The digital creator economy has evolved from a niche side hustle into one of the most significant economic forces of our time. In 2026, this ecosystem represents a $234.65 billion global market that employs over 207 million creators worldwide and fundamentally reshapes how content is produced, distributed, and monetized. What began with a handful of YouTubers and bloggers experimenting with ad revenue has transformed into a sophisticated industry where creators function as autonomous media entrepreneurs, commanding marketing budgets that rival traditional advertising channels.

For the first time in history, user-generated content has surpassed traditional media in advertising revenue. This shift isn’t merely a trend—it’s a permanent restructuring of the media landscape. Brands now allocate substantial portions of their marketing budgets to creator partnerships, with influencer marketing spend exceeding $32 billion annually. The implications extend far beyond individual success stories; the creator economy is becoming the primary engine of digital commerce, community building, and cultural influence.

The democratization of content creation tools, combined with the global reach of social media platforms, has created unprecedented opportunities for individuals to build audiences and monetize their expertise, creativity, and personality. Unlike traditional media industries with high barriers to entry, the creator economy allows anyone with a smartphone and internet connection to potentially reach millions of people. This accessibility has led to an explosion of diverse voices and niche communities that traditional media could never serve effectively.

Market Overview: The $234.6 Billion Creator Economy Ecosystem

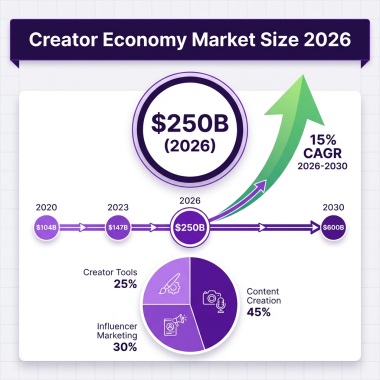

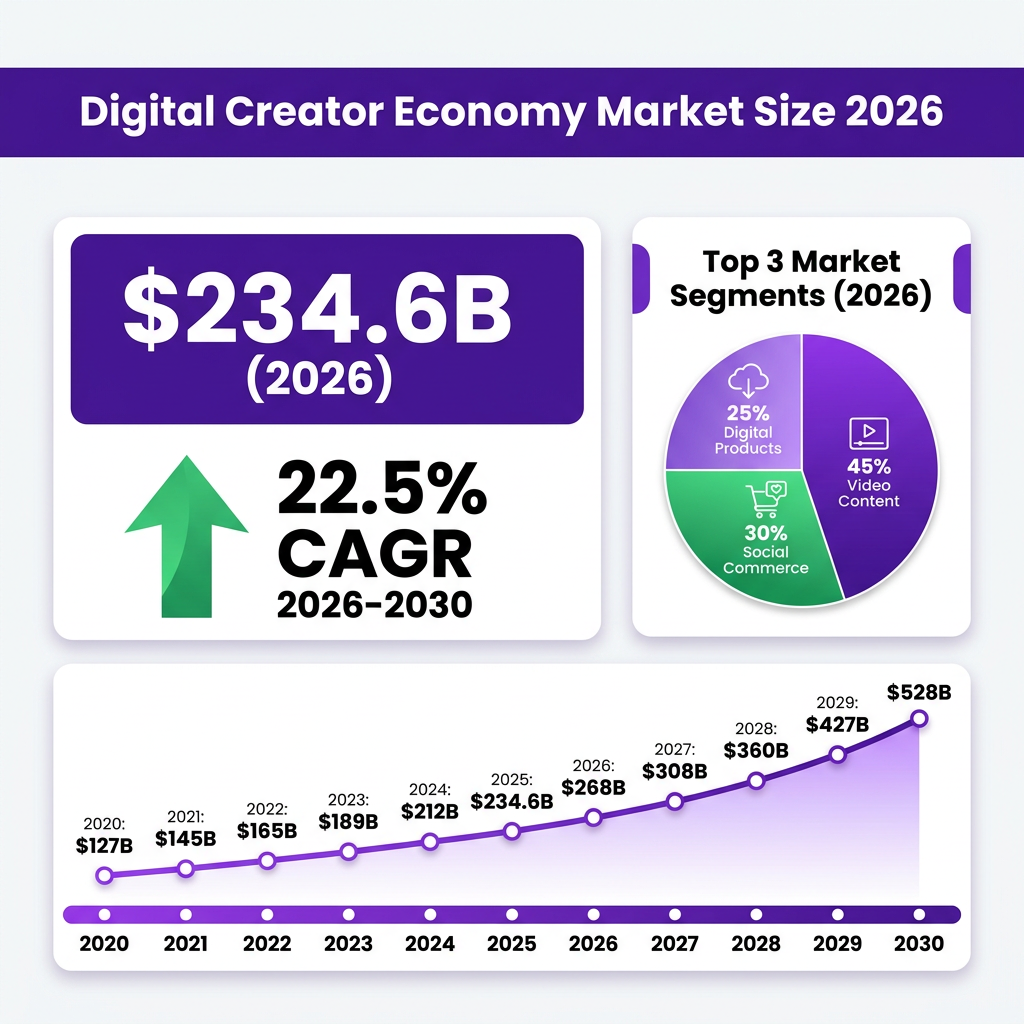

The creator economy’s market size varies by research methodology, but all indicators point to explosive growth. According to Grand View Research, the market was valued at $205.25 billion in 2024, while Goldman Sachs estimated approximately $250 billion for the same period. By 2026, consensus estimates place the market at $234.65 billion, with projections indicating growth to $480 billion by 2027 and potentially reaching $1.35 trillion by 2033.

This growth trajectory represents a compound annual growth rate (CAGR) of 22.5% to 23.3%, making the creator economy one of the fastest-expanding sectors in the global digital landscape. To put this in perspective, the creator economy is growing at approximately four times the rate of the overall media industry, which saw advertising revenue increase by only 6% year-over-year. This disparity highlights the fundamental shift in how audiences consume content and how brands allocate marketing resources.

North America dominates the current market, accounting for 34.2% of global creator economy revenue in 2024, with the United States alone representing a $50.9 billion market. However, Asia-Pacific is emerging as the fastest-growing region, driven by massive user bases on platforms like TikTok, Douyin, and emerging local platforms. The North American market is expected to reach $378.66 billion by 2033, exhibiting a CAGR of 35.1%.

