The artificial intelligence market has reached an unprecedented inflection point in 2026. With global AI investment hitting $202.3 billion in 2025—representing a staggering 50% of all venture capital deployed worldwide—the concentration of capital in AI has reached levels never before seen in technology history. This is not just another tech bubble; it is a fundamental restructuring of how businesses operate, compete, and create value.

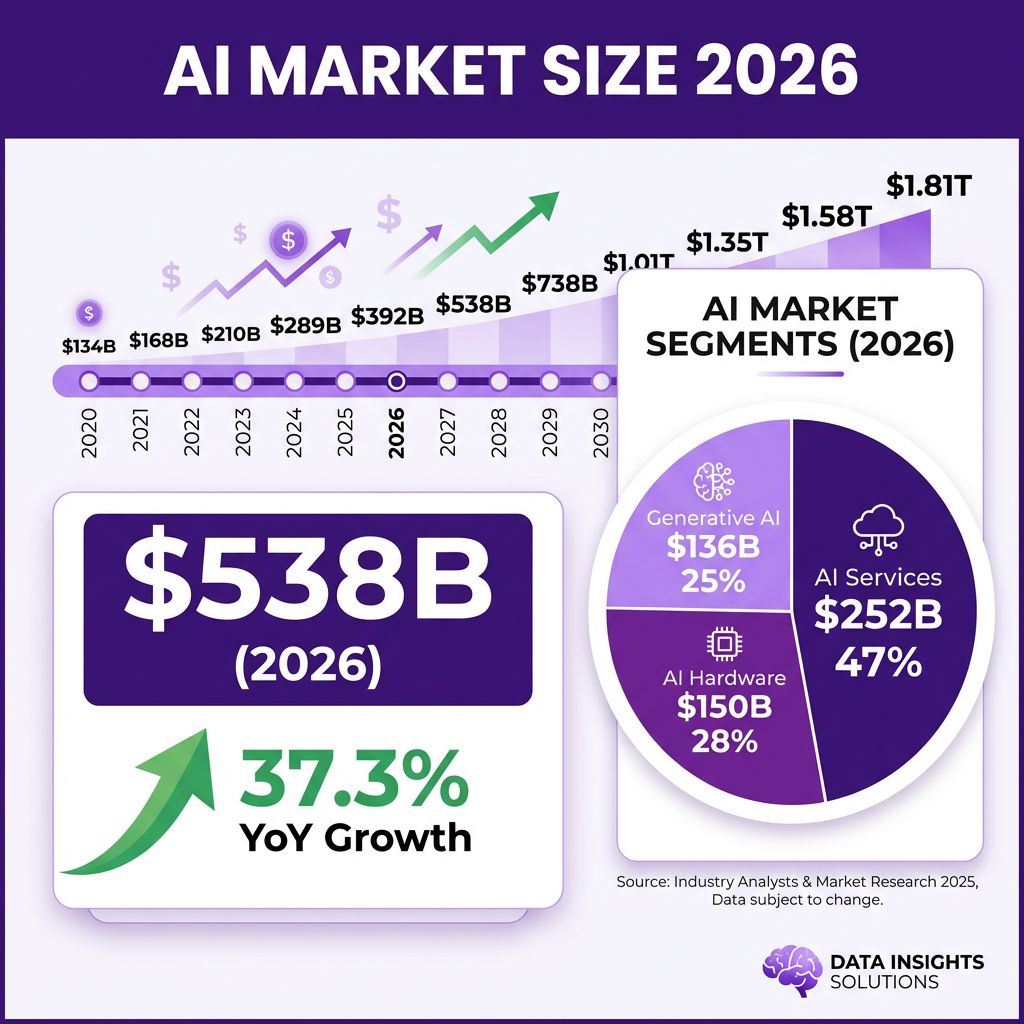

According to the latest market data, the global AI market size has reached $538 billion in 2026, growing at an explosive year-over-year rate of 37.3%. This growth trajectory puts the market on track to exceed $1.81 trillion by 2030, representing one of the fastest-growing technology sectors in history. For business leaders, developers, and investors, understanding this landscape is not optional—it is essential for survival in an increasingly AI-driven economy.

\n

\n

Market Overview: The $538 Billion AI Ecosystem

The artificial intelligence market in 2026 represents a complex ecosystem spanning software, hardware, services, and infrastructure. Understanding the scale and composition of this market is critical for anyone looking to capitalize on AI transformative potential.

