The artificial intelligence market has reached an inflection point in 2026. What started as experimental technology has transformed into a $539.5 billion global industry that is fundamentally reshaping how businesses operate, compete, and create value. From autonomous AI agents that execute complex workflows to generative models that produce everything from code to creative content, AI is no longer a futuristic concept—it is the present reality of modern business.

In this comprehensive analysis, we examine the state of the AI market in 2026, diving deep into market size projections, key statistics, emerging trends, competitive dynamics, and the challenges that organizations face as they scale AI initiatives. Whether you are a business leader evaluating AI investments, a developer building AI-powered applications, or an investor tracking the next wave of technological disruption, this report provides the data-driven insights you need to navigate the AI landscape.

Market Overview: The $539.5 Billion AI Ecosystem

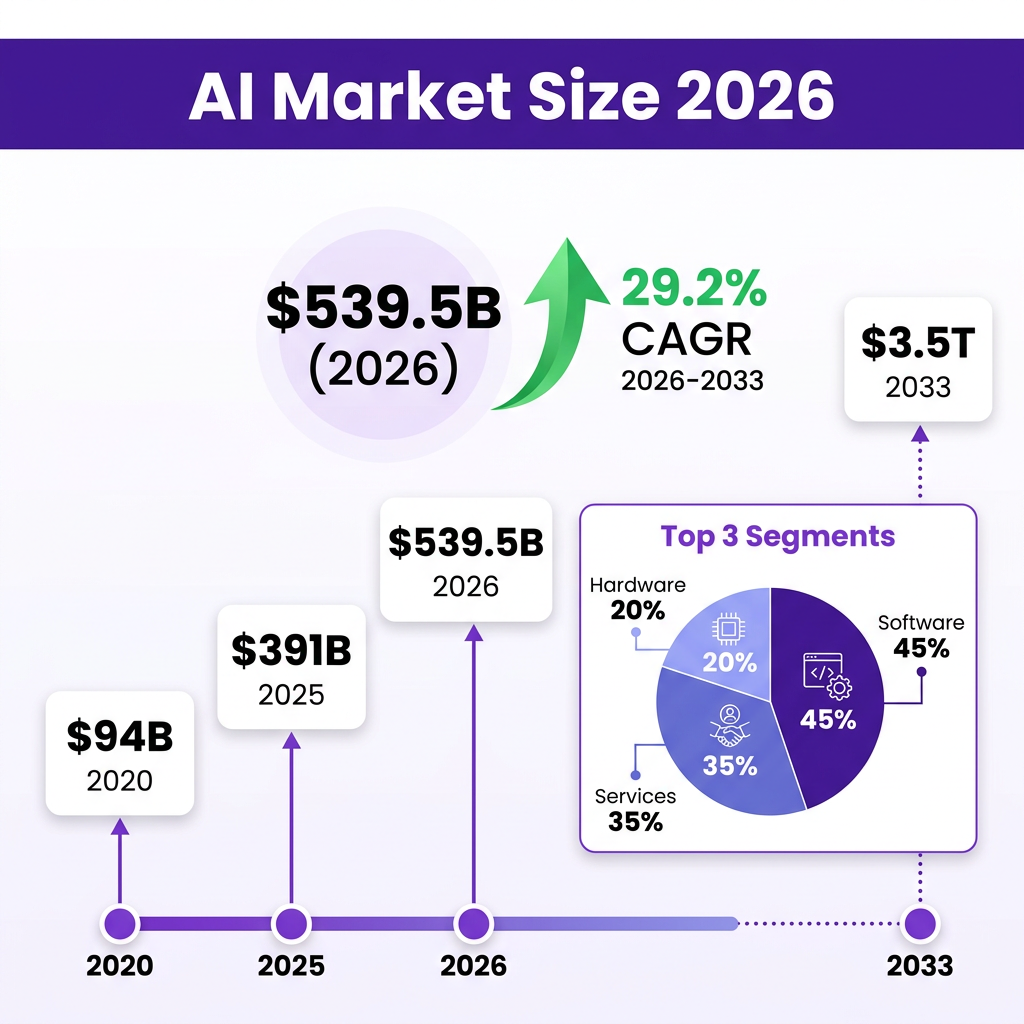

The global artificial intelligence market has experienced unprecedented growth, reaching $539.5 billion in 2026 according to Grand View Research. This represents a significant jump from $390.9 billion in 2025, demonstrating the accelerating pace of AI adoption across industries. The market is projected to reach a staggering $3.5 trillion by 2033, growing at a compound annual growth rate (CAGR) of 29.2%.

