The creator economy has exploded into a $234 billion global industry in 2026, fundamentally reshaping how content is produced, distributed, and monetized. What began as a niche phenomenon of bloggers and early YouTubers has evolved into a sophisticated economic ecosystem supporting over 207 million active creators worldwide. This transformation represents one of the most significant shifts in the global economy since the rise of e-commerce, with implications that extend far beyond social media into education, entertainment, marketing, and entrepreneurship.

The meteoric rise of the creator economy reflects a broader cultural shift in how people consume information, entertainment, and products. Traditional media gatekeepers—television networks, publishing houses, record labels—have lost their monopoly on content distribution. In their place, algorithms and social platforms have emerged as the new arbiters of attention, enabling individual creators to build audiences that rival major media properties. A teenager in their bedroom can now reach more viewers than a cable television show, and a solo newsletter writer can generate more revenue than a regional newspaper.

For brands, investors, and aspiring creators, understanding the digital creator landscape in 2026 is no longer optional—it is essential for staying competitive in an attention-driven economy. The lines between creator and entrepreneur, content and commerce, audience and community have blurred beyond recognition. Today’s successful creators operate as full-stack media companies, leveraging AI tools, multi-platform strategies, and diversified revenue streams to build sustainable businesses around their personal brands.

This comprehensive analysis examines the state of the digital creator economy in 2026, drawing on the latest market research, industry data, and expert insights. We will explore the market size and growth trajectory, key statistics that define the industry, major trends shaping the landscape, the competitive ecosystem of platforms and tools, challenges facing creators, opportunities for growth, and future predictions through 2030. Whether you are a brand seeking to navigate creator partnerships, an investor evaluating opportunities in the space, or an aspiring creator planning your entry into this dynamic industry, this report provides the data-driven insights you need to make informed decisions.