Global Market Size and Growth Trajectory

The global AI market has experienced explosive growth over the past decade, but 2026 marks a particularly significant milestone. With a market valuation of $538 billion, AI has cemented its position as one of the most valuable technology sectors globally. This represents a compound annual growth rate (CAGR) of approximately 36.6% to 37.6%, depending on the research methodology employed.

The growth trajectory shows no signs of slowing. Multiple research firms project the AI market will reach between $1.81 trillion and $3.5 trillion by 2033, with the most conservative estimates placing the 2030 market size at $1.81 trillion. This sustained growth is driven by several converging factors: the maturation of generative AI technologies, increasing enterprise adoption, the proliferation of AI-powered applications across industries, and continued massive investment from both private and public sectors.

Breaking down the market by component, we see AI software dominating with projections exceeding $800 billion by 2030. AI hardware, driven by the insatiable demand for GPUs and specialized AI chips, is expected to reach $150 billion by 2030. AI services—including consulting, implementation, and managed services—represent the remaining significant portion of the market.

Regional Market Distribution

The geographic distribution of the AI market reveals a concentration of activity in North America, particularly the United States. According to recent data, North American AI companies secured $214.5 billion in funding, representing the lion’s share of global investment. The San Francisco Bay Area alone captured 60% of global AI funding—approximately $126 billion—despite representing a much smaller fraction of the global population.

However, the landscape is shifting. China has accelerated its AI industrialization efforts significantly, and the performance gap between Chinese and American AI systems is narrowing rapidly. According to Stanford 2026 AI Index Annual Report, China is making substantial gains in AI model performance, challenging the long-held assumption of American dominance in the field.

Europe represents the third major AI market, with significant growth observed across healthcare, finance, manufacturing, and other technology sectors. European markets are characterized by strong regulatory frameworks, including the AI Act, which shapes how AI technologies are developed and deployed within the region.

\n

\n

Key Statistics and Data Points

The AI market in 2026 is defined by a series of remarkable statistics that illustrate both the scale of current adoption and the potential for future growth. These numbers tell a story of rapid transformation across every sector of the economy.

Market Size and Investment Statistics

- $538 billion — Global AI market size in 2026

- 37.3% — Year-over-year growth rate of the AI market

- $1.81 trillion — Projected AI market size by 2030

- $3.5 trillion — Long-term projection for AI market by 2033

- 36.6% to 37.6% — Compound Annual Growth Rate (CAGR) through 2030

- $202.3 billion — Global AI investment in 2025

- 50% — Share of total venture capital deployed to AI in 2025

- $211 billion — AI venture capital funding in 2025 (Crunchbase data)

- $270 billion — AI startup funding in 2025 (alternative measurement)

- 61% — Share of global VC investment captured by AI firms in 2025 (OECD)

- $330.9 billion — Record global VC investment in Q1 2026 (more than double Q4 2025)

- $214.5 billion — North American AI company funding in 2025

- 60% — Share of global AI funding captured by San Francisco Bay Area

- $126 billion — AI funding in San Francisco Bay Area specifically

Generative AI Market Statistics

- $136 billion — Generative AI market size in 2026

- 81% — OpenAI market share in generative AI

- 900 million — ChatGPT active users as of 2026

- 800 million+ — ChatGPT weekly active users

- 10% — Roughly 10% of global population uses ChatGPT weekly

- $8 billion — ChatGPT revenue generated for OpenAI in 2025

- 128% — Year-over-year revenue growth for ChatGPT

- 2.5 billion — Prompts processed by ChatGPT per day

- 18 billion — Messages sent per week on ChatGPT

- $10 billion — OpenAI annual recurring revenue

- $29.4 billion — OpenAI projected total revenue for 2026

- $30 billion — Anthropic annualized revenue run rate

- $4 billion — Anthropic revenue (mid-2025), up from $1B at start of year

Enterprise Adoption Statistics

- 58% — Companies using AI in production environments

- 56% — Enterprise leaders who are “enthusiastic champions” of AI adoption

- 67% — Organizations that have adopted AI in some form

- 40% — Companies reporting measurable productivity gains from AI

- 35% — Organizations with formal AI governance frameworks

- 72% — IT leaders planning to increase AI investments in 2026

- 45% — Businesses using AI for customer service automation

- 38% — Companies implementing AI for sales and marketing

- 52% — Organizations using AI for data analysis and insights

- 28% — Enterprises with AI fully integrated into core business processes

AI Hardware and Infrastructure Statistics

- $150 billion — Projected AI hardware market size by 2030

- $32.3 billion — AI data center GPU market size in 2026

- 58% — NVIDIA share of custom cloud AI accelerator market

- 192GB — HBM3 memory in AMD Instinct MI300X accelerator

- 3x — Expected growth in AI ASIC investments

- $800 billion — Projected AI software market size by 2030

Major Trends Shaping AI in 2026

The AI landscape in 2026 is being shaped by seven transformative trends that are redefining how businesses and consumers interact with artificial intelligence. These trends represent both opportunities and challenges for organizations looking to leverage AI effectively.

