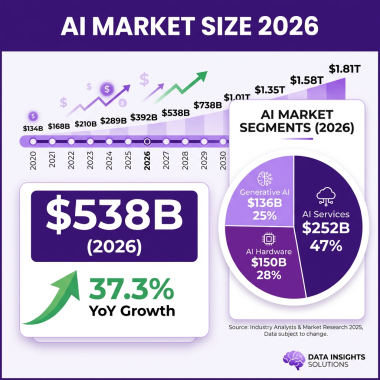

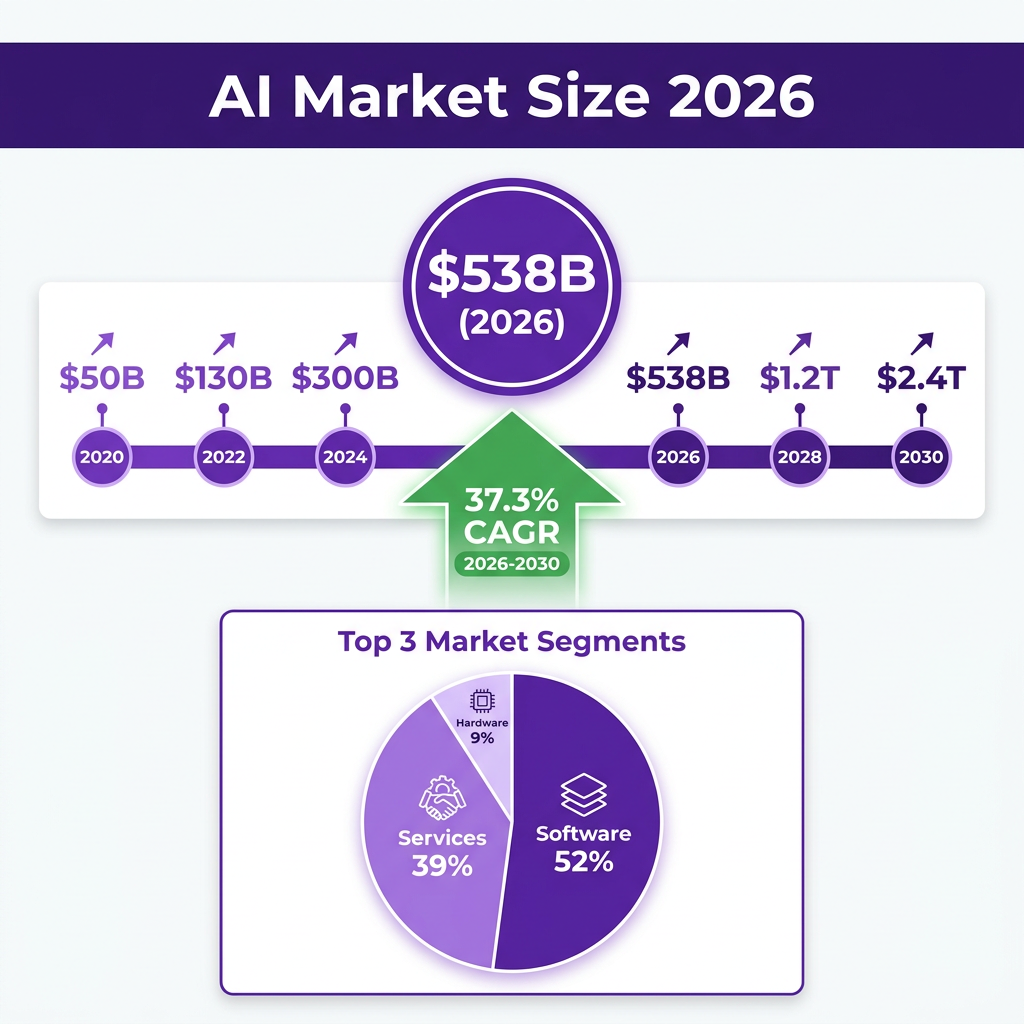

The artificial intelligence market has reached an inflection point in 2026. What began as experimental chatbots and image generators has evolved into a $434 billion global industry that is fundamentally reshaping how businesses operate, compete, and create value. According to Mordor Intelligence’s comprehensive market analysis, the AI market is projected to grow from $306 billion in 2025 to $434 billion in 2026, representing a staggering 42% year-over-year increase that signals the definitive transition from AI experimentation to enterprise-scale deployment.

