The creator economy has evolved from a side hustle phenomenon into a legitimate $314 billion global industry. What started as a playground for hobbyists posting cat videos has transformed into one of the most significant economic shifts of our generation. In 2026, being a content creator isn’t just a career path—it’s a business model that rivals traditional media in scale and influence.

Here’s the reality that should make every marketer, investor, and entrepreneur pay attention: creator platforms are projected to surpass traditional media in advertising revenue for the first time in 2026. This isn’t a trend. It’s a fundamental restructuring of how content is produced, distributed, and monetized. The implications extend far beyond the creators themselves to reshape advertising, entertainment, education, and commerce in ways we’re only beginning to understand.

The transformation has been rapid and profound. Five years ago, the creator economy was viewed as a niche phenomenon—a collection of YouTubers and Instagram influencers making side income from brand deals. Today, it encompasses over 207 million creators worldwide, spans every conceivable content category, and generates hundreds of billions in economic value. The question is no longer whether the creator economy matters, but how to participate in it effectively.

What makes this moment particularly significant is the convergence of several factors: the maturation of social media platforms, the development of sophisticated monetization tools, the rise of AI-powered content creation, and a fundamental shift in consumer behavior toward authentic, creator-driven content. Together, these forces have created an economic ecosystem that supports professional creators at unprecedented scale.

Market Overview: The $314 Billion Creator Economy

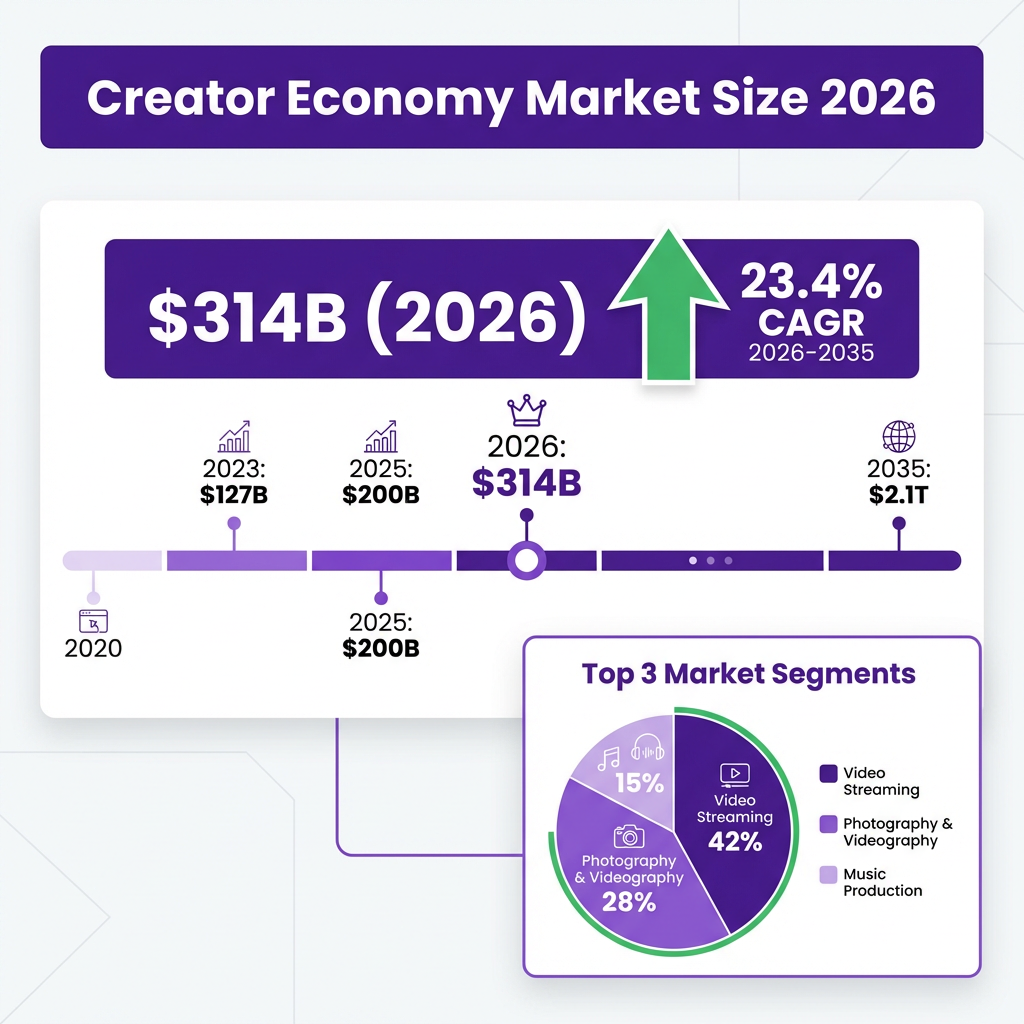

The global creator economy market has reached an estimated value of $314 billion in 2026, up from $254.4 billion in 2025. This represents a compound annual growth rate (CAGR) of 23.41% that is projected to continue through 2035, when the market could reach a staggering $2.08 trillion. These aren’t speculative numbers—they’re backed by consistent investment flows, platform revenue growth, and the professionalization of creator businesses across every major economy.

