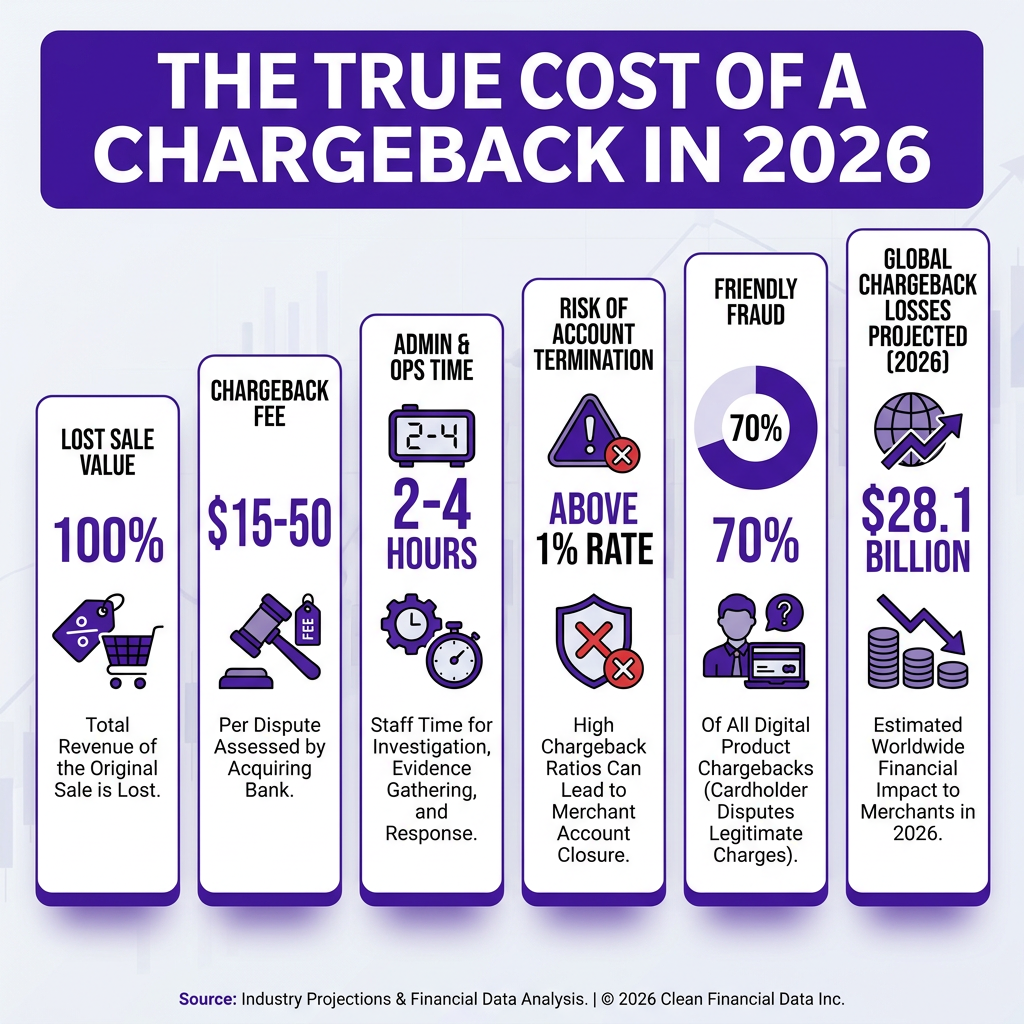

Here’s a number that should get your attention: by 2026, chargeback fraud is expected to cost merchants $28.1 billion — a 40% jump from $20 billion in 2023. And digital products? Chargeback rates for SaaS and digital goods rose 59% from 2023 to 2024, hitting 0.54% on average.

If you’re selling a SaaS product or digital goods and you’re not thinking about chargebacks, you’re flying blind. Blow past the 1% threshold and your payment processor will terminate your merchant account. No warning, no second chances.

This guide breaks down what chargebacks actually cost you, how to prevent them, how to win the ones you can’t prevent, and why a Merchant of Record changes everything about this equation.

What Is a Chargeback and Why Are Digital Products Extra Exposed?

A chargeback is when a customer disputes a transaction with their bank instead of asking you for a refund. The bank reverses the charge, takes the funds from your account, slaps you with a fee, and logs a strike against your dispute rate.

Digital products get hit harder than physical goods for a few reasons:

- No physical proof of delivery. You can’t show a FedEx tracking number. Proving a customer downloaded your software or accessed your SaaS is trickier.

- Forgotten subscriptions. Someone signs up for a free trial, forgets, gets charged three months later, doesn’t recognize the billing descriptor, and files a dispute.