1. The Rise of Agentic AI

Agentic AI—autonomous AI systems capable of planning, reasoning, and executing complex tasks with minimal human intervention—has emerged as the dominant paradigm in 2026. Unlike traditional AI models that respond to individual prompts, agentic AI systems can break down complex goals into subtasks, execute them sequentially, and adapt their approach based on intermediate results.

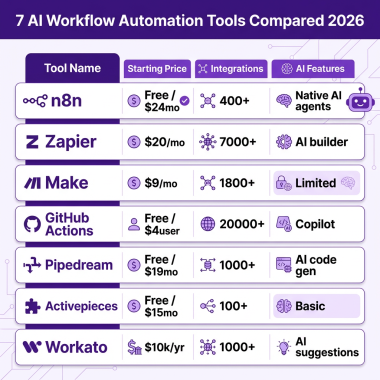

This shift represents a fundamental evolution in AI capabilities. Enterprises are increasingly deploying AI agents for workflow automation, customer support, sales pipeline management, and IT service management. Microsoft Copilot Studio, n8n, and other platforms are leading this transformation, enabling businesses to build custom AI agents tailored to their specific needs.

The impact on productivity is substantial. Organizations implementing agentic AI report significant reductions in manual task completion time, with some enterprises seeing 40-60% efficiency gains in automated workflows. As these systems become more sophisticated, they are handling increasingly complex business processes that previously required human judgment and decision-making.

2. Generative AI Market Maturation

The generative AI market has matured significantly in 2026, moving from experimental adoption to production deployment across enterprises. With a market size of $136 billion, generative AI now represents approximately 25% of the total AI market. This segment includes text generation (ChatGPT, Claude), image generation (Midjourney, DALL-E), code generation (GitHub Copilot), and multimodal systems.

OpenAI continues to dominate with an estimated 81% market share in generative AI, though competition is intensifying. Anthropic has emerged as a serious challenger, with some enterprise users preferring Claude for business applications due to its reasoning capabilities and safety features. Google Gemini and open-source alternatives like Llama are also gaining traction, particularly for organizations concerned about data privacy and vendor lock-in.

The business models in generative AI are also evolving. While API-based consumption remains popular, we are seeing increased adoption of fine-tuned models, on-premises deployments, and hybrid approaches that balance cost, performance, and data sovereignty requirements.

3. Domain-Specific AI Models

While general-purpose large language models (LLMs) like GPT-4 and Claude capture headlines, 2026 has seen explosive growth in domain-specific AI models optimized for particular industries or use cases. These specialized models often outperform general-purpose alternatives in their specific domains while requiring significantly less computational resources.

Healthcare AI models trained on medical literature and clinical data are achieving diagnostic accuracy that rivals human specialists. Legal AI systems are automating contract review and legal research with unprecedented speed and accuracy. Financial services AI models are detecting fraud and optimizing trading strategies in real-time. Manufacturing AI is predicting equipment failures and optimizing production schedules.

This trend toward specialization is driven by both technical and economic factors. Domain-specific models can be smaller and more efficient, reducing inference costs. They also face fewer regulatory hurdles in regulated industries because their training data and behavior can be more carefully controlled and audited.

4. AI Hardware and Infrastructure Boom

The insatiable demand for AI compute has driven unprecedented growth in AI hardware markets. NVIDIA remains the dominant player with its GPU offerings, but competition is intensifying from AMD, Intel, and a host of specialized AI chip startups. The AI data center GPU market alone is valued at $32.3 billion in 2026.

A particularly significant development is the rise of AI ASICs (Application-Specific Integrated Circuits). Tech giants including Google (TPU), Amazon (Trainium/Inferentia), Microsoft (Maia), and Meta (MTIA) are investing heavily in custom silicon optimized for their specific AI workloads. These custom chips offer better performance per watt and lower costs for high-scale deployments.