North America currently dominates the creator economy landscape, accounting for 35% of global market share in 2025. The region’s mature digital advertising ecosystem, high internet penetration, and established creator infrastructure give it a significant advantage. The United States alone represents the largest single market, with creators based in Los Angeles, New York, and Miami commanding premium rates for brand partnerships and building sophisticated media businesses that rival traditional entertainment companies.

However, the Asia Pacific region is emerging as the fastest-growing market, driven by massive creator populations in India, China, Japan, and South Korea. The Indian market alone is experiencing explosive growth, supported by a $1 billion government fund launched in March 2025 specifically for content creators and creative technology development. This government backing signals recognition at the highest levels that the creator economy represents a significant economic opportunity and employment generator for the country’s massive youth population.

The European market presents a more fragmented picture, with strong creator ecosystems in the UK, Germany, and France, but varying regulatory environments that impact growth. The EU’s Digital Services Act has introduced new compliance requirements that creators and platforms must navigate, creating both challenges and opportunities for market participants.

The market segmentation reveals where value is being created. Video streaming platforms command the largest share at 42%, followed by photography and videography services at 28%, and music production at 15%. This distribution reflects the visual nature of modern content consumption and the platforms that have successfully monetized attention. The dominance of video underscores a fundamental shift in how people consume information and entertainment—moving from text-based to visual-first experiences that demand more sophisticated production capabilities.

Looking at the revenue channels, advertising remains the dominant monetization method, but subscriptions are growing at the fastest rate. This shift toward recurring revenue models represents a maturation of the creator economy—moving from transactional brand deals to sustainable business models that don’t depend entirely on algorithm changes or platform policies. The subscription growth rate of over 25% annually suggests creators are successfully building direct relationships with their audiences that transcend platform boundaries.

The historical trajectory tells a compelling story. In 2023, the creator economy was valued at approximately $127 billion. By 2025, it had grown to $254 billion—doubling in just two years. The projection of $314 billion for 2026 and $2.08 trillion by 2035 suggests we’re still in the early innings of this transformation. Goldman Sachs Research estimates the market could approach $500 billion by 2027, with a 10-20% compound annual growth rate for the global creator population. If these projections hold, the creator economy will become one of the largest sectors in the global economy within a decade.

The end-use segmentation provides additional insight into market dynamics. Individual content creators dominated the market in 2025, but the businesses and brands segment is expected to grow at the fastest CAGR during the forecast period. This shift reflects the increasing integration of creator strategies into mainstream corporate marketing, as well as the emergence of creator-led businesses that operate at institutional scale with professional teams, sophisticated technology stacks, and diversified revenue models.

Key Statistics and Data Points

The creator economy by the numbers reveals an ecosystem of unprecedented scale and diversity. Understanding these metrics is essential for anyone looking to participate in, invest in, or compete with this growing market. The data points below paint a picture of an industry that has moved beyond novelty to become a core component of the digital economy.

Creator Population Statistics

The global creator population has reached approximately 207 million people worldwide who identify as content creators. This includes everyone from casual hobbyists to full-time professionals operating multi-million dollar media businesses. YouTube alone hosts 61.8 million creators, making it the largest single platform ecosystem. TikTok and Instagram each support tens of millions of creators, though exact numbers vary by how “creator” is defined.

What’s more significant than the total number is how creators are organizing their work. According to Circle’s 2026 Community Trends Report, 48% of creators operate as solo entrepreneurs, running their communities, content production, and monetization entirely alone. Another 19% lead small, community-focused teams that blend content creation with operations and member support. Only 15% work as hired community managers or strategists within larger creator-led or brand-led communities.

This solo-operator dominance has implications for the tools and services that succeed in the creator economy. Creators need all-in-one solutions that handle everything from content scheduling to payment processing to community management—because they’re doing it all themselves. The success of platforms like Beacons, Stan Store, and Linktree reflects this need for unified creator business infrastructure that simplifies complex operations.

The creator archetypes have also evolved significantly. We now see distinct categories emerging: the solo creator running everything independently, the small team leader managing a community-focused operation, the community manager working within larger organizations, and the creator-entrepreneur building diversified media businesses. Each archetype has different needs, revenue models, and growth trajectories that shape how they interact with platforms and brands.

Monetization and Revenue Data

The ways creators make money have diversified dramatically. The most significant shift in 2026 is the move toward owned, recurring revenue streams. According to Circle’s research, 88% of community-building creators now monetize through paid memberships—up from just 54% the previous year. This represents a fundamental rebalancing of creator business models away from platform-dependent income toward sustainable, owned revenue.