This is not merely another technology trend passing through the hype cycle. Artificial intelligence has become the foundational infrastructure for modern business operations, with McKinsey’s 2025 global survey revealing that 88% of organizations now use AI in at least one business function. Yet beneath these impressive adoption numbers lies a significantly more complex reality: only 20% of enterprises have successfully moved AI from pilot projects to sustained production use. This gap between experimentation and industrialization represents both the greatest challenge and the greatest opportunity in the current AI market.

The disparity between AI experimentation and production deployment has created a two-tier market. Organizations that have successfully industrialized AI are pulling ahead of competitors, capturing market share, and redefining customer expectations. Those stuck in pilot purgatory are watching their investments generate interesting demos but little business impact. In this comprehensive analysis, we will examine the AI market’s current state with unprecedented depth, explore the seven transformative trends driving explosive growth, analyze the competitive landscape dominated by both established tech giants and innovative startups, and provide actionable insights for organizations looking to capture sustainable value from their AI investments.

Market Overview: The $434 Billion AI Ecosystem

The global artificial intelligence market has experienced unprecedented expansion throughout 2025 and 2026, reaching $434 billion according to Mordor Intelligence’s latest comprehensive analysis. This represents a compound annual growth rate (CAGR) of 41.95% projected from 2026 to 2031, with the market expected to hit an astounding $2.5 trillion by 2031. These numbers place AI among the fastest-growing technology markets in human history, outpacing even the early internet boom in terms of absolute dollar growth and velocity of adoption.

The market’s composition reveals a remarkably diverse ecosystem spanning multiple technology categories and application domains. Machine learning continues to dominate with approximately 40% of total market share, representing the maturation of traditional AI applications in prediction, classification, and pattern recognition. Generative AI has captured 35% of the market, demonstrating explosive growth since ChatGPT’s launch in late 2022 transformed public awareness and enterprise interest. Computer vision accounts for 25% of market share, powering applications from autonomous vehicles to medical imaging and quality control systems.

Grand View Research provides alternative market sizing, estimating the total AI market at $391 billion in 2026 with projections approaching $3.5 trillion by 2033. The generative AI segment alone has reached $63 billion in 2026 according to Statista, representing one of the fastest-growing subsegments within the broader AI landscape. This variation in market sizing reflects the challenges of defining AI market boundaries, as AI capabilities increasingly become embedded within broader software and services.

Geographic distribution of AI investment and adoption reveals North America maintaining market leadership with approximately 37% of global AI market share. This dominance is driven by significant investments from U.S. technology giants, a robust venture capital ecosystem, and concentration of AI research talent. The United States AI market alone is valued at nearly $47 billion according to Statista’s country-level analysis. Asia-Pacific follows with 28% market share, led by China’s aggressive AI development initiatives, significant government investment, and the growing presence of competitive companies like DeepSeek that have demonstrated capabilities matching Western models at significantly lower cost structures.

Europe accounts for 23% of the global AI market, with the European Union’s AI Act creating a regulated but innovation-friendly environment that emphasizes responsible AI development. The regulatory clarity provided by the EU AI Act, despite compliance burdens, has given European enterprises confidence to invest in AI deployment. The remaining 12% of market share is distributed across Latin America, Middle East, and Africa, representing emerging markets with significant growth potential as AI infrastructure and talent become more globally distributed.

Industry adoption patterns reveal that IT and telecommunications lead with 28% of total AI spending, driven by network optimization, customer service automation, and infrastructure management applications. Banking and financial services follow at 22%, with AI deployed for fraud detection, algorithmic trading, risk assessment, and customer service. Healthcare accounts for 18% of AI spending, spanning drug discovery, medical imaging, clinical decision support, and administrative automation. Retail represents 15% of the market, with applications in demand forecasting, personalization, supply chain optimization, and customer service.

Manufacturing, automotive, and media/entertainment round out the top industry sectors, each representing significant growth opportunities as AI capabilities mature and deployment costs decline. The cross-industry nature of AI adoption suggests this is not a sector-specific trend but rather a fundamental shift in how all businesses operate, compete, and create value. Every industry is becoming an AI industry, with competitive advantage increasingly determined by an organization’s ability to effectively deploy and leverage artificial intelligence.