Europe represents the second-largest regional market, with particularly strong creator ecosystems in the United Kingdom, Germany, and France. The European market benefits from high digital penetration rates and strong brand investment in influencer marketing, though regulatory frameworks around advertising disclosure and data privacy create additional compliance requirements for creators operating in the region.

The market’s composition reflects the diverse ways creators monetize their audiences. Video content accounts for the largest segment at approximately 45% of total market value, followed by social commerce at 30%, and digital products including courses, templates, and memberships at 25%. This distribution highlights a critical evolution: creators are no longer dependent solely on platform advertising revenue but have developed sophisticated multi-stream business models that include brand partnerships, affiliate marketing, merchandise sales, and direct audience support through subscriptions and donations.

The professionalization of the creator economy is evident in the infrastructure that has developed to support it. Venture capital investment in creator economy startups reached nearly $2 billion in 2025 alone, funding tools for content creation, audience management, monetization, and business operations. This investment has created a robust ecosystem of services that enable creators to operate as legitimate businesses rather than hobbyists.

Key Statistics and Data: Understanding the Creator Landscape

The creator economy’s scale becomes apparent when examining the underlying statistics that define this ecosystem. Over 207 million people worldwide identify as creators, representing approximately 1 in 40 people globally. This figure includes everyone from casual hobbyists who occasionally post content to full-time professionals who have built substantial businesses around their online presence. The sheer number of participants demonstrates how deeply the creator economy has penetrated global culture and employment.

However, the distribution of earnings reveals significant inequality within the market. Only 4% of creators earn over $100,000 annually, while 50% make less than $15,000 per year from their creative endeavors. The $15,000 threshold represents a critical dividing line: creators earning above this amount typically view their work as a primary career, while those below often treat it as supplementary income. This disparity has sparked important conversations about sustainability and the structural challenges facing independent creators who aspire to make their passion a full-time profession.

The middle tier of creators—those earning between $15,000 and $100,000 annually—represents approximately 15% of the creator population. These creators often have established audiences in specific niches and have developed consistent revenue streams through a combination of platform monetization, brand partnerships, and direct audience support. While not earning celebrity-level income, many in this tier have achieved financial stability and career satisfaction that rivals traditional employment.