Market Overview: The $234 Billion Creator Economy Ecosystem

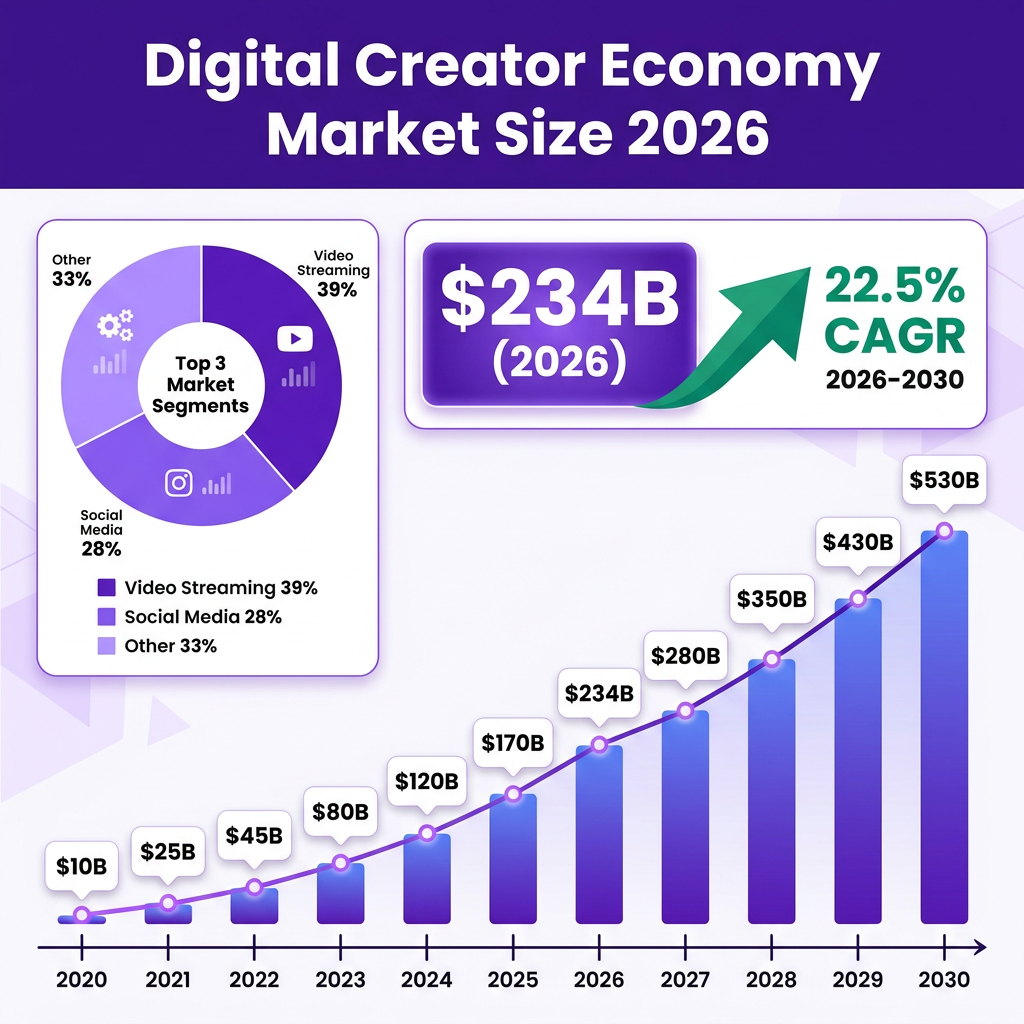

The global creator economy reached an estimated valuation of $234 billion in 2026, representing a compound annual growth rate of 22.5% from the previous year. This explosive growth trajectory shows no signs of slowing, with industry analysts projecting the market could approach $500 billion by 2027 and potentially exceed $1.35 trillion by 2035. These figures position the creator economy as one of the fastest-growing sectors in the global economy, outpacing traditional media, advertising, and even some technology subsectors.

The foundation of this growth rests on several interconnected factors. First, the widespread penetration of smartphones and high-speed internet has democratized content creation, enabling anyone with a mobile device to reach global audiences. Second, platform infrastructure has matured significantly, providing creators with sophisticated tools for content production, audience analytics, and monetization. Third, consumer behavior has shifted dramatically—particularly among younger demographics—who increasingly prefer authentic creator content over traditional advertising and corporate media.

Regional distribution of the creator economy reveals interesting patterns. North America currently holds the largest market share, with the United States alone accounting for approximately $50.9 billion in 2024, projected to reach $297.3 billion by 2034 at a 19.3% CAGR. However, Asia-Pacific represents the fastest-growing region, driven by massive user bases in India, Southeast Asia, and continued expansion in China. Europe maintains a strong position, particularly in lifestyle, fashion, and gaming content, while Latin America and Africa are emerging as significant growth markets with expanding internet infrastructure and young, digitally-native populations.

The creator economy’s value chain has become increasingly complex and professionalized. At the base layer are the platforms—YouTube, TikTok, Instagram, Twitch, and emerging players like Lemon8 and BeReal—that provide distribution infrastructure. Above them sit the creators themselves, ranging from nano-influencers with fewer than 1,000 followers to mega-creators with audiences in the tens of millions. Supporting this ecosystem are creator economy startups providing tools for content creation (Canva, Adobe Creative Suite, AI video generators), audience management (newsletter platforms, community tools), monetization (Patreon, Ko-fi, Stan Store), and brand collaboration (marketplaces, agencies, CRM tools).

Investment in creator economy infrastructure has accelerated dramatically. Venture capital funding for creator-focused startups exceeded $1.5 billion in 2024, with particular concentration in AI-powered content tools, social commerce platforms, and monetization infrastructure. Notable funding rounds included Substack’s $100 million Series C led by Bond Capital, beehiiv’s $33 million Series B from Lightspeed Venture Partners, and Agentio’s $40 million Series B for YouTube creator marketplaces. This capital influx signals institutional recognition of the creator economy’s permanence and growth potential.

Key Statistics and Data: Understanding the Creator Landscape

The scale of the creator economy becomes apparent when examining the underlying statistics that define this industry. Over 207 million people worldwide now identify as active creators, though this number likely undercounts part-time and aspiring creators who have not yet monetized their content. Of this total, approximately 50 million consider themselves professional creators—individuals who derive meaningful income from their creative activities. The remaining 157 million represent a vast reservoir of amateur creators, hobbyists, and aspiring professionals who contribute to the ecosystem’s vibrancy while potentially representing the next wave of professional talent.

Income distribution within the creator economy follows a stark power law, with significant implications for aspiring creators and platform economics. Only 4% of creators earn more than $100,000 annually from their creative activities, while approximately 50% earn less than $15,000 per year. The top 1% of creators capture an estimated 97% of platform-derived revenue, creating a winner-take-most dynamic that mirrors broader digital economy patterns. This inequality has sparked ongoing debates about platform responsibility, creator unionization, and the sustainability of creator careers for those outside the top tier.

Platform-specific statistics reveal divergent monetization models and creator experiences. YouTube remains the largest direct payer to creators, having distributed over $70 billion through its Partner Program since inception—making it the single largest source of platform-to-creator payouts in the digital economy. The platform’s AdSense model, while often criticized for opacity, provides relatively predictable revenue for established creators. In contrast, TikTok’s Creator Fund pays approximately $0.02-$0.04 per 1,000 views, forcing creators to rely heavily on brand partnerships and merchandise sales for meaningful income. Instagram’s monetization tools, including Reels bonuses and subscriptions, have shown promise but remain geographically limited and inconsistently available.

