The creator economy has reached an unprecedented inflection point. What began as a side hustle for passionate hobbyists has evolved into a $313.95 billion global industry supporting over 207 million active creators worldwide. Yet beneath the impressive headlines lies a stark reality: while MrBeast earns $82 million annually and the top 10% of creators on platforms like Uscreen generated $171 million over the past 12 months, 50% of all creators earn less than $5,000 per year, and only 4% surpass the $100,000 threshold that defines professional success.

This isn’t just another market analysis—it’s a data-driven examination of who wins, who loses, and what separates six-figure creators from those earning pocket change. Whether you’re considering content creation as a career, optimizing existing revenue streams, or deciding where to invest your limited time and resources, the statistics in this report provide the benchmarks you need to navigate an increasingly competitive and unforgiving landscape.

Market Overview: The $313.95 Billion Creator Economy Ecosystem

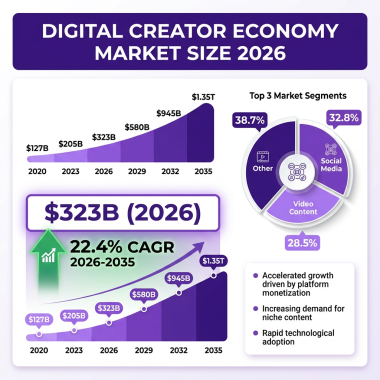

The global creator economy has experienced explosive growth over the past decade, transforming from a niche digital phenomenon into one of the most significant economic forces of the 21st century. According to Precedence Research, the creator economy market size reached $254.4 billion in 2025 and is projected to surge to $313.95 billion in 2026, representing a year-over-year growth rate of approximately 23.4%.

This growth trajectory shows no signs of slowing. Industry analysts project the market will reach $528.39 billion by 2030 and an astounding $2.08 trillion by 2035, expanding at a compound annual growth rate (CAGR) of 23.41% from 2026 to 2035. These figures position the creator economy as one of the fastest-growing sectors in the global economy, outpacing traditional media, advertising, and even many technology subsectors.

The historical evolution of this market tells a compelling story. In 2023, the creator economy was valued at $127.65 billion. By 2024, it had grown to approximately $156.37 billion, and then to $191.55 billion as reported by Exploding Topics. The 2026 projection of $313.95 billion represents a near-tripling of the market in just three years—a growth rate that few industries can match.

Regional distribution reveals North America’s continued dominance, accounting for 35-40% of the global market share in 2025. The United States remains the epicenter of creator economy innovation, home to the largest platforms, most successful creators, and highest advertising spend. However, Asia Pacific is emerging as the fastest-growing region, with countries like India, Indonesia, and the Philippines experiencing explosive creator adoption rates.

In March 2025, the Government of India announced a landmark $1 billion fund for content creators, alongside ₹391 crore ($47 million) for the Indian Institute of Creative Technologies in Mumbai. This investment signals a broader trend of governments recognizing the creator economy’s potential for job creation, cultural export, and economic development.

Europe represents approximately 25% of the global market, with the UK, Germany, and France leading in creator adoption and monetization. Latin America and the Middle East, while smaller in absolute terms, are experiencing some of the highest growth rates as internet penetration increases and mobile-first content consumption becomes the norm.

Key Statistics and Data: The Numbers Behind the Creator Economy

Understanding the creator economy requires diving deep into the statistics that define this complex ecosystem. The numbers reveal both unprecedented opportunity and brutal inequality—a market where astronomical success coexists with widespread struggle.

Creator Population and Distribution: There are currently over 207 million content creators worldwide actively participating in the creator economy. Of these, approximately 48% operate as solo creators, managing their communities, content production, and monetization strategies entirely independently. Only 2 million creators—less than 1% of the total—qualify as professional creators earning a full-time living from their content.

