approach, focusing on open-source AI through its Llama models. By making powerful AI models freely available, Meta has built a large developer ecosystem while avoiding the infrastructure costs of running consumer AI services. The company’s AI investments focus on content recommendation, advertising optimization, and its metaverse ambitions.

NVIDIA: The Infrastructure King

No discussion of the AI competitive landscape is complete without NVIDIA. The company’s GPUs have become the standard for AI training and inference, giving NVIDIA a position of enormous influence in the AI ecosystem. As AI models grow larger and more complex, demand for NVIDIA’s specialized chips continues to outstrip supply.

NVIDIA’s competitive moat extends beyond hardware to software. The CUDA platform and related tools have created significant switching costs for AI developers. Competitors like AMD and Intel are investing heavily in AI chips, but NVIDIA’s ecosystem advantage remains substantial.

OpenAI and the Foundation Model Startups

OpenAI, despite its close relationship with Microsoft, operates as a distinct entity and remains the most prominent pure-play AI company. ChatGPT’s rapid adoption made OpenAI a household name and demonstrated the consumer market potential of generative AI. The company’s GPT models continue to set benchmarks for language AI capabilities.

Anthropic has emerged as a significant competitor to OpenAI, positioning itself as the safety-focused alternative. The company’s Claude models have gained traction in enterprise applications where reliability and reduced hallucination rates are priorities. Anthropic’s constitutional AI approach to safety has resonated with organizations concerned about AI risks.

Other notable players in the foundation model space include Cohere, AI21 Labs, and Stability AI, each with different specializations and target markets. The foundation model layer of the AI stack remains highly competitive, with new entrants regularly announcing models that challenge established leaders on various benchmarks.

Enterprise AI Vendors

Beyond the foundation model providers, a robust ecosystem of enterprise AI vendors has developed. Companies like Salesforce (Einstein), ServiceNow, Workday, and SAP have integrated AI capabilities into their core products, making AI accessible to enterprises without requiring custom development.

Specialized AI vendors have also carved out significant market positions. Palantir’s AI platforms for government and defense, DataRobot’s automated machine learning tools, and UiPath’s robotic process automation with AI capabilities serve specific enterprise needs. These vendors often compete by offering industry-specific solutions that generic AI platforms cannot match.

The Forbes AI 50 list for 2026 highlights the most promising AI companies across categories, providing a snapshot of the competitive landscape. The list includes both established players and emerging startups, reflecting the dynamic nature of the AI market.

Challenges and Pain Points

Despite the impressive growth and adoption statistics, the AI industry faces significant challenges that are slowing progress and limiting value creation for many organizations. Understanding these pain points is crucial for developing realistic AI strategies and avoiding common pitfalls.

1. The ROI Gap: Adoption Without Returns

The most significant challenge facing enterprise AI is the gap between adoption and financial returns. While 72% of enterprises have deployed AI, only 25% of AI initiatives deliver expected returns. This disconnect creates a dangerous dynamic where organizations continue investing in AI based on competitive pressure and fear of missing out, without clear evidence of value creation.

Several factors contribute to the ROI gap. Many organizations approach AI as a technology project rather than a business transformation initiative. They invest in building capabilities without clearly defining the business problems they aim to solve. Pilot projects succeed technically but fail to scale because they do not integrate with existing workflows or deliver sufficient value to justify ongoing costs.

Data quality issues undermine many AI initiatives. Nearly 50% of organizations cite data accuracy concerns as a top barrier to AI adoption. AI systems are only as good as the data they are trained on, and many enterprises struggle with fragmented, inconsistent, or biased data sets. Cleaning and preparing data for AI can consume 60-80% of project timelines and budgets.

2. Skills Shortage and Talent Gaps

The demand for AI talent far exceeds supply, creating a significant bottleneck for AI adoption. Most teams lack the technical expertise to implement and maintain AI systems effectively. This skills gap exists at multiple levels—from data scientists and ML engineers who build models, to IT professionals who deploy and manage AI infrastructure, to business users who need to work effectively with AI tools.