Other monetization methods show the breadth of creator revenue opportunities: 53% sell courses, 51% offer coaching or services, 37% sell digital products, 22% generate affiliate revenue, and only 18% rely primarily on brand sponsorships. The ordering here is instructive—sponsorships, once the holy grail of creator monetization, now represent a minority revenue source for professional creators who have diversified their income streams.

U.S. annual creator economy ad spend reached $37.1 billion in 2026 according to the IAB. This figure encompasses influencer marketing budgets, platform advertising, and creator-led campaigns. The growth rate of creator marketing spend continues to outpace traditional advertising channels, with 74% of marketers planning to increase their investment in creator-led strategies. This represents a fundamental shift in how brands allocate marketing budgets.

The average creator income varies dramatically by tier. Nano-influencers (under 10K followers) might earn a few hundred dollars per sponsored post, while micro-influencers (10K-100K) can command $1,000-5,000 per partnership. Mid-tier creators (100K-500K) often earn $5,000-25,000 per campaign, and mega-influencers (1M+) can charge $50,000 or more for major brand partnerships. However, these figures represent only sponsorship revenue—total income often includes multiple streams that can significantly exceed these numbers.

Platform Performance Metrics

Platform dynamics reveal where creator attention and investment are flowing. Instagram leads in brand and agency preference, with the platform being named the most-used channel for creator marketing in 2026. TikTok follows closely, particularly for reaching younger demographics. YouTube, despite being the monetization king for creators through its Partner Program, ranks third in brand preference—suggesting a disconnect between where creators earn and where brands prefer to spend.

Engagement rates vary significantly by creator tier and platform. Micro-influencers on Instagram average 3.2% engagement, while nano-influencers can achieve 5-8%. Mega-influencers typically see 0.8-2% engagement. This inverse relationship between reach and engagement is driving a shift toward mid-tier creators (100K-500K followers) who offer the optimal balance of scale and connection.

CreatorIQ data shows that creator content now generates 11 times more impressions and 14 times more engagements than brand-owned content. This performance differential explains why brands are increasingly prioritizing creator partnerships over traditional advertising—even as they grapple with measurement and attribution challenges. The data suggests creator content has an 82% probability of outperforming standard brand ads without the paid partnership label.

Platform-specific metrics reveal additional insights. YouTube creators earn through the Partner Program based on CPM (cost per thousand views), with rates varying by niche, geography, and seasonality. Gaming content might earn $2-5 CPM, while finance content can command $15-30 CPM. TikTok’s Creator Fund pays based on views and engagement, though creators report rates significantly lower than YouTube. Instagram monetization remains primarily brand-driven, with the platform’s native monetization tools still developing.

Investment and Funding Activity

Venture capital continues to flow into creator economy infrastructure. AI content creation tools alone raised $1.2 billion in 2025, reflecting investor conviction that artificial intelligence will reshape how content is produced. Top-funded creator economy startups include ShopMy ($169M raised), GRIN ($145M), Mighty Networks ($66M), and Beacons ($30M).

The funding landscape has matured beyond early-stage bets on consumer apps. Today’s investments focus on B2B infrastructure—tools for creator management, analytics, payment processing, and community building. This shift indicates the market’s evolution from a consumer phenomenon to a professionalized industry requiring enterprise-grade solutions.

Notable VC firms active in the creator economy include Andreessen Horowitz (investor in Beacons, Clubhouse), Bessemer Venture Partners (ShopMy, GRIN), and Bain Capital Ventures. These firms recognize that the creator economy represents a fundamental shift in how media is produced and consumed—and they’re betting billions that this shift is permanent.

Major Trends Shaping the Creator Economy in 2026

Seven major trends are defining the creator economy in 2026. Understanding these shifts is essential for creators looking to build sustainable businesses and for brands seeking effective partnerships. These trends represent both opportunities and challenges that will determine who succeeds in this rapidly evolving landscape.

1. AI-Powered Content Creation

Artificial intelligence has moved from novelty to necessity in the creator economy. Tools like ChatGPT, Jasper, Copy.ai, RunwayML, and Adobe Sensei are now standard parts of the creator tech stack. AI enables everything from scriptwriting and video editing to voice synthesis and translation—allowing creators to produce more content, faster, at higher quality than ever before.

The impact extends beyond productivity gains. AI-generated virtual influencers are emerging as a new category of creator, enabling authentic storytelling without real-person constraints. Voice synthesis and translation tools allow podcasts and videos to be localized for global audiences instantly. For brands, this means creators can produce customized content at scales previously impossible.

However, platforms are establishing clear boundaries. LTK has explicitly stated their platform is only for real human creators, not AI influencers. The FTC has tightened enforcement on AI disclosure requirements, and the EU’s Digital Services Act now applies to AI-generated creator content. The message is clear: AI is a tool for creators, not a replacement for them.

The most successful creators in 2026 are those who have integrated AI into their workflows without losing their human touch. They use AI for research, first drafts, and optimization while maintaining authentic voice and personal connection with their audiences. This hybrid approach—AI efficiency plus human creativity—represents the winning formula.