Income Distribution and Reality: The income distribution in the creator economy follows a stark power law. According to multiple industry reports, 50% of creators earn up to $5,000 annually, often less than minimum wage when accounting for hours invested. Another 33% earn between $5,000 and $30,000 per year. Only 17% make between $30,000 and $100,000, and a mere 7% earn over $100,000 annually. This means 93% of creators earn less than a typical professional salary.

The average content creator in the United States makes $44,000 per year, equivalent to approximately $22 per hour or $3,680 per month. However, this average masks enormous variation—the salary range spans from $36,000 to $58,500 for typical creators, with top earners generating up to $74,500 annually. These figures exclude the elite earners making millions.

Platform-Specific Earnings: YouTube and TikTok tie as the top-paying platforms for creators. YouTube’s median earnings for full-time creators reached $141,000 in 2025—the highest and most stable platform income. Most successful YouTube creators earn 60-70% of their revenue from advertising through the YouTube Partner Program. TikTok creators, while having access to the Creator Fund, increasingly rely on brand partnerships, with influencers commanding $1,000-$3,000 per sponsored post for every 50,000 followers.

Instagram remains a powerhouse for influencer marketing, with the platform generating significant brand deal opportunities. However, the data shows that only 34% of creators earn their primary income from platform ads—most successful creators diversify across multiple revenue streams.

Revenue Source Breakdown: Brand deals dominate creator income, accounting for 68.8% of creators’ primary revenue source. However, this represents a decline from 2021, when 91% of creators received income from sponsored content, dropping to 82% by 2023. During this same period, affiliate marketing grew from 47% to 56% of creators, advertising revenue jumped from 18% to 33%, and merchandise sales increased from 11% to 15%.

Other significant revenue sources include: starting own brand (4.8%), affiliate links (4.6%), courses (4.4%), tips (3.5%), and various other monetization methods (2.7%). Notably, 3.7% of creators report no income at all from their content creation efforts.

Time to Monetization: The path to earning in the creator economy is slow and demanding. Content creators require an average of 6.5 months to earn their first dollar, more than 10 months to become self-supporting, and 24 months or more to secure their first brand partnership. This extended ramp-up period means most creators must sustain themselves through other income sources while building their audience and credibility.

Influencer Marketing Spend: Brands invested over $32 billion in influencer marketing in 2025, with this figure projected to grow significantly through 2026. The IAB’s 2025 Creator Economy Ad Spend & Strategy Report estimates $37 billion in U.S. creator ad spend alone. User-generated content has now surpassed traditional media in advertising revenue for the first time ever—a watershed moment for the industry.

Platform Dominance by Segment: Video streaming platforms dominate the creator economy, accounting for approximately 40% of market activity. Social media platforms represent 25%, audio and podcasting platforms 15%, gaming platforms 12%, and other platforms including e-commerce and blogging account for the remaining 8%. Within video, short-form content has seen explosive growth, with platforms like TikTok, Instagram Reels, and YouTube Shorts driving significant engagement and monetization opportunities.

Major Trends Shaping the Digital Creator Economy in 2026

The creator economy is evolving at a breakneck pace, with seven major trends defining the landscape in 2026. These trends represent both opportunities and challenges for creators navigating an increasingly complex ecosystem.

Trend 1: Creator and Entrepreneur Convergence

The line between creator and entrepreneur has become virtually indistinguishable. Most entrepreneurs are now creators building their personal brand, and most creators are entrepreneurs using their audience as a distribution channel. Rather than relying on unpredictable platform payouts or brand deals, creators are building diversified income streams they own.

We’re seeing more creators launch product lines, build teams, raise capital, and step into roles traditionally held by founders and C-suite executives. MrBeast, Emma Chamberlain, and Alex Cooper represent prime examples—running multi-seven-figure businesses powered by digital products, consumer lines, podcasts, streaming deals, and merchandise. They’re not just “posting online”—they’re building empires.