Platform-specific data reveals interesting patterns in creator distribution and earnings. YouTube remains the most stable income source for creators, with the YouTube Partner Program now including millions of creators worldwide. Finance and business content on YouTube earns $15-50 per 1,000 views, significantly higher than entertainment or lifestyle content, which typically earns $2-10 per 1,000 views. This disparity reflects the higher advertising value of audiences interested in financial products and business services.

However, only 34% of creators earn their primary income from platform ads, indicating the importance of diversified revenue strategies. The majority of successful creators combine multiple income sources including brand partnerships, affiliate marketing, merchandise sales, digital products, and subscription services. This diversification provides stability against algorithm changes and platform policy shifts that can dramatically impact advertising revenue.

Brand partnerships dominate creator revenue, with 68.8% of creators citing brand collaborations as their top income source. This reliance on sponsored content has created a $32 billion influencer marketing industry that continues to grow at 26% year-over-year—four times faster than traditional media advertising. The average brand deal value varies dramatically by follower count, with nano-influencers (1,000-10,000 followers) earning $100-500 per post while micro-influencers (10,000-100,000 followers) command $500-5,000 per sponsored post. Macro-influencers (100,000-1M followers) typically earn $5,000-25,000 per post, and mega-influencers (1M+ followers) can command $10,000-100,000 or more for major brand partnerships.

AI adoption has become a critical differentiator among creators. In 2026, 84% of creators use AI-powered tools in their daily workflows, with top earners using AI twice as frequently as lower-earning counterparts. Creators leveraging AI report 2-5x higher engagement rates, demonstrating that technological adoption directly correlates with commercial success. The most popular AI applications include content ideation, video editing automation, thumbnail generation, script writing assistance, and audience analytics.

Demographic data shows that the 25-34 age group represents the largest audience segment across platforms, though creator demographics skew slightly younger with the 18-29 age group being most represented among active creators. The average full-time creator spends 40-60 hours per week on content production, community management, and business development—challenging the perception of creator work as passive or effortless income.

Gender distribution in the creator economy shows relatively balanced participation, though earnings disparities exist across different content categories. Female creators dominate lifestyle, beauty, fashion, and parenting niches, while male creators are more represented in gaming, technology, and finance content. These patterns reflect broader societal interests rather than platform bias, though algorithmic recommendations can reinforce these distributions.

Major Trends Shaping the Digital Creator Economy in 2026

1. AI-Powered Content Creation and Virtual Influencers

Artificial intelligence has transitioned from experimental tool to essential infrastructure for professional creators. Beyond simple automation, AI now powers sophisticated content workflows including script generation, video editing, voice synthesis, image creation, and predictive analytics for optimal posting times. The emergence of fully AI-generated virtual influencers represents perhaps the most disruptive development, with the virtual influencer market valued at $15.9 billion in 2026 and projected to reach $62.67 billion by 2030 at a 40.9% CAGR.

Virtual influencers like Lil Miquela, Aitana López, and others have demonstrated that digital personas can command the same brand partnerships and audience loyalty as human creators. These AI-generated characters offer brands unprecedented control over messaging, availability, and risk management. Unlike human creators who may face controversies or personal issues that affect brand partnerships, virtual influencers can be carefully managed to maintain consistent brand alignment.

However, the most successful implementations combine virtual aesthetics with human creative direction, suggesting that AI augments rather than replaces human creativity. Audiences still crave authentic connection and storytelling that requires human emotional intelligence and lived experience. The creators and brands finding the most success with AI are those using it to enhance productivity while preserving the human elements that drive genuine audience engagement.

2. Multi-Platform Strategy and Audience Diversification

Successful creators in 2026 operate across multiple platforms simultaneously, treating each channel as a distinct touchpoint in their audience relationship. A typical professional creator maintains presence on YouTube for long-form content, TikTok or Instagram Reels for discovery, a newsletter for direct communication, Twitter or LinkedIn for professional networking, and a community platform like Discord or Patreon for superfans. This diversification protects against algorithm changes on any single platform while maximizing revenue opportunities.

