SaaS Market: The Complete 2026 Market Analysis with Data, Trends & Predictions

The global Software as a Service market hit $408.21 billion in 2025. Think about that number for a second. A decade ago, SaaS was a niche delivery model for a handful of applications. Today, it represents the dominant way businesses consume software. Precedence Research projects the market will reach $465.03 billion in 2026, and every major analyst firm agrees we’re on a trajectory toward a trillion-dollar market before 2035.

In my analysis of the data, what’s striking isn’t just the raw growth—it’s the transformation happening beneath the surface. AI-native architectures are replacing bolt-on features. Usage-based pricing is challenging traditional subscription models. Vertical SaaS is eating horizontal software’s lunch. And after years of unchecked sprawl, organizations are finally getting serious about SaaS management.

This article breaks down the complete picture: market size and growth trajectories, adoption patterns across company sizes, the seven trends reshaping competitive dynamics, key players and their strategies, and where the market heads through 2030. I’ve pulled data from Precedence Research, Fortune Business Insights, Gartner, McKinsey, and dozens of industry sources to give you actionable intelligence you can use whether you’re building, buying, or investing in SaaS.

Market Overview: The $408 Billion Ecosystem

Current Market Size and Growth Trajectory

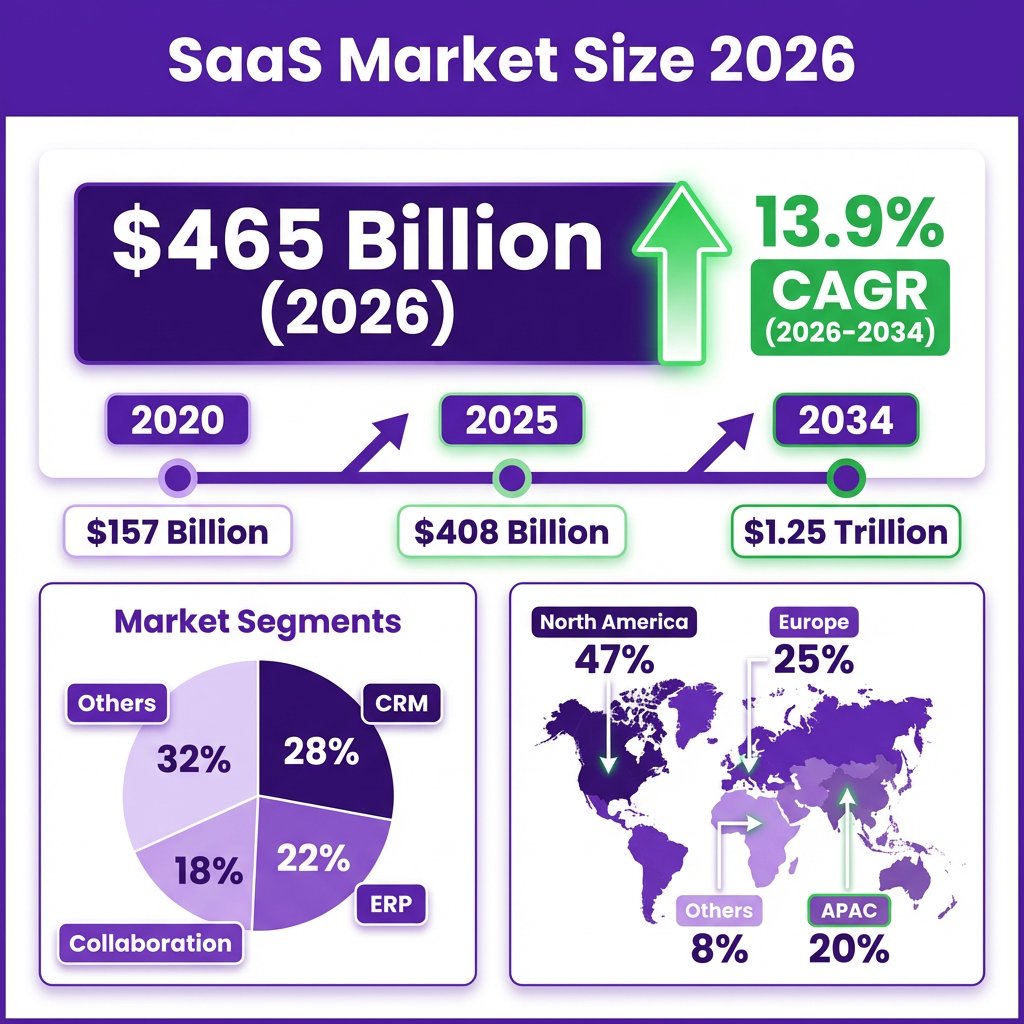

The SaaS market has evolved into a massive economic force. According to Precedence Research, the global market reached $408.21 billion in 2025 and is projected to hit $465.03 billion in 2026. That’s a 13.9% year-over-year jump—faster than overall IT spending growth of 8%.

Other research firms offer slightly different figures based on methodology. Fortune Business Insights uses a tighter SaaS-specific definition, placing the 2025 market at $315.68 billion with projections reaching $1.48 trillion by 2032 at an 18.7% CAGR. Statista sits in the middle at $390.50 billion for 2025, projecting $793.10 billion by 2029. The gap between these estimates comes down to scope—some analysts count broader cloud-delivered application services while others stick to pure SaaS definitions. The direction is identical regardless of methodology: sustained double-digit growth for the foreseeable future.

The long-term trajectory points to a $1.25 trillion market by 2034 according to Hostinger’s analysis, representing a compound annual growth rate of roughly 13%. This isn’t speculative fantasy—it’s based on the fundamental shift of enterprise software consumption from on-premise perpetual licenses to cloud-based subscriptions.