Trend 2: AI-Powered Content Creation

Artificial intelligence is fundamentally transforming how creators produce content. AI-driven platforms like ChatGPT, Jasper, and Copy.ai are gaining traction among individual creators and small businesses, simplifying and advancing content production. AI-generated characters enable authentic storytelling even without a real person, while tools like Adobe Sensei and RunwayML provide sophisticated editing capabilities previously available only to professionals.

AI is accelerating content creation while simultaneously testing authenticity. Social platforms are maturing while brands demand clearer ROI. The creators who thrive will be those who use AI as an amplifier of their unique voice rather than a replacement for it.

Trend 3: Owned Audiences and Community-Led Business Models

As burnout and attention scarcity reshape member behavior, community-led business models and owned memberships are emerging as the most sustainable foundation for creator income. Creators are increasingly moving their audiences off platforms they don’t control—building email lists, private communities, and membership sites that provide direct relationships with their most engaged fans.

By revenue channel, advertising dominated the market in 2025, but the subscriptions segment is expected to grow at the fastest CAGR from 2026 to 2035. This shift reflects creators’ desire for predictable, recurring revenue rather than volatile ad-based income.

Trend 4: Diversified Revenue Streams

The era of relying on a single platform or revenue source is over. Successful creators in 2026 operate diversified businesses with multiple income streams: brand partnerships, affiliate marketing, digital products, courses, merchandise, subscriptions, and increasingly, their own product lines and services.

Data shows that creators with 3+ revenue streams are significantly more likely to achieve professional income levels. The most successful creators treat their content as the top of a funnel that feeds into higher-margin, owned revenue streams.

Trend 5: Short-Form Video Dominance

Short-form video has become the dominant content format across all platforms. TikTok, Instagram Reels, and YouTube Shorts are driving the majority of new creator growth and audience engagement. The format’s low barrier to entry and high virality potential make it attractive for new creators, while established creators use it as a discovery mechanism to funnel audiences to long-form content and monetization opportunities.

However, the data reveals a crucial insight: while short-form drives discovery, long-form content generates higher monetization per view. The most successful creators use short-form as a funnel to their more profitable long-form and owned content.

Trend 6: Virtual Influencers and AI-Generated Personalities

The rise of virtual influencers represents one of the most fascinating developments in the creator economy. AI-generated characters can now create authentic-feeling content without the risks, costs, and limitations of human creators. These virtual personalities never age, never scandalize, and can be programmed to appeal to specific demographics with precision.

While still a small segment of the overall market, virtual influencers are growing rapidly and challenging traditional notions of authenticity and parasocial relationships in the creator economy.

Trend 7: Creator Investment in the Creator Economy

Top creators are increasingly investing directly into the future of the creator economy, putting their money behind platforms and people they believe will propel it forward. Stan Store raised the largest creator-led funding round ever, backed by Steven Bartlett and GaryVee. Steven Bartlett has continued investing heavily in other Creator brands as part of his vision to build the “Disney of the Creator economy.”

This trend represents a maturation of the creator economy—successful creators are no longer just participants but active investors shaping the industry’s future.

Key Players and Competitive Landscape

The creator economy ecosystem comprises multiple layers of platforms, tools, and service providers. Understanding the competitive landscape is essential for creators choosing where to invest their time and for businesses looking to enter this market.

Major Platforms: YouTube remains the dominant platform for long-form video creators, with the most mature monetization infrastructure through the YouTube Partner Program. The platform’s median creator earnings of $141,000 make it the most lucrative for established creators. YouTube Shorts has successfully challenged TikTok’s dominance in short-form video while providing better monetization pathways.

TikTok revolutionized short-form content and remains the platform of choice for reaching younger demographics. However, its monetization tools lag behind competitors, forcing creators to rely heavily on brand partnerships rather than platform payouts.

Instagram continues to dominate influencer marketing, with its combination of feed posts, Stories, Reels, and shopping features making it attractive for brand collaborations. The platform’s algorithm changes in recent years have prioritized Reels, forcing creators to adapt their content strategies.

