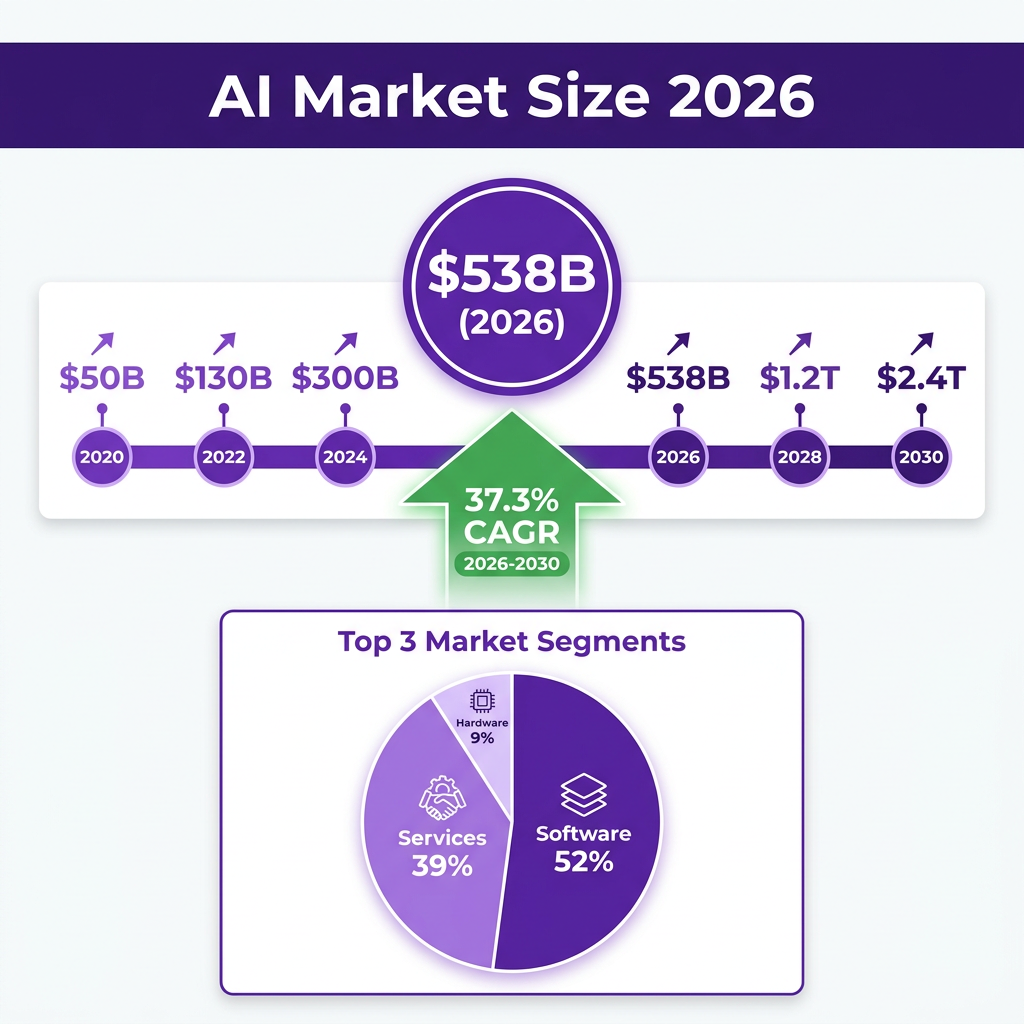

The artificial intelligence market has reached an inflection point that few predicted even three years ago. In 2026, the global AI market stands at $538 billion, representing a staggering 37.3% year-over-year growth rate that shows no signs of slowing. To put this in perspective: the AI industry is now growing faster than the early internet era, faster than mobile computing adoption, and faster than cloud computing’s meteoric rise.

This isn’t just another technology trend—it’s a fundamental restructuring of how businesses operate, how value is created, and how competitive advantage is built. With 72% of enterprises now running at least one AI workload in production and global AI spending projected to surpass $300 billion this year, we’re witnessing the largest technology transformation in modern business history.

Market Overview: The $538 Billion AI Ecosystem

The numbers tell a story of explosive growth that has reshaped the technology landscape. The global AI market, valued at $538 billion in 2026, represents a compound annual growth rate of 37.3% that has consistently outpaced even the most optimistic projections from just two years ago. This growth trajectory positions the AI market to reach approximately $2.4 trillion by 2032, according to MarketsandMarkets research.