- Friendly fraud is rampant. Roughly 70% of digital product chargebacks are friendly fraud — customers who received and used the product but dispute the charge anyway. Social media is literally full of tutorials on how to do it.

- Instant delivery = instant regret. There’s no cooling-off period in digital delivery. Buy, download, decide you don’t want it, dispute.

Digital purchases now account for 63% of all merchant transactions globally (Ethoca 2025 State of Chargebacks Report). That’s a huge surface area for disputes.

The Real Cost of a Chargeback (It’s Not Just the Lost Sale)

Most founders think a chargeback costs them the transaction value. That’s just the beginning.

| Cost Component | Typical Amount | Notes |

|---|---|---|

| Lost sale value | 100% of transaction | Funds reversed from your account |

| Chargeback fee | $15–$50 per dispute | Charged by your payment processor |

| Loss-of-dispute fee (Stripe) | ~$15 extra | Stripe now charges if you fight and lose |

| Ops/support time | 2–4 hours per case | Gathering evidence, submitting response |

| Account termination risk | Existential | Happens if dispute rate exceeds 1% |

| Merchant account re-registration | Weeks + legal costs | If terminated, starting over is brutal |

The 2025 data from Chargebacks911 puts it bluntly: every dollar lost to fraud costs US merchants $4.61 in total when you factor in all the downstream costs. A single $50 chargeback? It’s actually costing you closer to $230.

And here’s the threshold you need to memorize: Visa’s VAMP (Visa Acquirer Monitoring Program) threshold is 1.5% for merchants. Cross it and you’re in a monitoring program. Cross it repeatedly and you lose your merchant account. Mastercard has equivalent programs. In 2026, Visa also introduced tiered dispute fees based on response speed — with some U.S. merchants having as little as 9 days to respond to certain disputes.