Emerging Platforms: New platforms are constantly entering the market. BeReal gained significant traction with its authentic, unfiltered approach before being acquired. Twitch dominates live streaming for gaming and creative content. Spotify has invested heavily in podcasting and audio content. Each platform offers unique opportunities and challenges for creators.

Creator Tools and Infrastructure: The creator economy infrastructure layer includes companies providing essential tools for content creation, distribution, and monetization. Shopify leads in e-commerce enablement with $5.2 billion in annual revenue supporting the creator economy. Link-in-bio tools like Linktree and Beacons have become essential for creators managing multiple revenue streams.

AI-powered content creation tools are rapidly gaining market share. CapCut, owned by ByteDance (TikTok’s parent company), has become the dominant video editing tool for short-form content. Canva provides accessible design tools for creators without professional design skills. These tools lower the barrier to entry while increasing content quality expectations.

Monetization Platforms: Beyond advertising, creators use specialized platforms for different revenue streams. Patreon and Buy Me a Coffee enable fan subscriptions. Stan Store and Gumroad facilitate digital product sales. Teachable and Kajabi support online courses. Each platform takes a percentage of creator earnings, creating a complex ecosystem of fees and revenue sharing.

Venture Capital and Investment: The creator economy has attracted significant venture capital investment. Slow Ventures launched a $60 million dedicated creator fund in February 2025. Benchmark has led major investments in creator economy startups. Top-funded companies include ShopMy ($169 million raised), GRIN ($145 million), and various AI-powered creator tools.

According to Failory’s analysis of creator economy VC firms, the sector has attracted investment from both specialized creator funds and generalist venture capital firms recognizing the market’s growth potential.

Challenges and Pain Points in the Creator Economy

Despite the impressive growth statistics, the creator economy faces significant challenges that creators, platforms, and investors must navigate. Understanding these pain points is essential for anyone looking to build or invest in this space.

Challenge 1: Income Inequality and Sustainability

The most significant challenge facing the creator economy is extreme income inequality. With 50% of creators earning less than $5,000 annually and only 4% achieving professional income levels, the vast majority of participants cannot sustain themselves through content creation alone. This creates a “winner-take-most” dynamic that discourages new entrants and leads to high burnout rates among mid-tier creators.

The data reveals that nearly half of independent creators report having a hard time being successful in the creator economy, and 41% have experienced burnout. The pressure to constantly produce content, engage with audiences, and chase algorithmic favor takes a significant toll on creator mental health.

Challenge 2: Platform Dependency and Algorithm Volatility

Creators remain dangerously dependent on platforms they don’t control. Algorithm changes can destroy years of audience building overnight. Platform policy changes can eliminate monetization options. Account bans, often automated and without recourse, can end careers.

The recent trend of platforms reducing organic reach to force creators into paid promotion creates a challenging environment where creators must constantly pay to reach their own audiences. This “pay-to-play” dynamic particularly hurts smaller creators with limited marketing budgets.

Challenge 3: Content Saturation and Attention Scarcity

With 207 million creators producing content, the market is experiencing severe saturation. Breaking through the noise requires either exceptional talent, significant marketing spend, or algorithmic luck. The average person’s attention is fragmented across dozens of apps and platforms, making audience retention increasingly difficult.

Creators report that building an audience takes longer than ever, with the average time to first dollar increasing from 4 months in 2020 to 6.5 months in 2025. The window for organic growth is closing as platforms mature and competition intensifies.

Challenge 4: Monetization Complexity

The diversification of revenue streams, while beneficial for stability, adds significant complexity to creator businesses. Managing brand partnerships, affiliate relationships, digital product sales, subscriptions, and platform payouts requires business skills that many creators lack. The administrative burden can consume time that would otherwise go toward content creation.

Additionally, creators face complex tax situations, often operating as independent contractors responsible for their own tax withholding, healthcare, and retirement savings. The lack of benefits and job security creates financial instability even for creators with healthy gross revenues.