2. Community-Led Business Models

The most significant structural shift in the creator economy is the move from audience-building to community-building. According to Circle’s 2026 report, 69% of creators say community will become a bigger part of their strategy, signaling a long-term move toward owned, community-led business models that prioritize depth over breadth.

This shift is driven by the recognition that social media followers are rented, not owned. Platform algorithm changes can decimate reach overnight. Community members, by contrast, represent a direct relationship that platforms can’t sever. Recurring, community-based revenue now sits at the center of creator business models, while sponsorships and affiliate income play increasingly peripheral roles.

The data supports this strategy. Circle now supports over 18,000 active communities, with 56% of creators having launched their communities in the last two years. Interestingly, 44% of communities have between 1 and 100 members—suggesting that many creators are intentionally building small, high-value communities rather than chasing massive scale.

The community model changes the creator-audience relationship from transactional to transformational. Instead of creating content for passive consumption, community-led creators facilitate member progress, connection, and outcomes. This deeper engagement translates to higher lifetime value and more sustainable businesses that can weather platform changes.

3. The Rise of Mid-Tier Creators

While nano-influencers (under 10K followers) remain valuable for hyper-local campaigns, the real performance sweet spot in 2026 is mid-tier creators with 100K to 500K subscribers. These creators offer the optimal combination of reach and engagement, often achieving 3-5% engagement rates while maintaining authentic connections with their audiences.

Brands are recognizing this dynamic. Micro- and nano-influencers will claim 45.5% of influencer marketing spending in 2026, but mid-tier creators command premium rates due to their proven conversion performance. For creators, this validates the strategy of building engaged communities rather than chasing vanity metrics.

The mid-tier advantage comes from several factors. These creators have achieved enough scale to generate meaningful reach while maintaining the personal connection that drives conversion. They’re large enough to have professional infrastructure but small enough to maintain authentic relationships with their audiences. And they typically have more experience and better track records than smaller creators.

4. Platform Diversification

Smart creators are no longer building on single platforms. The top business goal for 28% of creators is expanding to new platforms, reflecting a hedging strategy against algorithm volatility and policy changes. Top creators in 2026 operate as diversified media businesses with presence across YouTube, TikTok, Instagram, podcasts, newsletters, and owned communities.

This diversification extends to monetization. The creators best positioned for long-term success combine multiple revenue streams: platform ad revenue, brand partnerships, affiliate commissions, course sales, coaching services, digital products, and community memberships. When one channel underperforms, others compensate.

The platform diversification strategy requires significant operational complexity. Creators must adapt content formats, posting schedules, and engagement strategies for each platform while maintaining a cohesive brand identity. Tools that simplify cross-platform management are becoming essential infrastructure for professional creators.

5. Performance-Based Creator Deals

The era of flat-fee sponsorships is ending. Brands increasingly want accountability, and creators with strong conversion data are commanding premiums. Performance-based deals—where creator compensation ties to measurable outcomes like sales, signups, or app installs—are becoming the standard for professional partnerships.

This shift benefits creators who can demonstrate ROI. Those with trackable affiliate revenue, conversion-optimized content, and engaged audiences can negotiate better terms than creators with impressive follower counts but no proof of influence. The data advantage is becoming the competitive advantage.

For brands, performance-based models reduce risk and improve accountability. Instead of paying for potential reach, brands pay for actual results. This alignment of incentives creates more sustainable partnerships and better campaign outcomes. The brands that master performance-based creator partnerships will outperform those stuck in traditional sponsorship models.

6. Video-First Content Dominance

Video content remains the dominant format in the creator economy, with video streaming platforms commanding 42% of market share. Short-form video (TikTok, Reels, Shorts) drives discovery, while long-form video (YouTube, podcasts) builds deep audience relationships and generates sustainable ad revenue.

The integration of these formats is key. Successful creators use short-form content to attract new audiences, then funnel engaged viewers to long-form content where monetization is more effective. This full-funnel approach maximizes both reach and revenue.

Live streaming has emerged as a particularly valuable format, enabling real-time engagement and monetization through tips, donations, and live shopping. Platforms like Twitch, YouTube Live, and TikTok LIVE have built significant businesses around live creator content. The authenticity and immediacy of live content creates connection that recorded content cannot match.

7. Professionalization and Business Infrastructure

Creators are no longer just content producers—they’re entrepreneurs, brand builders, and media companies. This professionalization requires business infrastructure: contracts, accounting, legal protection, team management, and strategic planning. The gap between amateur creators and professional creator businesses is widening.

Boutique agencies and management firms have emerged to support this transition, helping creators turn audiences into sustainable businesses. Tools for contract negotiation, rights management, payment processing, and analytics have become essential infrastructure. The creators who invest in these capabilities will outcompete those who don’t.