To understand the magnitude of this growth, consider the trajectory: the AI market was valued at just $94.81 billion in 2020. By 2031, Statista Market Insights forecasts it will reach $1.675 trillion—representing a 17.7× expansion in just over a decade. This growth is not merely incremental; it represents a fundamental restructuring of the global economy as AI capabilities mature and find applications across virtually every industry sector.

The United States continues to dominate the AI landscape, with the U.S. AI market size estimated at $173.56 billion in 2025 and projected to reach $976.23 billion by 2035, growing at a CAGR of 18.85%. According to OECD data, more than 80% of global private investment in AI flows to U.S. AI firms, underscoring the country’s position as the leading destination for AI innovation and funding.

The market is segmented across three primary categories: software, services, and hardware. Software dominates with approximately 45% market share, encompassing AI platforms, applications, and development tools. Services account for roughly 35%, including consulting, implementation, and managed services. Hardware represents about 20%, covering the specialized chips and infrastructure required to train and run AI models at scale.

Within the software segment, generative AI has emerged as the fastest-growing subcategory. The generative AI market alone is projected to grow from $37.87 billion in 2024 to $442 billion by 2031—a more than 10× increase in just seven years. This explosive growth is driven by enterprise adoption of large language models, image generation tools, and code completion systems that are transforming how knowledge work gets done.

Regional analysis reveals significant variations in AI adoption and investment. North America leads in absolute spending, driven by the concentration of technology companies and venture capital. However, Asia-Pacific is experiencing the fastest growth rates, with China making massive investments in AI research and development as part of its national strategy. Europe, while slightly behind in raw investment numbers, is leading in AI regulation and ethical frameworks, with the EU AI Act setting global standards for responsible AI development.

Key Statistics and Data: Understanding the AI Landscape

The numbers tell a compelling story about AI’s rapid mainstream adoption. According to McKinsey’s 2025 State of AI report, 88% of organizations now use AI in at least one business function—up from just 55% in 2023. This represents a 33-percentage-point increase in just two years, making AI one of the fastest-adopted enterprise technologies in history. To put this in perspective, it took cloud computing nearly a decade to achieve similar penetration levels.

However, the data also reveals a significant gap between experimentation and scaled deployment. While 88% of organizations use AI in some capacity, only 23% are scaling agentic AI systems across the enterprise. Just 7% of organizations have fully scaled AI implementations, while 63% remain in piloting or early scaling phases, and 32% are still in experimentation. This gap represents both a challenge and an opportunity for businesses looking to capture competitive advantage through AI.

Generative AI adoption is accelerating even faster than overall AI adoption. The percentage of companies using or exploring generative AI jumped from 33% in 2023 to 79% in 2025—a 46-percentage-point increase in just two years. This rapid uptake reflects the immediate productivity benefits that tools like ChatGPT, Claude, and GitHub Copilot deliver to knowledge workers. The accessibility of these tools, requiring no technical expertise to use effectively, has democratized AI in ways that previous technologies did not.

Enterprise spending on generative AI has grown proportionally. According to Menlo Ventures, companies spent $37 billion on generative AI in 2025, up from $11.5 billion in 2024—a 3.2× year-over-year increase. This spending is concentrated in two areas: AI applications ($19 billion) and AI infrastructure ($18 billion for what the industry calls “picks and shovels”). The application layer includes tools for content generation, code completion, customer service automation, and data analysis. The infrastructure layer includes compute resources, model serving platforms, and development tools.

The AI infrastructure investment is particularly noteworthy. Foundation model providers announced close to $1 trillion in AI infrastructure commitments, reflecting the massive capital requirements for training and deploying state-of-the-art models. This infrastructure build-out includes data centers, specialized AI chips, and networking equipment necessary to support the computational demands of modern AI systems. The scale of this investment is unprecedented in technology history, surpassing even the cloud computing build-out of the 2010s.