Opportunities and Growth Strategies

Despite the challenges, significant opportunities exist for creators and businesses willing to adapt to the evolving landscape. These strategies separate successful creators from those who struggle.

Opportunity 1: Niche Specialization

The data consistently shows that specialized creators outperform generalists. Creators who focus on specific niches—whether technical topics, hobby communities, or professional expertise—can command higher rates and build more engaged audiences. The era of being a “lifestyle influencer” is ending; the future belongs to creators with genuine expertise and authentic passion for specific subjects.

Successful niche creators often start with professional or educational backgrounds in their content areas, providing genuine value that attracts dedicated audiences willing to pay for expertise.

Opportunity 2: Community-First Business Models

Creators building owned communities through platforms like Circle, Discord, or private membership sites are achieving more sustainable businesses than those relying solely on algorithmic platforms. These communities provide predictable recurring revenue, direct audience relationships, and higher engagement rates.

The data shows that community-led business models are emerging as the most sustainable foundation for creator income, with subscriptions growing faster than advertising as a revenue channel.

Opportunity 3: AI-Augmented Creation

Rather than viewing AI as a threat, successful creators are using AI tools to amplify their productivity and creativity. AI can handle research, scripting, editing, and distribution tasks, allowing creators to focus on the human elements that differentiate their content. The creators who thrive in 2026 will be those who become AI-augmented entrepreneurs, managing diversified revenue streams with AI assistance.

Tools like ChatGPT for scripting, Midjourney for thumbnails, and automated editing software are becoming standard in professional creator workflows.

Opportunity 4: Cross-Platform Presence

Successful creators maintain presence across multiple platforms while using each platform strategically. Short-form content on TikTok and Reels drives discovery, while long-form content on YouTube and podcasts builds deeper audience relationships. Email lists and communities provide owned channels for direct monetization.

The data shows that creators active on 3+ platforms have significantly higher income stability and growth potential than single-platform creators.

Case Studies and Success Stories

Examining specific success stories provides valuable insights into what works in the creator economy. These case studies represent different paths to success and highlight key strategies that aspiring creators can emulate.

Case Study 1: MrBeast (Jimmy Donaldson)

MrBeast represents the pinnacle of creator economy success, earning an estimated $82 million annually across his various ventures. His strategy combines extreme content production values with diversified business operations. Rather than relying solely on YouTube ad revenue, MrBeast has built a multi-channel empire including merchandise (MrBeast Burger, Feastables chocolate), sponsorships, and content licensing.

Key lessons from MrBeast’s success include: reinvesting nearly all revenue into content production to maintain growth, building a team of over 100 employees to scale operations, and treating content as a product requiring significant capital investment. His approach demonstrates that creator businesses can scale to traditional media company levels with the right strategy and execution.

Case Study 2: Emma Chamberlain

Emma Chamberlain transitioned from YouTube vlogger to multi-faceted entrepreneur, building a coffee company (Chamberlain Coffee) valued at over $30 million, a podcast network, and numerous brand partnerships. Her success demonstrates the power of authentic personal branding and strategic business diversification.

Chamberlain’s approach emphasizes maintaining authentic connection with her audience while building products that align with her personal brand. Rather than taking every sponsorship opportunity, she has been selective about partnerships, preserving audience trust while building her own businesses.

Case Study 3: The Rise of Creator-Led Education

Creators like Ali Abdaal (productivity), Graham Stephan (finance), and Marques Brownlee (technology) have built significant businesses around educational content. These creators leverage their expertise to sell courses, templates, and digital products at premium prices, often generating more revenue from products than from platform ads.

This model works particularly well for creators with professional expertise in high-value niches. The combination of free content that demonstrates expertise and paid products that provide deeper value creates a sustainable business model less dependent on platform algorithms.