Influencer marketing spending has reached $32.55 billion globally in 2026, with brands reporting an average return of $5.78 for every $1 invested in creator partnerships. This ROI metric has driven increasing corporate investment in creator marketing, with companies like Unilever announcing plans to allocate 50% of marketing spend to influencer partnerships. The effectiveness of creator marketing stems from perceived authenticity, audience trust, and the ability to reach highly targeted demographics that traditional advertising struggles to engage.

Creator platform preferences show interesting demographic patterns. Video streaming platforms command 39% of creator economy revenue, reflecting the high engagement and monetization potential of video content. Social media platforms collectively account for 28% of revenue, while blogging, podcasting, and other formats make up the remaining 33%. Within video, short-form content (TikTok, Instagram Reels, YouTube Shorts) has experienced explosive growth, though long-form YouTube content maintains higher per-view monetization rates. Live streaming, particularly on Twitch and emerging platforms like Kick, represents a significant and growing segment, particularly in gaming and entertainment verticals.

AI adoption among creators has become nearly universal, with 84% of creators reporting use of AI tools in their workflows as of 2026. Top-earning creators use AI tools twice as frequently as their lower-earning counterparts, and achieve 2-5x higher engagement rates on AI-assisted content. Common applications include content ideation, script writing, thumbnail generation, video editing, and audience analytics. This technological arms race has raised the baseline for content quality while simultaneously increasing competitive pressure on creators who fail to adopt AI tools.

Community and subscription metrics reveal shifting monetization strategies. Patreon creators collectively earn over $2 billion annually, representing one of the largest direct-to-creator revenue streams outside of advertising. Survey data indicates that 88% of creators now offer paid memberships, 53% sell courses, 51% offer coaching or services, and 37% sell digital products. This diversification reflects creator recognition that platform-dependent advertising revenue is volatile and insufficient for building sustainable businesses. The trend toward owned audiences—email lists, communities, and direct relationships—represents a maturation of creator business models.

Micro and nano-influencers (creators with under 100,000 followers) are claiming an increasing share of brand spending, expected to capture 45.5% of influencer marketing budgets in 2026. This shift reflects brand recognition that smaller creators often deliver higher engagement rates, more authentic audience relationships, and better cost efficiency than mega-influencers. The average engagement rate for nano-influencers (1,000-10,000 followers) ranges from 5-8%, compared to 1-3% for mega-influencers (1M+ followers), making them particularly attractive for performance-focused campaigns.