Investment flows into AI have reached truly historic levels, fundamentally reshaping capital markets and technology valuations. Global venture funding in Q1 2026 hit approximately $300 billion across roughly 6,000 funded companies according to Crunchbase data. AI captured roughly 80% of this capital, representing approximately $242 billion in Q1 alone. This concentration of investment reflects both the massive opportunity investors perceive in AI and the risk of a potential market bubble if growth expectations are not met.

Combined Big Tech AI spending is projected at $725 billion in 2026, with Microsoft, Google, Meta, and Amazon making unprecedented capital expenditures on AI infrastructure including data centers, specialized chips, and research talent. This level of investment is creating a virtuous cycle: more compute enables larger models, which enable new capabilities, which drive more adoption, which justifies more investment. The scale of this infrastructure build-out has significant implications for energy consumption, supply chains, and competitive dynamics.

Key Statistics and Data Points

Understanding the AI market requires diving deep into the quantitative metrics that define its scale, growth trajectory, and business impact. Here are the critical statistics that every business leader, investor, and technology decision-maker should internalize:

Market Size and Growth Metrics: The global AI market reached $434 billion in 2026, representing growth from $306 billion in 2025, a remarkable 42% year-over-year increase. By 2031, the market is projected to reach $2.5 trillion, representing a compound annual growth rate (CAGR) of 41.95% according to Mordor Intelligence. Alternative estimates from Grand View Research place the 2026 market at $391 billion, with projections approaching nearly $3.5 trillion by 2033. The generative AI segment alone stands at $63 billion in 2026, having grown from essentially zero just three years prior.

Enterprise Adoption Statistics: 88% of organizations now use AI in at least one business function, up from 78% in 2024 according to McKinsey’s comprehensive global survey. However, only 20% of EU enterprises with 10 or more employees have AI in actual production use, highlighting the significant gap between experimentation and deployment. 100% of industries are increasing AI usage according to PwC’s AI Jobs Barometer research. 35.49% of people now use AI tools every day according to Exploding Topics consumer research.

User and Consumer Statistics: Nearly 1.8 billion people have used some kind of AI tool globally, representing approximately 22% of the world’s population. 63% of AI users turn to the technology primarily for research and question-answering tasks. Cooking and meal planning is the top “life situation” AI use case according to detailed consumer surveys. The wearable AI market is expected to reach $303 billion by 2035 according to Vantage Market Research.

Investment and Venture Capital: Global venture funding in Q1 2026 reached approximately $300 billion, with AI capturing roughly 80% ($242 billion) of total investment according to Crunchbase. 55 US-based AI startups raised $100 million or more in 2025 according to TechCrunch analysis. Combined Big Tech AI spending is projected at $725 billion in 2026. AI services across major technology companies generated approximately $25 billion in revenue in 2025.

ROI and Business Impact: 79% of organizations reported measurable ROI from at least one AI initiative according to McKinsey’s 2025 survey. AI drives productivity gains across every industry with 99% of telecommunications respondents reporting productivity improvements according to NVIDIA’s State of AI report. AI increases annual revenue and drives down costs across all sectors according to cross-industry analysis. The median first-year ROI across AI workforce automation case studies is 124% according to PeopleStackHub research.

Infrastructure and Compute: NVIDIA controls approximately 81% of the AI data center chip market in 2026 according to IDC. AMD holds roughly 10% of the AI accelerator market with its MI300X chip. Data centers will require a $6.7 trillion investment by 2030 to match growing compute power needs according to industry projections. AI uses about 14% of global data center power currently, projected to grow to 27% by 2027. Global data center capacity is expected to double by 2030.

Chatbot and Consumer AI Market: ChatGPT’s share of global AI chatbot traffic dropped from 87% in January 2025 to 64-68% by January 2026 as competitors gained traction. The global AI chatbot market continues rapid expansion with new entrants like Claude, Gemini, and Perplexity gaining significant market share. Voice AI reportedly handles 19% of inbound contact-center volume in 2026 versus just 6% in 2024 according to Forrester research.

AI Talent and Workforce: Demand for AI talent continues to significantly outstrip supply, with AI engineer salaries increasing 35% year-over-year in major markets. 78% of enterprises globally are now embedding AI in at least one primary business function according to Stanford AI Index data. The World Economic Forum predicts AI will displace 85 million jobs by 2025 while creating 97 million new ones, representing a net positive but significant transition challenge.

