The artificial intelligence market has reached an inflection point in 2026. With global revenues hitting $3.09 trillion this year, AI has evolved from an experimental technology to the primary engine driving global economic growth. What started as research projects in academic labs has transformed into an industry that’s reshaping every sector of the economy—from healthcare and finance to manufacturing and entertainment.

This isn’t just another technology cycle. The AI market’s 50.16% compound annual growth rate between 2026 and 2030 represents one of the fastest expansions in modern economic history. To put this in perspective: the AI market grew more in the past 12 months than the entire global software industry grew during the dot-com boom of the late 1990s.

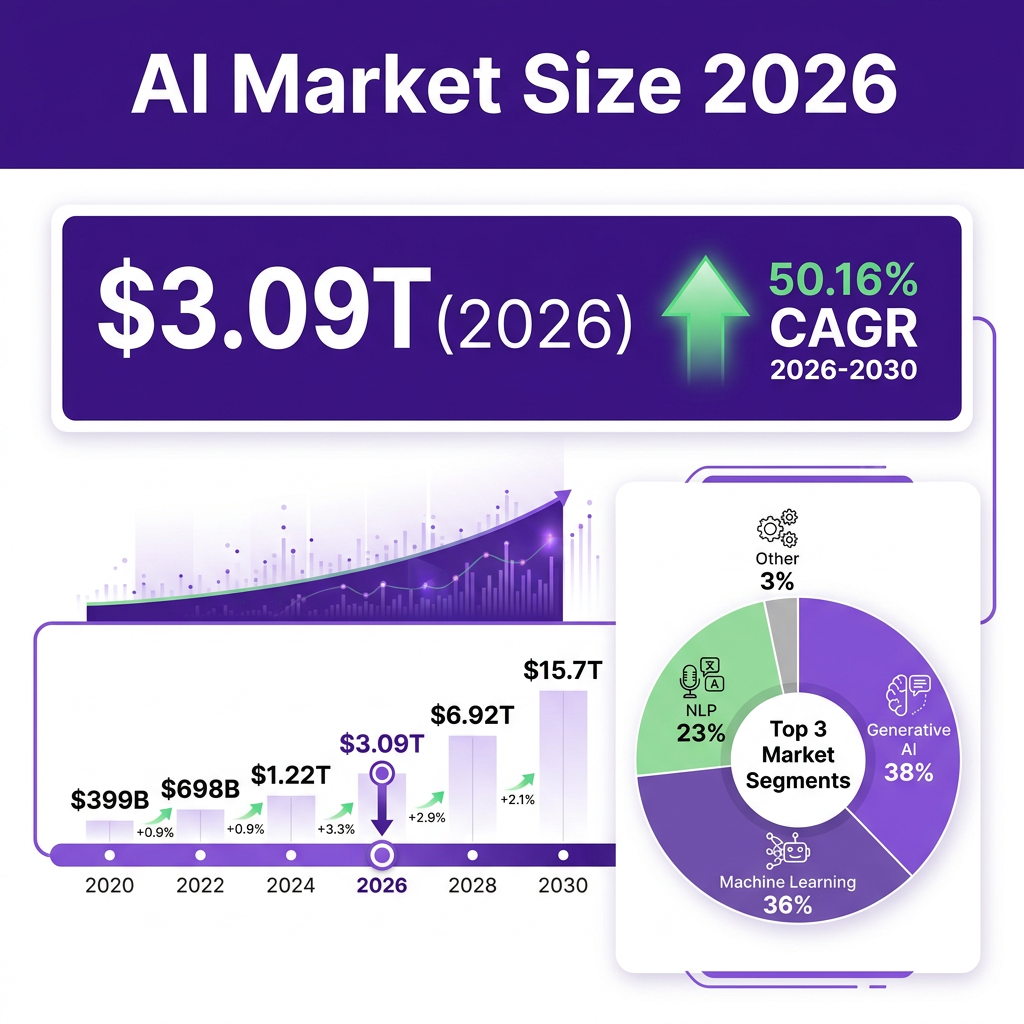

Market Overview: The $3.09 Trillion AI Ecosystem

The global AI market has experienced unprecedented expansion, growing from $1.06 trillion in 2020 to $3.09 trillion in 2026. This represents a compound annual growth rate that dwarfs virtually every other technology sector in history. The journey hasn’t been linear—market volatility in 2022 and 2023 saw temporary contractions as the industry digested early hype and recalibrated toward sustainable business models.