The professionalization trend extends to creator education. Courses, coaching programs, and communities focused on creator business skills have proliferated. The most successful creators invest heavily in learning—about business strategy, marketing, finance, and operations. The creator who treats their work as a business consistently outperforms the creator who treats it as a hobby.

Key Players and Competitive Landscape

The creator economy ecosystem has matured into a complex landscape of platforms, tools, agencies, and infrastructure providers. Understanding the key players is essential for navigating this market effectively. The competitive dynamics are shifting as the industry matures and consolidation begins.

Platform Giants

YouTube remains the monetization leader for creators through its Partner Program, which shares ad revenue directly with content creators. The platform’s strength is its mature advertising infrastructure and long-form content format that supports deep audience relationships. YouTube Shorts has successfully challenged TikTok in short-form video, giving creators a unified platform for both content types.

YouTube’s advantage extends beyond monetization. The platform’s search functionality makes content discoverable long after publication, creating evergreen value that ephemeral platforms cannot match. Educational and how-to content particularly benefits from this longevity, with creators earning from videos published years ago.

TikTok dominates short-form video and cultural trendsetting. Despite regulatory challenges in the U.S., the platform’s algorithm remains unmatched for content discovery. TikTok Shop has added e-commerce capabilities, allowing creators to monetize through product sales directly within the app. The platform’s cultural influence extends far beyond its user base, with TikTok trends regularly crossing into mainstream media.

Instagram has evolved from photo-sharing to a comprehensive creator platform with Reels, Stories, and shopping features. The platform’s strength is its integration with Meta’s advertising infrastructure, making it attractive for brand partnerships. Instagram’s creator marketplace simplifies brand-creator connections.

LinkedIn has emerged as a surprising winner in the B2B creator economy. Following the surge in B2B creator marketing, more consumer brands are exploring life-and-work-adjacent campaigns on the platform. LinkedIn’s professional context commands premium rates for business-focused creators.

Infrastructure and Tool Providers

Creator economy infrastructure has become a major investment category. CreatorIQ, GRIN, and Aspire provide enterprise-grade creator management and analytics. These platforms help brands discover creators, manage campaigns, track performance, and measure ROI at scale.

Link-in-bio tools like Beacons, Linktree, and Stan Store have become essential for creator monetization. These platforms aggregate a creator’s various offerings into a single link that can be shared across social profiles. The best of these tools also provide analytics, payment processing, and email capture.

Community platforms like Circle, Mighty Networks, and Skool enable creators to build owned communities outside of social media platforms. These tools provide the infrastructure for paid memberships, courses, discussions, and events.

ShopMy ($169M raised) has emerged as a leader in creator-driven shopping, connecting top creators with leading brands for affiliate partnerships. The platform’s curated approach has attracted high-value creators and premium brands.

Agencies and Management

The agency landscape is consolidating. The most successful firms combine talent management, brand services, and technology under one roof. This integrated model allows agencies to offer end-to-end creator marketing services.

AI is becoming an operating layer for these agencies, connecting talent data, historical performance, audience behavior, and brand outcomes. Customization at scale—once impossible—is now achievable through intelligent systems.

The top creator agencies now function like talent management companies in traditional entertainment, handling everything from contract negotiation to brand development to long-term career strategy.

Challenges and Pain Points

Despite its growth, the creator economy faces significant challenges that creators, platforms, and brands must navigate. Understanding these pain points is essential for developing strategies that can succeed in this complex environment.

1. Platform Algorithm Volatility

According to CreatorIQ, platform algorithm changes are the top barrier to business growth for creators worldwide. A single algorithm update can decimate a creator’s reach and revenue overnight. This dependence on platform decisions creates fundamental business risk.

The challenge is particularly acute for creators who built their businesses on a single platform. The creators who survive algorithm shifts are those who treat platforms as acquisition channels rather than business foundations.

Algorithm opacity compounds the problem. Creators often don’t understand why their content performs well or poorly, making optimization difficult. Platform changes can happen without warning, leaving creators scrambling to adapt.

2. Inconsistent Brand Deal Flow

Lack of consistent brand deals ranks as the second-biggest barrier to growth. The feast-or-famine nature of sponsorship revenue makes financial planning difficult.

45% of creators with over 100,000 followers prefer long-term brand partnerships over one-off agreements. Brands that can offer consistent, relationship-based partnerships will win preferential access to top creator talent.

The inconsistency problem is particularly acute for smaller creators who lack representation and established brand relationships. These creators often spend significant time on outreach and negotiation for deals that may never materialize.

3. Professional Infrastructure Gaps

Most creators enter the industry without access to professional guidance. Pricing work correctly and understanding usage rights remain major pain points.

This infrastructure gap is being addressed by a new generation of creator-focused service providers, but access remains uneven. Creators with management representation have significant advantages.

Burnout is a related challenge. 48% of creators operate solo, managing content production, community management, business operations, and monetization alone. The workload is unsustainable for many.

4. Regulatory Requirements

Multiple countries have introduced creator economy regulations. The FTC has tightened enforcement on undisclosed sponsorships. Brand safety has become more critical, with 72% of enterprise brands saying it has become more important.