[GRAPH: Global SaaS Market Size 2020-2034 showing historical growth from $157B in 2020 to projected $1.25T in 2034, with key milestones marked for 2025 ($408B), 2026 ($465B), 2029 ($793B), and 2034 ($1.25T)]

Regional Distribution: North America Dominates, APAC Accelerates

Geographic distribution tells a clear story of market maturity and emerging opportunity. North America accounts for 46.9% of global SaaS revenue, with the United States alone hosting roughly 17,000 SaaS companies. The U.S. market is projected to generate $141.06 billion in SaaS revenue in 2026 and exceed $412 billion by 2034.

U.S.-based SaaS providers serve an estimated 14 billion users worldwide, demonstrating the sector’s global reach. This vast user base enables faster innovation cycles through diverse feedback and data collection.

Europe holds approximately 25% of the global market, with Germany’s SaaS market expected to reach €16.3 billion in 2025. The region shows strong adoption across enterprise resource planning, customer relationship management, and collaboration tools.

Asia-Pacific is where growth is fastest. India’s SaaS companies have grown at a 24% compound annual rate since FY2019, and the country now boasts 250 companies with $10 million or more in annual recurring revenue. Private equity investment in Indian SaaS hit $1.38 billion in the first seven months of 2025, up sharply from $833 million across all of 2024. This isn’t just outsourcing anymore—Indian SaaS companies are building global products from day one.

Market Segments: Where the Money Flows

The SaaS market breaks down into distinct segments with varying growth rates and competitive dynamics. Customer Relationship Management (CRM) remains the largest segment, with Salesforce maintaining dominant market share. Enterprise Resource Planning (ERP) follows closely, though legacy vendors like SAP and Oracle are racing to transition cloud-native competitors.

Collaboration and communication tools saw explosive growth during remote work adoption and have maintained elevated usage levels. Content, collaboration, and communication applications represent one of the fastest-growing segments as hybrid work becomes permanent.

Human Capital Management (HCM) SaaS continues expanding as organizations prioritize talent acquisition and retention. Business Intelligence and Analytics platforms are experiencing renewed growth driven by AI integration and self-service capabilities.