AI’s share of new unicorn births has grown dramatically, from just 6% in 2015 to 53% in 2025. This shift indicates that AI has become the primary driver of high-value startup creation, replacing sectors like consumer internet and mobile apps as the dominant source of venture-scale returns. Investors are betting that AI will create entirely new categories of software and services, just as the internet and mobile did in previous decades.

Corporate AI adoption varies significantly by function. IT and Marketing & Sales lead with 36% adoption each, reflecting the natural fit between AI capabilities and these digitally mature functions. Manufacturing and Strategy & Corporate Finance show lower adoption at 12%, indicating that operational and regulated areas present greater implementation challenges. Healthcare, while showing promise, remains at moderate adoption levels due to regulatory constraints and the high stakes of medical decisions.

The ROI from AI investments is becoming clearer. Organizations employing AI for over three years document a 25% reduction in cost per contact in customer service, with a 30% drop for those applying generative AI to one or two use cases. These measurable returns are driving increased investment as early adopters demonstrate the financial benefits of AI implementation. Companies are moving beyond the “experimentation for experimentation’s sake” phase to demand concrete business outcomes from AI projects.

Looking at the broader economic impact, IDC projects that AI investments will generate a cumulative global impact of $22.3 trillion by 2030, accounting for roughly 3.7% of global GDP. This projection underscores AI’s transformation from a technology sector to a fundamental driver of economic growth. If these projections hold, AI will be one of the most significant technological drivers of economic value in human history.

Venture capital investment in AI has reached historic levels. AI startups attracted 53% of all global VC dollars in 2025, according to Pitchbook data. A record $40 billion AI deal in Q1 2025 lifted venture capital investment to its strongest quarter since Q1 2022. Information technology continued to dominate the VC ecosystem, representing 74% of investment and accounting for seven of the top 10 deals as investors retained their focus on companies with significant AI influence.

Major Trends Shaping AI in 2026

The AI landscape in 2026 is defined by seven major trends that are reshaping how organizations develop, deploy, and benefit from artificial intelligence. Understanding these trends is essential for businesses looking to build sustainable competitive advantage through AI. These trends represent not just technological evolution, but fundamental shifts in how AI is integrated into business processes and value creation.

1. The Rise of Agentic AI

The most significant trend in 2026 is the shift from AI as a tool to AI as an autonomous agent. Agentic AI refers to systems capable of understanding complex goals, planning multi-step actions, executing those actions independently, and self-correcting when necessary. Unlike earlier AI systems that required constant human guidance, agentic AI operates with defined business goals and can execute complete workflows end-to-end without human intervention.

According to IBM’s 2026 AI trends report, agentic AI and other non-human identities will outnumber human users in organizations significantly in the coming years. These agents can autonomously triage alerts, draft incident reports, qualify leads, manage customer journeys, and accelerate software development cycles by 10× or more. The implications for workforce structure and organizational design are profound.

The agentic AI market was valued at $5.4 billion in 2025 and is projected to grow exponentially as enterprises move from experimentation to production deployment. Companies report 70% automation of tier-1 support inquiries through AI agents, and Anthropic projects $70 billion in revenue by 2028 driven by B2B agent deployments. The shift from copilots that assist humans to agents that work autonomously represents a fundamental change in the human-AI relationship.

2. Enterprise Shift from Experimentation to Production

Enterprises are moving decisively from AI experimentation to production-grade deployments. As Tomás Hernando Kofman, Cofounder of Not Diamond, noted in an interview with IBM Think: “The massive middle of the enterprise bell curve begins to move from experimentation to production-grade systems.” This shift is characterized by a focus on private and secure deployments with real ROI expectations rather than innovation for its own sake.

However, this transition is not without challenges. According to Writer’s 2026 survey, 79% of organizations face challenges in adopting AI—a double-digit increase from 2025. The challenges include data quality issues, integration complexities, governance requirements, and the need for specialized talent. Organizations are discovering that moving from pilot to production requires solving a different set of problems than those addressed in the experimentation phase.