According to Statista’s comprehensive market forecast, the AI industry’s revenue trajectory shows remarkable momentum. In 2024, the market reached $1.20 trillion, representing a 95.84% year-over-year increase from 2023’s $965.55 billion. The acceleration continued into 2025, with revenues surging to $2.74 trillion—a staggering 517% growth rate that caught even optimistic analysts by surprise.

This explosive growth is driven by several converging factors. Enterprise adoption has moved beyond pilot programs into production deployments at scale. Cloud infrastructure has matured to support AI workloads efficiently. And perhaps most importantly, AI systems have demonstrated clear return on investment across multiple use cases—from customer service automation to software development to drug discovery.

Looking ahead, the market is projected to reach $3.55 trillion in 2027, $4.09 trillion in 2028, $4.71 trillion in 2029, and $5.40 trillion by 2030. By 2032, conservative estimates place the AI market at $7.08 trillion—nearly seven times its size just a decade earlier. These projections assume a moderation in growth rates as the market matures, but even the conservative scenario envisions sustained double-digit expansion through the decade.

The market’s structure has also evolved significantly. Where early AI revenues were concentrated in narrow applications like recommendation engines and basic natural language processing, 2026 sees balanced growth across multiple segments. Generative AI has emerged as the largest subsector, accounting for approximately 38% of total market value. Natural language processing represents 23% of the market, while machine learning platforms and computer vision each command significant shares.

Key Statistics and Market Data

The numbers behind the AI market’s growth tell a story of rapid transformation across every metric that matters. Here are the key statistics defining the AI landscape in 2026:

Market Size and Growth: The global AI market reached $3.09 trillion in 2026, up from $2.74 trillion in 2025. This 50.16% year-over-year growth rate, while lower than 2025’s exceptional 517% surge, still represents one of the fastest expansions of any major technology market. The compound annual growth rate from 2026 to 2030 is projected at 50.16%, with the market expected to exceed $5.4 trillion by decade’s end.

Segment Breakdown: Generative AI dominates the market with $1.18 trillion in revenue for 2026, representing 38% of total AI spending. Natural Language Processing accounts for $706.85 billion (23%), while Machine Learning platforms generate $1.12 trillion (36%). Computer Vision contributes $559.15 billion, and AI Robotics reaches $398.75 billion. Autonomous and Sensor Technology adds $307.65 billion to the total.

Enterprise Adoption: According to McKinsey’s State of AI 2025 report, 88% of organizations now use AI in at least one business function. However, only 23% have scaled AI agents beyond pilot programs, indicating significant runway for continued growth. High-performing AI organizations—those achieving significant value from AI—are 3.5 times more likely to have deployed AI agents at scale.

Industry Distribution: Healthcare leads AI adoption with 39% of sector-specific AI investment, followed by Finance at 22.6%, Security at 25%, and Semiconductor at 28.4%. Transportation captures 21.6% of industry-focused AI spending, while Manufacturing accounts for 15%. Media and Entertainment represents 12.8%, Energy 8.4%, Retail 7%, and Business and Legal Services 13.6%.

Productivity Impact: NVIDIA’s State of AI 2026 report reveals that 99% of telecommunications companies using AI report improved employee productivity, with 25% citing “major or significant improvement.” Across all industries, companies deploying AI report average productivity gains of 25-40% in automated workflows.

Venture Capital Investment: AI startups captured approximately $242 billion in Q1 2026 alone—representing roughly 80% of all global venture funding for the quarter. Four companies—OpenAI, Anthropic, xAI, and Waymo—absorbed approximately 65% of all AI venture dollars, raising a combined $188 billion in a single quarter. This marked the largest venture funding quarter on record, up more than 150% both quarter-over-quarter and year-over-year.

Revenue Concentration: OpenAI has reached $10 billion in annualized revenue as of mid-2025, while Anthropic grew from $1 billion to $4 billion in annualized revenue during the same period. This concentration of revenue among frontier labs highlights the winner-take-most dynamics emerging in foundation model development.

ROI Realization: According to PwC’s 2026 AI Performance Study, 29% of enterprises report seeing significant returns from AI investments. However, three-quarters of AI’s economic gains are captured by just 20% of companies—creating a widening gap between AI leaders and laggards. Companies in the top quartile for AI maturity report 2.6x ROI within the first year of deployment.