The infrastructure supporting AI is also evolving rapidly. Cloud providers are building massive AI-focused data centers, with some facilities consuming hundreds of megawatts of power. Edge AI infrastructure is growing to support low-latency applications, while new networking technologies are being developed to handle the massive data flows between AI training clusters.

5. AI Regulation and Governance

2026 marks a turning point in AI regulation, with major jurisdictions implementing comprehensive frameworks for AI governance. The European Union AI Act has come into full effect, establishing risk-based categories for AI systems and imposing strict requirements on high-risk applications. The United States has issued executive orders and agency-specific guidance, while China has implemented its own comprehensive AI regulations.

These regulations address concerns including algorithmic bias, data privacy, transparency, and accountability. Organizations deploying AI systems must now conduct impact assessments, maintain audit trails, and ensure human oversight of high-stakes decisions. The regulatory landscape is creating new compliance costs but also building trust in AI systems among consumers and businesses.

Ethics and governance have become board-level concerns. Companies are establishing AI ethics committees, implementing responsible AI frameworks, and investing in tools for bias detection and mitigation. The challenge of proving AI systems are trustworthy, auditable, and accountable has become central to enterprise AI strategy.

6. Focus on AI ROI and Business Value

After years of experimentation, enterprises in 2026 are demanding concrete returns on their AI investments. The conversation has shifted from “What can AI do?” to “What business value does AI deliver?” This focus on ROI is driving more disciplined approaches to AI implementation, with organizations carefully measuring productivity gains, cost savings, and revenue impacts.

Successful AI implementations are demonstrating measurable value across multiple dimensions. Direct financial returns include cost reduction through automation and revenue growth through enhanced products and services. Operational efficiency gains include faster processing times, reduced error rates, and improved resource utilization. Strategic benefits include enhanced decision-making capabilities, improved customer experiences, and competitive differentiation.

However, measuring AI ROI remains challenging. Benefits are often distributed across multiple business units, making attribution difficult. Intangible benefits like improved employee satisfaction or enhanced brand perception are hard to quantify. Organizations are developing more sophisticated measurement frameworks, but standardization across the industry remains limited.

7. AI-Powered Developer Tools and Coding Assistants

AI coding assistants have become indispensable tools for software developers in 2026. GitHub Copilot, Amazon CodeWhisperer, and similar tools are now used by the majority of professional developers, dramatically increasing coding productivity and reducing time spent on routine programming tasks.

The capabilities of these tools have expanded beyond simple code completion. Modern AI coding assistants can generate entire functions from natural language descriptions, explain complex code, suggest optimizations, identify bugs, and even generate comprehensive test suites. They are increasingly integrated into development workflows, participating in code reviews and continuous integration pipelines.

This trend is reshaping the software development profession. Junior developers can be productive more quickly, while senior developers can focus on architecture and complex problem-solving rather than routine implementation. However, concerns about code quality, security vulnerabilities, and over-reliance on AI-generated code remain active areas of discussion in the developer community.

\n

\n

Key Players and Competitive Landscape

The AI market in 2026 is characterized by intense competition among established technology giants, well-funded startups, and emerging challengers. Understanding the competitive dynamics is essential for predicting future market developments and identifying partnership or investment opportunities.

OpenAI: The Market Leader

OpenAI remains the dominant force in generative AI, with ChatGPT 900 million active users and $10 billion in annual recurring revenue. The company valuation has skyrocketed from $157 billion to a targeted $830 billion in just fourteen months—an unprecedented trajectory in technology history. OpenAI GPT models power countless applications across industries, and the company API business serves thousands of enterprise customers.

However, OpenAI faces increasing challenges. The company has shifted focus toward enterprise customers as consumer growth slows. Competition from Anthropic, Google, and open-source alternatives is intensifying. Questions about the company governance structure, safety commitments, and path to profitability remain topics of active discussion.

Anthropic: The Enterprise Favorite

Anthropic has emerged as OpenAI most credible challenger, with its Claude AI assistant gaining significant traction among enterprise users. The company has achieved a remarkable revenue trajectory, growing from $1 billion in annualized revenue at the beginning of 2025 to $4 billion by mid-2025, and now reaching a $30 billion annualized run rate. This growth has been driven by Claude reputation for safety, reasoning capabilities, and enterprise-friendly features.