The regulatory landscape is still evolving, creating uncertainty for creators and brands alike. What’s acceptable today may not be tomorrow.

Opportunities and Growth Strategies

Within these challenges lie significant opportunities for creators, brands, and platforms that can execute effectively.

1. Building Owned Communities

The most significant opportunity is the shift from rented audiences to owned communities. 88% of community-building creators monetize through paid memberships.

Community building requires a different mindset than audience building. Instead of optimizing for views, community-focused creators optimize for member outcomes.

2. AI-Augmented Content Production

AI tools offer creators the ability to produce more content, faster, at higher quality. For brands, AI-augmented creators can deliver customized content at scale.

3. Performance-Based Partnerships

The shift toward performance-based deals creates opportunities for creators who can demonstrate ROI.

Case Studies and Success Stories

Netflix’s Creator Content Strategy

Netflix has emerged as a major player through strategic content licensing from creators like Ms. Rachel and Mark Rober.

Meta’s Wearables Integration

Meta has been promoting Ray-Ban Meta smart glasses through creator partnerships, illustrating how hardware companies leverage creators.

Community-Led Creator Businesses

Circle’s data reveals that 56% of creators launched their communities in the last two years. Top creators now operate as diversified media businesses.

Future Outlook and Predictions

Industry analysts project the creator economy will reach $500-600 billion by 2030, with some estimates suggesting $2 trillion by 2035.

The platforms best positioned for success will offer scale, capital, AI-powered recommendation engines, effective monetization tools, robust analytics, and integrated e-commerce.

The gap between amateur and professional creator businesses will widen. AI will play an increasingly central role as an operating layer for creator businesses.

Deep Dive: Creator Economy Business Models

Understanding the various business models within the creator economy is essential for both creators and brands looking to participate effectively. The landscape has evolved far beyond simple brand sponsorships to encompass sophisticated revenue strategies that mirror traditional media companies.

The Subscription-First Model

The subscription-first model has emerged as the gold standard for sustainable creator businesses. By building direct relationships with audiences through paid memberships, creators generate predictable recurring revenue that isn’t subject to algorithm changes or platform policies. This model requires significant investment in community building and value delivery, but the returns are substantial.

Successful subscription-based creators typically offer tiered membership levels, with basic access at lower price points and premium offerings—including exclusive content, direct access, and specialized resources—at higher tiers. The key is delivering ongoing value that justifies the recurring charge.

The Productized Creator Model

Some creators have successfully productized their expertise, creating digital products that scale beyond their time. Courses, templates, ebooks, and software tools allow creators to serve thousands of customers without proportional time investment. This model offers high margins and scalability but requires significant upfront investment in product development.

The most successful productized creators identify specific problems their audiences face and create solutions that deliver clear, measurable outcomes. The product becomes an extension of the creator’s brand and expertise, reinforcing their authority while generating revenue.

The Media Company Model

Top creators are increasingly operating as media companies, building teams and infrastructure that enable scale. These operations include content production teams, business development staff, and specialized roles for community management, analytics, and strategy. The media company model treats the creator as a brand and intellectual property asset.

This model requires significant capital and operational expertise but offers the highest ceiling for growth. Creators like MrBeast have demonstrated that creator-led media companies can achieve valuations and revenues comparable to traditional media organizations.

Regional Analysis: Creator Economy by Geography

The creator economy manifests differently across regions, reflecting local market conditions, regulatory environments, and cultural preferences. Understanding these regional variations is essential for global strategies.

North America

North America remains the most mature creator economy market, with sophisticated infrastructure, high monetization rates, and established professional standards. The region leads in creator tools, agency services, and platform innovation. However, market saturation in certain niches has increased competition and raised barriers to entry for new creators.

The U.S. market is characterized by high CPM rates on platforms like YouTube, premium brand partnership opportunities, and a robust ecosystem of creator services. Canada offers similar conditions with slightly lower competition, making it attractive for creators targeting English-speaking audiences.

Europe

Europe presents a fragmented but growing creator economy landscape. The UK leads the region with a mature market similar to North America. Germany and France have strong domestic creator ecosystems, while Nordic countries punch above their weight in per-capita creator activity.

The EU’s regulatory environment, including GDPR and the Digital Services Act, creates compliance complexity but also establishes standards that protect creators and consumers. The regulatory clarity, once navigated, provides a stable operating environment.

Asia Pacific

The Asia Pacific region represents the highest growth potential, driven by massive populations, increasing internet penetration, and cultural enthusiasm for creator content. India has emerged as a particularly dynamic market, with government support and a large, young population driving rapid expansion.

China operates a distinct creator ecosystem centered on domestic platforms like Douyin and Xiaohongshu. While largely separate from the global creator economy, China’s market offers lessons in live commerce and social shopping that are increasingly relevant worldwide.