Forbes reports on overcoming barriers to AI adoption, emphasizing that building and acquiring the right skills is essential for AI success. Organizations are addressing this challenge through a combination of hiring, training, and partnerships. Some are building internal AI academies to upskill existing employees. Others are relying on managed AI services that reduce the need for in-house expertise.

The talent shortage is particularly acute for specialized roles like AI ethics specialists, MLOps engineers, and AI product managers. As AI becomes more regulated, demand for professionals who understand both the technical and compliance aspects of AI is growing rapidly.

3. Integration with Legacy Systems

Legacy system integration remains a major obstacle for enterprise AI adoption. Many organizations operate on technology infrastructure that was designed decades ago and cannot easily accommodate modern AI workloads. These systems were not designed to exchange data with AI models in real-time, creating integration challenges that can derail AI projects.

According to Kanerika’s research on AI adoption challenges, outdated infrastructure is a primary reason why AI projects stall. Organizations face a difficult choice: invest heavily in modernizing legacy systems to support AI, or work around limitations that constrain AI capabilities. Neither option is attractive from a cost or risk perspective.

The integration challenge extends beyond technical compatibility to organizational processes. AI systems often require changes to established workflows, decision-making hierarchies, and performance metrics. Resistance to these changes can be as significant a barrier as technical limitations.

4. Governance, Risk, and Compliance

As AI systems take on more critical functions, governance and risk management become increasingly important. Organizations must address concerns about AI bias, transparency, accountability, and data privacy. The regulatory environment is evolving rapidly, with new requirements emerging in jurisdictions around the world.

WRITER’s 2026 survey found that 79% of organizations face challenges in adopting AI—a double-digit increase from 2025. Many of these challenges relate to governance and compliance. Organizations struggle to establish appropriate oversight for AI systems, ensure fairness in AI-driven decisions, and maintain audit trails for regulatory compliance.

AI systems handling sensitive data create privacy risks that many organizations are not prepared to manage. Data breaches involving AI systems can have severe consequences, both financially and reputationally. The complexity of AI systems makes it difficult to predict and prevent all potential failure modes.

Opportunities and Growth Strategies

Despite the challenges, the AI market presents enormous opportunities for organizations that can navigate the complexity and execute effectively. Several growth strategies have emerged as particularly effective for capturing value from AI investments.

1. Industry-Specific AI Solutions

While general-purpose AI platforms receive the most attention, significant opportunities exist in developing AI solutions tailored to specific industries. Healthcare AI, financial services AI, manufacturing AI, and retail AI each have unique requirements, regulatory constraints, and value creation opportunities that generic solutions cannot address.

Organizations are finding success by focusing on high-value use cases within their industries. In healthcare, AI applications in medical imaging, drug discovery, and personalized medicine are showing strong returns. In finance, AI for fraud detection, algorithmic trading, and risk assessment has become standard. Manufacturing companies are using AI for predictive maintenance, quality control, and supply chain optimization.

The key to success with industry-specific AI is deep domain expertise combined with technical capabilities. Organizations that understand the nuances of their industries can identify opportunities that generalist AI vendors miss. They can also navigate regulatory requirements and build solutions that integrate seamlessly with industry-standard workflows.

2. AI-as-a-Service and Managed AI

For organizations that lack the resources or expertise to build AI capabilities in-house, AI-as-a-Service (AIaaS) offers an attractive alternative. Cloud providers and specialized vendors offer pre-built AI models, development platforms, and managed services that reduce the barriers to AI adoption.

The AIaaS model allows organizations to access cutting-edge AI capabilities without massive upfront investments in infrastructure and talent. Companies can start with small pilots, demonstrate value, and scale gradually. This approach reduces risk and accelerates time-to-value compared to building AI capabilities from scratch.

Managed AI services go a step further, providing not just technology but also the expertise to implement and operate AI solutions. For many mid-market organizations, this model offers the best path to AI value creation, combining vendor expertise with internal domain knowledge.

3. AI-Powered Product Innovation

Beyond operational efficiency, AI presents opportunities for fundamental product innovation. Companies are using AI to create entirely new product categories and enhance existing offerings with intelligent features that were previously impossible.