Workforce Impact: Larger shares of organizations expect AI to affect workforce size in 2026 than observed changes in 2025. While concerns about mass displacement persist, current data suggests AI is primarily augmenting rather than replacing workers—with 76% of companies reporting AI is being used to enhance employee capabilities rather than eliminate positions.

Seven Major Trends Shaping the AI Market in 2026

The AI market in 2026 is defined by seven transformative trends that are reshaping how organizations build, deploy, and benefit from artificial intelligence. Understanding these trends is essential for any business leader, investor, or technologist navigating this rapidly evolving landscape.

1. Agentic AI Moves from Experiment to Production

The most significant development in 2026 is the mainstream adoption of agentic AI—systems that can autonomously plan, execute, and complete complex multi-step tasks. While only 23% of organizations have scaled AI agents across their enterprise, this represents a dramatic increase from single-digit adoption rates in 2024. High-performing AI organizations are 3.5 times more likely to have deployed agents at scale, suggesting this technology is becoming a key differentiator.

Microsoft’s research indicates that agentic AI and other non-human identities will soon outnumber human users in organizations significantly. This shift from AI as a tool to AI as an autonomous worker represents a fundamental reimagining of how work gets done. Companies like Anthropic with Claude Code, OpenAI with its operator models, and Google with Antigravity 2.0 are competing to provide the infrastructure for this agentic future.

2. AI Superfactories and Global Infrastructure

Microsoft’s announcement of linked AI “superfactories”—global networks of data centers purpose-built for AI training and inference—signals a new phase in AI infrastructure. These facilities, connecting locations from Wisconsin to Atlanta and beyond, are designed to drive down costs while improving efficiency through resource sharing and load balancing.

The scale of investment is staggering. Meta has deployed tens of thousands of NVIDIA H100 GPUs across purpose-built data center clusters to train and serve its Llama models. Dell Technologies’ AI Factory with NVIDIA has been deployed by over 4,000 enterprise customers within two years of launch, with early adopters reporting up to 2.6x ROI within the first year.

3. Enterprise Shift from Experimentation to ROI

Perhaps the most important trend for sustainable market growth is the shift from AI experimentation to production deployments with real ROI expectations. As David Lanstein, CEO of Atolio, notes: “The most significant trend we see emerging is the shift from AI experimentation and excitement to private and secure deployments with real ROI expectations within enterprises.”

This shift is reflected in purchasing patterns. Enterprises are moving from buying AI tools to buying AI outcomes—paying for results rather than capabilities. This has profound implications for vendors, who must now demonstrate concrete value rather than simply showcasing impressive technology.

4. Open Source Accelerates Adoption

Meta’s strategy of releasing Llama models as open source has proven prescient. By making state-of-the-art models freely available, Meta has accelerated AI research and product development across industries while building an ecosystem that supports its commercial offerings. This approach has forced competitors to reconsider their own strategies, with many now offering open-weight models or API pricing that approaches open-source economics.

The open-source movement has democratized access to AI capabilities that were previously available only to well-funded tech giants. Startups and enterprises alike can now build on foundation models without paying premium API costs, driving innovation at the application layer.

5. Multi-Modal AI Becomes Standard

The leading AI systems of 2026 are inherently multi-modal, processing and generating text, images, audio, and video within unified architectures. Google’s Gemini 3.5 Flash, launched in 2026, explicitly targets “frontier performance for agents and coding” across multiple modalities.

This multi-modal capability is enabling new categories of applications—from real-time video analysis for security and manufacturing to voice-based interfaces that feel natural and intuitive. The distinction between different AI capabilities is blurring as unified models handle increasingly diverse tasks.

6. AI Leaders vs. Laggards Divergence

A troubling trend for the broader economy is the widening gap between AI leaders and laggards. According to PwC research, three-quarters of AI’s economic gains are captured by just 20% of companies. These leaders are not standing still—they’re moving into advanced techniques like multi-modal AI, real-time personalization, and autonomous decisioning while continually learning.

Meanwhile, laggards may still be trying to get basic predictive analytics in place. This divergence threatens to create a permanent competitive disadvantage for slow adopters, as AI capabilities compound over time in leading organizations.