Businesses are increasingly choosing Anthropic over OpenAI for sensitive applications, citing Claude more predictable behavior and stronger safety measures. The company Constitutional AI approach—training models to be helpful, harmless, and honest—resonates with organizations concerned about AI risks.

Google: The Integrated Challenger

Google Gemini AI models and integrated AI features across Search, Workspace, and Cloud represent a formidable competitive threat. The company advantages include massive compute infrastructure, proprietary training data from Search and YouTube, and the ability to integrate AI deeply into products used by billions of people.

Google strategy emphasizes multimodal capabilities—AI systems that can understand and generate text, images, audio, and video. The company custom TPU chips provide cost advantages for training and inference. However, Google faces challenges in monetizing its AI investments and concerns about AI potentially cannibalizing its core search advertising business.

Microsoft: The Enterprise Enabler

Microsoft has positioned itself as the leading enterprise AI platform through its partnership with OpenAI and integration of AI capabilities across its product suite. Copilot features in Office 365, GitHub, and Azure give Microsoft unparalleled distribution for AI tools in enterprise environments.

The company Azure AI services provide infrastructure for organizations building custom AI applications. Microsoft enterprise relationships, security credentials, and compliance capabilities make it a trusted partner for conservative organizations beginning their AI journeys. The company is also investing in custom AI silicon to reduce dependence on NVIDIA.

NVIDIA: The Infrastructure King

NVIDIA dominates AI infrastructure with its GPUs powering the majority of AI training and inference workloads. The company data center revenue has grown exponentially as demand for AI compute has surged. NVIDIA software ecosystem, including CUDA and specialized AI libraries, creates significant switching costs for customers.

The company is expanding beyond GPUs into specialized AI chips for inference, networking equipment for AI data centers, and software platforms for AI development. NVIDIA GTC conferences have become the definitive events for the AI industry. However, the company faces growing competition from custom silicon developed by cloud providers and specialized AI chip startups.

\n

\n

Other Notable Players

Beyond the major players, the AI market includes numerous significant companies. Meta continues to invest heavily in AI research and open-source models like Llama. Amazon offers AI services through AWS and is developing custom chips. Apple is integrating AI capabilities into its devices with a focus on privacy. IBM, Oracle, and Salesforce offer enterprise AI solutions. A vibrant ecosystem of AI startups addresses specific use cases and industry verticals.

AI Market Segmentation Deep Dive

Understanding the AI market requires examining its various segments in detail. Each segment has unique dynamics, growth drivers, and competitive landscapes that shape the overall market trajectory.

AI Software Market

The AI software market represents the largest segment, projected to exceed $800 billion by 2030. This segment includes machine learning platforms, natural language processing tools, computer vision software, and AI development frameworks. The dominance of software reflects the reality that AI value is primarily delivered through applications that process data, make predictions, and automate decisions.

Within AI software, generative AI has emerged as the fastest-growing subsegment. From $136 billion in 2026, this market is expected to grow rapidly as businesses integrate generative capabilities into their products and workflows. Applications range from content creation and code generation to drug discovery and materials science.

AI Hardware Market

The AI hardware market, valued at approximately $50 billion in 2026 and projected to reach $150 billion by 2030, includes GPUs, TPUs, specialized AI accelerators, and networking equipment. NVIDIA dominates this market with its data center GPUs, but competition is intensifying from AMD, Intel, and custom silicon developed by cloud providers.

The emergence of AI ASICs represents a significant shift in the hardware landscape. Google TPUs, Amazon Trainium and Inferentia chips, Microsoft Maia processors, and Meta MTIA accelerators are designed specifically for the AI workloads of their respective platforms. These custom chips offer better performance per watt and can reduce costs at scale, though they lack the flexibility of general-purpose GPUs.

AI Services Market

AI services—including consulting, system integration, and managed services—represent a growing and increasingly important segment. As AI technology becomes more complex and organizations lack internal expertise, demand for external AI services has surged. Major consulting firms have built substantial AI practices, while specialized AI consultancies have emerged to address specific industry needs.

The services market also includes AI training and education, as organizations invest in upskilling their workforces. With AI capabilities becoming essential across roles and industries, training programs have become a significant market in their own right. This includes both technical training for AI developers and awareness training for business users.

Regional AI Market Analysis

The AI market exhibits significant regional variation in adoption, investment, and regulatory approaches. Understanding these differences is essential for global AI strategies.

