The Software as a Service (SaaS) industry has evolved from a disruptive technology into the dominant software delivery model of our era. In 2026, the SaaS market stands at a pivotal inflection point, valued at $465.03 billion according to Precedence Research, with 99% of organizations now using at least one SaaS application in their operations. This represents a fundamental shift in how businesses consume software—from perpetual licenses and on-premise installations to subscription-based, cloud-delivered solutions that scale with organizational needs.

The journey from 2020’s $157 billion market to today’s nearly half-trillion-dollar ecosystem tells a story of relentless innovation, changing work patterns, and the democratization of enterprise-grade tools. The COVID-19 pandemic accelerated adoption by an estimated 5-7 years, forcing even the most traditional enterprises to embrace cloud solutions for remote work, collaboration, and digital transformation. What started as a necessity has become a competitive advantage, with SaaS now commanding 72% of all enterprise software spending according to IDC.

The subscription model has fundamentally changed the economics of software. Rather than large upfront license fees and complex implementation projects, organizations now pay predictable monthly or annual fees for immediate access to continuously updated capabilities. This shift aligns vendor incentives with customer success—vendors must continuously deliver value to maintain recurring revenue, rather than relying on one-time license sales. The result has been an explosion of innovation as SaaS companies compete to demonstrate ongoing value and reduce customer churn.

Market Overview: The $465 Billion Ecosystem

The global SaaS market has demonstrated remarkable resilience and growth trajectory throughout economic cycles. According to multiple industry analysts, the market size varies based on segmentation methodology, but the consensus points to a market valued between $375 billion and $465 billion in 2026. Precedence Research provides the most comprehensive forecast, estimating the market at $465.03 billion in 2026, up from $408.21 billion in 2025, representing a year-over-year growth of approximately 14%.

The B2B SaaS segment specifically is experiencing even more explosive growth than the broader market. Mordor Intelligence values the B2B SaaS market at $492.34 billion in 2026, projecting it to reach $1,578.2 billion by 2031 at a CAGR of 26.24%. This divergence in growth rates highlights a crucial trend: while consumer SaaS stabilizes, business applications continue to expand rapidly as enterprises digitize operations across every department from sales and marketing to finance, HR, and operations.

Regional distribution shows North America maintaining dominance with approximately 46.9% of global market share, driven by the concentration of major SaaS vendors and early enterprise adoption. The United States alone hosts over 17,000 SaaS companies, making it the undisputed epicenter of industry innovation. Europe and Asia-Pacific follow, with APAC showing the fastest growth rate as emerging economies accelerate digital transformation initiatives and leapfrog traditional on-premise infrastructure.

The long-term forecast remains exceptionally bullish for the industry. By 2035, the SaaS market is projected to reach $1.37 trillion according to Precedence Research, expanding at a CAGR of 12.85% from 2026 to 2035. Grand View Research offers a slightly more conservative but still impressive projection of $819.23 billion by 2030 at a 12.0% CAGR. These figures underscore that SaaS is not a mature market approaching saturation—it is a growth sector with decades of expansion ahead as more business functions digitize and more organizations adopt cloud-native approaches.

Deployment models continue to evolve alongside market growth. Public cloud SaaS dominates with the largest market share, but hybrid cloud deployments are growing at 20.1% CAGR according to Research and Markets, reaching $176.6 billion by 2030. This reflects enterprise demand for flexibility—combining the scalability of public cloud with the control of private infrastructure for sensitive workloads and regulated data.

Key Statistics and Data Points

The SaaS industry’s scale becomes even more impressive when examining granular statistics across adoption, spending, and operational metrics. These numbers tell the story of an industry that has become foundational to modern business operations:

Market Size and Growth Projections:

- Global SaaS market value 2026: $465.03 billion (Precedence Research)

- 2025 market value: $408.21 billion

- Projected 2030 value: $819.23 billion (Grand View Research)

- Projected 2035 value: $1.37 trillion (Precedence Research)

- CAGR 2026-2035: 12.85%

- Statista 2026 revenue forecast: $512.27 billion

- Revenue growth rate 2026: 19.47%

- B2B SaaS 2026 value: $492.34 billion (Mordor Intelligence)

- B2B SaaS 2031 projection: $1,578.2 billion

- B2B SaaS CAGR: 26.24%

Adoption and Usage Statistics:

- 99% of organizations use at least one SaaS application

- Average enterprise manages 291-371 SaaS applications

- 80-85% of all business applications are expected to be SaaS-based by end of 2026

- 70% of business applications are currently SaaS-based

- Average company spends $3,500 per employee annually on SaaS

- SaaS commands 72% of all enterprise software spending

- Organizations use an average of 80 SaaS apps for collaboration alone

Company and Vendor Landscape:

- Over 30,000 SaaS companies globally

- 17,000 SaaS companies based in the United States

- Average SaaS company has 36,000 customers

- Public SaaS companies serving enterprise: ~1,500 customers

- Public SaaS companies serving mid-market: ~13,000 customers

- Top 15 SaaS companies have combined market cap of $2.1 trillion

- Top 15 generated $100 billion in revenue collectively

Segment Distribution by Category:

- Customer Service Solutions: 17,000 companies

- Marketing Software: 15,000 companies

- eCommerce SaaS: 14,000 companies

- Data and Analytics: 12,000 companies

- Sales Software: 11,000 companies

- CRM represents approximately 28% of SaaS market

- ERP represents approximately 22% of SaaS market

- Collaboration tools represent approximately 18% of SaaS market

Financial and Operational Benchmarks:

- SaaS companies spend 50%+ of revenue on sales and marketing

- VC-backed SaaS spends 47% of revenue on S&M vs 33% for PE-backed

- Median CAC for B2B SaaS: $1,200 per customer (60% increase over 5 years)

- Median CAC payback period: 15-18 months

- Median spend to generate $1 ARR: $2.00

- Average gross margins: 70-85%

- Healthy NRR (Net Revenue Retention): 100%+

- Target LTV:CAC ratio: 3:1 or higher

- Expansion ARR as % of new ARR: 40% average, 50%+ for top performers

- Median blended CAC payback for $5M-$25M ARR SaaS: 18 months

Churn Benchmarks by Segment:

- Enterprise SaaS (>$100K ACV): 0.5-1% monthly churn

- Mid-Market SaaS: 1-2% monthly churn

- SMB SaaS: 3-5% monthly churn

- Excellent annual churn: Below 5%

- Good annual churn: 5-10%

- Concerning monthly churn: Above 7%

- Top quartile mid-market monthly churn: Below 1%

Regional Market Distribution:

- North America: 46.9% of global market share

- United States SaaS market: $187 billion

- Europe: Second largest market by revenue

- Asia-Pacific: Fastest growing region

- North America growth contribution: 56.9% during forecast period

Major Trends Shaping SaaS in 2026

The SaaS landscape is undergoing fundamental transformation driven by technological advancement, changing buyer expectations, and economic pressures. These seven trends are defining the industry in 2026 and will shape competitive dynamics for years to come:

1. AI-Native SaaS Becomes the Standard

Artificial intelligence has transitioned from a differentiating feature to a foundational expectation across all SaaS categories. By 2026, 75% of SaaS companies have embedded AI-driven automation in at least one core process, and the AI SaaS market segment is projected to exceed $200 billion by year-end. Companies like NeuroFlow AI demonstrate this potential, growing from $500K seed funding to $100M ARR in just 18 months by making AI agents the core product rather than an add-on feature.

The distinction between “AI-enabled” and “AI-native” has become critical for investors and customers alike. AI-native companies—those built from the ground up with artificial intelligence as their core architecture—are raising capital at 40% higher valuations than traditional SaaS. Median Series B valuations for AI-powered SaaS hit $175 million in Q3 2025, representing a 38% year-over-year increase. This premium reflects the understanding that AI-native architectures can deliver capabilities and efficiencies impossible for retrofitted competitors.

The integration of AI affects every aspect of SaaS operations—from product development to customer support to sales and marketing. AI-powered code generation accelerates feature development. AI chatbots handle routine support inquiries. AI sales assistants qualify leads and personalize outreach. Companies that fail to leverage AI across their operations face mounting cost disadvantages against AI-native competitors.

2. Usage-Based and Hybrid Pricing Models

The traditional flat-rate subscription model is rapidly giving way to consumption-based pricing that aligns vendor revenue with customer value realization. Over 80% of SaaS companies now use some form of usage-based or hybrid pricing. This shift benefits both parties—customers pay only for what they use, while vendors capture more revenue from high-value customers who derive significant benefit from the platform.

AI is accelerating this transition by making usage tracking more sophisticated and billing more granular. Companies can now meter API calls, compute resources, data storage, feature access, and transaction volume with precision impossible just years ago. This trend particularly benefits infrastructure and developer-tooling SaaS, where consumption correlates directly with customer growth and success.

However, the shift creates challenges. Revenue becomes less predictable, complicating financial planning and potentially affecting valuation multiples. Customers may experience bill shock if usage spikes unexpectedly. Successful implementation requires sophisticated metering infrastructure, clear customer communication, and tools that help customers forecast and control their spending.

3. Vertical SaaS Dominance

Horizontal SaaS—generic tools applicable across industries—faces increasing competition from vertical solutions purpose-built for specific sectors. Vertical AI SaaS companies for healthcare, legal, and financial services raised the largest early-stage rounds in 2025, with median Series A sizes of $22 million versus $15 million for traditional horizontal SaaS.

This specialization delivers superior value through industry-specific workflows, compliance features, and integrations. A construction management SaaS understands job costing, subcontractor coordination, and lien waivers; a generic project management tool does not. As markets mature, vertical solutions capture increasing share by solving industry problems more completely than generalist alternatives.

The vertical SaaS playbook has proven repeatable: identify an underserved industry, build deep domain expertise, achieve category leadership in that vertical, then expand to adjacent functions or geographies. Companies like Toast (restaurants), Shopify (e-commerce), and Procore (construction) demonstrate this model’s power. The approach creates significant barriers to entry—generalist competitors struggle to match the depth of industry knowledge embedded in the product.

