Creator Economy Statistics 2026: Global Market Size, Data & Trends (Comprehensive Report)

The creator economy has evolved from a digital side hustle into a $323 billion global industry that is reshaping how content is produced, distributed, and monetized. With over 207 million content creators worldwide and U.S. advertising spend alone reaching $37 billion in 2025, this sector now represents one of the fastest-growing segments of the digital economy.

This comprehensive report compiles verified data from Grand View Research, Research and Markets, the IAB, and leading industry analysts to give you definitive statistics on market size, creator earnings, platform dynamics, regional breakdowns, and emerging trends. Whether you are a brand evaluating influencer partnerships, a creator building your business, or an investor tracking digital transformation, these numbers tell the story of an industry in rapid expansion.

Creator Economy Key Statistics at a Glance

- Global market size: $323.48 billion projected for 2026 (up from $255.66 billion in 2025)

- Long-term projection: $1.35 trillion by 2033-2035

- Annual growth rate: 23.3% CAGR (Grand View Research), with some analysts projecting up to 26.5%

- Total creators worldwide: 207-303 million active content creators

- High earners: Only 4% of creators earn over $100,000 annually

- Struggling creators: 50% make under $15,000 per year

- U.S. ad spend: $37 billion in 2025, growing 26% year-over-year

- North America market share: 34.2% of global creator economy revenue

- AI adoption: 84% of creators use AI tools in 2026

- Video dominance: Video streaming accounts for over 50% of creator economy revenue

Creator Economy Market Size & Growth

The creator economy growth trajectory is among the most aggressive in the global digital landscape. According to Grand View Research, the market was valued at $205.25 billion in 2024 and is projected to reach $1.35 trillion by 2033, representing a compound annual growth rate (CAGR) of 23.3%. This growth is fueled by several converging factors: the proliferation of high-performance digital infrastructure, the rise of AI-powered content creation tools, and the increasing professionalization of influencer marketing as a legitimate career path.

Research and Markets provides an even more aggressive near-term projection, estimating the market will grow from $255.66 billion in 2025 to $323.48 billion in 2026 at a CAGR of 26.5%. This exponential growth reflects the continuing shift toward creator-driven content consumption, platform expansion and feature development, and increasing brand investment in creator partnerships.

| Year | Market Size | Growth Rate | Source |

|---|---|---|---|

| 2023 | $250 billion | Baseline | Goldman Sachs |

| 2024 | $205.25 billion | Measured | Grand View Research |

| 2025 | $255.66 billion | 24.5% | Research and Markets |

| 2026 | $323.48 billion | 26.5% | Research and Markets |

| 2030 | $528+ billion | 23.3% CAGR | Multiple Sources |

| 2033 | $1.35 trillion | 23.3% CAGR | Grand View Research |

| 2034 | $1.49 trillion | 26.4% CAGR | Market.us |

| 2035 | $2.08 trillion | 22.4% CAGR | Precedence Research |

According to Market.us, the global creator economy market is expected to reach approximately $1.49 trillion by 2034, rising from an estimated $143 billion in 2024, driven by a robust CAGR of 26.4%. Precedence Research projects an even higher figure of $2.08 trillion by 2035, highlighting the tremendous variance in long-term forecasts while consistently pointing to massive expansion.