3. AI Tackling Complex Enterprise Workflows

The most powerful trend for 2026 is AI tackling complex enterprise workflows rather than isolated tasks. Steven Aberle, Founder of Rohirrim, an AI-native startup focused on complete procurement ecosystems, stated: “The most powerful trend I see for next year is AI tackling complex enterprise workflows.” This includes end-to-end automation of processes spanning cloud operations, finance, IT, security, and software delivery.

Organizations are connecting powerful AI systems to sensitive tools, delegating decisions to probabilistic systems, and relying on third-party platforms to mediate access. This requires new governance models, orchestration capabilities, and risk management frameworks. The complexity of these integrations is driving demand for AI orchestration platforms and enterprise AI operating systems.

4. Multimodal AI Expansion

The rise of multimodal and video-focused generative AI models is enabling richer and more immersive applications. Google’s Gemini 3 Flash delivers comparable reasoning and coding capabilities to Gemini 3 Pro but uses fewer tokens for daily tasks, enabling enterprises to adopt multimodal AI with lower latency and reduced operational costs.

Organizations are adopting these tools to generate realistic images, videos, and simulations, supporting faster content development cycles and personalized experiences for consumers and business clients. The multimodal AI market is growing rapidly as enterprises discover new use cases that combine text, image, audio, and video understanding. Marketing teams, product designers, and content creators are among the early adopters driving this trend.

5. Domain-Specific AI Solutions

In 2026, businesses increasingly prefer domain-specific agentic AI designed for their unique environments. Rather than general-purpose models, organizations are deploying AI systems fine-tuned for healthcare, finance, legal, manufacturing, and other specialized domains. This trend reflects the recognition that AI performance and reliability improve significantly when models are trained on domain-specific data and designed for specific use cases.

Context engineering has emerged as a critical discipline, representing the shift from generic prompting to sophisticated engineering of AI context for specific business applications. Organizations are building proprietary context layers that give AI systems the background knowledge needed to perform effectively in their specific environments. This approach reduces hallucinations and improves output quality for specialized tasks.

6. AI Superfactories and Infrastructure Scale

Microsoft’s 2026 AI trends report highlights the rise of flexible, global AI systems—a new generation of linked AI “superfactories” that will drive down costs and improve efficiency. These massive data center complexes are designed specifically for AI workloads, featuring specialized cooling systems, high-bandwidth networking, and power densities that far exceed traditional data centers.

The infrastructure build-out is unprecedented. With nearly $1 trillion in announced commitments, the AI infrastructure market is creating new opportunities for hardware vendors, data center operators, and energy providers. This scale of investment reflects the conviction that AI will be a foundational technology for decades to come. The geographic distribution of these facilities is also becoming a strategic consideration, with countries competing to attract AI infrastructure investment.

7. Governance-First AI Deployment

As AI systems become more autonomous and impactful, governance has emerged as a critical priority. Governance-first Agentic AI is one of the most critical trends in 2026, addressing questions of accountability, transparency, and control. Organizations are implementing frameworks to ensure AI systems operate within defined boundaries, maintain audit trails, and can be explained to regulators and stakeholders.

By 2026, regulators and supervisors are making it clear that innovation no longer shields organizations from responsibility. AI systems are now assessed not by their novelty, but by their impact on customers, markets, and society—and by the governance structures behind them. This shift is driving investment in AI governance platforms, model monitoring tools, and compliance automation.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a mix of established technology giants and emerging specialists, each competing across different layers of the AI stack—from foundation models to applications to infrastructure. The competitive dynamics vary significantly by layer, with different winners emerging in models, infrastructure, and applications.

Foundation Model Providers

OpenAI and Anthropic have emerged as the dominant players in the foundation model space. According to Menlo Ventures, Anthropic now earns 40% of enterprise LLM spend, up from 24% in 2024 and 12% in 2023. This represents a remarkable ascent for the company, which has positioned itself as the enterprise-friendly alternative to OpenAI with stronger safety commitments and more transparent practices.

OpenAI maintains a strong position with ChatGPT and its API offerings, though it faces increasing competition. The company is reportedly targeting an $850 billion valuation in an upcoming IPO, reflecting investor confidence in its technology and market position. However, questions remain about its path to profitability and the sustainability of its massive compute costs.