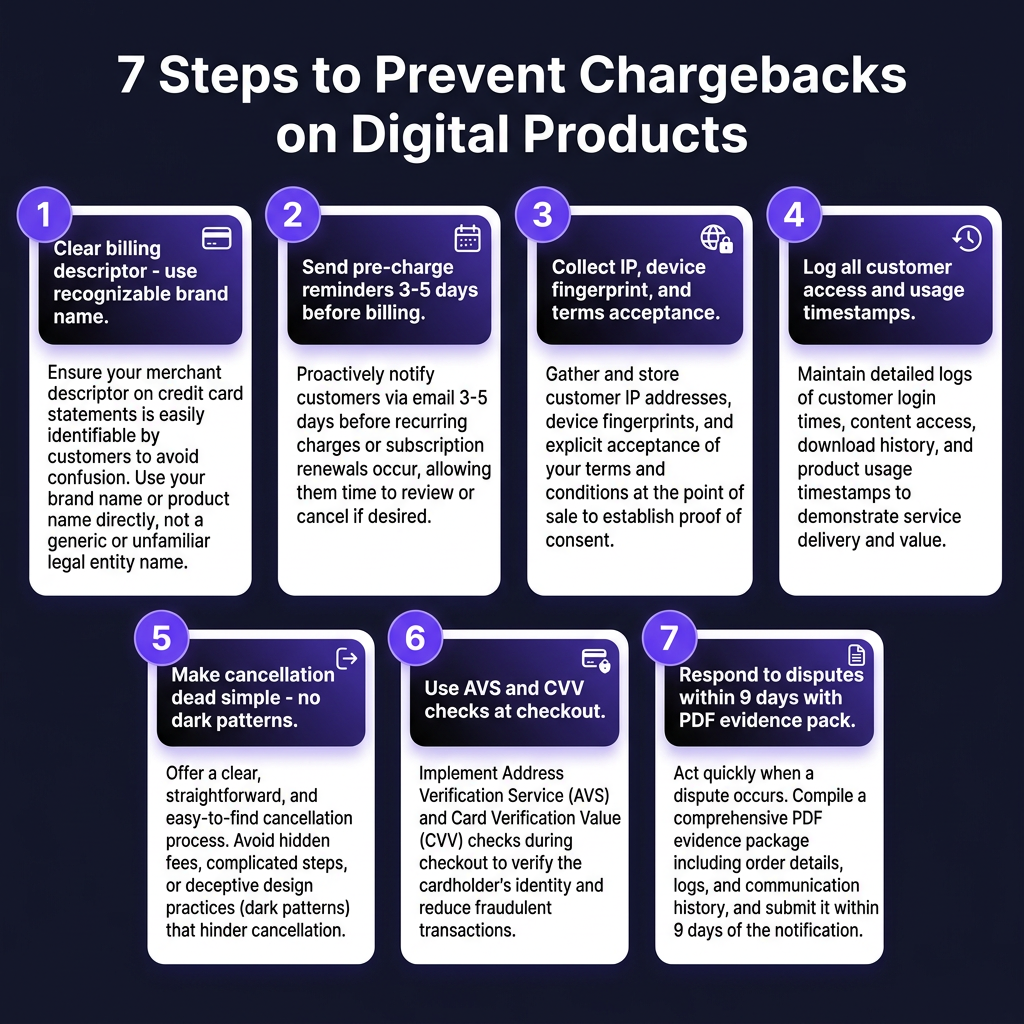

The 7 Prevention Strategies That Actually Work

Let’s skip the generic advice. Here’s what actually moves the needle for SaaS and digital product companies.

1. Fix Your Billing Descriptor

The #1 reason customers file chargebacks on legitimate purchases: they don’t recognize the charge on their bank statement. If your billing descriptor says “SVC*TECHCORP” instead of “Fungies.io – Subscription,” you’re creating chargebacks.

Use a recognizable brand name. Add a customer service phone number or URL. Most processors let you customize this — actually do it.

2. Send Pre-Charge Reminders

For subscriptions, email customers 3–5 days before renewal. Tell them: exact amount, billing date, what they’re paying for, and how to cancel. Yes, some will cancel. The ones who would have charged back are worse — they cost you money AND damage your dispute rate.

3. Collect Evidence at Checkout

Before a dispute happens, you need to be collecting:

- IP address and geolocation at purchase

- Device fingerprint

- Timestamped checkbox or click confirming terms acceptance

- Email confirmation with order details

- For high-value transactions: CVV + AVS verification

You can’t submit evidence you don’t have. Build the paper trail before you need it.

4. Log Access and Usage Data

This is the single most powerful piece of evidence in a digital product dispute. If you can show timestamped login records proving a customer accessed your product after purchase, you win the vast majority of friendly fraud chargebacks.

Log: first login timestamp, feature usage events, last active date, emails opened and clicked. Store this in a queryable format tied to customer email and transaction ID.

5. Make Cancellation Dead Simple

Dark patterns around cancellation are a chargeback factory. If a customer can’t easily cancel, they’ll dispute instead. One-click cancellation in your customer portal isn’t just good UX — it’s a financial risk reduction strategy. Chargebacks cost 10x more than a refund.

6. Offer Proactive Refunds on High-Risk Cases

Got a support ticket from a customer who sounds like they’re heading toward a dispute? Refund them proactively. A refund costs you the transaction value. A chargeback costs you the transaction value + the fee + the dispute rate hit. This math is always the same: refund wins.

7. Use Chargeback Alert Tools

Services like Ethoca Alerts and Verifi Order Insight give you a 24–72 hour window to issue a refund before a customer dispute becomes a formal chargeback. For high-volume merchants, this is essential infrastructure. The key limitation: alerts work for prevention, not for repeat friendly fraudsters — you’ll need to blacklist those customers entirely.

How to Win a Chargeback Dispute: Building a Compelling Evidence Package

If prevention fails and you’re facing a chargeback, here’s the reality: the average merchant win rate for fraud-related chargebacks is just 17.1%. For all chargebacks they choose to fight, merchants win about 54% (Chargeback.io, 2026).

The gap between 17% and 54% comes down to evidence quality. Here’s what a winning evidence package looks like.

What to Include in Your Dispute Response

| Evidence Type | What to Include | Why It Matters |

|---|---|---|

| Customer identification | Name, email, billing address matching card | Proves who made the purchase |

| Transaction details | Date, amount, invoice number, payment method | Baseline facts the bank needs |

| Authorization evidence | IP address, device fingerprint, terms checkbox timestamp | Proves they authorized the charge |

| Product delivery proof | Download confirmation email, license key delivery log | Proves what was delivered |

| Access and usage timeline | First login, feature events, last active date | Strongest evidence — proves they used it |

| Terms acceptance | Screenshot of T&C checkbox + timestamp | Proves they agreed to your refund policy |

| Communication history | Support tickets, emails, chats | Shows the full customer relationship |

Structure this as a single PDF with clear sections. Banks and card networks receive thousands of these — make yours easy to navigate. Add a one-page executive summary at the top. If you have usage logs with SHA-256 hash verification (proving the document wasn’t altered after the fact), even better.

Reason Code Matters

Visa and Mastercard chargebacks come with reason codes that tell you what the customer is claiming. The two most common for digital products:

- Code 10.4 (Fraud – Card Absent): Customer claims they didn’t make the purchase. Fight with: IP, device fingerprint, geolocation, terms acceptance timestamp, usage logs.