Regional Breakdown: Creator Economy by Geography

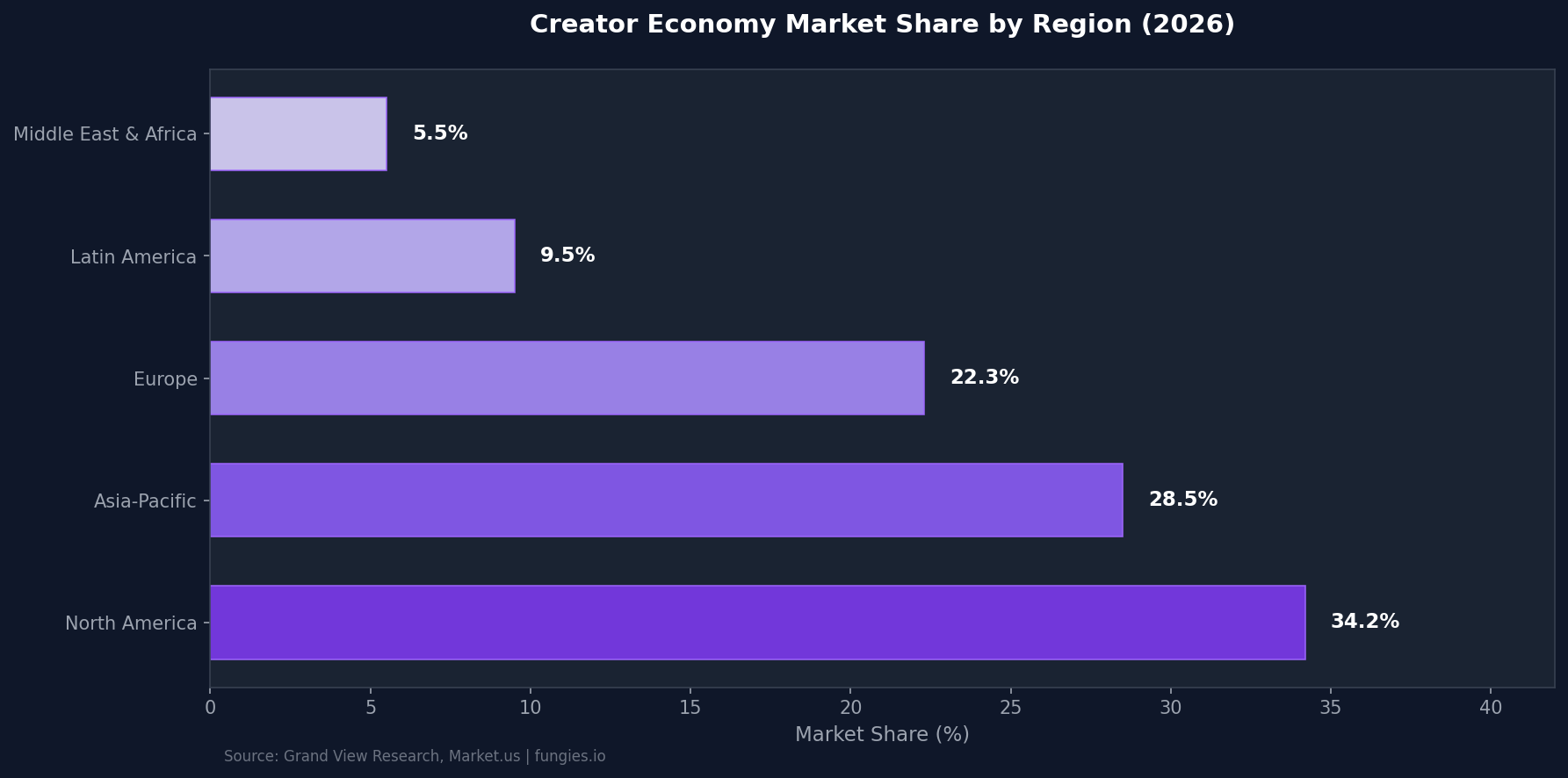

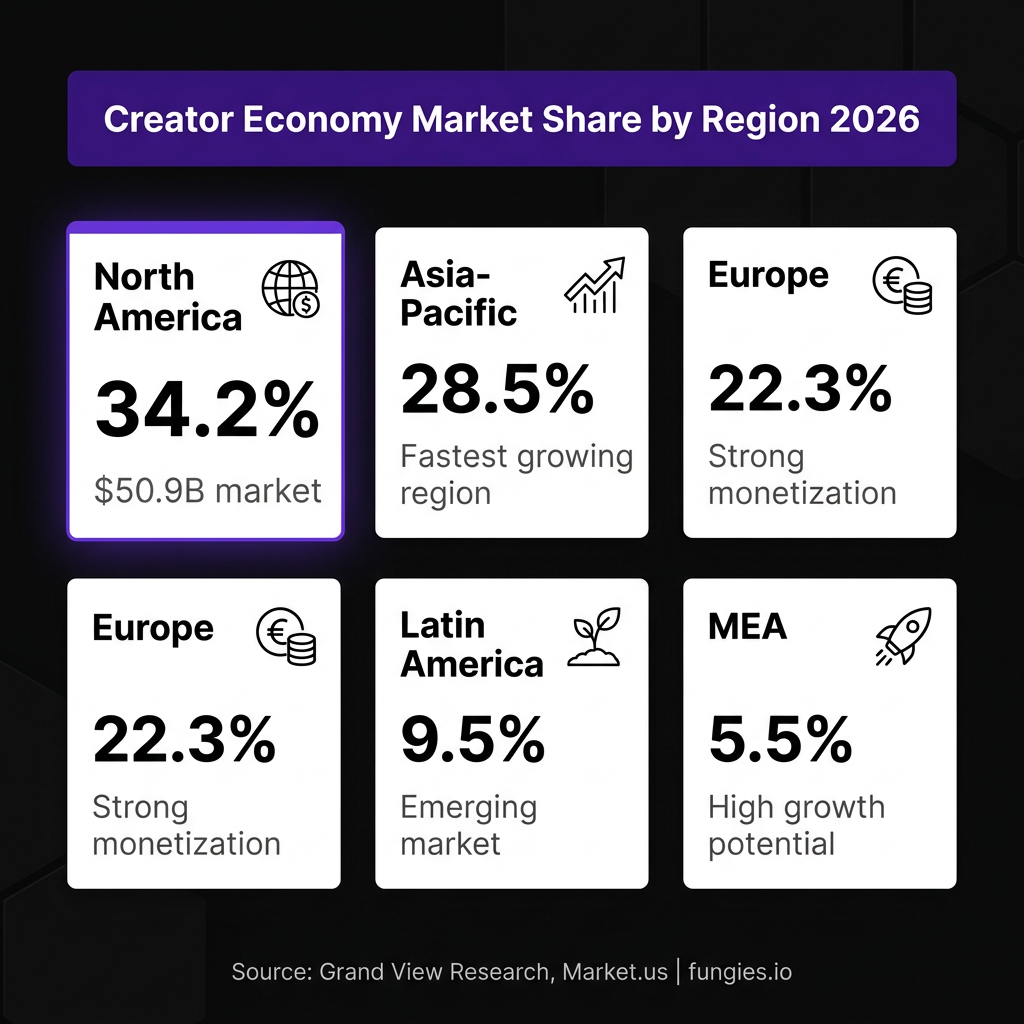

North America dominates the global creator economy, but Asia-Pacific is emerging as the fastest-growing region. The distribution of market share reflects varying levels of digital infrastructure maturity, platform penetration, and monetization sophistication across different geographies.

| Region | Market Share (2024-2026) | Key Characteristics | Growth Outlook |

|---|---|---|---|

| North America | 34.2% – 37.4% | Mature market, highest monetization rates | 19.5% CAGR through 2034 |

| Asia-Pacific | 28.5% | Fastest growing, mobile-first adoption | Highest growth potential |

| Europe | 22.3% | Strong regulatory framework, steady growth | Moderate expansion |

| Latin America | 9.5% | Emerging market, rising creator adoption | Above-average growth |

| Middle East & Africa | 5.5% | Early stage, high growth potential | Rapid expansion expected |

The United States alone represents a $50.9 billion market as of 2024, with projections pointing to $297.3 billion by 2034 at a 19.3% CAGR according to Grand View Research. North America’s dominance is attributed to early adoption of creator platforms and tools by influencers and individual creators, combined with higher advertising rates and more mature monetization infrastructure.

Asia-Pacific’s rapid growth is driven by massive user bases on platforms like TikTok (ByteDance), the proliferation of mobile-first content consumption, and increasing internet penetration across emerging economies. The region’s 28.5% market share represents a significant opportunity for platforms and brands looking to expand beyond Western markets.