Google has made significant gains, with revenue from generative AI products growing 800% from Q4 2025 to Q1 2026. The company’s Gemini models and Vertex AI platform are gaining traction in enterprise accounts, leveraging Google’s cloud infrastructure and existing customer relationships. AWS Bedrock customer spending jumped 170% over the same period, demonstrating strong demand for cloud-based AI services.

Microsoft continues to integrate AI across its product portfolio, from Copilot in Office 365 to Azure OpenAI Service. The company’s partnership with OpenAI gives it unique access to cutting-edge models while it develops its own capabilities. Microsoft’s enterprise relationships and distribution channels provide significant advantages in the commercial AI market.

Infrastructure Providers

Nvidia remains the dominant provider of AI training and inference chips, with its GPUs powering the majority of AI workloads. The company briefly became the world’s most valuable company in 2025, reflecting the critical importance of AI infrastructure. Nvidia’s CUDA software ecosystem creates significant switching costs that protect its market position.

CoreWeave and Lambda have emerged as significant players in GPU cloud infrastructure. CoreWeave, which pivoted from cryptocurrency mining to AI compute, reached a $19 billion valuation and became one of the largest GPU cloud providers. These companies provide the specialized infrastructure needed to train and run large AI models, offering alternatives to the major cloud providers.

Application Layer

The application layer has seen new entrants gain significant ground. According to Menlo Ventures, new AI-native entrants captured nearly $2 in revenue for every $1 earned by incumbents in 2025—63% of the market, up from 36% in 2024. This shift indicates that AI is creating opportunities for startups to disrupt established players rather than simply enhancing incumbent products.

AI coding tools represent one of the most successful application categories. Products like Cursor, GitHub Copilot, and Windsurf have achieved rapid adoption among developers, demonstrating the immediate value of AI assistance in software development workflows. These tools are not just incrementally improving productivity—they are fundamentally changing how software is written.

Challenges and Pain Points

Despite the rapid growth and adoption, the AI market faces significant challenges that organizations must navigate to realize the full potential of artificial intelligence. These challenges span technical, organizational, and regulatory dimensions, and addressing them is essential for sustainable AI deployment.

1. Hallucinations and Reliability

AI hallucinations—confident but false information generated by AI systems—remain a critical challenge. According to Master of Code, 56% of organizations cite hallucinations as a top generative AI threat. The consequences can be severe: a large language model used in a U.S. courtroom cited six cases that did not exist, demonstrating the risks of unchecked AI outputs in high-stakes contexts.

Organizations are addressing this through human review for high-stakes outputs, retrieval-augmented generation (RAG) systems that ground AI responses in verified sources, and improved model training techniques. However, achieving perfect reliability remains an unsolved problem, particularly for open-domain question answering and creative tasks.

2. Data Quality and Management

Data quality and data management failures are among the top AI challenges businesses face in 2026. AI systems are only as good as the data they are trained on, and many organizations struggle with fragmented, inconsistent, or incomplete data. This remains one of the foundational limitations of artificial intelligence.

Successful AI implementation requires significant investment in data infrastructure, including data pipelines, quality monitoring, and governance frameworks. Organizations that have not solved their data challenges find that AI projects fail to deliver expected results. The old adage “garbage in, garbage out” applies with particular force to AI systems.

3. AI Talent Shortage

The shortage of AI talent continues to constrain adoption. Organizations struggle to hire and retain data scientists, machine learning engineers, and AI product managers. This talent gap creates delivery risk for AI initiatives and drives up costs for skilled professionals. The competition for talent is particularly intense for individuals with experience deploying AI in production environments.

Companies are addressing this challenge through upskilling existing employees, partnering with AI consultancies, and using low-code/no-code AI platforms that reduce the need for specialized technical expertise. However, the demand for AI talent continues to outpace supply, creating a persistent bottleneck for AI adoption.

4. Security and Privacy Risks

AI security and data privacy risks are major concerns, with 53% of organizations citing cybersecurity as a top generative AI threat. AI systems can be vulnerable to attacks that manipulate model outputs, extract sensitive training data, or bypass safety controls. The attack surface for AI systems is broader than traditional software, encompassing both the models themselves and the infrastructure that supports them.