The healthcare SaaS segment deserves special mention—projected to reach $452.4 billion by 2029 with a CAGR of approximately 26%. Regulatory complexity and the need for interoperability are driving healthcare organizations toward specialized cloud solutions.

Key Statistics and Data: The Numbers That Matter

Adoption Rates: Saturation and Consolidation

SaaS adoption has reached near-universal levels. 99% of organizations now use at least one SaaS application. This isn’t early-adopter territory anymore—it’s the standard operating model for businesses of every size.

The average company runs 106 SaaS applications in 2024, down from 112 in 2023. This consolidation rate has slowed from 14% year-over-year to just 5%, suggesting organizations have trimmed obvious redundancies and now face tougher decisions about which tools truly deliver value.

Scale changes everything. Large enterprises with 10,000+ employees run an average of 473 SaaS applications. Managing this complexity has become a full-time job—literally. The rise of SaaS Management Platforms (SMPs) is a direct response to this sprawl.

Automation adoption is widespread: 81% of organizations have automated at least one business process using SaaS applications. This reduces repetitive manual tasks, improves accuracy, and helps companies manage complex SaaS environments more efficiently.

[GRAPH: SaaS Applications per Company by Size showing SMBs at 35 apps, Mid-market at 89 apps, Enterprise at 187 apps, and Large Enterprise at 473 apps]

Spending Patterns: Growth with Waste

Enterprise SaaS spending tells a story of aggressive investment paired with shocking inefficiency. The average enterprise now spends $52 million per year on SaaS, up from $45 million in 2024. SaaS spending grew 18% year-over-year from 2024 to 2025, outpacing overall IT spending growth.

SaaS now accounts for 70% of total software budgets, up from 55% in 2020. This shift reflects both new SaaS adoption and the migration of existing on-premise software to cloud delivery models.

Here’s the uncomfortable truth: 50% of purchased SaaS licenses go unused. The average enterprise loses roughly $18 million per year on licenses nobody touches. This waste represents both a cost management opportunity and a competitive threat to SaaS vendors who can’t demonstrate clear ROI.

Shadow IT compounds the problem. 30% to 40% of IT spending in large organizations happens outside official channels. Business units purchase SaaS tools with credit cards, bypassing procurement and security review. This creates governance gaps and security vulnerabilities that keep CISOs awake at night.

AI Integration: The Transformation Accelerator

Artificial intelligence isn’t coming to SaaS—it’s already here. 95% of organizations are expected to use AI-powered SaaS applications by 2025. A McKinsey report found that 78% of organizations already use some form of analytical AI.

Gartner predicts more than 80% of companies will have AI-enabled applications deployed by the end of 2026—up from just 5% in 2023. This represents one of the fastest technology adoption curves in business history.

The average organization currently uses 7.3 SaaS apps with AI functionality. 45% use AI in IT service management SaaS applications. Agentic AI technologies reduce customer support handling time by 52%, saving companies hundreds of thousands of work hours.

AI infrastructure software is projected to reach $230 billion in 2026, up from $60 billion in 2024. The AI-created SaaS market alone is expected to hit $770 billion by 2031 at a 40.2% CAGR—triple the growth rate of traditional SaaS.

AI software revenue has grown from $9.5 billion in 2018 to $118.6 billion in 2025. CIOs report an average 8.9% cost increase on existing IT products as vendors bake generative AI features into standard offerings.

[GRAPH: AI Integration in SaaS showing adoption curve from 5% in 2023 to projected 80%+ by end of 2026, with key milestones and AI software revenue growth]

Major Trends Shaping the Market in 2026

Trend 1: AI-Native SaaS Becomes the Default

The conversation has shifted from “SaaS with AI features” to “AI-native SaaS.” In 2026, AI isn’t a bolt-on—it’s the foundation. AI-native platforms embed intelligence into core workflows rather than treating it as an add-on capability.

This shift shows in valuations. SaaS companies with AI at their core command 12.5x EV:Revenue multiples compared to lower multiples for legacy platforms. Investors recognize that AI-native architecture creates sustainable competitive advantages through data moats and workflow integration.