Breaking down the market composition reveals where value is being created. Software dominates with 52% of total AI spending, reflecting the industry’s shift toward AI-powered applications, platforms, and development tools. Services account for 39% of the market, as enterprises increasingly rely on consulting, implementation, and managed services to navigate AI adoption. Hardware, while the smallest segment at 9%, remains critical—particularly the AI data center GPU market, which reached $12.83 billion in 2026 and is projected to grow to $77.15 billion by 2035.

The United States maintains its position as the largest single AI market, accounting for $173.56 billion in 2025 with projections to reach $976.23 billion by 2035. This represents a CAGR of 19.33%, though this figure understates the true growth when considering AI integration across existing technology spending. North America as a whole commands 31.8% of global AI market share, driven by the concentration of major AI labs, cloud providers, and enterprise headquarters in the region.

The generative AI subsegment deserves special attention. Having grown from $37.1 billion in 2024 to $136 billion in 2026, generative AI now represents roughly 25% of the total AI market. ABI Research forecasts this segment will reach $220 billion by 2030, with enterprise value creation from generative AI use cases projected at $434 billion annually by that same year. Marketing, advertising, and creative applications account for 46% of current enterprise value creation from generative AI, though this is rapidly diversifying across industries.

Cloud deployment models dominate AI infrastructure, with 73.8% of generative AI deployments running on cloud platforms. This reflects both the computational intensity of AI workloads and the preference of enterprises to avoid massive capital expenditures on AI infrastructure. The AI software platform market specifically—covering the tools and infrastructure that enable AI development—reached $79.38 billion in 2025 and is projected to grow to $106.92 billion in 2026 at a 34.7% CAGR.

Key Statistics and Data Points

The scale of AI adoption in 2026 is best understood through the specific metrics that define this transformation. Here are the critical data points that every business leader, investor, and technology professional should know:

Market Size and Growth: The global AI market reached $538 billion in 2026, up from approximately $223 billion in 2025. This 37.3% year-over-year growth rate exceeds the CAGR of 29.2% projected between 2024 and 2032, indicating that AI adoption is accelerating faster than anticipated. The U.S. AI market specifically accounts for $173.56 billion, with the broader North American region commanding 31.8% of global market share.

Enterprise Adoption Metrics: 72% of enterprises now have at least one AI workload in production as of Q1 2026, according to McKinsey’s Global AI Survey. This represents a dramatic increase from previous years and signals the transition from experimental AI projects to production deployments. The average enterprise runs 4.2 AI models in production, up from just 1.9 in 2023. Perhaps most strikingly, 88% of organizations now use AI in at least one business function—a figure that would have seemed impossible just three years ago.

Generative AI Specifics: The generative AI market reached $136 billion in 2026, growing from $37.1 billion in 2024. ChatGPT alone has over 800 million weekly active users as of December 2025, with users sending 18 billion messages per week. OpenAI’s annualized revenue crossed $20 billion in 2025 and exceeded $25 billion by February 2026. ChatGPT generated $8 billion for OpenAI in 2025, accounting for approximately 66% of the company’s total revenue.

Venture Capital and Investment: AI firms captured 61% of global venture capital in 2025, totaling $258.7 billion out of $427.1 billion in total VC investment. This represents an 85% increase in AI-specific funding from 2024. San Francisco alone captured $126 billion (60%) of global AI funding, despite accounting for only 22% of total global deals. Within the Bay Area, 81% of all startup capital was allocated to AI businesses—an 11 percentage point increase from 2024.

Hardware and Infrastructure: NVIDIA’s data center revenue reached approximately $62 billion in Q4 fiscal 2026, rising 75% year-over-year. For the full fiscal year 2026, NVIDIA’s data center segment grew 68% to nearly $194 billion. The AI data center GPU market is projected to grow from $12.83 billion in 2026 to $77.15 billion by 2035 at a 22.06% CAGR. Global enterprise spending on cloud infrastructure services reached a record $129 billion in Q1 2026, a 35% year-over-year increase.

Workforce and Talent: AI/ML engineers command a 42% salary premium compared to traditional software engineers. Tech megacaps are projected to invest over $300 billion in AI infrastructure and research in 2026. The talent war for AI expertise shows no signs of abating, with major technology companies offering compensation packages that reflect the scarcity of qualified AI researchers and engineers.