Key Players & Platform Market Share

The creator economy platform landscape is dominated by a handful of major players that have built massive ecosystems around content creation, distribution, and monetization. These platforms serve as the infrastructure upon which the entire creator economy operates.

| Platform | Parent Company | Primary Content Type | Key Strength |

|---|---|---|---|

| YouTube | Alphabet/Google | Long-form video | Established monetization via Partner Program |

| Meta | Short-form video, photos | Brand partnerships, shopping integration | |

| TikTok | ByteDance | Short-form video | Algorithm-driven discovery, viral potential |

| Twitch | Amazon | Live streaming, gaming | Subscription model, engaged communities |

| Substack | Independent | Newsletters, written content | Direct subscription revenue |

| Patreon | Independent | Multi-format membership | Direct fan support, recurring revenue |

| Spotify | Spotify | Audio, podcasts | Audio monetization, podcast growth |

By platform type, video streaming dominates the creator economy with over 50% revenue share, driven by platforms like YouTube and TikTok. The high growth in this segment is attributed to the surge in online video consumption and the emergence of platforms that enable creators to build audiences and monetize content effectively.

The platform landscape is increasingly bifurcated between “discovery platforms” (TikTok, Instagram, YouTube) where attention is captured, and “revenue platforms” (communities, memberships, courses) where actual monetization occurs. According to Circle’s 2026 research, successful creators are increasingly operating across both types of platforms to maximize reach and revenue.

Creator Demographics & Earnings

Understanding who creators are and how much they earn reveals the stark reality of the creator economy: while the potential for high earnings exists, the majority of creators struggle to generate significant income. This income inequality has important implications for brands seeking partnerships and platforms designing monetization tools.

| Creator Tier | Annual Earnings | Percentage of Creators | Characteristics |

|---|---|---|---|

| Elite Creators | $500,000+ | <1% | Major influencers, celebrity creators |

| High Earners | $100,000 – $500,000 | ~3% | Full-time professionals with large audiences |

| Mid-Tier | $15,000 – $100,000 | ~15% | Part-time or emerging full-time creators |

| Low Earners | Under $15,000 | ~50% | Hobbyists, side hustlers |

| Non-Monetized | $0 | ~31% | Aspiring creators, early stage |

According to Archive.com’s analysis, while 207-303 million creators exist globally, only 4% earn over $100,000 annually and 50% make under $15,000. The $15,000 annual earnings threshold effectively separates creators who struggle from those positioned to scale their operations.

The Tilt’s research reveals that content creators spend an average of $10,700 to start their business, with over half (66%) relying on personal savings to fund their new venture. Technology expenses alone cost approximately $1,000 annually, creating barriers to entry for aspiring creators without capital.

Monetization Methods & Revenue Channels

Creator monetization has diversified significantly beyond traditional advertising revenue. Today’s creators employ multiple revenue streams, with direct-to-fan models gaining prominence over platform-dependent advertising.

| Monetization Method | Adoption Rate | Avg Revenue Share | Growth Trend |

|---|---|---|---|

| Paid Memberships/Subscriptions | 88% | Creator keeps 70-95% | Rapidly growing |

| Online Courses | 53% | Creator keeps 80-100% | Strong growth |

| Coaching/Services | 51% | Creator keeps 100% | Steady growth |

| Digital Products | 37% | Creator keeps 90-100% | Growing |

| Affiliate Revenue | 22% | 5-30% commission | Stable |

| Brand Sponsorships | 18% | Varies widely | Maturing |

| Platform Advertising | Variable | 55-68% to creator | Saturating |

According to Circle’s 2026 survey data, paid memberships lead monetization methods at 88% adoption among creators, followed by selling courses (53%) and offering coaching or services (51%). Notably, brand sponsorships—often perceived as the primary creator revenue source—are used by only 18% of creators, highlighting the shift toward direct fan relationships.

Survey data also shows that 69% of creators now prioritize member transformation as their primary driver of retention and growth, signaling a shift from vanity metrics (followers, likes) to meaningful audience impact as the foundation of sustainable creator businesses.