The practical impact? AI-driven workflows that span multiple SaaS tools. Predictive analytics that surface insights before users ask. Natural language interfaces that eliminate complex navigation. Companies building on AI-native foundations will dominate the next decade.

Trend 2: Vertical SaaS Deepens Domain Advantage

Horizontal SaaS—tools designed for broad use across industries—faces increasing pressure from vertical specialists. Industry-specific solutions deliver measurable outcomes that generic tools cannot match.

Vertical SaaS is often more profitable because it allows for deeper integration and specialized AI features. A construction management platform understands job site workflows. A dental practice software knows insurance coding. These domain-specific advantages create stickier products and higher switching costs.

Micro SaaS startups are capitalizing on this trend, often achieving profit margins up to 80% thanks to low overhead and specialized focus. The best vertical SaaS companies build data moats through proprietary industry datasets that generalist competitors cannot access.

Trend 3: Usage-Based and Consumption Pricing Models

The subscription economy is evolving. Pure seat-based pricing is giving way to usage-based and consumption models that align vendor success with customer value realization.

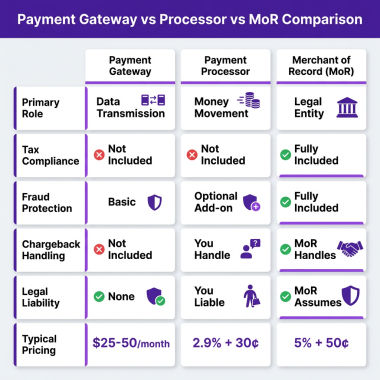

IDC data suggests usage-based pricing is now preferred by SaaS buyers. Companies want to pay for what they use, not for theoretical maximum capacity. This shift requires sophisticated billing infrastructure—precisely why companies like Fungies.io see growing demand for flexible payment solutions.

Expansion ARR now represents 40% of new ARR overall, and over 50% for companies above $50M ARR. This land-and-expand strategy depends on usage-based pricing that grows with customer success.

Trend 4: SaaS Management Platforms Become Critical Infrastructure

SaaS sprawl has created a governance crisis. The response? SaaS Management Platforms (SMPs) that provide visibility, control, and optimization across the entire software portfolio.

70%+ of organizations will centralize SaaS application management using an SMP by 2028, up from less than 30% in 2025. 50% of organizations will adopt SMPs with AI governance features by 2027.

The business case is compelling. 93% of organizations using SMPs find the primary benefit is increased organizational productivity. 65% say their SMP is critical to SaaS file and data security. 85% of organizations automate some SaaS management processes.

Trend 5: API-First and Composable Architectures

SaaS is shifting from isolated applications to composable systems built on shared data foundations. API-first design enables integration, automation, and custom workflow creation.

Standards like MCP (Model Context Protocol) are emerging to enable AI agents to interact with multiple SaaS tools through a single interface. A single AI interface becomes the primary way employees interact with dozens of SaaS applications.

This composability creates both opportunities and challenges. Vendors must decide between open ecosystems that drive adoption and closed platforms that capture more value. The winners will balance both.

Trend 6: Enhanced Security and Compliance Requirements

As SaaS becomes mission-critical, security expectations have escalated. Cloud and SaaS security risks are rising in 2026 as trust and outages collide.

Ransomware groups now target platforms like Microsoft 365 directly, using cloud footholds to pivot into on-premise environments. Third-party SaaS supply chains have become primary entry points for breaches as attackers exploit integration webs that organizations struggle to inventory.

Regulatory pressure compounds the challenge. GDPR, CCPA, and industry-specific regulations require rigorous data governance. 62% of organizations cite lack of data governance as the primary data challenge inhibiting their AI initiatives.

Trend 7: Data-as-a-Service Integration

SaaS companies are increasingly bundling data with software. Data-as-a-Service (DaaS) offerings provide pre-cleaned, continuously updated datasets through APIs that accelerate reporting and support machine learning initiatives.