Consumer applications range from AI-powered personal assistants that can handle complex tasks to creative tools that help users generate content, music, and art. Enterprise products increasingly include AI capabilities as standard features—predictive analytics in CRM systems, intelligent automation in ERP platforms, and AI-assisted development tools.

The most successful product innovations combine AI with deep understanding of user needs. Companies that treat AI as a feature rather than a product tend to struggle. Those that use AI to solve real problems in ways that delight users are capturing significant market share.

Case Studies and Success Stories

Real-world implementations provide the most valuable insights into what works in AI adoption. The following case studies illustrate successful AI deployments across different industries, highlighting the strategies, challenges, and results that other organizations can learn from.

Case Study 1: Klarna’s AI-Powered Customer Service

Klarna, the global fintech company serving 150 million customers, has become a benchmark for AI implementation in customer service. The company deployed an AI-powered customer service chatbot built on OpenAI GPT integration, fundamentally transforming how it handles customer interactions.

The results have been remarkable. Klarna’s AI assistant now handles the equivalent workload of 700 full-time customer service agents, resolving customer inquiries in multiple languages around the clock. The system has maintained high customer satisfaction scores while dramatically reducing response times and operational costs.

The key lesson from Klarna’s implementation is the importance of starting with volume patterns rather than edge cases. By focusing on the most common customer inquiries first, Klarna was able to achieve immediate impact while gradually expanding the AI’s capabilities to handle more complex scenarios. This approach allowed the company to demonstrate ROI quickly while building organizational confidence in AI capabilities.

Case Study 2: Microsoft’s Copilot Integration

Microsoft’s integration of AI through its Copilot products represents one of the largest-scale AI deployments in history. By embedding AI capabilities across Microsoft 365, Azure, and Windows, Microsoft has made AI accessible to hundreds of millions of users.

The company’s strategic partnership with OpenAI has given it access to cutting-edge language models, which it has integrated into products ranging from Word and Excel to Teams and Outlook. The Copilot products have become the standard for AI-assisted productivity, with enterprise adoption growing rapidly.

Microsoft’s approach demonstrates the value of integrating AI into existing workflows rather than requiring users to adopt new tools. By meeting users where they already work, Microsoft has achieved adoption rates that standalone AI applications struggle to match. The company’s $145 billion AI run-rate reflects both the investment required and the revenue potential of deeply integrated AI.

Case Study 3: Healthcare AI Diagnostics

Healthcare has emerged as one of the most promising domains for AI application, with diagnostic imaging leading the way. Multiple healthcare systems have deployed AI tools that can analyze medical images with accuracy matching or exceeding human radiologists for specific conditions.

These implementations have demonstrated significant improvements in diagnostic speed and accuracy. AI systems can flag potential issues for human review, prioritize urgent cases, and identify patterns that might be missed in routine analysis. The result is faster diagnosis, earlier intervention, and better patient outcomes.

The healthcare case studies highlight the importance of human-AI collaboration. The most successful implementations position AI as a tool that augments human expertise rather than replacing it. Radiologists using AI tools report higher confidence in their diagnoses and the ability to focus on complex cases that require human judgment.

Future Outlook and Predictions

Looking beyond 2026, the AI industry is poised for continued rapid evolution. Several key developments are expected to shape the market through 2030 and beyond, creating new opportunities and challenges for organizations across industries.

The Path to Artificial General Intelligence

The most significant long-term question facing the AI industry is the timeline for Artificial General Intelligence (AGI)—AI systems that can match or exceed human capabilities across a wide range of tasks. While opinions vary widely, the consensus among researchers has shifted toward earlier timelines than previously expected.

Some experts predict that AI systems will become smarter than humans in specific domains by 2027, with broader human-level capabilities following in the 2028-2030 timeframe. The AI-2027 forecast from superforecasters who have accurately predicted AI development over the past five years suggests significant capability improvements in the near term.

The implications of AGI would be profound, potentially transforming every aspect of society and the economy. Organizations should monitor developments in this area while recognizing that predictions about AGI timelines have historically been unreliable.

Market Growth Trajectory

The AI market is projected to grow from $538 billion in 2026 to $1.81 trillion by 2030, representing a CAGR of approximately 37.3%. This growth will be driven by continued enterprise adoption, the development of new use cases, and the expansion of AI capabilities into previously untouched domains.