The data supports this approach: creators using three or more platforms report 3.5x higher earnings than single-platform creators. However, multi-platform success requires sophisticated content adaptation—simply cross-posting identical content yields diminishing returns as platform algorithms increasingly penalize duplicate content. Top performers create platform-native content that leverages each channel’s unique strengths and audience expectations.

3. The Rise of Creator-Led Commerce

Creators are increasingly launching their own product lines, moving beyond sponsored content to build equity in brands they control. This trend encompasses physical products, digital courses, membership communities, software tools, and service offerings. The most successful creator brands generate eight-figure annual revenues, with creators retaining significantly higher margins than traditional brand partnerships offer.

Platforms like Stan Store, Fourthwall, Shopify, and Gumroad have lowered the technical barriers to creator commerce, enabling one-person operations to manage sophisticated e-commerce operations. These platforms handle payment processing, digital delivery, and even tax compliance, allowing creators to focus on product development and marketing.

4. Long-Term Brand Partnerships Replace One-Off Deals

The era of transactional sponsored posts is giving way to strategic, long-term partnerships between creators and brands. These ambassador relationships typically span 6-12 months and involve deeper integration than traditional advertising. Creators become genuine stakeholders in brand success, often receiving performance bonuses tied to sales attribution and long-term brand health metrics.

This shift benefits both parties: brands gain authentic advocacy and consistent messaging that builds over time, while creators secure predictable income and stronger audience trust. Data shows that long-term partnerships generate 2.3x higher engagement rates than one-off sponsored content, as audiences recognize and value genuine brand relationships over transactional promotions.

5. Short-Form Video Dominance and Platform Competition

Short-form video continues to drive the highest engagement rates across all creator content formats. TikTok, Instagram Reels, and YouTube Shorts compete aggressively for creator attention through improved monetization programs and algorithmic reach. Meta’s Creator Fast Track program now pays $1,000 monthly to creators with 100,000+ followers and $3,000 monthly to those with 1M+ followers who post consistently on Facebook.

This competition has created a creator-friendly funding environment where platforms invest billions in retaining top talent. Meta reported paying nearly $3 billion to creators in 2025, up 35% from the previous year. YouTube has expanded its Partner Program to include Shorts monetization, while TikTok continues developing its Creativity Program to compete with established revenue-sharing models.

6. Generative Engine Optimization (GEO)

As AI-powered search and recommendation systems become primary content discovery mechanisms, creators are developing new optimization strategies beyond traditional SEO. Generative Engine Optimization focuses on creating content that AI systems can effectively parse, summarize, and recommend. This includes structured content formats, clear topical authority signals, and metadata optimization for AI consumption.

7. Community-First Business Models

The most resilient creator businesses in 2026 prioritize community over audience. While audience metrics (views, followers) remain important, community metrics (engagement rate, retention, direct relationships) better predict long-term success. Creators are building private communities through paid memberships, exclusive content tiers, and direct communication channels that reduce dependence on platform algorithms.

This shift recognizes that a smaller, highly engaged community generates more sustainable revenue than a large, passive audience. A creator with 10,000 dedicated community members paying $10 monthly generates $1.2 million annually—often more than creators with millions of followers relying solely on advertising revenue.

Key Players and Competitive Landscape

The creator economy infrastructure spans platforms, tools, and service providers that enable creator success. Understanding this ecosystem is essential for creators seeking to optimize their operations and for businesses looking to engage with the creator market effectively.

Major Platforms

YouTube remains the monetization leader, offering the most mature revenue-sharing program and diverse income streams including AdSense, channel memberships, Super Chat, and Shopping. The platform’s long-form content format supports higher CPMs ($5-50 depending on niche) and deeper audience relationships than short-form alternatives. YouTube’s algorithm favors watch time and session duration, rewarding creators who keep viewers engaged for extended periods.

TikTok dominates discovery and viral growth, with its algorithm capable of catapulting unknown creators to millions of views overnight. The TikTok Creator Fund and newer Creativity Program offer monetization, though rates remain lower than YouTube. TikTok Shop has emerged as a significant commerce opportunity, particularly for product-focused creators who can demonstrate items in engaging short videos.

Instagram balances content formats with Reels for discovery, Feed posts for community, and Stories for engagement. The platform’s shopping features and brand collaboration tools make it particularly valuable for lifestyle, fashion, and beauty creators. Meta’s increased creator investments signal continued commitment to competing for creator talent across its family of apps.