AI Search and Discovery: ChatGPT holds 60.2% of the generative AI chatbot market share, followed by Google Gemini at 15.3%, Microsoft Copilot at 12.8%, Perplexity at 5.5%, and Claude at 4.9%. AI search engines collectively handle hundreds of millions of queries per week, fundamentally changing how users discover information and interact with digital content.

Major Trends Shaping AI in 2026

Seven major trends are defining the AI landscape in 2026, each representing a significant shift in how AI is developed, deployed, and consumed. Understanding these trends is essential for anyone seeking to navigate this rapidly evolving market.

1. Agentic AI and Autonomous Systems

The most significant trend of 2026 is the shift from AI assistants that answer questions to AI agents that execute work. Agentic AI systems plan multi-step workflows, retain memory across interactions, and execute actions directly against production systems such as APIs, databases, cloud infrastructure, and internal tools. Unlike earlier AI systems that required constant guidance, agentic AI focuses on autonomous action guided by business goals.

According to Deloitte, 80% of automation leaders plan to accelerate agentic AI deployments this year. These systems are being designed to operate within defined limits, adapt to changing conditions, and support business continuity without constant supervision. The market for agentic AI tools is expanding rapidly, with major players including Microsoft, OpenAI, and Google all investing heavily in autonomous agent capabilities.

2. Enterprise AI Production Deployment

The massive middle of the enterprise market is moving from experimentation to production-grade AI systems. As IBM’s research notes, “The most significant trend we see emerging is the shift from AI experimentation and excitement to private and secure deployments with real ROI expectations within enterprises.” This transition is characterized by a focus on measurable business outcomes rather than proof-of-concept demonstrations.

Enterprises are increasingly demanding AI solutions that integrate with existing systems, maintain security and compliance standards, and deliver quantifiable returns on investment. This has led to a preference for domain-specific AI solutions designed for unique enterprise environments rather than general-purpose AI tools.

3. Multi-Modal AI Models

AI systems that can process and generate multiple types of content—text, images, audio, and video—are becoming the new standard. GPT-5, Claude, and Gemini all offer multi-modal capabilities that enable more natural and comprehensive interactions. This trend is particularly important for creative industries, where AI tools now support end-to-end content creation workflows.

The integration of multi-modal capabilities is driving new use cases in healthcare (medical imaging analysis), manufacturing (visual quality inspection), and media (automated content production). As these models improve, the line between different types of AI applications continues to blur.

4. AI Regulation and Governance

As AI capabilities advance, regulatory frameworks are evolving to address concerns around safety, bias, transparency, and accountability. The International AI Safety Report 2026 highlights the growing focus on risk management practices, including techniques developers use to make AI models more robust and resistant to misuse.

Governance-first AI has become one of the most critical trends in 2026. Organizations are implementing comprehensive AI governance frameworks that address data privacy, model explainability, and ethical use. This trend is particularly pronounced in regulated industries such as healthcare, finance, and government.

5. AI Infrastructure and “AI Factories”

NVIDIA’s “AI factory” vision represents a fundamental shift in how AI infrastructure is conceived and deployed. Rather than simply selling chips, NVIDIA and other infrastructure providers are offering full-stack solutions including chips, interconnects, and software platforms. This vertical integration enables more efficient AI training and inference at scale.

Data centers currently account for 4.4% of U.S. energy demand, with projections estimating this will triple by 2028 due to AI workloads. This has sparked innovation in energy-efficient AI computing and renewed interest in alternative computing architectures.

6. Open Source and Model Democratization

Meta’s Llama models and other open-source AI initiatives are democratizing access to powerful AI capabilities. This trend is challenging the dominance of closed AI systems and enabling smaller organizations to deploy sophisticated AI without massive investments. The availability of open-source models is also driving innovation in model fine-tuning and domain-specific applications.

However, the open-source trend exists in tension with safety concerns, as freely available powerful models can be misused. This dynamic is shaping ongoing debates about AI governance and responsible release practices.

7. AI-Human Collaboration Models

The most successful AI implementations in 2026 are those that reimagine workflows around AI-human collaboration rather than simple automation. As MIT research highlights, “Corporate innovators automating tasks will improve margins 10-20%. Innovators reimagining business models will capture 10x more value from the same AI capabilities.”