This trend blurs the line between software and data providers. The most valuable SaaS companies combine workflow tools with proprietary datasets that improve through usage. This data moat creates defensibility that pure workflow tools cannot match.

Key Players and Competitive Landscape

The Dominant Giants

Salesforce remains the largest pure-play SaaS company with a market capitalization of $161.4 billion. That’s larger than Atlassian ($33.3 billion), the fifth-largest company on the list. Salesforce’s ecosystem approach—combining CRM with marketing automation, analytics, and platform capabilities—has created switching costs that competitors struggle to overcome.

Microsoft leads the broader SaaS market through Microsoft 365, Azure Cloud Services, and Dynamics 365. Their bundling strategy and enterprise relationships make them the default choice for many organizations.

The top 50 largest SaaS companies have seen their median value increase by 179% over the past year to $21.5 billion. This concentration of value reflects the winner-take-most dynamics of SaaS markets.

Major Public SaaS Companies

Beyond Salesforce, the public SaaS landscape includes:

- Adobe: Transformed from perpetual license software to cloud subscriptions, maintaining market leadership in creative tools

- Atlassian: Product-led growth pioneer with Jira and Confluence dominating developer and project management markets

- DocuSign: Agreement Cloud platform with expanding workflow capabilities beyond e-signatures

- HubSpot: Marketing automation and CRM for mid-market companies

- Slack: Workplace collaboration (now part of Salesforce)

- Zoom: Video communications that became essential infrastructure

- ServiceNow: Enterprise workflow platform with expanding ITSM dominance

- Workday: Human capital management and financial management

- Snowflake: Data cloud platform enabling modern analytics

- Datadog: Cloud monitoring and observability

Emerging Players and Regional Champions

India has emerged as a SaaS powerhouse with 250 companies exceeding $10 million ARR. Companies like Zoho, Freshworks, and BrowserStack have built global businesses from Indian foundations. These aren’t cost arbitrage plays—they’re product companies competing on features and user experience.

Europe’s SaaS ecosystem continues maturing with strong players in fintech, compliance, and privacy-focused tools. GDPR created competitive advantages for European SaaS companies serving global markets.

Competitive Dynamics and Valuation Metrics

The median year-over-year revenue growth rate for SaaS companies is now 16-17%, the lowest since 2014. This is far from the +30% YoY growth that fueled higher multiples in previous years. 80% of SaaS companies are growing less than 20%.

This growth deceleration reflects market maturity and the post-COVID normalization of digital spending. It also creates pressure on valuations and increases the importance of capital efficiency.

[IMAGE: Competitive landscape visualization showing major SaaS companies by market cap and growth rate quadrant]

Challenges and Pain Points

SaaS Sprawl and Shadow IT

The proliferation of SaaS applications has created a management nightmare. Organizations struggle to maintain visibility into what software employees use, how much it costs, and what security risks it creates.

Shadow IT—software purchased outside official procurement channels—represents 30% to 40% of IT spending in large organizations. Business units buy tools with credit cards, bypassing security review and integration planning. This creates governance gaps that compound over time.

The consolidation rate has slowed to just 5% year-over-year, suggesting organizations have picked the low-hanging fruit and now face difficult decisions about entrenched tools with sticky workflows.

Rising Customer Acquisition Costs

On average, SaaS companies spend $2.00 in sales and marketing to acquire $1.00 of new customer revenue. This CAC intensity reflects competitive markets and longer sales cycles for enterprise deals.

VC-backed companies invest 47% of revenue in sales and marketing compared to 33% for PE-backed firms. This growth-at-all-costs approach faces increasing scrutiny as capital efficiency becomes a priority.

The New CAC Ratio for new customers rose 14% higher in 2024, while blended CAC ratios declined 10% due to increased expansion ARR. This suggests companies are focusing more on growing existing customers than acquiring new ones.

Security Vulnerabilities and Supply Chain Risk

Cloud-native intrusions are rising, with ransomware groups targeting SaaS platforms directly. Supply-chain-style attacks exploit the sprawling web of integrations that most organizations struggle to inventory.