Twitch leads in live streaming monetization through subscriptions, bits, and donations, particularly for gaming and entertainment creators. The platform’s high engagement rates and direct fan relationships create strong monetization potential for consistent streamers who build loyal communities.

Newsletter Platforms (Substack, Beehiiv) have enabled creators to build direct audience relationships outside social media algorithms. Top newsletter creators earn seven figures annually through subscription revenue alone, demonstrating the value of owned audience channels that aren’t subject to platform algorithm changes.

Creator Economy Startups and Tools

The infrastructure supporting creators has attracted significant venture capital investment. In 2025, creator economy startups raised nearly $2 billion across major funding rounds. Notable companies include:

Beehiiv provides newsletter infrastructure with built-in monetization features, growing rapidly as newsletter creation expands beyond traditional writers to include creators from all backgrounds.

Stan Store offers creator commerce solutions enabling one-page storefronts for digital products, courses, and services, with particularly strong adoption among TikTok and Instagram creators.

Fourthwall provides creator storefronts with integrated merchandise fulfillment, allowing creators to sell physical products without managing inventory or shipping.

Spotter Studio delivers AI-powered YouTube research tools including trend analysis, title/thumbnail testing, and outlier video detection to help creators optimize their content strategy.

OpusClip uses generative AI to repurpose long-form videos into short-form content, addressing the resource intensity of multi-platform publishing by automating editing and formatting.

Runway provides professional-grade AI video generation tools including text-to-video, image-to-video, and video-to-video capabilities with Hollywood-quality output, enabling creators to produce high-production content without expensive equipment.

CapCut, developed by ByteDance, remains the dominant AI-powered editing platform for short-form video creators, offering sophisticated editing features in a free, accessible package.

Challenges and Pain Points in the Creator Economy

1. Sustainability and Burnout

Despite glamorous success stories, the creator economy faces a significant sustainability problem. Nearly half of independent creators report difficulty achieving success, and 41% have experienced burnout. The pressure to maintain consistent posting schedules across multiple platforms while engaging with communities creates unsustainable workloads. Unlike traditional employment, creators cannot take sick days or vacations without potentially damaging their algorithmic reach and audience engagement.

The “always-on” nature of creator work, combined with income volatility, creates mental health challenges that the industry is only beginning to address. Platform algorithm changes can destroy years of audience building overnight, adding psychological stress to an already demanding profession. Many creators report feeling trapped in a cycle of content production with no clear exit strategy or retirement plan.

2. Income Inequality and Access Barriers

The creator economy exhibits extreme income inequality, with a small percentage of top earners capturing disproportionate revenue while the majority struggle to generate sustainable income. This concentration creates barriers to entry for new creators who must compete with established players with greater resources, audience trust, and algorithmic advantages.

Access to creator economy opportunities also varies by geography, language, and demographic factors. Platform monetization programs often have country restrictions, and brand partnerships historically favor creators in major media markets. While the democratization promise of creator platforms remains partially true, structural advantages persist that favor certain creators over others.

3. Platform Dependence and Algorithm Risk

Creator businesses built entirely on platforms they don’t control face existential risk from algorithm changes, policy updates, and account bans. High-profile cases of creators losing years of work due to policy violations—sometimes incorrectly applied—highlight the precariousness of platform-dependent businesses.

The recent TikTok regulatory challenges in the United States demonstrated how quickly platform access can become uncertain, potentially destroying businesses built on those audiences. Diversification across platforms mitigates but doesn’t eliminate this risk, as major platform policy shifts can affect entire segments of the creator economy simultaneously.

4. Measurement and Attribution Challenges

Brands struggle to accurately measure creator campaign ROI, while creators face challenges demonstrating their value beyond vanity metrics like follower counts and view numbers. Attribution modeling for creator marketing remains less sophisticated than other digital channels, creating friction in brand-creator relationships and potentially limiting budget allocation.

The lack of standardized metrics across platforms makes it difficult to compare creator performance or establish fair pricing benchmarks. This opacity benefits neither party and creates opportunities for platforms that can provide better analytics and attribution capabilities.