This trend is reflected in the shift from asking “what tasks can AI automate?” to asking “what outcomes can AI deliver that we couldn’t profitably deliver before?” Organizations that approach AI as a business transformation rather than a tool deployment are capturing disproportionate value.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a mix of established technology giants and well-funded private companies, each competing across multiple layers of the AI stack. Understanding this competitive landscape is crucial for predicting where value will accrue in the coming years.

OpenAI remains the most valuable private AI company with a valuation of $182.6 billion (per Forbes AI 50) or $157 billion (per other sources). The company’s ChatGPT product dominates the consumer AI market with 60.2% market share and over 800 million weekly active users. OpenAI’s revenue exceeded $25 billion annualized by February 2026, representing one of the fastest revenue ramps in business history. The company’s partnership with Microsoft provides both cloud infrastructure and enterprise distribution.

Anthropic, the creator of Claude, has emerged as OpenAI’s primary competitor in the large language model space. Valued at over $60 billion, Anthropic has differentiated itself through a focus on AI safety and more capable reasoning models. The company’s Claude 3 and subsequent releases have gained traction particularly among developers and enterprise users who value the model’s analytical capabilities.

Google DeepMind combines Google’s research capabilities with DeepMind’s AI expertise. The Gemini model family represents Google’s response to OpenAI’s GPT models, with tight integration into Google’s product ecosystem. Google’s advantages in data, compute infrastructure, and distribution make it a formidable long-term competitor, despite initial challenges in the generative AI race.

Microsoft has positioned itself as the enterprise AI leader through its Copilot products and exclusive cloud partnership with OpenAI. Microsoft’s strategy focuses on integrating AI capabilities across its productivity and cloud platforms, making AI accessible to the millions of businesses already using Microsoft services. The company’s Azure cloud platform is a major beneficiary of AI-driven infrastructure demand.

Meta has taken a different approach, focusing on open-source AI through its Llama model family. By making powerful models freely available, Meta is building an ecosystem around its AI infrastructure while avoiding the massive compute costs of serving consumer AI products. This strategy has gained significant traction among developers and researchers.

NVIDIA dominates AI hardware, with its GPUs powering the majority of AI training and inference workloads. The company’s data center revenue reached $194 billion in fiscal 2026, up 68% year-over-year. NVIDIA’s “AI factory” vision extends its influence beyond chips to full-stack AI infrastructure solutions.

Amazon Web Services (AWS), Alibaba Cloud, and Oracle round out the major cloud providers competing for AI workloads. AWS maintains the largest overall cloud market share at approximately 31%, though Microsoft Azure is growing faster due to its AI advantages. Google Cloud reported $20 billion in revenue in Q1 2026, a 63% year-over-year increase driven largely by AI demand.

Beyond these giants, the Forbes AI 50 list highlights emerging players including ElevenLabs (voice generation, $800M valuation), Gamma (AI graphic design), and Notion (AI-powered productivity). These companies represent the application layer of AI, where specialized solutions are being built on top of foundation models.

Challenges and Pain Points

Despite the extraordinary growth and optimism surrounding AI, significant challenges remain. These pain points represent both risks for current market participants and opportunities for new solutions.

1. Integration with Legacy Systems

The most commonly cited barrier to enterprise AI adoption is difficulty integrating AI with existing IT infrastructure and legacy systems. Many enterprises operate on decades-old technology stacks that were not designed for AI integration. This challenge is particularly acute in regulated industries such as banking and healthcare, where system modernization must be carefully managed.

Organizations are addressing this challenge through API-centric architectures that allow AI systems to interact with legacy applications without requiring full system replacement. The rise of agentic AI is partly driven by the need for AI systems that can navigate complex, heterogeneous enterprise environments.

2. Data Quality and Availability

AI systems are fundamentally limited by the data they’re trained on and have access to. Many enterprises struggle with data silos, inconsistent data formats, and poor data quality. The International AI Safety Report 2026 highlights data-related risks including privacy concerns, bias in training data, and the challenges of maintaining data security in AI systems.

Data centers currently account for 4.4% of U.S. energy demand, with projections estimating this will triple by 2028. The environmental impact of AI training and inference is becoming a significant concern, particularly as models grow larger and more compute-intensive.

3. Talent Scarcity and Skills Gap

The demand for AI talent far exceeds supply. AI/ML engineers command 42% salary premiums, and the competition for top researchers has intensified to the point where major technology companies are acquiring entire AI startups primarily for their talent. This scarcity extends beyond technical roles to include AI product managers, ethicists, and professionals who can bridge the gap between technical capabilities and business applications.