An attacker now just needs to hit one small vendor connected to a thousand other environments to create massive impact at relatively low risk. Many SaaS providers still treat security as a premium feature rather than table stakes.

AI Governance Gaps

62% of organizations cite lack of data governance as the primary data challenge inhibiting their AI initiatives. Organizations adopted AI, analytics, and cloud platforms before modernizing their data foundations.

This governance gap blocks AI value creation and creates compliance risks. Companies that invest in data governance early create foundations that support AI, compliance, and long-term growth.

How Leading Companies Are Addressing These Challenges

Forward-thinking organizations are implementing SaaS Management Platforms to gain visibility and control. They’re establishing SaaS procurement policies that balance business unit autonomy with security requirements. And they’re investing in data governance frameworks that enable AI while managing risk.

The most sophisticated companies treat SaaS management as a strategic capability, not an administrative burden. They recognize that controlling software spend and risk is as important as controlling any other major cost category.

Opportunities and Growth Strategies

Product-Led Growth (PLG)

Product-led growth lets the product itself drive acquisition, expansion, and retention. Users try before they buy, experience value immediately, and spread the product through their organizations.

Atlassian pioneered this approach with low-friction trials and transparent pricing. The model works because it aligns vendor incentives with customer success—vendors only grow when users actually adopt and benefit from the product.

PLG requires different capabilities than traditional sales-led growth: self-serve onboarding, in-product guidance, and usage-based pricing that scales with value realization.

Vertical Specialization

Horizontal SaaS faces commoditization pressure. Vertical SaaS—industry-specific solutions—commands premium pricing and higher retention through domain expertise.

The strategy requires deep customer understanding and willingness to serve narrower markets. But the rewards include higher switching costs, less competition, and clearer value propositions.

Vertical SaaS companies should build data moats through proprietary industry datasets. This creates defensibility that pure workflow tools cannot match against AI-powered competitors.

AI-Driven Expansion

AI creates opportunities for SaaS companies to expand into adjacent workflows. A project management tool can add resource planning. A CRM can add sales intelligence. An accounting platform can add financial analytics.

The key is using AI to deliver value that would have required separate tools. This consolidation play increases customer lifetime value while reducing competitive threats.

Companies should budget for data readiness, orchestration layers, and operational reliability before investing in new AI features. AI at scale requires production-grade infrastructure, not experimental prototypes.

Usage-Based Pricing Optimization

Usage-based pricing aligns vendor success with customer value realization. It reduces friction for initial adoption and creates natural expansion as customers grow.

Implementing usage-based pricing requires sophisticated billing infrastructure and clear value metrics. Companies need to identify which usage dimensions correlate with customer success and price accordingly.

The expansion ARR data is compelling: 40% of new ARR comes from existing customer expansion, rising to over 50% for larger companies. Usage-based pricing is the engine driving this growth.

Actionable Strategies for SaaS Founders

- Build AI-native from the ground up, not as a bolt-on feature. Architecture decisions made today will determine competitive position for the next decade.

- Focus on vertical markets where domain expertise creates defensibility. Horizontal plays face increasing pressure from AI commoditization.

- Implement usage-based pricing that grows with customer success. This aligns incentives and creates natural expansion.

- Invest in data governance early to enable AI initiatives and compliance. Data infrastructure is a strategic asset.

- Create workflow integration stickiness through APIs and ecosystem partnerships. The more integrated your product, the harder it is to replace.

- Build data moats through proprietary datasets that improve with usage. This creates sustainable competitive advantages.

Case Studies and Success Stories

Case Study 1: Salesforce — CRM Dominance Through Ecosystem

Salesforce pioneered SaaS CRM and has maintained market leadership through relentless expansion. The company quickly gained more than 3 million customers by building a user-friendly product that integrated easily with existing software platforms.

The key lesson: ecosystem strategy wins. Salesforce built an app marketplace, platform capabilities, and integration tools that made their product stickier over time. Each new integration increased switching costs and deepened customer relationships.