Future Outlook and Predictions (2026-2030)

The creator economy’s trajectory points toward continued explosive growth, but the nature of that growth will evolve significantly. Here are the key predictions for the remainder of this decade.

Market Size Projections: Multiple analyst firms project the creator economy will reach between $525 billion and $600 billion by 2030, with some estimates as high as $820 billion. The most conservative projections show a CAGR of 22-23%, while more aggressive forecasts suggest 26%+ growth rates. By 2035, the market could exceed $2 trillion, making it larger than many traditional media industries combined.

Goldman Sachs Research expects the 50 million global professional creators to grow at a 10-20% compound annual rate, while spending on influencer marketing and platform payouts fueled by short-form video monetization will drive the majority of market growth.

Platform Evolution: The platform landscape will continue consolidating, with major players acquiring smaller competitors and expanding their feature sets. We expect to see more platforms offering comprehensive creator tool suites—combining content hosting, monetization, community features, and commerce in single ecosystems.

AI integration will become standard across all platforms, with automated editing, content recommendations, and audience analysis becoming table stakes. Platforms that fail to offer competitive AI tools will lose creators to more advanced competitors.

Monetization Innovation: New monetization models will emerge beyond current advertising, subscriptions, and brand partnerships. Creator tokens, fractional ownership of content, and blockchain-based revenue sharing are likely to gain traction. However, regulatory scrutiny of these models will increase as they become more mainstream.

The smallest creators will claim close to 50% of total creator economy revenue by 2030, according to eMarketer projections, as platforms improve monetization tools for emerging creators and micro-influencers prove more effective for brand campaigns than mega-influencers.

Professionalization of Creator Work: The creator economy will increasingly resemble traditional industries in terms of professional standards, unionization, and regulatory oversight. We’re already seeing the formation of creator unions and advocacy groups pushing for better platform terms, transparent algorithms, and fair revenue sharing.

Creator education will become a significant sub-industry, with universities and professional training programs offering degrees and certifications in content creation, audience development, and creator business management.

Key Takeaways

- The creator economy reached $313.95 billion in 2026 and is projected to grow to $2.08 trillion by 2035 at a 23.41% CAGR

- Only 4% of creators earn professional incomes ($100K+), while 50% earn less than $5,000 annually—success requires exceptional strategy or significant time investment

- Brand deals remain the primary revenue source (68.8%), but diversification across multiple streams is essential for sustainability

- AI-powered content creation, community-led business models, and creator-entrepreneur convergence are the defining trends of 2026

- Successful creators treat their work as a business, building teams, diversifying revenue, and investing in owned audiences rather than relying solely on platform algorithms

Sources and Citations

- Precedence Research – Creator Economy Market Size Report 2026: https://www.precedenceresearch.com/creator-economy-market

- Exploding Topics – Creator Economy Market Size (2025-2030): https://explodingtopics.com/blog/creator-economy-market-size

- AutoFaceless – Content Creator Income Statistics 2026: https://autofaceless.ai/blog/content-creator-income-statistics-2026

- Stan Store – 8 Trends That Will Define the Creator Economy in 2026: https://stan.store/blog/creator-economy-trends-2026/

- ThriveCart – State of the Global Creator Economy 2025-26: https://thrivecart.com/resources/state-of-the-global-creator-economy-2025-26/

- Goldman Sachs – The Creator Economy Could Approach Half-a-Trillion Dollars by 2027: https://www.goldmansachs.com/insights/articles/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027

- Circle Blog – Creator Economy Statistics for 2026: https://circle.so/blog/creator-economy-statistics

- eMarketer – Creator Economy 2026: https://www.emarketer.com/content/creator-economy-2026

- DemandSage – Creator Economy Statistics: https://www.demandsage.com/creator-economy-statistics/

- Forbes – 7 Of The Most Profitable Platforms For Creators In 2026: https://www.forbes.com/sites/meggenharris/2026/03/25/7-of-the-most-profitable-platforms-for-creators-in-2026/

- Failory – Top 13 Creator Economy Venture Capital Firms (2026): https://www.failory.com/blog/creator-economy-venture-capital-firms

Additional Market Dynamics and Emerging Segments:

Beyond the headline figures, several emerging segments within the creator economy warrant detailed examination. The music production segment, while currently smaller than video and photography, is projected to grow at the fastest CAGR through 2035. This growth is driven by the democratization of music production tools, the rise of platforms like Spotify and Apple Music for independent artists, and the increasing use of creator-made music in short-form video content.