Privacy concerns are equally significant. AI systems trained on sensitive data may inadvertently expose that information in their outputs. Organizations must implement privacy-first data practices, access controls, and monitoring systems to manage these risks. The tension between AI performance (which often requires more data) and privacy (which requires data minimization) creates ongoing challenges.

5. Integration and Scalability

Integration and scalability failures prevent many AI pilots from reaching production. AI systems must integrate with existing enterprise systems, workflows, and data sources—a complex undertaking that often proves more difficult than anticipated. Legacy systems, in particular, can be challenging to integrate with modern AI capabilities.

Scalability presents additional challenges. Models that work well in pilot environments may struggle with production workloads, latency requirements, or cost constraints at scale. Organizations need robust MLOps and LLMOps practices to manage these complexities. The cost of inference at scale can be substantial, requiring careful optimization and architecture decisions.

6. Ethical and Bias Concerns

Bias continues to be one of the most difficult AI challenges for 2026. AI systems can perpetuate or amplify biases present in their training data, leading to unfair outcomes in hiring, lending, criminal justice, and other sensitive domains. The challenge is compounded by the difficulty of defining fairness in contexts where different stakeholders have different perspectives.

Explainability is closely related—many AI models cannot explain their decisions, creating compliance gaps in regulated sectors and eroding trust. Organizations are investing in explainability tools and bias detection systems, but these remain imperfect solutions. The tension between model performance (often achieved through complexity) and explainability (often requiring simplicity) is a persistent challenge.

7. Regulatory Fragmentation

A defining feature of AI risk in 2026 is fragmented regulation with unified expectations. Different jurisdictions are implementing varying AI regulations—the EU AI Act, U.S. executive orders, and various national frameworks—creating compliance complexity for global organizations. The pace of regulatory change often exceeds the pace of organizational adaptation.

Despite this fragmentation, expectations are converging around principles of transparency, accountability, and human oversight. Organizations must navigate this complex landscape while maintaining innovation velocity. The cost of compliance is significant, particularly for smaller organizations with limited legal and regulatory resources.

Opportunities and Growth Strategies

The challenges facing AI adoption are significant, but so are the opportunities. Organizations that successfully navigate these challenges can capture substantial competitive advantages and create significant value for customers and stakeholders.

1. Vertical AI Solutions

The opportunity for vertical-specific AI solutions is enormous. Rather than competing with general-purpose models, startups and enterprises can build AI systems tailored to specific industries—healthcare diagnostics, legal document analysis, financial risk assessment, manufacturing quality control. These domain-specific solutions can achieve higher accuracy, better compliance, and stronger customer lock-in than horizontal alternatives.

AI in healthcare is predicted to reach a valuation of over $187 billion by 2035—around 17× the 2021 figure. Similar growth opportunities exist in other regulated industries where AI can automate complex, high-value workflows. The key is combining deep domain expertise with AI capabilities to solve problems that generic solutions cannot address effectively.

2. AI Infrastructure and Tools

The infrastructure layer presents significant opportunities. As AI workloads grow, demand for specialized chips, data center capacity, and development tools continues to outpace supply. Companies providing “picks and shovels” for the AI gold rush—observability platforms, model serving infrastructure, data labeling tools, and security solutions—are capturing significant value.

With $18 billion in enterprise spending on AI infrastructure in 2025, this category represents a substantial and growing market opportunity. The infrastructure requirements for AI are distinct from traditional cloud computing, creating opportunities for specialized providers who understand the unique demands of AI workloads.

3. AI-Enabled Services

Professional services firms have an opportunity to help enterprises navigate AI adoption. Consulting, implementation, and managed services for AI are growing rapidly as organizations seek expertise to bridge the gap between AI potential and practical deployment. The complexity of AI implementation creates sustained demand for expert guidance.

Organizations that can combine domain expertise with AI capabilities can deliver transformative outcomes for clients while building sustainable competitive moats. The services opportunity extends beyond initial implementation to ongoing optimization, governance, and evolution of AI systems.