Major Trends Shaping the Digital Creator Economy in 2026

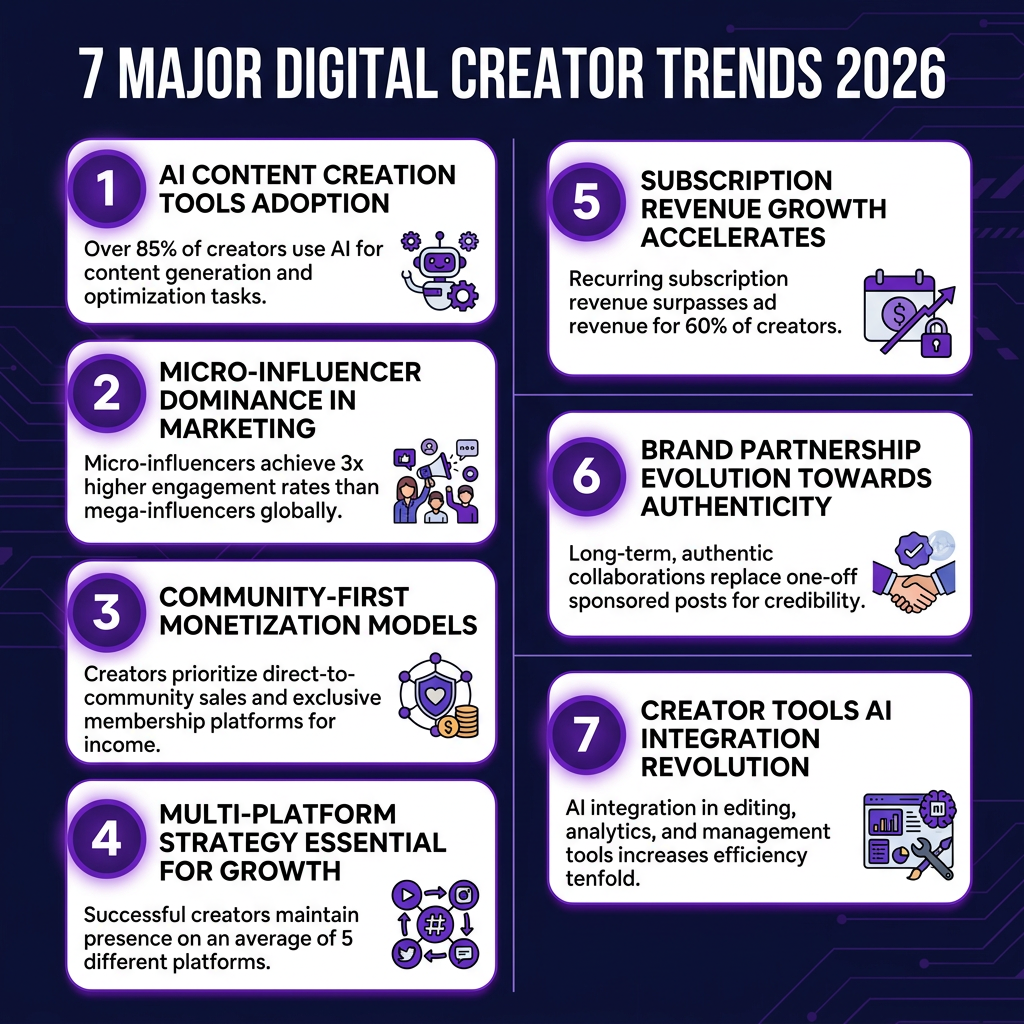

The creator economy in 2026 is defined by seven transformative trends that are reshaping how creators build audiences, generate revenue, and operate their businesses. Understanding these trends is essential for anyone seeking to navigate or invest in this rapidly evolving landscape.

1. AI-Powered Content Creation and Workflow Automation

Artificial intelligence has moved from experimental tool to essential infrastructure for creators. Beyond simple automation, AI now handles sophisticated creative tasks including script writing, video editing, thumbnail optimization, and even synthetic voice generation. Tools like Runway ML for video editing, Midjourney and DALL-E for image generation, and specialized AI writing assistants have democratized production capabilities that previously required expensive equipment and technical expertise. The most successful creators in 2026 treat AI as a creative partner rather than a replacement, using it to amplify their unique voice and perspective while handling time-consuming technical tasks.

2. The Rise of Micro and Nano-Influencers

Brand strategies have shifted decisively toward smaller creators who deliver higher engagement and authenticity. Micro-influencers (10,000-100,000 followers) and nano-influencers (1,000-10,000 followers) now command nearly half of all influencer marketing spending. This trend reflects maturation in the influencer marketing industry—brands have learned that reach metrics alone don’t drive results, and that highly engaged niche audiences often outperform mass-market exposure. For creators, this trend creates opportunity: you no longer need millions of followers to build a sustainable creator business.

3. Community-First Monetization Models

The most successful creators in 2026 have shifted from audience-building to community-building. Rather than treating followers as passive consumers of content, top creators cultivate engaged communities where members interact with each other, not just with the creator. This shift enables more sustainable monetization through memberships, courses, coaching, and digital products. Survey data shows that 69% of creators now prioritize member transformation—helping their community achieve specific outcomes—as their primary growth driver. Platforms like Circle, Skool, and Discord have become essential infrastructure for community-based creator businesses.

4. Multi-Platform Content Strategies

Platform dependency has proven dangerous for creators who built their businesses on single platforms. Algorithm changes, policy updates, and platform shutdowns have destroyed countless creator businesses. In response, sophisticated creators now operate across multiple platforms simultaneously, treating each platform as a channel for different audience segments and content formats. The typical professional creator in 2026 maintains active presence on 3-5 platforms, with content repurposed and optimized for each platform’s unique characteristics. This diversification provides resilience while maximizing audience reach.

5. Subscription and Recurring Revenue Growth

Advertising-dependent business models have proven volatile and insufficient for most creators. The trend toward subscription-based revenue has accelerated, with creators building predictable income through Patreon, Substack, YouTube memberships, and proprietary subscription platforms. This shift transforms creators from gig workers into business owners with recurring revenue streams. The most successful subscription creators offer exclusive content, community access, and direct interaction—value propositions that advertising-supported free content cannot match.

6. Evolution of Brand Partnerships

Brand-creator relationships have matured beyond simple sponsored posts. Long-term ambassadorships, co-created product lines, and equity partnerships are becoming standard for top-tier creators. Brands recognize that authentic, ongoing relationships deliver better results than one-off campaigns, while creators benefit from stable income and deeper integration with brands they genuinely support. This trend also sees creators becoming investors in other creator businesses, with figures like Steven Bartlett building portfolios of creator-led companies.

7. Creator Tool Ecosystem Maturation

The infrastructure supporting creators has become increasingly sophisticated. Specialized tools now exist for every aspect of creator business: content planning, production, distribution, audience analytics, monetization, and business operations. This maturation enables creators to operate as lean, efficient media companies without large teams. AI-powered tools have been particularly transformative, allowing individual creators to produce content quality that previously required professional production studios.