Opportunities and Growth Strategies

1. Niche Authority and Specialization

The most successful new creators in 2026 focus on narrow niches where they can establish genuine authority rather than competing in saturated broad categories. Specialized creators in finance, technology, health, professional development, and hobby-specific content command premium rates due to their valuable audience demographics and demonstrated expertise.

Case studies show that creators who focus on specific niches achieve monetization 40% faster than generalists, as their audiences have clearer value propositions for brand partnerships and are more likely to purchase recommended products. A creator who dominates a small niche often earns more than a generalist with 10x the audience size.

2. B2B Creator Opportunities

While consumer-facing creator content receives more attention, B2B creator opportunities represent an underserved and high-value market. LinkedIn creators focusing on professional development, industry insights, and business strategy can command higher rates than consumer creators due to the direct business value of their audiences.

The rise of “thought leadership” content on LinkedIn, Twitter/X, and newsletters has created opportunities for professionals to monetize their expertise without leaving their industries. B2B creators typically have smaller but more valuable audiences, with higher conversion rates for relevant products and services. A LinkedIn creator with 50,000 followers in the SaaS industry may generate more revenue than an Instagram creator with 500,000 lifestyle followers.

3. AI-Augmented Creation Workflows

Creators who effectively integrate AI tools into their workflows can produce higher-quality content at greater scale than competitors relying solely on manual processes. This efficiency advantage compounds over time, allowing AI-adopting creators to test more content, iterate faster, and identify winning formats before competitors.

Successful AI integration focuses on automation of repetitive tasks (editing, transcription, thumbnail generation, content scheduling) while preserving human creativity for strategy, storytelling, and community engagement. Creators reporting 2-5x engagement improvements with AI typically use it to enhance rather than replace their creative judgment.

4. International Market Expansion

While North America and Western Europe dominate current creator economy value, emerging markets present significant growth opportunities. Creators who localize content for Latin America, Southeast Asia, the Middle East, and Africa can access rapidly growing internet populations with less competition than saturated English-language markets.

Platforms are investing heavily in emerging market expansion, creating infrastructure for creators to build audiences in these regions. Early movers in underrepresented languages and markets often achieve faster growth due to reduced competition and hungry audiences seeking relevant content.

Case Studies and Success Stories

Case Study 1: MrBeast and the Multi-Platform Empire

Jimmy Donaldson (MrBeast) represents the pinnacle of creator economy success, building a business valued at over $500 million through strategic platform diversification and relentless focus on content quality. Starting with YouTube challenge videos filmed in his bedroom, MrBeast expanded into merchandise (Feastables chocolate bars generating $100M+ annually), branded content, mobile games, and philanthropy-focused content that reinforces his brand values.

The MrBeast model demonstrates how creators can transcend platform dependence by building genuine brands with product-market fit independent of content algorithms. His team of over 100 employees operates with corporate-level production values while maintaining the authentic connection that drove initial success. The key lesson: creators who build businesses around their content rather than relying solely on platform revenue achieve greater sustainability and scale.

Case Study 2: Newsletter Writers and Direct Monetization

Writers on Substack and Beehiiv have demonstrated that creators can build sustainable businesses with relatively small but highly engaged audiences. Top newsletter creators earn $1-5 million annually through subscription revenue alone, with audiences of 10,000-50,000 paid subscribers. This model works particularly well for professional and educational content where audiences have clear willingness to pay for valuable insights.

These success stories highlight the value of direct audience relationships outside platform algorithms. By owning their distribution channels, newsletter creators achieve revenue stability impossible on advertising-dependent platforms. The model has proven successful across diverse niches including technology analysis, financial advice, health and wellness, and creative writing.

Case Study 3: AI Influencer Economics

Virtual influencers like Lil Miquela (2.5M+ Instagram followers) and Aitana López demonstrate that AI-generated personas can achieve commercial success comparable to human creators. Aitana reportedly earns €1,000-10,000 per brand partnership despite being entirely computer-generated. These cases reveal important insights about audience behavior: followers engage with compelling content and consistent personas regardless of whether the creator is human or virtual.

For brands, virtual influencers offer advantages including 24/7 availability, perfect brand safety, complete creative control, and no risk of personal scandals affecting partnerships. However, the most successful virtual creators maintain human creative direction and storytelling expertise, suggesting that AI augments rather than replaces human creativity in the creator economy.