North America

North America, particularly the United States, remains the dominant region for AI development and investment. The San Francisco Bay Area alone captured $126 billion of global AI funding in 2025, representing 60% of the worldwide total. This concentration reflects the region’s unique ecosystem of venture capital, leading research universities, and major technology companies.

U.S. AI companies lead in foundational model development, with OpenAI, Anthropic, Google, and Meta based in the country. The regulatory approach in the U.S. has been relatively permissive, favoring innovation while addressing specific risks through sectoral regulations. However, executive orders and agency guidance have begun to establish frameworks for AI governance.

China

China represents the second-largest AI market and is rapidly closing the gap with the United States. According to Stanford 2026 AI Index, the performance gap between Chinese and American AI systems has narrowed significantly. Chinese companies like Baidu, Alibaba, and Tencent have developed competitive AI models, while government support has accelerated AI adoption across industries.

China AI strategy emphasizes industrial applications, smart cities, and autonomous systems. The country has also implemented comprehensive AI regulations, including algorithmic recommendation management provisions and deep synthesis regulations for synthetic media. These regulations reflect China focus on maintaining social stability while promoting technological development.

Europe

Europe has taken a distinctive approach to AI, prioritizing regulation and ethical considerations alongside innovation. The EU AI Act, which came into full effect in 2026, establishes a risk-based framework for AI governance, with strict requirements for high-risk applications. This regulatory leadership has influenced AI governance discussions globally.

European AI companies have focused on specific niches, including industrial AI, privacy-preserving technologies, and AI for sustainability. While Europe lacks the tech giants of the U.S. and China, it has strengths in research, specialized applications, and regulatory technology. The European approach to AI emphasizes human-centric development and democratic values.

AI Investment and Funding Landscape

The funding environment for AI has been extraordinary, with investment levels unprecedented in technology history. Understanding this landscape is crucial for entrepreneurs, investors, and corporate strategists.

Venture Capital Concentration

AI has captured an extraordinary share of venture capital investment. In 2025, AI firms accounted for 61% of global VC investment according to OECD data, totaling $258.7 billion out of $427.1 billion globally. This concentration reflects both the massive capital requirements for AI development and investor conviction in AI transformative potential.

The first quarter of 2026 set new records, with global VC investment reaching $330.9 billion—more than double the $128.6 billion in Q4 2025. This surge was driven by AI megadeals, including massive funding rounds for foundation model companies. The scale of these investments has raised concerns about valuation sustainability and the potential for market corrections.

Notable Funding Rounds

Several AI companies have raised extraordinary funding rounds that reflect market enthusiasm. OpenAI valuation trajectory from $157 billion to a targeted $830 billion in fourteen months represents one of the fastest value appreciations in business history. Anthropic has also raised substantial funding to support its rapid growth and competitive positioning.

Beyond the foundation model companies, significant funding has flowed to AI infrastructure providers, vertical AI applications, and AI-enabled services. The breadth of investment across the AI stack suggests market confidence in the technology long-term potential, even as specific valuations may be debated.

Corporate Investment and M&A

Corporate investment in AI has also surged, with major technology companies investing billions in AI research, development, and acquisitions. Microsoft investment in OpenAI, Google investments in DeepMind and internal AI development, and Amazon investments in AI infrastructure represent some of the largest corporate technology investments in history.

M&A activity in AI has been robust, with established companies acquiring AI startups to gain talent, technology, and market position. This consolidation trend is likely to continue as larger companies seek to build comprehensive AI capabilities and startups look for exit opportunities in a competitive funding environment.

Challenges and Pain Points

Despite the remarkable growth and potential of the AI market, significant challenges remain. Organizations implementing AI face technical, organizational, and societal obstacles that must be addressed for the technology to reach its full potential.

1. Algorithmic Bias and Fairness

AI models learn from historical data, and that data often reflects human biases. This creates risks of AI systems perpetuating or amplifying discrimination in hiring, lending, criminal justice, and other high-stakes domains. Addressing algorithmic bias requires careful attention to training data, model design, and ongoing monitoring of AI system outputs.

The challenge is compounded by the difficulty of defining fairness across different contexts. Mathematical definitions of fairness can conflict with each other, and what constitutes fair treatment varies across cultures and applications. Organizations deploying AI must navigate these complexities while maintaining system performance and usability.

2. Data Privacy and Security

AI systems require massive amounts of data, raising significant privacy concerns. Training data may include personal information, and AI models can sometimes memorize and regurgitate sensitive data from their training sets. The use of AI for surveillance, facial recognition, and behavioral analysis creates additional privacy risks.