Key Players and Competitive Landscape

The creator economy competitive landscape spans multiple layers, from dominant distribution platforms to specialized tool providers and emerging challengers. Understanding this ecosystem is crucial for creators choosing where to invest their time and for investors evaluating opportunities in the space.

Distribution Platforms

YouTube remains the dominant force in creator monetization, with its Partner Program having paid out over $70 billion to creators. The platform’s strength lies in its mature advertising infrastructure, search-based discovery, and long-form content format that enables deep audience relationships. YouTube Shorts has successfully challenged TikTok’s dominance in short-form video, while the platform’s subscription features (channel memberships, Super Chat) provide additional revenue streams. Google’s backing provides stability that newer platforms cannot match.

TikTok has transformed from entertainment platform to cultural force, particularly among younger demographics. Despite regulatory challenges and uncertain monetization for creators (the Creator Fund pays notoriously little), TikTok remains essential for reach and cultural relevance. The platform’s algorithm provides unmatched organic discovery potential, allowing unknown creators to reach millions overnight. TikTok Shop has added e-commerce capabilities, creating new monetization opportunities for product-focused creators.

Instagram continues evolving to compete with TikTok, prioritizing Reels and video content over the static images that originally defined the platform. While creator sentiment toward Instagram has declined due to algorithm changes and reduced organic reach, the platform remains essential for lifestyle, fashion, and beauty creators. Instagram’s shopping features and subscription tools provide monetization options, though they lag behind dedicated platforms in functionality.

Twitch dominates live streaming, particularly in gaming but expanding into other verticals including music, talk shows, and creative content. Amazon’s ownership provides infrastructure and Prime integration, while the platform’s subscription model (where viewers pay monthly to support creators) has proven highly effective. Competition from Kick and YouTube Live has pressured Twitch to improve creator revenue shares and features.

Monetization Infrastructure

Patreon pioneered creator subscriptions and remains a leader in the space, with creators collectively earning over $2 billion annually through the platform. Patreon’s strength lies in its flexibility—creators can offer tiered memberships with varying benefits—and its established user base of patrons willing to pay for content. The platform has expanded beyond traditional creators to include podcasters, writers, and educators.

Substack has become the dominant platform for newsletter-based creators, combining publishing tools with subscription management. The platform’s $100 million Series C funding in 2025 reflects investor confidence in the newsletter format and Substack’s position within it. Substack’s recent expansion into video and podcast hosting signals ambitions to become a comprehensive creator platform rather than just an email tool.

Stan Store and similar link-in-bio commerce platforms have enabled creators to sell digital products, courses, and services directly to their audiences. These tools transform social media followers into customers, addressing the monetization gap that leaves most creators earning little from platform-native revenue sharing. The simplicity of these tools—enabling storefront setup in minutes—has democratized creator commerce.

AI and Creation Tools

The AI creation tool space has exploded, with companies like Runway ML (video editing), Midjourney (image generation), and various writing assistants becoming essential creator infrastructure. These tools have raised the baseline for content quality while reducing production time and costs. The most successful creators integrate multiple AI tools into their workflows, using each for its specific strengths.

Traditional creative software providers like Adobe have responded to the creator economy by adding AI features and simplifying their tools for non-professional users. Adobe Express competes directly with Canva for the casual creator market, while professional-grade tools remain essential for top-tier production quality.

Challenges and Pain Points in the Creator Economy

Despite its growth and opportunities, the creator economy faces significant challenges that threaten creator sustainability and ecosystem health. Understanding these pain points is essential for creators building businesses and for platforms seeking to attract and retain talent.

1. Algorithm Unpredictability and Platform Dependency

Creator surveys consistently identify algorithm unpredictability as the top challenge, cited by 51.7% of creators. Platform algorithms determine content visibility, yet their opaque operation makes it impossible for creators to optimize strategically. A single algorithm update can destroy years of audience building overnight, as creators on Instagram, Facebook, and YouTube have experienced repeatedly. This unpredictability makes financial planning difficult and creates chronic stress for professional creators whose livelihoods depend on platform distribution.

The platform dependency problem extends beyond algorithms to policy changes, account bans, and platform shutdowns. Creators who build businesses on single platforms face existential risk from decisions entirely outside their control. The 2025 TikTok ban threats in the United States demonstrated this vulnerability, with creators facing potential loss of their primary distribution channel and audience relationships.

2. Income Inequality and Sustainability

The stark income inequality in the creator economy creates sustainability challenges for the vast majority of creators. With only 4% earning over $100,000 annually and 50% earning under $15,000, most creators cannot support themselves through creative work alone. This inequality has led to high burnout rates, with creators abandoning their channels after failing to achieve financial viability. The “starving artist” dynamic that plagued traditional creative industries has replicated itself in the digital creator economy.