Brand Spending & Influencer Marketing

Brand investment in creator partnerships has accelerated dramatically, with the IAB reporting that U.S. creator economy ad spend reached $37 billion in 2025—up 26% year-over-year and growing nearly 4x faster than the overall media industry. This represents a fundamental shift in how brands allocate marketing budgets.

| Metric | 2024 | 2025 | 2026 (Projected) |

|---|---|---|---|

| U.S. Creator Ad Spend | $29.5 billion | $37.0 billion | $46+ billion |

| Paid Amplification of Creator Content | $8.9 billion | $13.2 billion | $17+ billion |

| Intentional Ad Adjacencies | $5.9 billion | $7.9 billion | $10+ billion |

| YoY Growth Rate | 22% | 26% | 25%+ |

According to the IAB’s 2025 Creator Economy Ad Spend & Strategy Report, $13.2 billion of the total spend comes from paid amplification of content from direct partnerships on social media—representing a 48% increase from $8.9 billion in 2024. Additionally, $7.9 billion accounts for intentional ad adjacencies to creator content, up 33% from $5.9 billion.

The influencer marketing industry specifically grew to $24 billion in 2025, marking a 13.74% year-over-year increase according to Tribe Group. Notably, 93% of brands plan to increase their creator marketing efforts in 2025, indicating continued confidence in creator-driven advertising despite economic uncertainties.

5 Major Trends Shaping the Creator Economy 2026-2030

1. AI-Powered Content Creation

Artificial intelligence has become integral to creator workflows, with 84% of creators using AI tools in 2026 according to Archive.com. Top earners use AI twice as frequently as lower-tier creators and achieve 2-5x higher engagement rates. AI applications range from content ideation and scriptwriting to video editing, thumbnail generation, and audience analytics. This technological adoption is creating competitive gaps between AI-enabled creators and those relying solely on manual processes.

2. Direct-to-Fan Monetization

The shift from platform-dependent advertising to direct fan relationships is accelerating. With 88% of creators now offering paid memberships and 53% selling courses, creators are building sustainable businesses independent of algorithm changes and platform policy shifts. This trend is exemplified by the rise of platforms like Patreon, Substack, and Circle, which enable creators to own their audience relationships and retain higher revenue shares.

3. Video Content Dominance

Video streaming accounts for over 50% of creator economy revenue, driven by platforms like YouTube, TikTok, and Twitch. The surge in online video consumption shows no signs of slowing, with short-form video (TikTok, Instagram Reels, YouTube Shorts) capturing increasing attention share. Video’s versatility, high engagement rates, and superior monetization potential make it the dominant content format for creators seeking sustainable income.

4. The Rise of Solo Creator-Entrepreneurs

According to Circle’s research, 48% of creators operate as solo entrepreneurs, running communities, content production, and monetization independently. These creators increasingly function as full-stack operators, overseeing monetization, member lifecycle design, and analytics without traditional organizational support. This trend reflects the democratization of business tools and the increasing feasibility of one-person media companies.

5. Professionalization and Business Infrastructure

Creators are increasingly treating their work as serious businesses rather than side projects. This professionalization manifests in formal business structures, investment in production quality, hiring of support staff (19% lead small teams), and adoption of sophisticated analytics and CRM tools. The average startup cost of $10,700 and ongoing technology expenses of $1,000+ annually reflect this shift toward professional operations.

Methodology & Data Sources

This report compiles data from multiple authoritative sources to provide a comprehensive view of the creator economy. Market size figures are derived from Grand View Research, Research and Markets, Precedence Research, Market.us, and Goldman Sachs analyses. Regional breakdowns incorporate data from Coherent Market Insights and Grand View Research geographic reports.

Creator earnings and demographic data come from surveys conducted by Circle, The Tilt, Archive.com, and Influencer Marketing Hub. Platform statistics are sourced from company reports, industry analyses, and third-party research firms. Advertising spend figures are derived from the IAB’s Creator Economy Ad Spend & Strategy Report.