Security concerns are also paramount. AI systems can be vulnerable to adversarial attacks designed to cause misclassification or inappropriate outputs. The concentration of AI capabilities among a few providers creates systemic risks. Organizations must implement robust security measures while maintaining the utility of AI systems.

3. Regulatory Compliance and Governance

The evolving regulatory landscape creates compliance challenges for AI deployers. Different jurisdictions have adopted varying approaches to AI governance, creating complexity for global organizations. Requirements for transparency, explainability, and human oversight can conflict with the black-box nature of many AI systems.

Organizations must develop governance frameworks that address these requirements while enabling innovation. This includes establishing AI ethics committees, implementing model risk management processes, and maintaining audit trails for AI decisions. The cost and complexity of compliance can be significant, particularly for smaller organizations.

Opportunities and Growth Strategies

The challenges in the AI market are significant, but so are the opportunities. Organizations that successfully navigate the complexities of AI adoption can achieve substantial competitive advantages and create significant value.

1. Industry-Specific AI Solutions

One of the largest opportunities lies in developing AI solutions tailored to specific industries. Generic AI tools often fail to address the unique requirements, regulatory constraints, and workflows of particular sectors. Companies that develop deep domain expertise and build AI solutions optimized for specific industries can command premium pricing and build durable competitive moats.

Healthcare AI, for example, requires understanding of medical workflows, regulatory requirements, and clinical evidence standards. Financial services AI must address compliance, risk management, and market dynamics. Manufacturing AI needs to integrate with operational technology and handle real-time constraints. The companies that master these domain-specific challenges will capture significant value.

2. AI Infrastructure and Tooling

The explosive growth in AI adoption creates massive demand for infrastructure and tooling. This includes compute resources for training and inference, data management platforms, model monitoring tools, and development frameworks. Companies that provide reliable, scalable infrastructure for AI workloads can build highly profitable businesses.

Specific opportunities include specialized hardware for AI inference at the edge, tools for managing AI model lifecycles, platforms for fine-tuning and customizing models, and services for ensuring AI safety and compliance. As AI becomes more pervasive, the infrastructure supporting it becomes more valuable.

3. AI-Enabled Services and Consulting

Many organizations lack the internal capabilities to implement AI effectively. This creates opportunities for service providers who can help companies develop AI strategies, implement solutions, and manage ongoing operations. AI consulting, system integration, and managed services represent growing markets with attractive margins.

The most successful service providers combine technical AI expertise with deep industry knowledge. They can translate business problems into AI solutions, manage the organizational change required for AI adoption, and ensure ongoing value delivery. As AI technology continues to evolve rapidly, the demand for expert guidance will remain strong.

Case Studies and Success Stories

Real-world examples illustrate the transformative potential of AI when implemented effectively. These case studies demonstrate how organizations across industries are leveraging AI to create value.

Case Study 1: Enterprise Workflow Automation

A global financial services firm implemented agentic AI to automate complex back-office workflows. The company deployed AI agents capable of processing loan applications, verifying documentation, and making preliminary approval decisions. The implementation reduced processing time from days to hours, improved accuracy by 35%, and freed human employees to focus on complex cases requiring judgment.

The key success factors included careful process mapping, extensive training of the AI system on historical data, and a phased rollout that allowed for iterative improvement. The company also invested heavily in change management, ensuring employees understood how AI would augment rather than replace their roles.

Case Study 2: AI-Powered Customer Service

A major telecommunications provider deployed generative AI to transform its customer service operations. The company implemented AI assistants capable of handling routine inquiries, troubleshooting technical issues, and processing service changes. The system integrates with backend systems to access customer data and transaction history.

Results included a 50% reduction in average handling time, a 40% improvement in first-call resolution rates, and significantly higher customer satisfaction scores. The AI system handles 70% of inquiries without human intervention, while seamlessly escalating complex issues to human agents with full context.

Case Study 3: AI-Assisted Software Development

A mid-sized software company adopted AI coding assistants across its development teams. Developers use AI tools for code completion, bug detection, test generation, and documentation. The company also implemented AI for code review, automatically flagging potential issues and suggesting improvements.

The results were transformative: 45% increase in developer productivity, 30% reduction in bugs reaching production, and 50% faster onboarding of new developers. The company was able to deliver more features with the same team size, significantly improving its competitive position. Importantly, developer satisfaction increased as engineers spent more time on creative problem-solving and less on routine coding tasks.