Major Trends Shaping AI in 2026

The AI landscape in 2026 is defined by seven transformative trends that are fundamentally reshaping how organizations develop, deploy, and derive value from artificial intelligence. Understanding these trends is essential for any business leader looking to build sustainable competitive advantage through AI.

1. The Rise of Agentic AI Systems

The most significant trend in 2026 is the emergence of agentic AI, autonomous systems that can plan, execute multi-step tasks, and make decisions without constant human oversight. Unlike traditional AI tools that respond to individual prompts, agentic AI operates as an active workflow participant capable of handling complex enterprise processes from initiation through completion. These AI agents manage functions such as cloud cost optimization, security incident response, financial monitoring, supply chain coordination, and customer service without waiting for human prompts or intervention.

According to IBM’s 2026 tech trends report, agentic AI and other non-human identities will outnumber human users in organizations significantly within the coming years. Enterprises operating across multi-cloud and hybrid infrastructure setups increasingly rely on agentic AI to coordinate multiple AI agents responsible for cost management, performance optimization, security monitoring, and compliance enforcement simultaneously. This shift represents a fundamental transformation from AI as a passive productivity assistant to AI as an autonomous digital worker capable of independent action within defined guardrails.

2. Enterprise Production Deployment at Scale

The year 2026 marks a definitive inflection point when enterprises moved decisively from AI experimentation to production-grade deployments with real ROI expectations. According to IBM’s research, the most significant trend is the shift from AI excitement and experimentation to private, secure deployments with measurable business returns. The massive middle of the enterprise bell curve is finally moving from proof-of-concept to production-grade systems integrated into core business processes.

However, this transition remains challenging for most organizations. Only 5% of enterprises successfully move AI from pilot to sustained production according to BCG’s 2026 benchmark study. 42% of companies abandoned most of their AI initiatives in 2026, up dramatically from 17% in 2024 according to S&P Global Market Intelligence research. The primary bottleneck is organizational readiness, encompassing governance frameworks, employee training, data infrastructure, and most critically, the willingness to redesign business processes rather than simply bolt AI onto existing workflows.

3. Massive AI Infrastructure Investment

The infrastructure supporting AI has become a primary investment focus for technology companies and enterprises alike. Global AI spending is projected to reach $2 trillion in 2026, driven by investments in AI infrastructure, application software, and generative AI models according to Insight Global research. $5.2 trillion in AI infrastructure investment is expected through 2030 according to McKinsey analysis, representing one of the largest capital deployment cycles in technology history.

This infrastructure boom spans data centers, specialized AI chips, high-speed networking, and cloud computing resources. NVIDIA’s dominance in AI training chips, holding approximately 95% market share, is being actively challenged by AMD’s MI300X, custom silicon from Google (TPUs), Amazon (Trainium), and Microsoft (Maia). The competition in AI infrastructure is intensifying as major cloud providers race to build capacity sufficient to meet exploding demand.

4. Generative AI Integration into Enterprise Workflows

Generative AI has rapidly evolved from standalone chatbots to deeply embedded capabilities within enterprise software applications. From drafting contracts and generating software code to analyzing complex datasets and producing marketing content, generative AI is becoming invisible infrastructure woven throughout business applications. This integration trend means users increasingly interact with AI capabilities as a natural part of their workflow rather than consciously choosing to use a separate AI tool.

The generative AI market at $63 billion in 2026 is expected to grow at over 40% CAGR through 2030. Key enterprise applications include content creation at scale, software development assistance, document summarization and analysis, and creative design automation. Companies like Jasper, Copy.ai, and Grammarly have established strong positions in specific use cases, while Microsoft Copilot and Google Workspace AI bring powerful generative capabilities to billions of existing enterprise users.

5. Multi-Model Orchestration and AI Abstraction Layers

Enterprises are increasingly adopting sophisticated multi-model strategies rather than relying on a single AI provider for all use cases. Platforms like Not Diamond and open-source tools like LiteLLM enable organizations to intelligently route requests to the most appropriate model based on cost, performance, latency, and capability requirements. This trend is driving rapid commoditization of base model capabilities while significantly increasing the value of orchestration and abstraction layers.