The skills gap is particularly challenging for smaller organizations that cannot compete with the compensation packages offered by major technology companies. This dynamic threatens to concentrate AI capabilities within a small number of large organizations.

4. Regulatory Uncertainty

AI regulation is evolving rapidly, with different jurisdictions taking varying approaches. The European Union’s AI Act, various U.S. state-level regulations, and emerging frameworks in China and other markets create a complex compliance landscape. Organizations operating globally must navigate multiple, sometimes conflicting regulatory requirements.

Key regulatory concerns include algorithmic transparency, data privacy, liability for AI decisions, and restrictions on high-risk AI applications. The rapid pace of AI development means that regulations often lag behind technological capabilities, creating uncertainty for businesses planning multi-year AI investments.

5. Cost and ROI Pressure

While AI adoption is widespread, demonstrating clear ROI remains challenging for many organizations. The costs of AI infrastructure, talent, and ongoing model maintenance are substantial. As the initial excitement around AI gives way to more measured evaluation, organizations are increasingly demanding proof of business value.

This pressure is particularly acute for generative AI projects, where the costs of inference (running models in production) can be significant at scale. Organizations are responding by focusing on high-value use cases, optimizing model efficiency, and implementing careful cost monitoring.

Opportunities and Growth Strategies

The challenges in the AI market create significant opportunities for organizations that can address them effectively. Here are the key growth strategies that are proving successful in 2026:

1. Vertical AI Solutions

Rather than competing with general-purpose AI platforms, many successful AI companies are building deeply specialized solutions for specific industries. Healthcare AI, financial services AI, manufacturing AI, and legal AI are all substantial markets with unique requirements that general-purpose models cannot fully address.

These vertical solutions can command premium pricing due to their specialized capabilities and regulatory compliance. They also benefit from network effects as industry-specific data improves model performance over time. Companies like Insilico Medicine in drug discovery and Harvey in legal AI exemplify this strategy.

2. AI Infrastructure and Tooling

The explosive growth in AI adoption has created massive demand for infrastructure and tooling. Companies providing model serving infrastructure, AI development platforms, data labeling services, and AI monitoring tools are experiencing rapid growth. This “picks and shovels” approach to the AI gold rush offers more predictable business models than competing directly in the foundation model space.

The AI software platform market, which includes these infrastructure and tooling solutions, reached $79.38 billion in 2025 and is projected to grow to $106.92 billion in 2026. Companies like Hugging Face, Weights & Biases, and LangChain are building essential infrastructure for the AI ecosystem.

3. AI Services and Consulting

With 72% of enterprises running AI in production but many struggling with implementation, AI services represent a massive opportunity. Consulting firms, system integrators, and specialized AI consultancies are seeing unprecedented demand. The services segment accounts for 39.52% of the U.S. AI market, indicating the scale of this opportunity.

Successful AI services firms combine technical expertise with deep domain knowledge and change management capabilities. As AI moves from experimentation to production, the need for implementation support, training, and ongoing optimization continues to grow.

4. Edge AI and Distributed Computing

As AI applications proliferate, running all AI workloads in centralized cloud data centers becomes increasingly inefficient. Edge AI—running AI models on local devices—offers lower latency, improved privacy, and reduced bandwidth costs. This trend is particularly important for applications in autonomous vehicles, industrial IoT, and mobile devices.

The development of more efficient AI models and specialized edge AI chips is enabling increasingly sophisticated applications to run on resource-constrained devices. Companies like Qualcomm, Apple, and NVIDIA are investing heavily in edge AI capabilities.

Case Studies and Success Stories

Real-world implementations demonstrate how organizations are capturing value from AI in 2026. These case studies illustrate different approaches to AI adoption and the results they’re achieving.

Case Study 1: JPMorgan Chase — AI-Powered Software Development

JPMorgan Chase has deployed AI coding assistants across its engineering organization, with remarkable results. According to Reuters reporting, the bank’s engineers experienced efficiency gains of up to 20% using AI coding assistants. This translates to significant cost savings and faster time-to-market for software projects across the organization.

The implementation required careful attention to security and compliance, given the sensitive nature of financial services software. JPMorgan’s approach demonstrates how even highly regulated industries can capture value from AI when implementation is thoughtful and controlled.