Future Outlook and Predictions

Looking ahead to 2027-2030, several trends will shape the evolution of the AI market. These predictions are based on current trajectories, technological developments, and market dynamics.

Market Growth Projections

The AI market is projected to continue its rapid growth, reaching $1.81 trillion by 2030 according to Grand View Research. More aggressive projections suggest the market could exceed $3.5 trillion by 2033. This growth will be driven by continued enterprise adoption, the emergence of new AI-powered products and services, and the integration of AI into virtually every aspect of business and consumer technology.

The generative AI segment is expected to maintain its position as the fastest-growing component of the AI market, with applications expanding beyond text and images to video, audio, 3D content, and multimodal experiences. The hardware market will also see substantial growth as demand for AI compute continues to outpace supply.

Technological Developments

Several technological developments will shape the AI landscape in the coming years. Multimodal AI systems capable of seamlessly processing and generating text, images, audio, and video will become increasingly sophisticated. AI agents will gain the ability to handle more complex, multi-step tasks with less human supervision. Edge AI will enable sophisticated AI capabilities on devices with limited computational resources.

Advances in AI efficiency will reduce the computational resources required for training and inference, making AI more accessible to smaller organizations. New architectures beyond transformers may emerge, offering improvements in efficiency, interpretability, or capability. The integration of AI with robotics, IoT, and other technologies will create new application categories.

Competitive Dynamics

The competitive landscape will continue to evolve rapidly. OpenAI market dominance will face continued challenges from well-funded competitors and open-source alternatives. The major cloud providers—Amazon, Microsoft, and Google—will compete aggressively to be the platform of choice for AI development and deployment. NVIDIA dominance in AI hardware will be challenged by custom silicon from cloud providers and specialized chip companies.

Consolidation is likely as larger companies acquire promising AI startups to acquire talent and technology. Regulatory scrutiny of the largest AI companies may increase, potentially leading to structural separations or operational restrictions. The geographic distribution of AI capabilities may shift as countries invest in domestic AI industries.

Societal Impact

The societal impact of AI will become increasingly apparent. Workforce transformation will accelerate as AI automates more cognitive tasks, requiring significant investments in education and workforce development. Questions about AI rights, consciousness, and moral status may emerge as systems become more sophisticated. The concentration of AI capabilities and economic benefits will raise concerns about inequality and power distribution.

Addressing these challenges will require collaboration between technologists, policymakers, and civil society. The choices made in the coming years about AI development, deployment, and governance will have profound implications for the future of work, democracy, and human flourishing.

Key Takeaways

- The global AI market has reached $538 billion in 2026, growing at 37.3% year-over-year, with projections to exceed $1.81 trillion by 2030

- AI captured 50% of all venture capital in 2025 ($202.3 billion), with 61% of global VC funding going to AI firms

- Seven major trends are shaping the AI landscape: Agentic AI, Generative AI maturation, Domain-specific models, Hardware boom, Regulation, ROI focus, and Developer tools

- OpenAI maintains market leadership with 81% generative AI share and 900 million ChatGPT users, but Anthropic is gaining ground with $30 billion revenue run rate

- Enterprise adoption is accelerating with 58% of companies using AI in production, though measuring ROI remains challenging

- Key challenges include algorithmic bias, data privacy, security, and regulatory compliance across multiple jurisdictions

- Major opportunities exist in industry-specific solutions, AI infrastructure, and consulting services

- The AI market will continue rapid growth through 2030, driven by technological advances and expanding enterprise adoption

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026

- Statista – AI Market Forecast and Industry Analysis

- Crunchbase – AI Venture Capital Investment Data 2025-2026

- OECD – AI Firms Capture 61% of Global Venture Capital in 2025

- KPMG – Global VC Investment Surges to Record $330.9 Billion in Q1 2026

- Noizz.io – AI Market Size 2026: Industry Analysis and Growth Data

- Business of Apps – ChatGPT Revenue and Usage Statistics 2026

- Reuters – Anthropic vs OpenAI Revenue Analysis 2026

- Stanford HAI – 2026 AI Index Annual Report

- Deloitte – State of AI in the Enterprise 2026

- Zapier – Enterprise AI Statistics 2026

- NVIDIA Blog – State of AI Report 2026

- ABI Research – Artificial Intelligence Software Market Forecast

- Precedence Research – U.S. Artificial Intelligence Market Size

- Vention Teams – State of AI 2026 Report

\n