The podcasting platform segment is also experiencing notable growth, fueled by increased investment from major platforms and the continued expansion of podcast listenership globally. Spotify’s exclusive deals with high-profile creators and the platform’s investment in podcasting infrastructure have legitimized audio content as a serious creator business model.

Gaming platforms represent another significant segment, with Twitch, YouTube Gaming, and emerging platforms like Kick competing for creator talent. The gaming creator economy extends beyond live streaming to include esports, game development, and gaming-related merchandise and digital products. Top gaming creators can earn millions annually through a combination of platform revenue, sponsorships, and their own product lines.

Demographic Shifts in Creator Economy Participation:

The demographic composition of the creator economy is evolving. While Gen Z and Millennials remain the dominant participants, we’re seeing increasing participation from older demographics who bring professional expertise and established networks to their creator businesses. The “expert creator”—someone with decades of industry experience sharing their knowledge—is becoming a significant force, particularly in B2B niches, finance, technology, and professional development.

Geographic diversification is also accelerating. While the United States and Western Europe have historically dominated, creators from Southeast Asia, Latin America, and Africa are gaining global audiences. This geographic expansion is enabled by improved internet infrastructure, affordable smartphones, and platforms that support multiple languages and currencies.

The Role of Traditional Media and Brand Integration:

Traditional media companies are increasingly integrating creator economy strategies into their operations. We’re seeing established media brands launching creator programs, acquiring creator-led media companies, and hiring creators as on-air talent. This convergence between traditional and creator media is blurring the lines between “professional” and “amateur” content production.

Brands are also evolving their approach to creator partnerships. The era of one-off sponsored posts is giving way to long-term ambassador relationships, co-created product lines, and equity partnerships where creators receive ownership stakes in the brands they promote. These deeper partnerships align creator and brand incentives more effectively and generate better returns for both parties.

Regulatory Environment and Legal Considerations:

The regulatory environment surrounding the creator economy is becoming more complex. Disclosure requirements for sponsored content have tightened globally, with the FTC in the United States and similar bodies in Europe and Asia increasing enforcement. Creators must now navigate a complex web of advertising standards, copyright laws, and platform-specific policies.

Intellectual property rights represent another growing concern. As creators build businesses around their content, questions of ownership, licensing, and derivative works become increasingly important. The rise of AI-generated content has added new dimensions to these debates, with ongoing discussions about training data rights, synthetic media disclosure, and the definition of creative authorship.

Taxation of creator income is also receiving increased scrutiny. As more individuals earn significant income through creator activities, tax authorities are developing guidance specific to this form of work. Creators must navigate complex situations involving multiple revenue streams, international income, and business expense deductions.

Technology Infrastructure and Creator Tools Evolution:

The technology infrastructure supporting creators has evolved dramatically. Cloud-based editing tools enable creators to produce broadcast-quality content from anywhere. AI-powered tools handle tasks from transcription to thumbnail generation to content optimization. Analytics platforms provide detailed insights into audience behavior, content performance, and revenue attribution.

Merchandise and fulfillment services have become increasingly sophisticated. Print-on-demand technology eliminates inventory risk. Direct-to-consumer shipping integrations simplify logistics. White-label product development allows creators to launch physical products without manufacturing expertise.

Financial services tailored to creators are also emerging. Creator-specific banking products, tax services, and investment platforms recognize the unique financial situations of content entrepreneurs. These services address the irregular income patterns, multiple revenue streams, and international transactions common in creator businesses.