Several factors could accelerate or decelerate this growth. On the upside, breakthroughs in AI capabilities could unlock new markets and use cases. Regulatory clarity could reduce uncertainty and accelerate enterprise adoption. On the downside, economic downturns could reduce technology spending, and regulatory restrictions could limit certain applications.

The generative AI segment is expected to grow particularly rapidly, with some projections suggesting it could reach $109.37 billion by 2030, up from $16.87 billion in 2024. This represents a CAGR of approximately 37.9%, reflecting the transformative potential of generative AI across industries.

Technology Developments to Watch

Several technology developments are expected to shape the AI landscape through 2030. Multimodal AI models that can process and generate text, images, audio, and video will become increasingly sophisticated, enabling new applications that combine multiple modalities.

AI hardware will continue to evolve, with specialized chips for AI inference and training becoming more efficient and affordable. This will democratize access to AI capabilities, enabling smaller organizations to deploy sophisticated AI systems without massive infrastructure investments.

Edge AI will mature, enabling AI processing on devices without cloud connectivity. This will be particularly important for applications requiring low latency, such as autonomous vehicles, industrial automation, and real-time healthcare monitoring.

Regulatory and Societal Implications

The regulatory environment for AI will continue to evolve, with significant implications for how AI systems are developed and deployed. The EU AI Act has set a precedent that other jurisdictions are likely to follow, creating a framework for risk-based regulation of AI applications.

Societal attitudes toward AI will also shape the market’s development. Public concerns about AI safety, job displacement, and privacy will influence regulatory approaches and consumer adoption. Organizations that proactively address these concerns will be better positioned for long-term success.

The workforce implications of AI will become increasingly significant. While AI is expected to create new job categories, it will also displace certain types of work. Organizations and policymakers will need to manage this transition, investing in education and training to prepare workers for an AI-augmented economy.

Key Takeaways

- The global AI market has reached $538 billion in 2026, growing at 37.3% year-over-year, with projections of $1.81 trillion by 2030.

- Enterprise adoption is widespread but shallow—72% of enterprises have deployed AI, but only 25% of initiatives deliver expected returns.

- Seven major trends are shaping the industry: agentic AI, multimodal models, workplace AI agents, edge AI, regulation, reasoning models, and ROI focus.

- Big Tech dominates with $650 billion in combined AI spending, but startups and specialized vendors are carving out significant niches.

- The gap between AI adoption and ROI represents both the industry’s biggest challenge and its greatest opportunity for improvement.

Sources and Citations

- Gartner – “Worldwide AI Spending Will Total $2.5 Trillion in 2026” – https://www.gartner.com/en/newsroom/press-releases/2026-1-15-gartner-says-worldwide-ai-spending-will-total-2-point-5-trillion-dollars-in-2026

- Noizz.io – “AI Market Size 2026: $538B Global + 37.3% YoY Growth” – https://noizz.io/statistics/ai-market-size-2026

- IBM – “The trends that will shape AI and tech in 2026” – https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- Microsoft – “What is next in AI: 7 trends to watch in 2026” – https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026/

- McKinsey – “The State of AI” – https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

- PwC – “2026 CEO Survey: AI ROI and Business Impact” – https://www.pwc.com/us/en/tech-effect/ai-analytics/ai-predictions.html

- Deloitte – “State of AI in the Enterprise 2026” – https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- Stanford HAI – “2025 AI Index Report” – https://hai.stanford.edu/ai-index/2025-ai-index-report

- Forbes – “Forbes AI 50 List 2026” – https://www.forbes.com/lists/ai50/

- Crunchbase News – “Q1 2026 Shatters Venture Funding Records” – https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026/

- MIT Sloan Management Review – “Practical AI Implementation Success Stories” – https://mitsloan.mit.edu/ideas-made-to-matter/practical-ai-implementation-success-stories-mit-sloan-management-review

- Campaign US – “Big Tech’s AI Spend in 2026” – https://www.campaignlive.com/article/big-techs-ai-spend-2026-following-money/1949168