Case Studies and Success Stories

Real-world implementations demonstrate the tangible benefits that organizations are achieving through AI adoption. These case studies illustrate the practical application of AI across different industries and use cases.

Customer Service Transformation

Veteran organizations employing AI for over three years document a 25% reduction in cost per contact, with a 30% drop for those applying generative AI to one or two customer service use cases. These improvements come from automated response generation, intelligent routing, and AI-assisted agent support that reduces handle times while improving customer satisfaction.

The most successful implementations combine AI automation for routine inquiries with human agents for complex, emotionally sensitive issues. This hybrid approach delivers cost savings while maintaining service quality. Organizations are finding that customers often prefer AI assistance for simple tasks like order status checks and password resets.

Software Development Acceleration

AI coding tools are delivering measurable productivity gains. Development teams using AI assistants report 10× acceleration in build-test cycles, with AI agents handling routine coding tasks, test generation, and documentation. This acceleration allows teams to ship features faster while maintaining quality standards.

The impact extends beyond individual developer productivity to team dynamics and project management. With AI handling routine implementation, senior developers can focus on architecture and complex problem-solving, while junior developers ramp up faster with AI assistance. The result is more efficient teams and higher-quality software.

Enterprise Workflow Automation

Financial services firms are deploying AI agents that autonomously triage alerts and draft incident reports, reducing response times from hours to minutes. Sales operations teams use AI agents to qualify leads and manage entire customer journeys without handoffs, improving conversion rates and reducing sales cycle times.

Companies report 70% automation of tier-1 support inquiries through AI agents, allowing human agents to focus on complex issues that require empathy and judgment. The key to success is designing clear escalation paths and maintaining human oversight for high-stakes decisions.

Future Outlook and Predictions

Looking ahead to 2027-2030, several trends will shape the evolution of the AI market. These predictions are based on current trajectories, expert analysis, and the underlying technological and economic drivers of AI development.

Continued Market Growth

The AI market is projected to maintain its rapid growth trajectory. With a CAGR of 29.2%, the market will reach approximately $1.4 trillion by 2030 and $3.5 trillion by 2033. This growth will be driven by continued enterprise adoption, new application categories, and the expansion of AI capabilities into domains currently resistant to automation.

The growth will not be evenly distributed. AI-native companies will likely capture disproportionate value, while organizations that fail to adapt may see their markets disrupted. The gap between AI leaders and laggards will widen, creating a “winner-take-most” dynamic in many industries.

AGI Timeline Debates

The timeline for artificial general intelligence (AGI) remains hotly debated. Some experts predict AGI could arrive by 2026-2027, while others believe it remains decades away. What is clear is that AI capabilities are advancing rapidly, with each generation of models demonstrating significant improvements in reasoning, creativity, and task completion.

Whether or when AGI arrives, the trend toward more capable AI systems is undeniable. Organizations should prepare for a future in which AI can handle increasingly complex cognitive tasks, while recognizing that human judgment, creativity, and empathy will remain essential for the foreseeable future.

Regulatory Maturation

AI regulation will mature significantly over the next five years. The EU AI Act will be fully implemented, the U.S. will likely pass comprehensive AI legislation, and international frameworks for AI governance will emerge. Organizations that invest in responsible AI practices now will be better positioned for this regulatory evolution. The companies that treat compliance as a competitive advantage rather than a burden will thrive in this environment.

Regulatory clarity will also unlock investment in AI applications that are currently constrained by uncertainty. Healthcare, financial services, and other regulated industries will accelerate AI adoption once clear rules are established. This regulatory maturation will be a catalyst for the next wave of AI growth.

Workforce Transformation

AI will continue to transform the workforce, automating routine cognitive tasks while creating new roles in AI development, governance, and human-AI collaboration. The organizations that thrive will be those that successfully reskill their workforce and redesign workflows to leverage human-AI collaboration. This transformation will require significant investment in training and change management.

The nature of work itself will evolve. As AI handles more routine tasks, human workers will focus on activities that require creativity, emotional intelligence, and complex judgment. This shift will require new skills, new organizational structures, and new approaches to talent development. Organizations that proactively manage this transition will have a significant advantage over those that react to it.