Salesforce’s acquisition strategy—buying complementary tools like Slack, Tableau, and MuleSoft—created a comprehensive platform that competitors struggle to match. The company shows how SaaS winners expand from single products to integrated suites.

Case Study 2: Atlassian — Product-Led Growth Mastery

Atlassian built a $33+ billion company with minimal traditional sales investment. Their product-led growth strategy let developers discover, try, and adopt tools like Jira and Confluence without sales intervention.

The company partnered with peer companies to drive cross-product integrations that made products stickier and widened the customer base. This ecosystem approach created network effects that reinforced market position.

Atlassian demonstrates that PLG works for enterprise software when the product delivers immediate value and transparent pricing removes friction. Their success inspired a generation of SaaS founders to lead with product rather than sales.

Case Study 3: Indian SaaS Unicorns — Global from Day One

Indian SaaS companies like Zoho, Freshworks, and BrowserStack prove that world-class products can emerge from anywhere. These companies built global businesses by focusing on product quality and customer success rather than geographic arbitrage.

Freshworks reached unicorn status by building a comprehensive customer engagement platform that competes directly with Salesforce and Zendesk. Zoho created an integrated suite of business applications that rivals Microsoft and Google.

The lesson: product-market fit matters more than location. These companies succeeded by obsessing over customers, disrupting established markets, and expanding their total addressable market through relentless innovation.

Future Outlook and Predictions

2026-2027 Near-Term Outlook

The next 18 months will see AI-native SaaS become the default expectation. Vendors that treat AI as an afterthought will face churn and procurement friction. Companies that provide granular visibility and AI safety controls will win enterprise contracts.

Consolidation will accelerate as organizations rationalize their SaaS portfolios. SMP adoption will grow rapidly as governance requirements become non-negotiable. Usage-based pricing will become standard for infrastructure and platform services.

Growth rates will remain under pressure as markets mature. The 16-17% median growth of 2026 may decline further as companies optimize spending and competitive intensity increases.

2028-2030 Medium-Term Projections

By 2028, 70%+ of organizations will centralize SaaS management using an SMP. AI governance will be standard, not optional. The market will reach approximately $700-800 billion depending on analyst methodology.

Vertical SaaS will capture increasing share from horizontal platforms. Industry-specific solutions with AI capabilities will dominate specialized workflows. The winners will combine domain expertise with AI-native architectures.

API-first platforms will enable new categories of composable applications. Standards like MCP will let AI agents orchestrate complex workflows across multiple SaaS tools. This creates both opportunities for integration specialists and threats to point solutions.

Long-Term Forecast Through 2034

The global SaaS market will reach $1.25 trillion by 2034 according to current projections. This represents a 13% CAGR from 2026 levels—slower than historical growth but from a much larger base.

AI-created SaaS will be a distinct category worth $770 billion by 2031. Traditional SaaS will face commoditization pressure while AI-native platforms capture premium valuations.

The distinction between SaaS and other software delivery models will blur. Edge computing, hybrid cloud, and AI agents will create new architectural patterns that don’t fit current categories.

Risks to Watch

AI commoditization threatens SaaS revenues through pricing pressure and reduced upsell attach rates. If AI makes it easy to build software, existing SaaS companies face disruption from AI-generated alternatives.

Economic downturn would accelerate SaaS consolidation as organizations cut discretionary spending. The 18% YoY growth of 2025 could reverse quickly if recession hits.

Regulatory fragmentation creates compliance complexity for global SaaS vendors. Data localization requirements, AI regulations, and industry-specific rules increase operational costs.

Security breaches at major SaaS providers could damage trust in cloud delivery models. Supply chain attacks exploiting SaaS integrations represent systemic risk.

Key Takeaways

After analyzing the data, trends, and competitive dynamics, here are the essential insights:

- The SaaS market reached $408 billion in 2025 and is projected to hit $465 billion in 2026, with trillion-dollar scale expected before 2035.

- AI-native architecture is becoming table stakes. Companies treating AI as a bolt-on feature will lose to competitors building intelligence into core workflows.