Educational and Training Ecosystem:

The creator education market has exploded alongside the creator economy itself. Courses on content creation, audience growth, monetization strategies, and business management for creators generate significant revenue. Established creators often earn more from teaching others to create content than from their original content activities.

This educational ecosystem includes formal courses, coaching programs, mastermind groups, and community-based learning. While quality varies significantly, the best programs provide genuine value and accelerate creator success. However, the proliferation of “get rich quick” schemes targeting aspiring creators represents a concerning trend that regulators and platforms are beginning to address.

Universities and traditional educational institutions are also entering the creator education space. Programs in digital media, content strategy, and influencer marketing are becoming common. Some institutions have launched dedicated creator economy curricula, recognizing the sector’s growing economic importance and career potential.

Social Impact and Cultural Influence:

The creator economy’s impact extends beyond economics into social and cultural spheres. Creators have become influential voices in politics, social movements, and cultural conversations. Their ability to reach massive, engaged audiences gives them power that rivals traditional media and political institutions. This influence brings both opportunities for positive impact and responsibilities that many creators are still learning to navigate.

The representation and diversity within the creator economy has improved but remains uneven. While platforms have made efforts to support underrepresented creators, data shows that creator income and opportunity still skew toward certain demographics. Addressing these disparities represents both a moral imperative and a market opportunity, as diverse creators can reach underserved audiences.

Mental health within the creator community has received increasing attention. The pressure to constantly produce content, maintain public personas, and deal with online harassment takes significant psychological tolls. Creator burnout is common, with many successful creators taking extended breaks or leaving the industry entirely. Platforms and creator service providers are beginning to offer mental health resources, but systemic challenges remain.

Environmental and Sustainability Considerations:

The environmental impact of the creator economy is an emerging concern. Content creation and consumption require significant energy, from the devices used to create and view content to the data centers powering platforms. Physical merchandise, a major revenue source for many creators, involves manufacturing and shipping impacts. As environmental consciousness grows, creators and platforms face pressure to adopt more sustainable practices.

Some creators have made sustainability a core part of their brand, promoting eco-friendly products and practices. Others are exploring digital-only revenue models that minimize physical environmental impact. Platform policies around environmental claims and sustainable practices are likely to evolve as this issue gains prominence.

Competitive Dynamics and Market Consolidation:

The creator economy is experiencing significant consolidation. Large platforms are acquiring smaller competitors and creator tool companies. Major creators are acquiring smaller creators’ businesses or bringing them under management companies. This consolidation concentrates power and resources but may also provide smaller creators with access to better tools and opportunities.

Barriers to entry, while still lower than traditional media, are rising. Content quality expectations have increased dramatically. Algorithmic distribution favors established creators with large audiences. The cost of professional equipment, software, and team members can be substantial. These factors may slow the growth of new creator entrants and favor those with existing resources.

However, niche opportunities remain abundant. Specialized knowledge, unique perspectives, and authentic connections with specific communities can still drive success even without massive resources. The key is finding underserved audiences and serving them exceptionally well rather than competing for broad attention.

Global Economic Factors and Creator Economy Resilience:

The creator economy has shown remarkable resilience during economic downturns. While brand marketing budgets may fluctuate, the underlying demand for content and the fundamental value creators provide to audiences remain strong. During the COVID-19 pandemic, creator economy activity actually increased as locked-down consumers turned to online content and aspiring creators had time to start their journeys.

However, creators are not immune to economic pressures. Advertising rates fluctuate with economic conditions. Consumer spending on creator products and subscriptions may decline during recessions. Creators without diversified revenue streams are particularly vulnerable to economic shocks.

The creator economy’s growth projections assume continued economic growth and technological advancement. Significant economic disruptions could slow growth or shift the competitive landscape. Creators and platforms that build resilient, diversified businesses will be best positioned to weather potential storms.