7. Regulatory and Ethics Frameworks Emerge

As AI capabilities advance, regulatory frameworks are finally catching up. The EU AI Act has set precedents that influence global standards. Inaccuracy remains the AI-related risk most often cited by organizations, with companies increasingly investing in AI governance, safety testing, and responsible deployment practices.

Ethics has become a defining issue for AI’s future. As one analysis put it: “Ethics is the defining issue for the future of AI. And time is running short.” Companies that treat ethics and safety as afterthoughts risk regulatory action, reputational damage, and ultimately, competitive disadvantage.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a handful of well-funded players, but competition remains intense as new entrants challenge incumbents across multiple segments. Understanding this competitive landscape is crucial for predicting where value will accrue in the coming years.

Frontier Labs: The Foundation Model Wars

OpenAI remains the revenue leader with $10 billion in annualized revenue as of mid-2025. The company’s GPT models power countless applications, and its ChatGPT product maintains 53.9% global market share in AI chatbots. OpenAI’s strategy focuses on building increasingly capable general-purpose models while developing specialized variants for coding, reasoning, and multimodal tasks.

Anthropic has emerged as the primary challenger, growing from $1 billion to $4 billion in annualized revenue. The company’s Claude models are particularly strong in coding tasks—Claude Code has been adopted by companies like MongoDB and Snowflake. Anthropic’s focus on AI safety and constitutional AI has resonated with enterprise customers concerned about responsible deployment.

Google has leveraged its massive infrastructure and research capabilities to build Gemini into a formidable competitor. With 27.9% of the AI chatbot market, Gemini benefits from integration with Google’s broader ecosystem. The company’s emphasis on agentic AI—demonstrated by Antigravity 2.0’s ability to orchestrate multiple agents in parallel—positions it well for the next phase of AI adoption.

Meta has taken a different approach, betting on open source through its Llama model family. By releasing models freely, Meta has built goodwill with developers while creating a platform that supports its commercial ambitions. The company’s massive AI infrastructure investments—tens of thousands of H100 GPUs—demonstrate its commitment to remaining competitive.

Enterprise Platforms: The Battle for Business

Microsoft has emerged as the enterprise AI leader through its Copilot strategy. By integrating AI across its productivity suite, Microsoft has created a comprehensive platform that touches every aspect of business operations. As Josh Bersin notes, “Microsoft’s new Copilot ‘surface’ (ie. product strategy) is likely to give them the lead in revenue and market share for Enterprise AI.”

NVIDIA continues to dominate the AI infrastructure layer. Its GPUs power virtually every major AI training cluster, and the company’s software ecosystem—CUDA, TensorRT, and specialized frameworks—creates significant switching costs. NVIDIA’s State of AI reports have become essential reading for understanding industry trends.

Amazon Web Services, Google Cloud, and Microsoft Azure compete fiercely to host AI workloads. Each offers managed AI services, pre-trained models, and specialized infrastructure. The cloud providers’ ability to offer AI as a service has democratized access while creating massive revenue streams.

Emerging Challengers

xAI, Elon Musk’s venture, has raised significant funding and attracted attention with its Grok chatbot (2.4% market share). While smaller than established players, xAI’s integration with X (formerly Twitter) provides unique data advantages.

DeepSeek, a Chinese AI lab, has captured 4.1% of the global chatbot market. The company’s R1 reasoning model demonstrated that Chinese labs can compete at the frontier, challenging assumptions about Western dominance in AI development.

Perplexity has carved out a niche in AI-powered search, holding 1.3% of the chatbot market. Its focus on citations and accuracy has attracted users dissatisfied with traditional search engines.

Challenges and Pain Points

Despite the AI market’s impressive growth, significant challenges threaten to slow adoption or limit value realization. Organizations navigating the AI landscape must address these pain points to succeed.

1. The Talent Gap

The shortage of AI expertise remains the single biggest barrier to adoption. According to NVIDIA’s research, lack of AI experts is cited as the primary challenge by organizations across industries. This shortage affects every aspect of AI deployment—from model development and training to deployment and maintenance.

The competition for talent has driven salaries to extraordinary levels, with top AI researchers commanding compensation packages in the millions. This concentration of talent at well-funded tech giants leaves smaller organizations struggling to build capable AI teams.