Future Outlook and Predictions (2026-2030)

The creator economy’s trajectory points toward continued expansion and professionalization. Goldman Sachs projects the market could approach $500 billion by 2027, while more aggressive forecasts suggest $1.35 trillion by 2033. Several factors will drive this growth and reshape the industry over the coming years.

Platform Maturation and Competition

As the creator economy proves its commercial value, platform competition for creator talent will intensify. This competition drives improved monetization features, better revenue sharing, and creator-friendly policies. Meta’s $3 billion in creator payments during 2025 (up 35% year-over-year) represents just the beginning of platform investment in creator retention.

We can expect platforms to develop more sophisticated creator tools, better analytics, and more favorable revenue splits as they recognize creators as essential partners rather than content suppliers. The platforms that best serve creator needs will attract the highest-quality content and most engaged audiences.

AI Integration Acceleration

AI will become increasingly central to creator workflows, with tools becoming more sophisticated and accessible. By 2030, AI assistance in content creation will likely be standard rather than differentiating. The competitive advantage will shift from AI usage to creative strategy and community building that AI cannot replicate.

Regulatory Evolution

As the creator economy matures, regulatory frameworks will evolve to address labor classification, advertising disclosure, platform accountability, and data privacy. Creators should prepare for increased compliance requirements, particularly around sponsored content disclosure and audience data handling.

Creator Economy Infrastructure

The tools and services supporting creators will continue professionalizing, with enterprise-grade solutions becoming accessible to individual creators. This infrastructure evolution will enable smaller teams to achieve production values previously requiring major media company resources.

Traditional Media Convergence

The distinction between “creator” and “traditional media” will continue blurring as creators launch production companies, traditional talent agencies acquire creator representation practices, and media companies build creator-native content strategies. By 2030, the creator economy may simply be “the economy” for digital content and influence.

Key Takeaways

- The digital creator economy reached $234.65 billion in 2026 and is projected to grow to $480 billion by 2027, representing one of the fastest-growing sectors in the global economy.

- Over 207 million people worldwide identify as creators, though significant income inequality exists—only 4% earn over $100,000 annually while 50% make less than $15,000.

- AI adoption has become essential for creator success, with 84% of creators using AI tools and top performers achieving 2-5x higher engagement through effective AI integration.

- Brand partnerships remain the dominant revenue source (68.8% of creators), but successful creators are diversifying into product lines, subscriptions, and owned communities.

- Multi-platform strategies generate 3.5x higher earnings than single-platform approaches, with successful creators treating each platform as a distinct audience touchpoint.

- The virtual influencer market is emerging as a significant force, valued at $15.9 billion in 2026 and growing at 40.9% CAGR.

- Sustainability challenges including burnout, income volatility, and platform dependence represent the primary risks facing creator economy participants.

- By 2030, the creator economy is projected to reach $528 billion to $1.35 trillion, potentially overtaking traditional agency sectors in value.

Sources and Citations

- Grand View Research – Creator Economy Market Size and Forecast 2024-2033

- Goldman Sachs – “The creator economy could approach half-a-trillion dollars by 2027”

- Archive.com – “25 Creator Economy Market Size Statistics Every Brand Should Track in 2026”

- Research Nester – Creator Economy Market Size & Share Forecast Report 2026-2035

- The Influencer Marketing Factory – “The 2026 Creator Economy Report”

- Coherent Market Insights – North America Creator Economy Market Analysis

- Business Insider – “3 Creator Economy Trends That Helped Startups Raise Millions From VCs”

- Exploding Topics – Creator Economy Market Size (2025-2030)

- Technavio – Creator Economy Market Growth Analysis 2026-2030

- Research and Markets – Virtual Influencers Market Report 2026

- CNBC – Meta Creator Pay Programs 2026

- Forbes – “7 Of The Most Profitable Platforms For Creators In 2026”

- MiDia Research – “The creator economy has a sustainability problem”

- Stan.Store – “The State of the Creator Economy 2026”

- ThriveCart – “The State of the Global Creator Economy in 2025-26”

Deep Dive: Creator Revenue Models and Monetization Strategies

Understanding the various revenue models available to creators is essential for anyone looking to build a sustainable career in the digital creator economy. The most successful creators typically combine multiple income streams, creating a diversified portfolio that reduces dependence on any single source.