Case Study 2: Procter & Gamble — AI for Consumer Insights

Procter & Gamble has leveraged AI to unlock new insights from consumer data, transforming how the company understands and responds to market trends. By applying advanced analytics and machine learning to vast datasets, P&G has improved demand forecasting, optimized supply chain operations, and enhanced marketing effectiveness.

The company’s approach, documented in MIT Sloan Management Review, emphasizes the integration of AI into existing business processes rather than creating separate AI initiatives. This “AI as infrastructure” approach has enabled P&G to scale AI capabilities across its global operations.

Case Study 3: Schneider Electric — AI in Manufacturing

Schneider Electric has scaled AI across both its products and internal processes, demonstrating how industrial companies can leverage AI for competitive advantage. The company’s AI implementations span predictive maintenance, energy optimization, and automated quality control.

Schneider Electric’s approach highlights the importance of domain expertise in successful AI implementation. By combining deep knowledge of industrial systems with AI capabilities, the company has developed solutions that deliver measurable improvements in efficiency and reliability.

Future Outlook and Predictions

The AI market’s trajectory points to continued explosive growth through 2030 and beyond. Here’s what the data suggests about the future of AI:

Market Size Projections: Multiple research firms project the AI market will reach between $1.8 trillion and $2.4 trillion by 2030-2032. MarketsandMarkets forecasts $2.4 trillion by 2032 at a 30.6% CAGR. Grand View Research projects growth from $375.93 billion in 2026 to $2.48 trillion by 2034 at a 26.6% CAGR. These projections, while varying in specifics, all indicate sustained high growth for the remainder of the decade.

Technology Evolution: By 2030, AI capabilities will likely exceed current levels in ways that are difficult to predict. The International AI Safety Report suggests that AI systems will demonstrate significantly improved reasoning capabilities, multi-modal understanding, and autonomous operation. The report also highlights the importance of preparing for potential risks associated with increasingly capable AI systems.

Enterprise Adoption: The gap between AI leaders and laggards will continue to widen. Organizations that successfully integrate AI into their core operations will capture disproportionate value, while those that delay risk being permanently disadvantaged. McKinsey research suggests that top performers pair efficiency gains with growth and innovation, redesigning work end-to-end rather than simply automating existing processes.

Regulatory Landscape: AI regulation will continue to evolve, with increasing focus on high-risk applications, algorithmic transparency, and international coordination. Organizations should expect a more structured regulatory environment by 2030, with established standards for AI safety, privacy, and accountability.

Investment Continuity: Tech megacaps are projected to invest over $300 billion annually in AI infrastructure and research. This sustained investment will drive continued innovation in model capabilities, hardware efficiency, and application development. The concentration of investment among major technology companies raises questions about market competition and the distribution of AI benefits.

Workforce Transformation: AI will continue to reshape labor markets, with some roles being automated while new roles emerge. The World Economic Forum and other organizations project significant shifts in skill requirements across industries. Organizations that proactively manage this transition will be better positioned than those that react to changes as they occur.

Regional AI Market Analysis

The global AI market exhibits significant regional variations in adoption, investment, and regulatory approaches. Understanding these regional dynamics is essential for businesses operating in multiple markets and for investors seeking to allocate capital effectively.

North America: The United States and Canada continue to dominate the global AI landscape, with North America accounting for 31.8% of global AI market share. The U.S. market alone reached $173.56 billion in 2025 and is projected to grow to $976.23 billion by 2035. This dominance is driven by the concentration of leading AI research institutions, major technology companies, and venture capital funding. San Francisco’s Bay Area alone captured $126 billion in AI funding in 2025, representing 60% of global AI investment despite accounting for only 22% of deals.

The regulatory environment in North America remains relatively permissive compared to other regions, though this is evolving. The U.S. approach has favored innovation while gradually introducing sector-specific regulations for high-risk applications. This has enabled rapid deployment of AI technologies across industries, though concerns about safety and accountability are driving increased regulatory attention.

Europe: The European AI market is characterized by a more cautious approach to adoption, influenced by the European Union’s AI Act and strong data protection regulations. While European AI investment lags behind North America, the region has strengths in industrial AI, robotics, and AI for manufacturing. Germany’s AI market is expected to grow at a 30.9% CAGR from 2024 to 2030, reflecting strong industrial applications.