The concentration of revenue among top creators also creates barriers to entry. New creators face intense competition from established players with professional production capabilities, large existing audiences, and brand relationships. The algorithmic advantage of existing popularity (platforms promote content that already has engagement) makes breaking in increasingly difficult.

3. AI Content Proliferation and Authenticity Concerns

The explosion of AI-generated content has created authenticity challenges for human creators. While 84% of creators use AI tools, the proliferation of fully AI-generated channels and content has made it harder for authentic human creators to stand out. Audiences have become increasingly skeptical of content authenticity, with “AI slop” (low-quality AI-generated content) flooding platforms and degrading the overall content experience.

Creators report that distinguishing themselves from AI-generated competitors has become a significant challenge. The value proposition of human creativity—authenticity, personal experience, genuine emotion—must be actively communicated in an environment where AI can mimic these qualities superficially. This challenge is particularly acute in informational and educational content, where AI can generate competent explanations faster than human creators.

4. Creator Burnout and Mental Health

The demands of consistent content creation, audience engagement, and platform optimization have created an epidemic of creator burnout. Professional creators report working 60+ hour weeks, with the always-on nature of social media making true disconnection impossible. The pressure to maintain posting schedules, respond to comments, and stay culturally relevant creates chronic stress that drives talented creators from the industry.

Mental health challenges are exacerbated by the public nature of creator work. Creators face constant feedback—both positive and negative—from massive audiences, with harassment and toxicity particularly affecting creators from marginalized groups. The personal nature of creator content blurs boundaries between work and personal life, making it difficult to maintain healthy separation.

Opportunities and Growth Strategies for 2026

Despite significant challenges, the creator economy offers substantial opportunities for creators who approach the industry strategically. The following growth strategies have proven effective for creators building sustainable businesses in 2026.

1. Niche Specialization and Authority Building

The most successful new creators in 2026 have abandoned broad appeal in favor of deep niche specialization. Rather than competing as general lifestyle or entertainment creators, they establish authority in specific domains—whether that is vintage watch restoration, Excel automation, or sustainable urban gardening. This specialization enables creators to command premium pricing for their expertise, attract highly engaged audiences, and build defensible positions against generalist competitors.

Authority building requires consistent educational content that demonstrates expertise. Creators who combine entertainment with genuine education create more value for their audiences and differentiate themselves from AI-generated content. The most successful niche creators position themselves as the definitive resource for their specific topic, creating moats that are difficult for competitors to cross.

2. Owned Audience Development

Smart creators in 2026 prioritize building owned audiences over platform-dependent followings. Email lists, community memberships, and direct relationships provide stability that social media followings cannot match. The strategy involves using social platforms for discovery while systematically converting followers to owned channels. This might mean offering a free lead magnet in exchange for email signup, creating exclusive community content for members, or building direct messaging relationships with top fans.

Owned audiences also enable better monetization. Direct relationships allow for higher-priced offerings, personalized services, and recurring revenue models that platforms cannot facilitate. Creators with strong owned audiences are less vulnerable to algorithm changes and platform policy shifts, providing business stability that pure social media creators lack.

3. Diversified Revenue Streams

The creators building the most sustainable businesses in 2026 have diversified beyond any single revenue source. Rather than relying solely on platform advertising or brand partnerships, they combine multiple income streams: advertising revenue, brand partnerships, affiliate marketing, digital products, courses, coaching, memberships, merchandise, and speaking engagements. This diversification provides stability—when one revenue stream underperforms, others can compensate.

The specific mix of revenue streams varies by creator niche and audience, but the principle remains consistent: over-dependence on any single source creates vulnerability. Successful creators continuously experiment with new monetization approaches, doubling down on what works while quickly abandoning what does not. This experimental mindset is crucial in an industry where platform policies, audience preferences, and monetization opportunities change rapidly.

Data from successful creator businesses reveals common patterns in revenue diversification. Most sustainable creator businesses derive no more than 40% of revenue from any single source, with healthy businesses typically showing 4-6 distinct revenue streams contributing meaningfully to total income. The exact mix depends on niche, audience size, and creator strengths—some creators excel at brand partnerships while others find more success with digital products or coaching services. The key is building a portfolio that provides stability while allowing creators to focus on their highest-value activities.

Case Studies and Success Stories

Examining successful creator businesses provides concrete examples of strategies that work in the current environment. The following case studies illustrate different paths to creator success in 2026.

Case Study 1: The Niche Expert

A former financial analyst built a seven-figure creator business by focusing exclusively on cryptocurrency tax strategy—a hyper-specific niche with high commercial intent. Rather than competing in the crowded general crypto content space, this creator positioned themselves as the definitive resource for a specific, painful problem. Content focused on educational tutorials, tax software reviews, and regulatory updates. Revenue came from affiliate partnerships with tax software (generating $50,000+ monthly), a premium course on crypto tax strategy ($2,000 price point, 200+ students), and a paid newsletter with 5,000+ subscribers at $20/month.