2. Inaccuracy and Hallucination

Inaccuracy is the AI-related risk most often cited by organizations in McKinsey’s research. Large language models, despite their impressive capabilities, continue to generate plausible-sounding but false information—a phenomenon known as hallucination. This limits their deployment in high-stakes contexts where errors carry significant consequences.

Organizations are investing heavily in mitigation strategies—retrieval-augmented generation, fact-checking systems, and human-in-the-loop workflows—but the fundamental challenge remains unsolved at scale.

3. Infrastructure Costs

Training and running frontier AI models requires massive computational resources. The cost of training a state-of-the-art model has reached hundreds of millions of dollars, with inference costs adding ongoing expenses. This creates a barrier to entry that favors well-capitalized incumbents.

According to Yahoo Finance analysis, “Big Tech’s $2.7 trillion AI bill is coming due.” The massive investments in data centers, GPUs, and specialized infrastructure represent a bet on continued exponential growth that may not materialize if market conditions shift.

4. Regulatory Uncertainty

While regulatory frameworks are emerging, uncertainty remains a significant challenge. The EU AI Act has set precedents, but implementation details continue to evolve. In the United States, the regulatory landscape remains fragmented, with different agencies asserting jurisdiction over different aspects of AI.

This uncertainty makes long-term planning difficult and creates compliance risks for organizations deploying AI across borders. Companies must navigate a complex patchwork of regulations while anticipating future requirements.

Opportunities and Growth Strategies

For organizations looking to capitalize on the AI market’s growth, several strategic opportunities present themselves. Success requires understanding where value is being created and positioning to capture it.

1. Vertical AI Applications

While foundation models capture headlines, significant value is being created by companies applying AI to specific industry verticals. Healthcare AI, with 39% of sector-specific investment, offers opportunities in drug discovery, diagnostic imaging, and personalized medicine. Financial services (22.6% of investment) presents opportunities in fraud detection, algorithmic trading, and risk assessment.

Companies that combine deep domain expertise with AI capabilities are building sustainable competitive advantages. These vertical applications often face less competition than horizontal platforms and can command premium pricing.

2. AI Infrastructure and Tooling

The infrastructure layer continues to offer significant opportunities. Companies building tools for AI development, deployment, and monitoring are seeing strong demand. This includes model serving platforms, observability tools, safety testing frameworks, and specialized hardware.

Dell Technologies’ AI Factory success—4,000 enterprise customers and 2.6x ROI for early adopters—demonstrates the appetite for integrated AI infrastructure solutions. As AI moves from experimentation to production, the tooling that enables reliable deployment becomes increasingly valuable.

3. AI-Enabled Services

Professional services firms are finding opportunities in helping enterprises navigate AI adoption. From strategy consulting to implementation services to ongoing support, the services ecosystem around AI is growing rapidly.

Companies like Vention and others are building significant businesses by providing AI development teams and consulting services. This model allows enterprises to access AI expertise without building internal capabilities.

Case Studies and Success Stories

Siemens: Manufacturing AI at Scale

Siemens has emerged as a leader in industrial AI, helping manufacturers realize productivity gains and optimize workflows by integrating AI into tools and applications. The company’s approach focuses on practical applications that deliver measurable ROI—predictive maintenance, quality control, and process optimization.

The results have been impressive: manufacturers using Siemens’ AI solutions report significant reductions in downtime, improved product quality, and increased operational efficiency. This success demonstrates that AI’s value extends far beyond tech companies to traditional industries.

Snowflake: AI-Native Data Analytics

Snowflake has successfully integrated AI into its data analytics platform, with programmers depending on the company’s CoCo development tool and Claude Code. CEO Sridhar Ramaswamy has positioned AI as central to the company’s strategy, recognizing that the future of data analytics is AI-powered.

The company’s success demonstrates how AI can enhance existing software categories rather than simply replacing them. By making AI a seamless part of the analytics workflow, Snowflake has increased user productivity and differentiated its platform.

MongoDB: Developer Productivity Through AI

Database software maker MongoDB has rolled out three generative AI tools, including Anthropic’s Claude Code, to its engineers. CEO CJ Desai reports that these tools have significantly improved developer productivity, allowing engineers to focus on higher-value work.

MongoDB’s approach—offering developers choice among AI tools rather than mandating a single solution—reflects the reality that different AI systems excel at different tasks. This flexibility has been key to adoption.