AI Democratization

The democratization of AI will accelerate, with powerful AI capabilities becoming accessible to smaller organizations and individual developers. Open-source models, low-code AI platforms, and AI-as-a-service offerings will lower the barriers to entry. This democratization will unleash a wave of innovation as entrepreneurs and small businesses apply AI to problems that were previously the domain of large enterprises with significant resources.

The implications for competition are significant. Industries that have been protected by high barriers to entry may face disruption from AI-enabled startups. Incumbents will need to innovate rapidly to maintain their positions. The pace of change will accelerate, and the ability to adapt will be a critical determinant of success.

Key Takeaways

- The global AI market reached $539.5 billion in 2026 and is projected to grow to $3.5 trillion by 2033 at a 29.2% CAGR

- 88% of organizations now use AI in at least one business function, up from 55% in 2023

- Agentic AI represents the most significant trend, with autonomous agents moving from experimentation to production deployment

- Anthropic has emerged as a leader in enterprise LLM market share with 40%, challenging OpenAI’s dominance

- Enterprise spending on generative AI reached $37 billion in 2025, a 3.2× increase from 2024

- Key challenges include hallucinations, data quality, talent shortage, security risks, and regulatory fragmentation

- Organizations achieving the highest ROI focus on domain-specific applications and governance-first deployment approaches

- AI is projected to generate $22.3 trillion in cumulative global economic impact by 2030

- 53% of new unicorn births in 2025 were AI companies, up from just 6% in 2015

- The shift from AI experimentation to production deployment is the defining enterprise trend of 2026

Conclusion

The AI market in 2026 represents a watershed moment in the technology’s evolution. What was once the domain of research labs and technology enthusiasts has become a fundamental driver of business strategy and economic growth. The $539.5 billion market size, the 88% enterprise adoption rate, and the $37 billion in generative AI spending all point to a technology that has crossed the chasm from early adoption to mainstream deployment.

However, the journey is far from complete. The gap between experimentation and scaled deployment, the challenges of hallucinations and bias, and the complexities of regulatory compliance all represent significant hurdles that organizations must overcome. The companies that navigate these challenges successfully will capture disproportionate value in the coming years.

For business leaders, the message is clear: AI is no longer optional. It is a fundamental capability that will determine competitive position in virtually every industry. The question is not whether to adopt AI, but how to adopt it effectively, responsibly, and at scale. The organizations that answer this question well will define the next era of business.

For investors, the AI market offers unprecedented opportunities, but also significant risks. The winners will be those who can distinguish between genuine innovation and hype, between sustainable competitive advantages and temporary market dynamics. The due diligence required for AI investments is evolving rapidly as the technology and market mature.

For developers and technologists, the AI revolution creates opportunities to build solutions that were previously impossible. The tools and platforms available today enable small teams to accomplish what would have required massive resources just a few years ago. The barriers to innovation have never been lower, and the potential impact has never been greater.

As we look toward 2030 and beyond, one thing is certain: AI will continue to reshape the global economy, redefine the nature of work, and create new possibilities for human achievement. The $539.5 billion market of 2026 is just the beginning. The organizations, investors, and individuals who understand and act on this reality will be the architects of the AI-powered future.

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size & Share Report, 2026-2033

- Statista Market Insights – AI Market Forecast 2020-2031

- Precedence Research – Artificial Intelligence (AI) Market Size, Share and Trends 2026 to 2035

- McKinsey & Company – State of AI 2025 Report

- Menlo Ventures – 2025: The State of Generative AI in the Enterprise

- IBM Think – AI Tech Trends and Predictions for 2026

- Microsoft Source – What’s Next in AI: 7 Trends to Watch in 2026

- OECD – Venture Capital Investments in Artificial Intelligence Through 2025

- MIT Sloan Management Review – Five Trends in AI and Data Science for 2026

- Crunchbase News – Q1 2026 Venture Funding Records

- Exploding Topics – AI Market Size Statistics (2025-2032)

- TechnologyChecker – AI Market Size Statistics 2026

- Master of Code – 350+ Generative AI Statistics 2026

- Deloitte – The State of AI in the Enterprise 2026

- IDC – Global AI Economic Impact Analysis 2025-2030