The key success factors were: extreme niche focus that eliminated competition, high commercial intent audience willing to pay for solutions, diversified revenue streams, and consistent educational content that built authority. This creator’s story demonstrates that massive audiences are not necessary for creator success—targeted, high-intent audiences are more valuable.

Case Study 2: The Community Builder

A fitness creator transitioned from Instagram workout videos to a comprehensive community business. Starting with free content that demonstrated expertise, they built an email list through a free 7-day challenge. This list became the foundation for a paid community hosted on Circle, where members paid $49/month for workout programs, nutrition guidance, and direct access to the creator. The community grew to 2,000+ members, generating nearly $100,000 in monthly recurring revenue.

Beyond subscriptions, the creator launched digital products (workout templates, meal plans), group coaching programs, and an annual retreat. Total annual revenue exceeded $2 million with a team of just three people. The success factors were: systematic conversion of social followers to owned audience, focus on transformation and results rather than content consumption, and tiered offerings that served customers at different price points and commitment levels.

Case Study 3: The Multi-Platform Strategist

A technology reviewer built resilience through aggressive platform diversification. Rather than building solely on YouTube (where they started), they systematically expanded to TikTok for discovery, Twitter/X for industry commentary, a newsletter for deeper analysis, and a podcast for long-form interviews. Each platform served a different purpose in the business: TikTok brought new audiences through viral clips, YouTube provided advertising revenue and detailed reviews, the newsletter enabled direct communication and affiliate marketing, and the podcast built industry relationships and sponsorship revenue.

When YouTube algorithm changes reduced reach for tech content in 2025, the creator’s business remained stable because other channels compensated. Total revenue exceeded $500,000 annually, split relatively evenly across platforms. The key lesson: platform diversification is not just about reach—it is about business resilience. This creator’s experience illustrates why sophisticated creators in 2026 view platform dependency as an existential risk that must be actively managed through diversification strategies.

The implementation of this multi-platform strategy required significant investment in workflow optimization. The creator developed systems for repurposing content across platforms, used scheduling tools to maintain consistent presence, and built a small team to handle platform-specific optimization. This operational infrastructure enabled the creator to maintain quality across channels without burning out—a common failure mode for creators who attempt multi-platform presence without adequate systems.

Future Outlook and Predictions 2026-2030

The creator economy will undergo significant evolution in the coming years, driven by technological change, platform competition, and maturing business models. The following predictions outline likely developments through 2030.

Market Size and Growth Projections

Industry analysts project the creator economy will approach $500 billion by 2027 and could exceed $1.35 trillion by 2035, representing a CAGR of 22-26%. Goldman Sachs estimates the market could approach half a trillion dollars by 2027 alone. This growth will be driven by increasing brand investment in creator marketing, expansion of creator tools and infrastructure, and the continued shift of consumer attention from traditional media to creator content.

The creator economy is expected to overtake the traditional advertising agency sector in value within this timeframe, representing a fundamental shift in how marketing content is produced and distributed. Unilever’s commitment to allocate 50% of marketing spend to influencers signals broader corporate recognition of this shift.

AI Integration and Creator Evolution

By 2030, AI will be fully integrated into every aspect of creator workflows. The distinction between AI-assisted and human-created content will become meaningless as creators routinely use AI for research, scripting, editing, distribution, and audience interaction. However, this integration will raise the baseline for content quality, making it harder for creators who do not effectively leverage AI to compete.

The most successful creators will be those who combine AI efficiency with genuine human insight, personality, and expertise. AI will handle production tasks while creators focus on strategy, community building, and unique perspectives that AI cannot replicate. This evolution will transform creators from content producers to creative directors overseeing AI-assisted production.

Platform Consolidation and New Entrants

The platform landscape will likely see both consolidation and disruption. Dominant platforms (YouTube, Meta properties, TikTok) will face increasing regulatory pressure, potentially creating opportunities for new entrants. Emerging platforms focused on specific verticals or creator-friendly policies may capture significant market share, particularly if major platforms make creator-hostile policy changes.

Decentralized platforms and blockchain-based creator tools may gain traction, offering creators ownership of their content and direct audience relationships without platform intermediaries. While adoption has been limited to date, technological maturation and creator frustration with platform policies could accelerate decentralized alternatives.

Professionalization and Industry Maturation

The creator economy will continue professionalizing, with established career paths, industry standards, and professional organizations. Creator education will become formalized, with universities offering degrees in content creation and creator business management. Industry associations will develop to advocate for creator interests, establish ethical standards, and provide professional development.