Future Outlook and Predictions

Looking beyond 2026, several developments will shape the AI market’s trajectory through 2030 and beyond. Organizations preparing for this future should consider these predictions:

Market Size Projections

The AI market is projected to reach $3.55 trillion in 2027, $4.09 trillion in 2028, $4.71 trillion in 2029, and $5.40 trillion by 2030. By 2032, the market could exceed $7 trillion. These projections assume continued enterprise adoption, infrastructure improvements, and the development of new use cases.

Scenario analysis suggests significant upside potential. In an optimistic scenario, the AI market reaches $3.52 trillion by 2032—more than double the conservative projection. This scenario assumes breakthroughs in AI capabilities, accelerated enterprise adoption, and the emergence of entirely new AI-powered industries.

Technology Trajectories

Agentic AI will likely become the dominant paradigm, with AI systems evolving from assistants to autonomous workers. This shift will require new infrastructure, new safety approaches, and new organizational structures to manage human-AI collaboration.

Multi-modal AI will become standard, with the distinction between different AI capabilities (NLP, computer vision, speech) blurring into unified systems. This will enable new categories of applications that seamlessly handle diverse data types.

Industry Transformation

By 2030, AI will be deeply embedded in virtually every industry. Healthcare will see AI-powered drug discovery become routine, with development timelines compressed from years to months. Financial services will operate with AI managing risk, detecting fraud, and optimizing portfolios in real-time. Manufacturing will run on AI-optimized supply chains and predictive maintenance systems.

The companies that thrive will be those that successfully integrate AI into their core operations—not as a bolt-on capability, but as a fundamental part of how they create value.

Regional Market Analysis

The AI market’s growth is not evenly distributed across regions, with significant variations in adoption rates, investment levels, and regulatory environments shaping local market dynamics.

North America: The Innovation Hub

North America continues to dominate the global AI market, with the United States accounting for the largest share of AI investment and development. The U.S. AI market was estimated at $173.56 billion in 2025 and is projected to reach $976.23 billion by 2035, representing a CAGR of 18.85%. This dominance is driven by the concentration of leading AI labs—OpenAI, Anthropic, Google DeepMind, and Meta AI—all headquartered in the region.

The region benefits from a mature venture capital ecosystem, with Silicon Valley and other tech hubs providing the funding necessary for AI startups to scale. Additionally, the presence of world-class research institutions like MIT, Stanford, and Carnegie Mellon ensures a steady pipeline of AI talent and innovation.

Europe: Regulatory Leadership

Europe has taken a different approach, prioritizing regulatory frameworks and ethical AI development. The EU AI Act, implemented in 2024, has set global standards for AI governance, influencing how companies develop and deploy AI systems worldwide. While this regulatory focus has sometimes been criticized for potentially stifling innovation, it has also positioned European companies as leaders in trustworthy AI.

European AI investment has grown steadily, with particular strength in industrial AI applications and automotive AI. Companies like Siemens, SAP, and ASML are leveraging AI to maintain competitive advantages in their respective sectors.

Asia-Pacific: Rapid Adoption

The Asia-Pacific region represents the fastest-growing AI market, driven by massive investments from China, Japan, and South Korea. Chinese AI labs, particularly DeepSeek, have demonstrated that they can compete at the frontier of AI development, challenging Western dominance in the field.

Japan and South Korea are focusing on robotics and manufacturing AI, leveraging their strengths in hardware and automation. The region’s large population and rapid digitalization create ideal conditions for AI adoption across consumer and enterprise applications.

AI Technology Segments in Detail

Generative AI: The Market Leader

Generative AI has emerged as the dominant segment, with revenues reaching $1.18 trillion in 2026. This represents a remarkable transformation from just $179 million in 2023, demonstrating the explosive impact of large language models and image generation technologies.

The segment’s growth is driven by enterprise adoption of tools like ChatGPT, Claude, and Gemini for content creation, code generation, and customer service. Businesses are finding that generative AI can significantly reduce time-to-market for content-heavy projects while improving quality and consistency.

Machine Learning Platforms

Machine learning platforms generate $1.12 trillion in revenue, serving as the foundational infrastructure for AI development. These platforms provide the tools and frameworks necessary for organizations to build, train, and deploy custom AI models.