- Vertical SaaS outperforms horizontal through domain expertise, data moats, and specialized AI capabilities that generic tools cannot match.

- Usage-based pricing drives expansion revenue, which now represents 40% of new ARR and over 50% for larger companies.

- SaaS Management Platforms are critical infrastructure as organizations struggle with sprawl, waste, and governance across hundreds of applications.

- Customer acquisition costs are rising while growth rates decline, making capital efficiency and product-led growth essential strategies.

- Security and compliance are competitive differentiators as organizations face increasing threats and regulatory requirements.

The SaaS market in 2026 is simultaneously mature and rapidly evolving. The basic model—cloud delivery of software via subscription—is now standard. But AI integration, pricing innovation, and vertical specialization are creating new opportunities for differentiation and growth.

For SaaS founders, the message is clear: build AI-native, focus on vertical markets or unique data advantages, implement usage-based pricing, and treat security as a core feature. The companies that master these elements will define the next decade of software.

For buyers, the imperative is governance. With 99% adoption and average deployments of 106+ applications, unmanaged SaaS sprawl creates massive cost and risk. SMPs and procurement discipline are no longer optional.

The data tells a story of transformation. SaaS isn’t just how software is delivered anymore—it’s how business gets done. The companies that recognize this shift and adapt their strategies accordingly will thrive in the trillion-dollar market ahead.

Sources and Citations

This analysis draws on data from the following sources:

- Precedence Research — Global SaaS market size projections and growth forecasts. https://www.quantumrun.com/consulting/saas-industry-growth-statistics/

- Fortune Business Insights — SaaS market segmentation and regional analysis. https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222

- Grand View Research — Global SaaS market size estimated at $399.10 billion in 2024, projected $819.23 billion by 2030. https://www.grandviewresearch.com/industry-analysis/saas-market-report

- Hostinger — SaaS statistics for 2026 including adoption rates and growth projections. https://www.hostinger.com/tutorials/saas-statistics

- BetterCloud — 147 SaaS statistics covering management, security, and AI integration. https://www.bettercloud.com/monitor/saas-statistics/

- Gartner — IT spending forecasts and AI adoption predictions. https://www.gartner.com/

- McKinsey — AI adoption statistics and organizational usage patterns. https://www.mckinsey.com/

- Statista — Worldwide SaaS revenue projections and market data. https://www.statista.com/

- Zylo — SaaS spending benchmarks and management statistics. https://zylo.com/blog/saas-statistics/

- Vena Solutions — 85 SaaS statistics, trends and benchmarks for 2026. https://www.venasolutions.com/blog/saas-statistics

- Benchmarkit — 2025 SaaS performance metrics and growth benchmarks. https://www.benchmarkit.ai/2025benchmarks

- Phoenix Strategy Group — SaaS KPI benchmarks and industry standards. https://www.phoenixstrategy.group/blog/benchmarking-saas-kpis-industry-standards-2026

- Cyclr — 7 SaaS predictions for 2026 including AI-native platforms. https://cyclr.com/resources/ai/7-saas-predictions-for-2026-the-year-ai-native-platforms-go-mainstream

- Ardas IT — SaaS 2026 trends from AI experiments to production-ready platforms. https://ardas-it.com/saas-2026-trends-from-ai-experiments-to-production-ready-platforms

- Tridens Technology — Top 6 SaaS industry trends for 2026. https://tridenstechnology.com/saas-trends/

- Custify — Future of SaaS trends and predictions. https://www.custify.com/blog/future-of-saas-trends-and-predictions-2024/

- LBMC — 2026 Technology & SaaS outlook. https://www.lbmc.com/blog/business-outlook-trends-in-technology/

- Ken Research — US SaaS market outlook to 2030. https://www.kenresearch.com/industry-reports/us-saas-market-outlook-to-2028

- Mike Sonders — The 50 biggest SaaS companies in the U.S. https://www.mikesonders.com/largest-saas-companies/

- <