Data limitations include variations in market definition across research firms, self-reported creator income figures, and rapidly evolving platform policies that may affect comparability year-over-year. Where multiple sources provide conflicting figures, we have prioritized the most recent data and indicated the range of estimates where appropriate.

Frequently Asked Questions

How big is the creator economy in 2026?

The global creator economy is projected to reach $323.48 billion in 2026, according to Research and Markets. This represents growth from $255.66 billion in 2025, with a compound annual growth rate (CAGR) of 26.5%. Long-term projections suggest the market could exceed $1.35 trillion by 2033.

How many content creators are there worldwide?

Estimates vary between 207 million and 303 million active content creators globally. This includes creators across all platforms and monetization levels, from hobbyists to full-time professionals. The number continues to grow as barriers to content creation decrease and platform accessibility increases.

What percentage of creators make a living wage?

Only 4% of creators earn over $100,000 annually, while approximately 50% make under $15,000 per year. The $15,000 threshold is often cited as the dividing line between creators who struggle and those positioned to scale their operations. This income inequality reflects the competitive nature of attention economies and the challenges of monetizing creative work.

Which platforms dominate the creator economy?

YouTube, TikTok, and Instagram are the dominant platforms, with video streaming accounting for over 50% of creator economy revenue. YouTube leads in established monetization through its Partner Program, TikTok excels at algorithm-driven discovery, and Instagram offers strong brand partnership and shopping integration capabilities.

How are creators monetizing their content in 2026?

The most popular monetization methods are paid memberships (88% adoption), selling online courses (53%), and offering coaching or services (51%). Brand sponsorships, often perceived as the primary revenue source, are used by only 18% of creators. This reflects a broader shift toward direct-to-fan monetization models that provide more sustainable and predictable income.

Sources & Citations

- Grand View Research – Creator Economy Market Size, Share & Trends Report (2025-2033): https://www.grandviewresearch.com/industry-analysis/creator-economy-market-report

- Research and Markets – Creator Economy Market Report 2026: https://www.researchandmarkets.com/reports/6226071/creator-economy-market-report

- IAB – 2025 Creator Economy Ad Spend & Strategy Report: https://www.iab.com/insights/2025-creator-economy-ad-spend-strategy-report

- Precedence Research – Creator Economy Market Size to Hit USD 2084.57 Billion by 2035: https://www.precedenceresearch.com/creator-economy-market

- Market.us – Creator Economy Market Size, Share | CAGR of 21.8%: https://market.us/report/creator-economy-market

- Coherent Market Insights – Global Creator Economy Market Size and Forecast: https://www.coherentmarketinsights.com/industry-reports/global-creator-economy-market

- Research Nester – Creator Economy Market Size & Share | Forecast Report 2026-2035: https://www.researchnester.com/reports/creator-economy-market/5691

- Circle – Creator Economy Statistics for 2026: https://circle.so/blog/creator-economy-statistics

- Archive.com – 25 Creator Economy Market Size Statistics Every Brand Should Track in 2026: https://archive.com/blog/creator-economy-market-size

- ShortsIntel – Creator Economy Statistics 2026: https://www.shortsintel.com/statistics/creator-economy

- Tribe Group – The Top Creator Marketing Stats you Need to Know: https://www.tribegroup.co/blog/top-creator-marketing-statistics

- The Tilt – Creator Economy | Content Entrepreneur Research: https://www.thetilt.com/research

- Digiday – Here’s what the creator economy is expected to look like in 2026: https://digiday.com/marketing/in-graphic-detail-heres-what-the-creator-economy-is-expected-to-look-like-in-2026

- Influencer Marketing Factory – What Is the Creator Economy? Market Size, Trends, and Statistics: https://theinfluencermarketingfactory.com/creator-economy

- Polaris Market Research – Creator Economy Platforms Market Forecast 2034: https://www.polarismarketresearch.com/industry-analysis/creator-economy-platforms-market

Last updated: June 12, 2026. Statistics compiled from publicly available research reports and industry analyses. For platforms like Fungies.io that serve digital creators and SaaS businesses, understanding these creator economy dynamics is essential for building products that align with how modern creators monetize their audiences.