Major players in this space include Amazon SageMaker, Google Vertex AI, Microsoft Azure ML, and open-source platforms like TensorFlow and PyTorch. The democratization of machine learning through these platforms has enabled organizations of all sizes to leverage AI capabilities.

Computer Vision and Robotics

Computer vision contributes $559.15 billion to the AI market, with applications ranging from autonomous vehicles to medical imaging. The technology has matured significantly, with modern systems achieving human-level performance in many visual recognition tasks.

AI robotics, generating $398.75 billion, is transforming manufacturing, logistics, and healthcare. Advances in robotic manipulation and navigation are enabling robots to operate in unstructured environments, expanding their potential applications.

Investment and Funding Landscape

The AI investment landscape in 2026 is characterized by unprecedented capital concentration and massive funding rounds that dwarf previous technology cycles.

The $242 Billion Quarter

Q1 2026 saw AI startups capture approximately $242 billion in venture funding—representing roughly 80% of all global venture capital for the quarter. This concentration reflects investor conviction that AI represents a generational technology shift comparable to the internet or mobile computing.

Four companies dominated this funding: OpenAI, Anthropic, xAI, and Waymo collectively raised $188 billion, or 65% of all AI venture dollars. Anthropic’s $65 billion Series H in May 2026 valued the company at $965 billion, making it the second-most valuable private company globally behind only SpaceX.

Public Market Performance

AI-related public companies have significantly outperformed broader market indices. NVIDIA, the leading AI chipmaker, has seen its market capitalization exceed $3 trillion, making it one of the world’s most valuable companies. Other AI beneficiaries including Microsoft, Google, and Meta have also delivered strong returns.

The successful IPO of Cerebras Systems in 2026, pricing at the upper end of its range at $185 per share and opening at $350, demonstrated strong public market appetite for AI infrastructure plays. This liquidity event is expected to fuel further private market investment as returns are recycled into new AI ventures.

AI Impact on Employment and Workforce

The relationship between AI and employment remains one of the most debated aspects of the technology’s impact. While fears of mass displacement persist, current data suggests a more nuanced picture of augmentation and transformation rather than simple replacement.

The Augmentation Paradigm

According to McKinsey’s research, 76% of companies report using AI primarily to enhance employee capabilities rather than eliminate positions. This augmentation approach leverages AI to handle routine tasks while freeing human workers for higher-value activities requiring creativity, judgment, and emotional intelligence.

Industries seeing the strongest productivity gains include software development, where AI coding assistants have become standard tools; customer service, where AI handles routine inquiries while humans manage complex cases; and healthcare, where AI assists with diagnosis and treatment planning.

Workforce Transformation

While overall employment levels have remained stable, the nature of work is changing rapidly. Roles focused on AI prompt engineering, model fine-tuning, and AI-human interaction design have emerged as high-demand specialties. Traditional roles in data entry, basic content creation, and routine analysis are declining.

Organizations are investing heavily in reskilling programs, with 84% of leaders planning to expand training initiatives to prepare their workforce for AI integration. The most successful companies are those that view AI as a tool for elevating human potential rather than simply reducing headcount.

AI Ethics and Responsible Development

As AI capabilities advance, the importance of ethical development and deployment has moved from academic concern to boardroom priority. Organizations are increasingly recognizing that responsible AI is not just a moral imperative but a competitive necessity.

The EU AI Act and Global Standards

The European Union’s AI Act, which came into full effect in 2024, has established the world’s first comprehensive regulatory framework for artificial intelligence. The legislation categorizes AI systems by risk level, with strict requirements for high-risk applications in areas like healthcare, transportation, and criminal justice.

This regulatory approach is influencing standards globally, with other jurisdictions adopting similar risk-based frameworks. Companies operating internationally must now navigate a complex landscape of requirements, driving investment in AI governance and compliance infrastructure.

Addressing Bias and Fairness

AI systems trained on historical data can perpetuate and amplify existing biases. Leading organizations are implementing rigorous testing protocols to identify and mitigate bias in their AI systems. Techniques like adversarial debiasing, fairness constraints, and diverse training datasets are becoming standard practice.

The business case for fairness is compelling: biased systems can lead to regulatory penalties, reputational damage, and missed market opportunities. Companies that prioritize fairness are finding that it leads to better products that serve broader customer bases.

AI Infrastructure and Compute

The computational requirements of modern AI systems have created a massive infrastructure market, with specialized hardware and data center investments reaching unprecedented scales.