API pricing for AI models has dropped dramatically over the past two years, with costs falling from $20-60 per million tokens in 2023 to $1-2 per million tokens in 2026 for many common use cases. This price compression is making advanced AI accessible to smaller businesses and startups while pressuring pure-play model providers to differentiate through unique capabilities, vertical specialization, or superior performance on specific tasks.

6. Edge AI and Distributed Intelligence

AI is rapidly moving from centralized cloud data centers to distributed edge devices. The wearable AI market is expected to reach $303 billion by 2035 according to Vantage Market Research. Smartphones, laptops, Internet of Things devices, and autonomous vehicles increasingly run sophisticated AI models locally, reducing latency, improving privacy, enabling offline operation, and reducing cloud computing costs.

This distributed AI architecture enables entirely new use cases from real-time language translation to fully autonomous driving, while reducing dependence on constant cloud connectivity. The AI chipsets market is projected to hit $931 billion by 2034 according to Precedence Research, reflecting massive demand for specialized silicon across the entire computing spectrum from data centers to edge devices.

7. AI Regulation and Governance Frameworks

As AI capabilities advance and deployment scales, regulatory frameworks are evolving rapidly across jurisdictions. The EU AI Act, implemented in phases through 2024-2026, establishes comprehensive risk-based categories for AI applications with corresponding compliance requirements. The United States has taken a more sectoral approach, with agencies including the FDA, FTC, SEC, and NIST developing AI guidance specific to their regulatory domains.

Enterprises are investing heavily in AI governance to ensure regulatory compliance, manage risk, and build stakeholder trust. Responsible AI frameworks increasingly focus on explainability, fairness, transparency, and meaningful human oversight. Companies that proactively address these governance concerns are finding competitive advantage as customers, partners, and regulators increasingly demand AI accountability and transparency.

Key Players and Competitive Landscape

The AI market features a complex, multi-layered competitive landscape spanning chip manufacturers, cloud infrastructure providers, foundation model developers, and application-layer companies. Understanding this ecosystem is crucial for identifying partnership opportunities, competitive threats, and investment prospects.

Infrastructure Layer: NVIDIA continues to dominate AI training with approximately 81-95% market share in AI data center chips according to IDC. The company posted $44.1 billion in Q1 FY2026 revenue, a remarkable 69% year-on-year jump, with data center sales making up 90% of total revenue. AMD represents the primary challenger with its MI300X accelerator capturing roughly 10% of the AI accelerator market. Major cloud providers including AWS, Google Cloud, and Microsoft Azure provide the compute infrastructure that powers the majority of AI workloads globally.

Foundation Model Providers: OpenAI maintains market leadership with a valuation of $182.6 billion and flagship products including GPT-5, ChatGPT, and DALL-E. The company has established strong enterprise traction with ChatGPT Enterprise and API services. Anthropic, valued at $60 billion, has differentiated through its focus on AI safety, constitutional AI approaches, and Claude models that have gained significant enterprise adoption. Google DeepMind combines Google’s research capabilities with DeepMind’s AI expertise, offering the Gemini model family and comprehensive enterprise AI services.

Big Tech AI Integration: Microsoft has deeply integrated AI across its entire product suite through its strategic partnership with OpenAI, offering Copilot capabilities in Office 365, Windows, GitHub, and Azure. The company is seeing 40-50% revenue growth annually through 2027 driven primarily by AI adoption. Google has responded aggressively with Gemini integration across Search, Workspace, and Cloud platforms. Meta continues investing heavily in open-source AI through its Llama model family while integrating AI capabilities across its social platforms. Amazon offers comprehensive AI services through AWS Bedrock and is developing proprietary models.

Emerging Players: The Forbes AI 50 list highlights innovative companies including ElevenLabs ($800M valuation) in voice generation technology, Midjourney in image generation, Gamma ($91M raised) in AI graphic design, and Notion ($330M raised) in AI-powered productivity software. Chinese companies like DeepSeek have emerged as significant global competitors, with DeepSeek-R1 demonstrating capabilities comparable to leading Western models at substantially lower cost.

Enterprise AI Startups: Glean raised $150 million at a $7.2 billion valuation for its enterprise AI search and knowledge management platform. Cursor (Anysphere) raised $900 million at a nearly $10 billion valuation for its AI coding assistant. Abridge reached a $5.3 billion valuation for its healthcare AI medical scribe technology. These extraordinary valuations reflect intense investor confidence in AI applications that deliver clear, measurable enterprise value.