The EU’s regulatory framework prioritizes safety, transparency, and fundamental rights, creating compliance requirements that affect AI deployment across member states. While this approach may slow adoption in some areas, it also creates opportunities for companies specializing in AI governance, explainability, and compliance solutions.

Asia-Pacific: The Asia-Pacific region represents the fastest-growing AI market, with rapid adoption in China, Japan, South Korea, and Singapore. China has made AI a national priority, with substantial government investment and a thriving ecosystem of AI companies. The region benefits from large data populations, strong

manufacturing bases for AI hardware, and significant government support for AI development.

Japan and South Korea lead in robotics and industrial AI applications, while Singapore has positioned itself as a hub for AI research and development in Southeast Asia. The diverse regulatory approaches across the region create both opportunities and challenges for multinational AI deployments.

AI Industry Segments Deep Dive

The AI market comprises multiple distinct segments, each with its own growth dynamics, competitive landscape, and value creation opportunities. Understanding these segments helps identify where investment and innovation are most concentrated.

Natural Language Processing (NLP): NLP remains the most mature and widely deployed AI technology, powering everything from chatbots to document analysis to code generation. The success of large language models like GPT-5, Claude, and Gemini has demonstrated the commercial viability of advanced NLP capabilities. The NLP software market continues to grow rapidly, driven by enterprise demand for automated content generation, customer service automation, and knowledge management.

Computer Vision: Computer vision applications have expanded beyond traditional use cases in manufacturing quality control and security to include medical imaging, autonomous vehicles, and augmented reality. The integration of computer vision with generative AI is creating new possibilities for image and video generation, editing, and analysis. The market for AI sensing software, which includes computer vision, is experiencing strong growth as hardware capabilities improve and deployment costs decline.

Predictive Analytics: Predictive AI software helps organizations forecast demand, identify risks, and optimize operations. This segment has been a staple of enterprise AI adoption for years and continues to evolve with more sophisticated machine learning techniques. The integration of predictive analytics with real-time data streams is enabling more responsive and adaptive business processes.

Robotics and Autonomous Systems: While still emerging compared to software-based AI, robotics and autonomous systems represent a significant growth opportunity. Applications range from warehouse automation to surgical robots to autonomous vehicles. The convergence of AI with robotics hardware is enabling more capable and flexible automated systems.

AI for Science: Perhaps the most transformative long-term application of AI is in scientific research and discovery. AI systems are accelerating drug discovery, materials science, climate modeling, and fundamental physics research. While the commercial models for AI in science are still evolving, the potential impact on human knowledge and capability is immense.

AI Business Models and Monetization

The AI industry has developed diverse business models as companies seek to capture value from AI capabilities. Understanding these models is essential for both AI providers and customers evaluating AI investments.

API-Based Services: The most common AI business model involves providing access to AI capabilities through APIs, typically charged based on usage (per token, per image, per minute of audio, etc.). OpenAI, Anthropic, and most AI providers use this model, which aligns pricing with value delivered and enables easy integration into existing applications.

Subscription SaaS: Many AI applications are delivered as SaaS products with monthly or annual subscriptions. This model provides predictable revenue and aligns provider incentives with ongoing customer success. Examples include AI writing assistants, design tools, and productivity applications.

Enterprise Licensing: For on-premise or private cloud deployments, enterprise licensing remains common. This model addresses security and compliance requirements while enabling customization and integration with existing systems. Enterprise licenses typically involve significant upfront costs plus ongoing maintenance fees.

Outcome-Based Pricing: An emerging model ties AI pricing to measurable business outcomes. This approach reduces customer risk and aligns provider incentives with delivering real value. While challenging to implement due to the complexity of attributing business results to AI specifically, outcome-based pricing is gaining traction in areas with clear ROI metrics.

Hardware-Integrated Solutions: Companies like NVIDIA combine hardware sales with software and services to capture value across the AI stack. This integrated approach can provide better performance and support while creating higher barriers to competition.

Implications for Business Leaders

The rapid evolution of the AI market has profound implications for business leaders across industries. Here are the key strategic considerations for executives navigating this transformation:

AI as Competitive Necessity: With 72% of enterprises now running AI in production, AI has transitioned from a competitive advantage to a competitive necessity. Organizations that fail to adopt AI risk being permanently disadvantaged in efficiency, customer experience, and innovation. The question is no longer whether to adopt AI, but how quickly and effectively.