The GPU Shortage and Alternatives

NVIDIA’s GPUs remain the dominant platform for AI training, with demand consistently outstripping supply. This shortage has driven interest in alternative architectures, including Google’s TPUs, Amazon’s Trainium, and various startup offerings. Microsoft and Meta have invested billions in building custom AI chips to reduce their dependence on NVIDIA.

The energy consumption of AI data centers has become a significant concern, with some estimates suggesting that AI could account for 3-4% of global electricity consumption by 2030. This is driving innovation in more efficient architectures and increased investment in renewable energy to power AI infrastructure.

Edge AI and Distributed Computing

While large models trained in data centers get the headlines, significant growth is occurring in edge AI—systems that run on local devices rather than in the cloud. This approach reduces latency, improves privacy, and enables AI applications in environments with limited connectivity.

Apple’s Neural Engine, Qualcomm’s AI accelerators, and a growing ecosystem of edge AI chips are enabling sophisticated AI capabilities on smartphones, IoT devices, and industrial equipment. The edge AI market is projected to grow at over 40% annually through 2030.

AI in Specific Industries

Healthcare Transformation

Healthcare represents one of the most promising applications for AI, with 39% of sector-specific AI investment flowing into this space. AI systems are demonstrating remarkable capabilities in medical imaging, with some studies showing AI can match or exceed human radiologists in detecting certain conditions.

Drug discovery is being revolutionized by AI, with companies like DeepMind’s AlphaFold providing unprecedented insights into protein structures. AI-designed drugs are entering clinical trials, potentially reducing the time and cost of bringing new treatments to market from years to months.

Financial Services Innovation

The financial services industry has been an early and aggressive adopter of AI, with 22.6% of sector-specific investment. Applications include fraud detection, algorithmic trading, risk assessment, and customer service automation.

AI-powered trading systems now account for a significant portion of market volume, with the ability to analyze vast datasets and execute trades in milliseconds. Regulatory technology (RegTech) powered by AI is helping financial institutions navigate complex compliance requirements more efficiently.

Manufacturing and Industry 4.0

Manufacturing accounts for 15% of industry-focused AI spending, with applications in predictive maintenance, quality control, and supply chain optimization. Siemens, GE, and other industrial giants are leveraging AI to transform traditional manufacturing processes.

Predictive maintenance powered by AI can reduce equipment downtime by up to 50%, delivering substantial cost savings. Computer vision systems are automating quality inspection, detecting defects that human inspectors might miss while operating at much higher speeds.

Key Takeaways

- The global AI market reached $3.09 trillion in 2026, with a projected 50.16% CAGR through 2030

- Generative AI dominates with $1.18 trillion in revenue, representing 38% of the total market

- 88% of organizations now use AI in at least one business function, though only 23% have scaled AI agents

- ChatGPT leads the AI chatbot market with 53.9% share, followed by Google Gemini at 27.9%

- AI startups captured $242 billion in Q1 2026 alone—80% of all global venture funding

- Three-quarters of AI’s economic gains are captured by just 20% of companies, creating a widening gap between leaders and laggards

- Agentic AI, AI superfactories, and enterprise ROI focus are the defining trends of 2026

- The talent gap, inaccuracy concerns, and infrastructure costs remain significant challenges

- Vertical AI applications and AI infrastructure present the strongest growth opportunities

- The AI market is projected to exceed $5.4 trillion by 2030 and potentially $7 trillion by 2032

Sources and Citations

- Statista AI Market Forecast 2026-2032: https://www.statista.com/outlook/tmo/artificial-intelligence/worldwide

- McKinsey State of AI 2025: https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

- Microsoft AI Trends 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026

- NVIDIA State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026

- Grand View Research Generative AI Market: https://www.grandviewresearch.com/industry-analysis/generative-ai-market-report

- Crunchbase Q1 2026 Venture Funding: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026

- Digital Applied AI Funding 2026: https://www.digitalapplied.com/blog/ai-venture-funding-2026-where-242b-went-data-atlas

- Momentic AI Chatbot Market Share July 2026: https://momenticmarketing.com/blog/top-ai-chatbots

- MarketsandMarkets AI Market Report: https://www.marketsandmarkets.com/Market-Reports/artificial-intelligence-market-74851580.html

- IBM AI Tech Trends 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026