Southeast Asian markets including Indonesia, Thailand, and Vietnam are experiencing rapid creator economy growth, often leapfrogging traditional media development. Mobile-first consumption patterns and high social media engagement create fertile ground for creator businesses.

The Future of Creator-Brand Partnerships

The relationship between creators and brands continues to evolve, moving from transactional sponsorships to strategic partnerships that deliver mutual value. Understanding this evolution is essential for both sides.

From Sponsorship to Collaboration

The most successful creator-brand relationships in 2026 look more like collaborations than sponsorships. Brands are increasingly involving creators in product development, marketing strategy, and even business decisions. This deeper integration creates more authentic content and better business outcomes.

Creators are becoming brand advisors, equity holders, and long-term partners rather than one-off promoters. This shift reflects the recognition that creators understand their audiences better than traditional marketers and can provide insights that drive product-market fit.

Measurement and Attribution

The measurement of creator marketing impact has improved significantly. Advanced analytics platforms now track the full customer journey from creator content to purchase, providing clear ROI data. This measurement capability enables performance-based partnerships and justifies increased investment in creator channels.

However, attribution remains challenging, particularly for upper-funnel awareness campaigns. Brands are developing sophisticated multi-touch attribution models that account for creator influence across the customer journey. The brands that solve attribution will gain significant competitive advantage in creator partnerships.

Long-Term Partnerships

The trend toward long-term creator-brand partnerships reflects the recognition that sustained collaboration delivers better results than one-off campaigns. Long-term partnerships allow creators to develop deeper product knowledge, create more authentic content, and build genuine advocacy.

For creators, long-term partnerships provide income stability and reduce the burden of constant new business development. For brands, they ensure consistent presence with target audiences and access to creator insights and feedback. The most successful partnerships span years rather than months.

Conclusion: The Creator Economy in Context

The creator economy of 2026 represents a fundamental shift in how media is produced, distributed, and consumed. What began as a democratization of content creation has evolved into a sophisticated economic ecosystem that supports millions of professional creators and generates hundreds of billions in value.

The trends shaping the creator economy—AI integration, community-led business models, platform diversification, and professionalization—suggest continued growth and maturation. The creators and brands that adapt to these trends will thrive; those that don’t will struggle to compete.

For creators, the message is clear: treat your work as a business, diversify your revenue streams, build owned communities, and invest in professional infrastructure. The era of the hobbyist creator isn’t ending, but the gap between hobbyists and professionals is widening.

For brands, the creator economy offers unprecedented opportunities to connect with audiences through authentic, engaging content. The key is moving beyond transactional sponsorships to genuine partnerships that deliver value for creators, audiences, and brands alike.

For investors, the creator economy infrastructure space offers significant opportunities. The tools and platforms that enable creator success are becoming essential business infrastructure with predictable revenue and strong growth trajectories.

The creator economy has come of age. It’s no longer an experimental channel or a niche phenomenon—it’s a central component of the digital economy that will shape media, marketing, and commerce for years to come. Understanding this ecosystem isn’t optional for anyone in digital business; it’s essential.

Technology Stack for Modern Creators

The modern creator operates with a sophisticated technology stack that enables professional content production, distribution, and monetization. Understanding this stack is essential for both creators building their operations and developers building tools for the creator economy.

Content Creation Tools

Content creation has been democratized by powerful, affordable tools. Video editing software like Adobe Premiere Pro, Final Cut Pro, and DaVinci Resolve enable broadcast-quality production. AI-powered tools like RunwayML and Descript automate editing tasks and enable new creative possibilities. Graphic design tools like Canva and Adobe Creative Suite make professional visual content accessible to non-designers.

The barrier to professional content creation has never been lower. A creator with a smartphone, basic editing software, and creativity can produce content that rivals traditional media production. This democratization has enabled the explosion of creator content and the rise of individual creators as media properties.

Distribution and Publishing Platforms

Distribution platforms form the foundation of the creator economy. YouTube, TikTok, Instagram, and other social platforms provide reach and monetization infrastructure. Newsletter platforms like Substack and Beehiiv enable direct audience relationships. Podcast hosting platforms like Spotify for Podcasters and Anchor simplify audio distribution.

The key for creators is maintaining presence across multiple platforms while directing audiences toward owned channels. This multi-platform approach maximizes reach while building durable audience relationships.

Monetization Infrastructure

Monetization tools have evolved significantly. Payment processors like Stripe and PayPal handle transactions. Membership platforms like Circle, Mighty Networks, and Patreon enable subscription revenue. E-commerce platforms like Shopify and Stan Store facilitate product sales. Affiliate networks connect creators with brands for commission-based partnerships.

The integration of these tools into cohesive creator business platforms has simplified monetization. A creator can now manage content, community, and commerce from unified dashboards that would have required multiple separate tools just a few years ago.

Analytics and Optimization

Data-driven decision making has come to the creator economy. Analytics platforms provide insights into audience behavior, content performance, and monetization effectiveness. A/B testing tools enable optimization of content and offers. Social listening tools help creators understand audience sentiment and trending topics.