This professionalization will raise barriers to entry while improving conditions for established creators. The “wild west” phase of the creator economy will give way to a more structured industry with clearer paths to success and clearer reasons why many creators fail. Industry associations will emerge to advocate for creator rights, establish ethical standards for brand partnerships, and provide professional development resources. Educational institutions will offer formal training in content creation, audience development, and creator business management, creating a pipeline of professionally prepared talent.

The regulatory landscape will also evolve significantly. Governments worldwide are grappling with how to classify creators—are they employees, independent contractors, or something entirely new? Tax implications, labor protections, and intellectual property rights will be clarified through legislation and court decisions. Platforms will face increasing pressure to provide transparency in algorithmic decision-making and to share more revenue with the creators who generate their content. These changes will create both opportunities and challenges, potentially raising costs for creators while improving working conditions and income stability.

Key Takeaways

The digital creator economy in 2026 represents a maturing industry with enormous potential but significant challenges. Based on our comprehensive analysis, here are the critical insights for brands, investors, and creators navigating this landscape:

- The creator economy reached $234 billion in 2026 and is projected to exceed $1.35 trillion by 2035, making it one of the fastest-growing sectors in the global economy with a 22.5% CAGR.

- Over 207 million active creators exist worldwide, but income inequality is extreme—only 4% earn over $100,000 annually while 50% earn under $15,000, creating sustainability challenges for the majority.

- AI adoption is nearly universal among creators (84%), with top earners using AI tools twice as frequently and achieving 2-5x higher engagement rates than those who do not leverage AI.

- Seven major trends define 2026: AI-powered creation, micro-influencer rise, community-first monetization, multi-platform strategies, subscription growth, evolved brand partnerships, and tool ecosystem maturation.

- Platform dependency remains the top creator challenge (51.7% cite algorithm unpredictability), driving the strategic shift toward owned audiences and diversified revenue streams.

- YouTube has paid creators over $70 billion through its Partner Program, making it the largest source of platform-to-creator payouts, while TikTok pays only $0.02-$0.04 per 1,000 views.

- Micro and nano-influencers now capture 45.5% of influencer marketing spending as brands prioritize engagement and authenticity over raw reach metrics.

- Successful creators in 2026 operate as full-stack media companies, combining content creation with community building, product development, and direct audience relationships.

- The future belongs to niche specialists who establish authority in specific domains rather than generalists competing for mass attention in saturated markets.

- Creator burnout and mental health challenges have reached epidemic levels, with professional creators reporting 60+ hour work weeks and chronic stress from the always-on nature of social media.

Sources and Citations

- Research Nester – Creator Economy Market Size & Share Forecast Report 2026-2035: https://www.researchnester.com/reports/creator-economy-market/5691

- Evolvance Market Research – Creator Economy Market Size: https://evolvancemarketresearch.com/reports/creator-economy-market/

- Archive.com – 25 Creator Economy Market Size Statistics: https://archive.com/blog/creator-economy-market-size

- Circle.so – Creator Economy Statistics for 2026: https://circle.so/blog/creator-economy-statistics

- Companies History – Creator Economy Statistics and Market Size 2026: https://www.companieshistory.com/creator-economy-market-size/

- Autofaceless.ai – Content Monetization Statistics 2026: https://autofaceless.ai/blog/content-monetization-statistics-2026

- Forbes – 7 Most Profitable Platforms for Creators in 2026: https://www.forbes.com/sites/meggenharris/2026/03/25/7-of-the-most-profitable-platforms-for-creators-in-2026–how-they-pay/

- Stan Store – 8 Trends That Will Define the Creator Economy in 2026: https://stan.store/blog/creator-economy-trends-2026/

- eMarketer – Creator Economy 2026: https://www.emarketer.com/content/creator-economy-2026

- Business Insider – 17 Creator Economy Startups to Watch: https://www.businessinsider.com/creator-economy-ai-startups-to-watch-according-vc-investors-2026-3

- Ellty – 15 Creator Economy Investors Funding Content Startups 2026: https://www.ellty.com/blog/creator-economy-investors

- Goldman Sachs – The Creator Economy Could Approach Half-a-Trillion Dollars by 2027: https://www.goldmansachs.com/insights/articles/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027

- Precedence Research – Creator Economy Market Size to Hit USD 2084.57 Billion by 2035: https://www.precedenceresearch.com/creator-economy-market

- Netinfluencer – Creators Cite Algorithm Unpredictability As Top Challenge: https://www.netinfluencer.com/creators-cite-algorithm-unpredictability-as-top-challenge-in-2026-survey/

- Street Fight – Biggest Risks Facing Influencer Marketing in 2026: https://streetfightmag.com/2026/01/21/the-biggest-risks-facing-influencer-marketing-in-2026/