AI Services and Consulting: Traditional management consultancies including McKinsey, Deloitte, Accenture, and BCG have built substantial AI practices helping enterprises with strategy development, implementation, and organizational change management. Specialized AI consultancies and system integrators are also thriving as enterprises seek external expertise to bridge the gap between AI potential and production deployment reality.

Challenges and Pain Points

Despite tremendous market growth and technology potential, organizations face significant challenges in realizing sustainable value from their AI investments. Understanding these pain points is essential for developing effective strategies to overcome them.

1. The Production Deployment Gap

The most significant challenge facing enterprises is successfully moving AI from pilot projects to production deployment. While 88% of organizations use AI in some form according to McKinsey, only 20% have achieved sustained production deployment according to Eurostat data. 42% of companies abandoned most of their AI initiatives in 2026, up significantly from 17% in 2024 according to S&P Global Market Intelligence. This gap between experimentation and industrialization represents billions in wasted investment and lost competitive opportunity.

The root causes include organizational resistance to change, lack of clear success metrics, insufficient data governance, and failure to redesign workflows around AI capabilities. Many organizations treat AI as a technical upgrade rather than a fundamental business transformation, leading to disappointing results and abandoned initiatives.

2. Data Quality and Management

Nearly 50% of organizations cite data accuracy concerns as a top barrier to AI adoption according to Kanerika research. Many organizations struggle with the quality of unstructured data, which is critical for successful AI implementation. Without strong data governance frameworks, AI models produce unreliable outputs, leading to user mistrust and low adoption rates.

Integration with outdated legacy systems is a common roadblock, often causing project delays and financial losses. Limited access to data due to internal organizational silos, on-premise systems with limited scalability, and insufficient training data all contribute to AI project failures.

3. Skills Gap and Talent Shortage

Most organizations lack the technical expertise required to implement and maintain AI systems effectively. The demand for AI talent far outstrips available supply, with companies competing aggressively for data scientists, ML engineers, AI product managers, and infrastructure specialists. This skills gap extends beyond technical roles to include AI-literate business leaders capable of identifying high-value use cases and managing AI-driven transformation.

The talent shortage is particularly acute for specialized roles like AI infrastructure engineers, MLOps specialists, and AI ethicists. Organizations are responding with aggressive upskilling programs, university partnerships, and increased reliance on AI service providers.

4. ROI Measurement and Value Demonstration

Only 25% of AI initiatives deliver expected returns according to Kanerika research, making budget approval difficult for subsequent projects. Traditional ROI measurement, focused solely on cost reduction or revenue lift, often fails to capture the broader value AI creates, including faster innovation, enhanced decision-making, improved customer experiences, and competitive differentiation.

Many AI projects lack defined success metrics from the outset, making it impossible to demonstrate value. The intangible benefits of AI, better decisions, faster innovation, improved employee experience, are real but difficult to quantify in traditional financial terms.

5. Security, Privacy, and Compliance Risks

AI systems handling sensitive data create serious compliance concerns, particularly under regulations like GDPR and the EU AI Act. Data privacy risks are a top barrier to AI adoption, especially in regulated industries like healthcare and financial services. The EU AI Act and similar emerging regulations impose significant compliance requirements on high-risk AI applications.

Security concerns include model inversion attacks, data poisoning, prompt injection vulnerabilities, and the risk of AI systems being used to generate convincing disinformation. Organizations must implement robust AI governance frameworks to manage these risks while still capturing AI’s transformative benefits.

Opportunities and Growth Strategies

Despite significant challenges, substantial opportunities exist for organizations that approach AI strategically and systematically. Here are the key growth strategies that successful enterprises are employing:

1. Focus on High-ROI Use Cases

Organizations achieving the highest returns focus relentlessly on use cases with clear, measurable business impact. Customer service automation, document processing, code generation, and predictive maintenance consistently deliver strong ROI across industries. AI forecasting, document automation, and productivity assistants reduce cost, errors, and manual workload at scale.

The most successful implementations start with narrowly scoped problems, build compliant data pipelines, select right-sized models, establish measurable ROI from day one, and create integration plans before choosing specific models. This disciplined approach separates successful AI deployments from failed experiments.