Focus on Business Outcomes: Successful AI implementations start with clear business objectives rather than technology capabilities. Organizations should identify specific problems that AI can solve or opportunities it can create, then select appropriate technologies. This outcome-focused approach helps avoid the common trap of implementing AI for its own sake without delivering measurable value.

Invest in Data Infrastructure: AI capabilities are fundamentally limited by data quality and availability. Organizations should prioritize investments in data infrastructure, governance, and management to ensure AI systems have access to accurate, timely, and relevant data. This foundational work often determines the success or failure of AI initiatives.

Develop AI Talent: The scarcity of AI talent means organizations must invest in developing internal capabilities through training, hiring, and partnerships. This includes not just technical roles but also AI product managers, ethicists, and business translators who can bridge the gap between technical possibilities and business needs.

Manage Risk and Governance: As AI becomes more deeply embedded in business processes, organizations must develop robust governance frameworks addressing ethics, safety, privacy, and compliance. Proactive risk management is essential for maintaining stakeholder trust and avoiding regulatory penalties.

Prepare for Continuous Change: The AI landscape is evolving so rapidly that static strategies quickly become obsolete. Organizations should build adaptive capabilities that enable rapid response to new technologies, competitive moves, and market conditions. This includes maintaining strategic optionality through partnerships, pilot programs, and modular architectures.

Key Takeaways

- The global AI market reached $538 billion in 2026, growing at 37.3% year-over-year—faster than any major technology transition in history

- 72% of enterprises now run AI in production, with the average enterprise deploying 4.2 AI models—up from 1.9 in 2023

- Generative AI has emerged as a $136 billion subsegment, with ChatGPT alone generating $8 billion in revenue for OpenAI

- AI firms captured 61% of global venture capital in 2025 ($258.7 billion), with San Francisco alone receiving $126 billion in AI funding

- Agentic AI represents the most significant trend of 2026, shifting from AI assistants to autonomous AI agents that execute complex workflows

- NVIDIA dominates AI hardware with $194 billion in data center revenue, while OpenAI leads in models with a $157-182 billion valuation

- The AI market is projected to reach $2.4 trillion by 2032, representing a multi-trillion dollar opportunity for businesses, investors, and professionals

- 88% of organizations now use AI in at least one business function, making AI adoption a competitive necessity rather than an option

- The services segment accounts for 39.52% of the U.S. AI market, highlighting the massive opportunity in AI consulting and implementation

- AI/ML engineers command 42% salary premiums, reflecting the critical shortage of AI talent across all industries

Sources and Citations

- Noizz.io – AI Market Size 2026: $538B Global + 37.3% YoY Growth

- Precedence Research – U.S. Artificial Intelligence Market Size 2026-2035

- Exploding Topics – AI Market Size Statistics 2025-2032

- ABI Research – Artificial Intelligence Software Market Size 2024-2030

- IBM Think – AI Tech Trends Predictions 2026

- MIT Sloan Management Review – Five Trends in AI and Data Science for 2026

- Gartner – Strategic Predictions for 2026

- Miniloop.ai – Best AI Companies in 2026

- Crunchbase – Q1 2026 Venture Funding Records

- OECD – Venture Capital Investments in AI Through 2025

- MedhaCloud – 67 AI Adoption Statistics for 2026

- PixelBrainy – AI Adoption Statistics in 2026

- Deloitte – State of AI in the Enterprise 2026

- Gleecus – The Future of AI in 2026: Major Trends and Predictions

- PlektonLabs – Agentic Enterprise in North America: Trends in 2026

- Futran Solutions – Agentic AI Trends Business Leaders Can’t Ignore

- Adopt.ai – Agentic AI Trends Report 2026

- The Globe and Mail – NVIDIA’s AI Factory Vision

- New York Times – Nvidia’s Quarterly Profit Hits $43 Billion

- MarketsandMarkets – AI Market Growth Forecast 2030

- Fortune Business Insights – Artificial Intelligence Market Size 2034

- Grand View Research – Artificial Intelligence Market Report 2033

- Global Market Insights – Generative AI Market Size 2026-2035

- Business of Apps – ChatGPT Revenue and Usage Statistics 2026

- TechnologyChecker.io – ChatGPT Statistics 2026

- GetPanto.ai – ChatGPT Statistics 2026

- International AI Safety Report 2026

- AIHub.org – Top AI Ethics and Policy Issues 2025-2026

- Forbes – 8 AI Ethics Trends That Will Redefine Trust in 2026