- Code 13.1 (Merchandise Not Received): Customer claims they never got the product. Fight with: download confirmation, license delivery log, access logs showing they logged in.

Remember: in 2026, Visa’s new tiered response system means some disputes require action in as little as 9 days. If you don’t have an automated system tracking incoming disputes, you will miss deadlines.

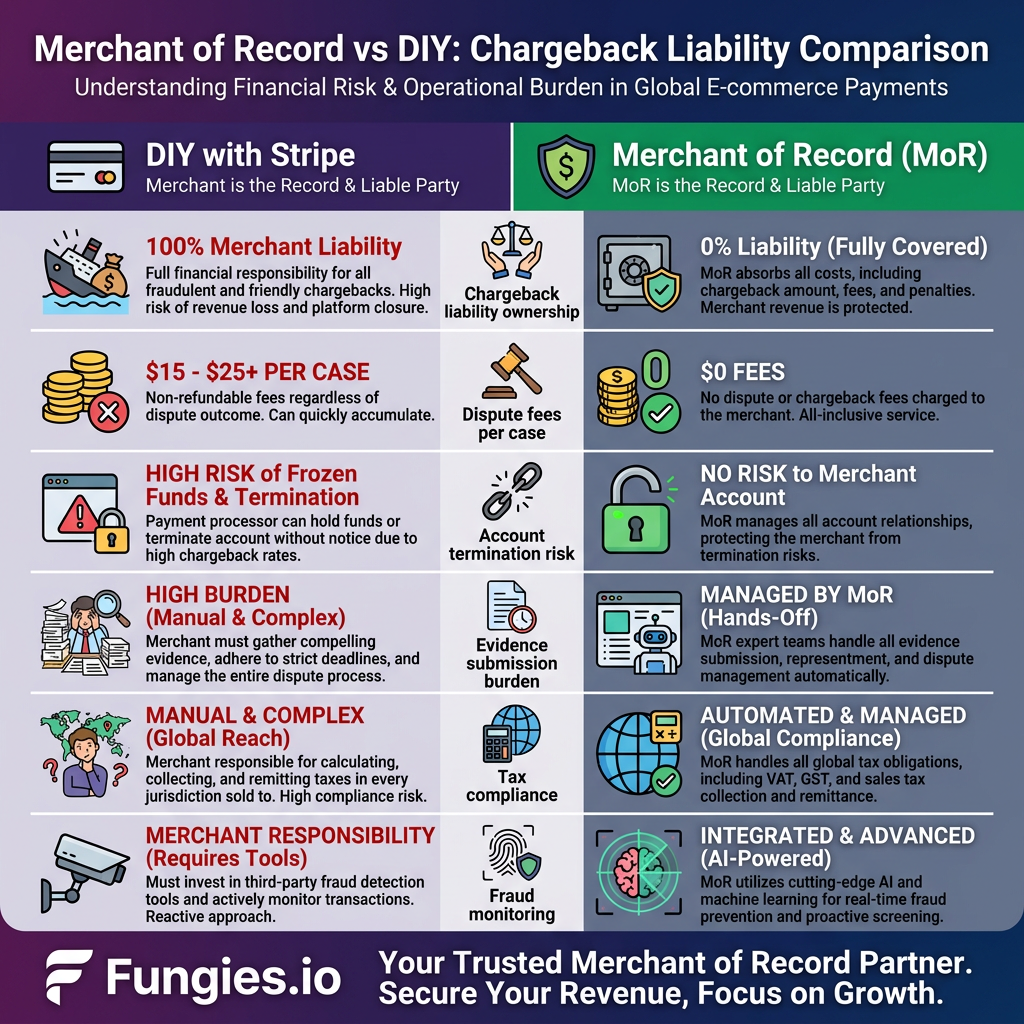

The Merchant of Record Option: Offloading the Entire Problem

Here’s the approach most SaaS founders don’t fully understand until they’ve lost a merchant account or burned hundreds of hours on disputes: use a Merchant of Record (MoR).

When you sell through an MoR like Fungies.io, the MoR is the legal seller of record — not you. That means:

- Chargebacks land on the MoR’s merchant account, not yours

- Dispute fees are absorbed by the MoR

- The MoR handles evidence submission and dispute management

- Your account termination risk: zero (you don’t have a direct merchant account)

- Fraud monitoring and prevention tools are built in

FastSpring’s documentation puts it explicitly: “As the Merchant of Record, FastSpring is responsible for monitoring fraud rates and chargebacks to remain within thresholds set by card networks.” Same applies to Fungies.io, Paddle, and similar MoR providers.