2. Build Strong Data Foundations

Long-term ROI depends on strong data foundations, integration readiness, governance frameworks, and continuous model tuning. Enterprises treating AI as an ongoing capability rather than a one-time deployment achieve more consistent and repeatable business impact.

Key investments include data pipeline engineering, enterprise data modernization, master data management, and data quality management. Organizations that get their data infrastructure in order before scaling AI see significantly better outcomes than those that rush to deploy models on messy, poorly governed data.

3. Develop AI Talent and Culture

Leading organizations develop AI skills across their entire workforce, not just within technical teams. This includes training business users to work effectively with AI tools, educating leaders on AI strategy and governance, and building internal AI centers of excellence.

Clear communication about AI’s role, transparency in AI decision-making, and inclusive implementation strategies reduce employee resistance. Organizations that treat AI as a tool to augment human capabilities rather than replace workers see higher adoption rates and better business outcomes.

4. Implement Phased Deployment

Rather than attempting enterprise-wide AI transformation simultaneously, successful organizations use phased deployment strategies. Start with pilot projects that can demonstrate value quickly, learn best practices while building internal capability, then scale to adjacent use cases and business units.

This approach allows organizations to build confidence, refine their AI governance frameworks, and demonstrate ROI before making larger investments. It also provides opportunities to course-correct based on early learnings.

5. Leverage AI Service Providers

For many organizations, partnering with experienced AI implementation partners accelerates time to value and reduces project risk. AI consulting projects deliver 15-40% cost reductions and 2-5x productivity gains according to industry benchmarks.

Partners can provide specialized expertise, proven methodologies, and accelerators that would take years to build internally. They also offer staffing flexibility for projects that do not justify permanent hires.

Case Studies and Success Stories

Real-world examples from leading organizations demonstrate how companies are capturing measurable value from AI investments:

Case Study 1: Nasdaq AI Platform

Nasdaq, one of the world’s premier stock exchanges and financial technology platforms, built a comprehensive AI platform to optimize its internal operations and enhance its external products. The implementation helped improve platform functionality and user experience while streamlining internal work processes. This demonstrates how financial services companies can leverage AI for both operational efficiency and product enhancement.

Case Study 2: Rachio Customer Support

Rachio, a smart sprinkler and irrigation company, successfully managed seasonal customer support surges for over one million users using AI-powered customer service automation. The implementation enabled high-quality support without proportionally inflating operational costs, demonstrating how AI can help businesses scale customer service efficiently during peak demand periods.

Case Study 3: Financial Services Compliance AI

A major financial services firm implemented compliance AI that required significant custom configuration but paid back the initial investment in just 3.2 months due to the high cost of compliance staff and the high volume of structured reviews required. This case illustrates how AI can deliver rapid ROI in high-value, document-intensive workflows common in regulated industries.

Case Study 4: Telecommunications Productivity Gains

In NVIDIA’s State of AI in Telecommunications report, 99% of respondents said AI helped improve employee productivity, with a quarter saying the technology provided a major or significant improvement. This cross-industry pattern demonstrates AI’s consistent ability to drive productivity when properly implemented and integrated into workflows.

Case Study 5:

AI-Native Customer Support

AI-native customer support deployments report average handle time under 3 minutes on automated tickets versus approximately 6 minutes for the industry average, representing a more than 50% reduction in ticket-level resolution time. Gartner cost benchmarks show $1.84 per self-service contact versus $13.50 per agent-assisted contact, representing a 7.3x cost advantage for automated support.

Future Outlook and Predictions

Looking ahead to 2027-2030, several key developments will fundamentally shape the AI market trajectory:

Market Growth Trajectory: The AI market is projected to reach $1.68 trillion by 2031 according to Statista, with a CAGR of 36.89%. More aggressive forecasts from Grand View Research suggest the market could approach $2.5-3.5 trillion by 2033. This growth will be driven by continued enterprise adoption, new application categories, and the emergence of AI-native businesses built entirely around artificial intelligence capabilities.

Technology Evolution: By 2027, agentic AI systems will move from early adoption to mainstream deployment, with AI agents handling complex multi-step workflows across industries. Multimodal AI, systems that can process and generate text, images, audio, and video seamlessly, will become standard. AI reasoning capabilities will continue to improve rapidly, with models like DeepSeek-R1 demonstrating the potential for AI systems that can think through complex problems step by step.