Platform Advertising Revenue

Platform advertising remains the foundation of creator monetization, though its importance varies significantly by platform and content category. YouTube’s AdSense program offers the most mature revenue-sharing model, with creators typically receiving 55% of advertising revenue generated by their content. CPM rates (cost per thousand views) vary dramatically based on content category, audience demographics, and seasonality.

Finance and business content commands the highest CPMs, often ranging from $15-50 per thousand views, while entertainment and gaming content typically earns $2-10 per thousand views. This disparity reflects the relative value of different audience segments to advertisers—business audiences represent higher purchase intent and lifetime value than general entertainment viewers.

TikTok’s Creativity Program and Instagram’s various monetization features offer alternative advertising revenue models, though these typically generate lower per-view earnings than YouTube. The trade-off is higher viral potential and audience growth rates on these platforms, which can lead to greater overall earnings despite lower unit economics.

Brand Partnerships and Sponsored Content

Brand partnerships represent the largest revenue opportunity for most professional creators, with 68.8% of creators citing brand collaborations as their primary income source. The brand partnership market has matured significantly, with standardized pricing models emerging based on follower count, engagement rates, content category, and exclusivity requirements.

Nano-influencers (1,000-10,000 followers) typically earn $100-500 per sponsored post, leveraging their highly engaged, niche audiences to deliver strong ROI for brands targeting specific demographics. Micro-influencers (10,000-100,000 followers) command $500-5,000 per post, offering the optimal balance of reach and engagement for many brand campaigns.

Macro-influencers (100,000-1 million followers) earn $5,000-25,000 per sponsored post, while mega-influencers (1M+ followers) can command $10,000-100,000 or more for major brand partnerships. These figures represent base rates—additional factors like usage rights, exclusivity, and content complexity can significantly impact final pricing.

Affiliate Marketing and Commerce

Affiliate marketing enables creators to earn commissions on products and services they recommend, creating passive income streams that can generate revenue long after content is published. Amazon Associates remains the largest affiliate program, though specialized networks like LTK (rewardStyle), ShopMy, and platform-specific programs often offer higher commission rates for relevant product categories.

The integration of social commerce features directly into content platforms has created new affiliate opportunities. TikTok Shop, Instagram Shopping, and YouTube Shopping allow creators to tag products directly in their content, reducing friction between discovery and purchase while earning commissions on resulting sales.

Digital Products and Courses

Digital products represent one of the highest-margin revenue opportunities for creators, with profit margins often exceeding 90% after platform fees. Popular digital products include online courses, ebooks, templates, presets, and software tools. The key advantage of digital products is scalability—once created, they can be sold infinitely without additional production costs.

Online courses have emerged as a particularly lucrative category, with successful course creators earning seven or eight figures annually. Platforms like Teachable, Thinkific, and Kajabi provide infrastructure for course creation and delivery, while marketplaces like Udemy and Skillshare offer built-in audiences at the cost of lower margins.

Memberships and Subscriptions

Recurring revenue through memberships and subscriptions provides creators with predictable income that reduces the volatility inherent in advertising and brand partnership revenue. Patreon pioneered the creator membership model, though platforms like Ko-fi, Buy Me a Coffee, and platform-native features (YouTube Channel Memberships, Twitch Subscriptions) now offer alternatives.

Newsletter subscriptions through Substack, Beehiiv, and ConvertKit have emerged as a particularly powerful model for writers and thought leaders. Top newsletter creators earn $1-5 million annually through subscription revenue alone, demonstrating that relatively small but highly engaged audiences can generate substantial income when monetized through direct relationships.

Physical Products and Merchandise

Physical products and merchandise allow creators to extend their brands into tangible goods, creating additional revenue streams while deepening audience relationships. Print-on-demand services like Printful and Printify have lowered the barriers to merchandise creation, enabling creators to offer custom apparel, accessories, and home goods without managing inventory or fulfillment.

More ambitious creators have launched standalone product brands, like MrBeast’s Feastables chocolate bars and Logan Paul’s Prime Hydration. These ventures require significant capital and operational expertise but offer uncapped upside potential and true business ownership beyond content creation.