The creators who leverage data effectively gain significant advantages. Understanding what content performs, when audiences are most engaged, and which monetization strategies work enables continuous improvement and growth.

Creator Economy Impact on Traditional Industries

The rise of the creator economy is disrupting traditional industries in profound ways. Understanding these disruptions helps predict future developments and identify opportunities.

Media and Entertainment

Traditional media companies are adapting to the creator economy reality. Television networks are licensing creator content. Movie studios are partnering with YouTube creators. Music labels are signing TikTok stars. The lines between traditional media and creator content are blurring.

This convergence creates opportunities for creators to reach mainstream audiences and for traditional media to access creator authenticity and audience relationships. The winners will be those who can bridge the gap between traditional production values and creator authenticity.

Advertising and Marketing

Creator marketing has become a core component of advertising strategy. Brands are shifting budgets from traditional advertising to creator partnerships. Ad agencies are building creator practices. Marketing technology is evolving to support creator campaigns.

This shift reflects the recognition that creator content outperforms traditional advertising in engagement and conversion. The challenge for brands is scaling creator partnerships while maintaining authenticity and measuring impact.

Education and Knowledge

Creators are becoming educators. Online courses, coaching programs, and educational content represent significant revenue streams for knowledgeable creators. This trend is democratizing education and creating new pathways for skill development.

Traditional educational institutions are taking notice. Universities are partnering with creators for courses. Corporate training programs are incorporating creator content. The creator-educator model is reshaping how knowledge is shared and monetized.

Commerce and Retail

Social commerce has become a major revenue stream for creators. Live shopping, affiliate marketing, and creator-branded products are generating billions in sales. Retailers are building creator partnerships to drive e-commerce growth.

The integration of content and commerce creates new shopping experiences. Consumers discover products through creator content and purchase without leaving the platform. This seamless experience is driving the growth of creator-led commerce.

Ethical Considerations in the Creator Economy

As the creator economy matures, ethical considerations become increasingly important. Creators, brands, and platforms must navigate complex questions about transparency, authenticity, and responsibility.

Transparency and Disclosure

Regulatory requirements around sponsorship disclosure have tightened globally. The FTC in the United States, ASA in the United Kingdom, and similar bodies worldwide require clear labeling of paid partnerships. Creators must navigate these requirements while maintaining content quality.

Beyond regulatory compliance, ethical creators prioritize transparency with their audiences. Clear disclosure of partnerships, honest reviews, and authentic recommendations build trust that sustains long-term creator careers.

Authenticity and Trust

The creator economy depends on authenticity. Audiences follow creators they trust, and that trust is easily broken by inauthentic partnerships or misleading content. Maintaining authenticity while monetizing is the central challenge for professional creators.

Successful creators are selective about partnerships, choosing brands that align with their values and audience interests. They maintain editorial independence and prioritize audience trust over short-term revenue. This long-term approach builds durable creator businesses.

Mental Health and Sustainability

Creator burnout has become a significant issue. The pressure to constantly produce content, maintain social media presence, and grow audiences takes a toll on mental health. The creator economy must address sustainability to retain talent.

Some creators are pushing back against hustle culture, setting boundaries, and prioritizing well-being. Platforms and brands are beginning to recognize the importance of creator sustainability. The future of the creator economy depends on creating conditions where creators can thrive long-term.

Key Takeaways

- The creator economy has reached $314 billion in 2026 and is projected to grow to $2.08 trillion by 2035.

- Creator platforms are projected to surpass traditional media in ad revenue in 2026.

- 88% of community-building creators monetize through paid memberships.

- AI is transforming content creation from manual craft to AI-augmented workflow.

- Mid-tier creators (100K-500K followers) represent the performance sweet spot.

- Platform algorithm volatility remains the top business risk for creators.

- The creator economy is professionalizing rapidly.

Sources and Citations

- Precedence Research – Creator Economy Market Size and Forecast 2026-2035: https://www.precedenceresearch.com/creator-economy-market

- Goldman Sachs Research – The creator economy could approach half-a-trillion dollars by 2027: https://www.goldmansachs.com/insights/articles/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027

- Circle – 2026 Community Trends Report: https://circle.so/blog/creator-economy-statistics

- Influencer Marketing Factory – 2026 Creator Economy Report: https://theinfluencermarketingfactory.com/creator-economy/

- CreatorIQ – State of Creator Marketing Report 2025-2026: https://www.creatoriq.com/white-papers/state-of-creator-marketing-trends-2026

- Future Market Insights – Creator Economy Market Report: https://www.futuremarketinsights.com/reports/creator-economy-market

- IAB – Creator Economy Ad Spend Data 2026

- Lindsey Gamble – Creator Economy Trends and Predictions 2026

- Forbes – The Creator Economy In 2026: The Era Of Consolidation

- eMarketer – Creator Economy 2026