This doesn’t mean you’re completely hands-off — if your products generate excessive chargebacks, the MoR will come to you. But you’re no longer facing account termination, and you’re not building dispute management infrastructure from scratch.

MoR vs DIY: What Actually Changes

| Factor | DIY (Stripe / Direct) | Merchant of Record (Fungies.io) |

|---|---|---|

| Chargeback liability | Your responsibility | MoR’s responsibility |

| Dispute fees | $15–$50 per case, your cost | Absorbed by MoR |

| Account termination risk | Your merchant account at risk | No direct merchant account to lose |

| Evidence submission | You build and submit | MoR handles |

| Dispute monitoring | Manual or third-party tools | Built-in |

| Tax compliance | Separate problem entirely | Included in MoR service |

| Global payment methods | Stripe supports ~40 countries well | Localized checkout worldwide |

| Engineering overhead | High — you own the stack | Low — MoR owns it |

The trade-off: MoRs take a percentage of revenue as their fee (typically 5–9% depending on volume and features). For early-stage products, that’s often worth it. For high-volume businesses with dedicated ops teams, the math shifts.

Key Takeaways

- The 1% rule is real. If your chargeback rate exceeds 1% of transactions, you’re in danger zone. Visa’s VAMP threshold is 1.5% — cross it and you’ll be in a monitoring program with potential account termination.

- The true cost of a chargeback is 4–5x the transaction value. Fees, time, and downstream risk multiply fast. Proactive refunds are almost always cheaper than disputes.

- Usage logs are your best defense. Timestamped access records after purchase are the single strongest evidence against friendly fraud. Build this logging from day one.

- Respond fast in 2026. Visa’s new rules mean some disputes require action in as little as 9 days. Manual processes won’t cut it at any real volume.

- A Merchant of Record removes the existential risk. If you’re a small team and chargebacks are eating your ops bandwidth, the MoR model shifts liability and infrastructure cost off your plate entirely.

FAQ

What happens if my chargeback rate goes above 1%?

You’ll be placed in a payment processor’s dispute monitoring program (like Visa’s VAMP or Mastercard’s MDMM). This triggers additional fees, more scrutiny, and if the rate doesn’t drop, merchant account termination. Getting a new merchant account after termination is slow and expensive. The priority is preventing it.

Can I blacklist customers who file chargebacks?

Yes, and you should. Many payment processors support blocklists by card number, email, device fingerprint, or IP. Services like Kount and Signifyd maintain cross-merchant fraud networks. If someone files a fraudulent chargeback, block them from repurchasing. Some MoRs handle this automatically.

How do I prove digital product delivery to win a chargeback?

The best evidence is timestamped server-side logs showing when the customer first logged in or downloaded after purchase. Back this up with: license key delivery email, download confirmation, IP and device matching the purchaser’s identity, and terms acceptance records. Compile it into a single PDF with a clear summary page.

Is a Merchant of Record worth it just for chargeback protection?

Chargeback protection is one benefit among several. MoRs also handle global VAT/GST compliance, localized checkout, payment method optimization, and fraud detection. For early-stage founders who want to focus on product over payment infrastructure, the full package makes sense. If your only concern is chargebacks, targeted tools like Chargebacks911 or Chargeblast may be a better starting point before committing to a full MoR.

Conclusion

Chargebacks on digital products aren’t going down — they went up 59% in a single year and the $28 billion annual loss figure is still climbing. But this isn’t a hopeless situation. The merchants who get hurt are the ones reacting to chargebacks rather than building systems to prevent them.

Start with the basics: fix your billing descriptor, log customer access data, and make cancellation easy. Add pre-dispute alert tools when volume justifies it. And if you want to offload the liability entirely — including chargebacks, global taxes, and payment compliance — a Merchant of Record like Fungies.io handles all of it so you can ship product instead of managing disputes.

Ready to sell digital products without the chargeback headaches? Start with Fungies.io — free to try, no upfront fees.

References

- Ethoca 2025 State of Chargebacks Report — Justt.ai

- Chargeback Stats 2026 — Chargebacks911

- Chargeback Statistics 2025: Trends, Costs, Solutions — Chargeflow

- Q4 2025 Digital Trust Index: Dispute & Chargeback Data — Sift

- Visa Chargeback Rules 2026: Time Limits & Thresholds — SeamlessChex

- Why Digital Goods Are More Susceptible to Chargebacks — PayCompass

- Chargebacks and Disputes — FastSpring Docs

- Chargeback Prevention for SaaS: 12 Strategies — Dodo Payments

- How to Win a Chargeback Dispute as a SaaS Company — Revano