Infrastructure Investment: Data centers will require a $6.7 trillion investment by 2030 to match growing compute power needs according to JLL research. AI’s share of global data center power will grow from 14% currently to 27% by 2027. Global data center capacity is expected to double by 2030. This infrastructure build-out will enable new AI capabilities while creating challenges around energy consumption, sustainability, and resource allocation.

Regulatory Environment: AI regulation will mature significantly, with the EU AI Act serving as a template for other jurisdictions worldwide. Organizations will need to invest substantially in AI governance, explainability, and compliance. Companies that proactively address these requirements will find competitive advantage in an increasingly regulated environment.

Workforce Transformation: AI will significantly reshape the global workforce, with some roles being automated while entirely new categories of roles emerge. The World Economic Forum predicts AI will displace 85 million jobs by 2025 while creating 97 million new ones, representing a net positive but significant transition challenge for affected workers and industries.

Market Consolidation: The AI market will likely see significant consolidation as winners emerge in key categories. High valuations for AI startups assume continued rapid growth; any significant slowdown could trigger market correction. The infrastructure layer may consolidate around a few major players, while the application layer remains more fragmented with vertical-specific solutions.

Key Takeaways

- The global AI market reached $434 billion in 2026 and is projected to grow to $2.5 trillion by 2031 at a 42% CAGR

- 88% of organizations now use AI, but only 20% have achieved sustained production deployment, revealing a significant deployment gap

- Agentic AI represents the most significant trend, with autonomous AI agents moving from experimentation to enterprise workflows

- NVIDIA dominates AI infrastructure with 81% market share, while OpenAI ($182.6B valuation) and Anthropic ($60B) lead foundation models

- AI captured 80% of global venture funding in Q1 2026 ($242 billion), reflecting massive investor confidence

- Organizations achieving the highest ROI focus on narrowly scoped use cases with clear metrics and strong data foundations

- The primary challenges are production deployment, data quality, skills gaps, and demonstrating measurable ROI

- By 2030, AI will require $6.7 trillion in data center investment and consume 27% of global data center power

Sources and Citations

- Mordor Intelligence – Artificial Intelligence Market Size and Share Analysis (2026-2031)

- Grand View Research – Artificial Intelligence Market Size Report 2026

- McKinsey Global Survey – The State of AI in 2025

- Exploding Topics – 45+ Artificial Intelligence Statistics (January 2026)

- Statista – Artificial Intelligence Worldwide Market Forecast

- Crunchbase – Q1 2026 Venture Funding Report

- IBM Think – AI Tech Trends Predictions 2026

- PwC – 2026 AI Performance Study

- Deloitte – State of AI in the Enterprise 2026

- NVIDIA Blog – State of AI Report 2026

- Forbes AI 50 List 2026

- TechCrunch – AI Startup Funding Analysis 2025-2026

- BCG – AI Benchmark Study 2026

- Gartner – AI Customer Service Statistics 2026

- Insight Global – AI Industry Growth Impact 2026

- Precedence Research – Artificial Intelligence Market Analysis

- S&P Global Market Intelligence – Enterprise AI Adoption Survey

- Eurostat – EU Enterprise AI Usage Statistics

Research conducted May 31, 2026. Market data reflects the most recent available reports and industry analyses. All figures are based on publicly available research from reputable sources.

The artificial intelligence market in 2026 represents a pivotal moment in technology history. With $434 billion in global market value and projections reaching $2.5 trillion by 2031, AI has transitioned from experimental technology to essential business infrastructure. The organizations that successfully navigate the challenges of production deployment, data governance, and organizational change management will capture disproportionate value in their respective markets. Those that fail to make this transition risk being left behind as competitors leverage AI to deliver superior customer experiences, operate more efficiently, and innovate faster. The data is clear: AI is no longer optional—it is the foundation of competitive advantage in the modern economy.

For business leaders evaluating AI strategy, the path forward requires clear-eyed assessment of organizational readiness, disciplined focus on high-ROI use cases, and sustained commitment to building the data foundations and talent required for success. The window for early mover advantage is closing rapidly as AI capabilities become commoditized. The question is no longer whether to invest in AI, but how quickly organizations can transform AI potential into production reality. The next five years will determine which companies emerge as leaders in the AI-powered economy—and which become cautionary tales of missed opportunity.