4. API-First Architecture

Modern SaaS is built API-first, with user interfaces becoming one of many possible consumption methods. This architecture enables seamless integration into customer workflows, supports headless implementations, and facilitates ecosystem partnerships. The API-first approach recognizes that SaaS value increasingly derives from data flow between systems rather than isolated application usage.

Developer experience has become a primary competitive differentiator. SaaS companies now invest heavily in documentation, SDKs, developer relations, and partner programs. The most successful platforms function as infrastructure—reliable, scalable, and invisible—powering customer applications without dictating their architecture. Companies like Stripe and Twilio built empires by providing developer-friendly APIs that solve complex problems with simple integration.

The API economy continues to expand, with companies monetizing access to their data and capabilities. API marketplaces aggregate offerings from multiple providers, making it easier for developers to discover and integrate services. As AI agents become more capable, API-first architecture becomes even more critical—agents need programmatic interfaces to interact with software systems.

5. Product-Led Growth 2.0

Product-led growth (PLG) has evolved beyond simple free trials and freemium models into a sophisticated go-to-market strategy. The new PLG combines self-serve onboarding with intelligent sales assistance, community-driven adoption, and viral product mechanics. Companies like Notion, Loom, and Superhuman exemplify this evolved approach, using the product itself as the primary acquisition and expansion engine.

The most successful PLG companies in 2026 have learned to layer sales touchpoints at strategic moments—when users hit usage limits, invite team members, or demonstrate expansion potential. This hybrid model captures the scalability of self-serve with the revenue acceleration of sales-led approaches. Data science identifies which users are ready for sales engagement, optimizing resource allocation.

Community has become a critical component of PLG strategy. User communities drive adoption through tutorials, templates, and best practice sharing. They reduce support burden by enabling peer-to-peer assistance. And they create network effects—as more users join the community, its value increases for all members. SaaS companies increasingly invest in community management as a core function.

6. Micro-SaaS and Solopreneur Explosion

The barrier to building SaaS has collapsed thanks to AI coding tools, no-code platforms, and cloud infrastructure that enable individuals to launch sophisticated software businesses with minimal capital. The micro-SaaS segment—products generating $50K to $3M+ annually with 1-5 person teams—is growing at 30% annually, from $15.70 billion in 2024 to a projected $59.60 billion by 2030.

These niche products solve specific problems for targeted audiences, reaching profitability within 1-2 years rather than the 5-7 year timelines typical of VC-backed SaaS. The micro-SaaS movement represents a fundamental democratization of software entrepreneurship, enabling domain experts to monetize specialized knowledge without traditional startup infrastructure or venture capital requirements.

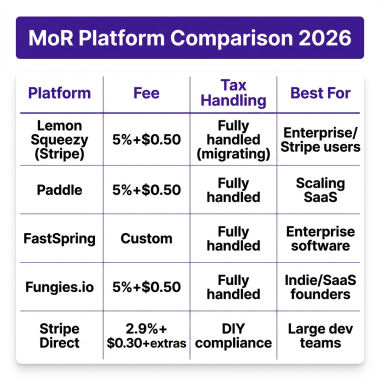

Platforms like Gumroad, LemonSqueezy, and Fungies.io have emerged to serve this market, providing payment processing, tax compliance, and distribution infrastructure. These merchant-of-record platforms handle the complexity of global sales, allowing solopreneurs to focus on product development. The result is an explosion of creativity as individuals build tools for problems they personally experience.

7. Security-First and Zero Trust Architecture

As SaaS applications handle increasingly sensitive data, security has moved from checkbox compliance to competitive differentiation. Zero trust architecture—never trust, always verify—has become the default security model for enterprise SaaS. Buyers demand SOC 2 compliance, encryption at rest and in transit, and granular access controls as table stakes for any serious consideration.

SaaS vendors are responding with advanced security features: AI-powered threat detection, automated compliance monitoring, customer-controlled encryption keys, and detailed audit logs. In regulated industries like healthcare and finance, security capabilities often determine vendor selection more than feature breadth or pricing. A data breach can destroy customer trust and trigger regulatory penalties that threaten business viability.

Security is also becoming a product category within SaaS. Companies like Vanta and Drata automate compliance processes, making it easier for SaaS vendors to achieve and maintain certifications. This infrastructure layer enables smaller SaaS companies to meet enterprise security requirements that previously required dedicated security teams.

Key Players and Competitive Landscape

The SaaS competitive landscape spans from trillion-dollar giants to single-founder micro-SaaS operations. Understanding this ecosystem requires examining both the established leaders defending their positions and the emerging challengers reshaping the industry through innovation and specialization.

The Dominant Platforms:

Microsoft continues to lead the overall SaaS market, with its cloud offerings generating substantial growth across multiple categories. In fiscal year 2024, Microsoft’s SaaS revenue increased by $8.5 billion, or 12% year-over-year. The company’s comprehensive suite spanning productivity (Microsoft 365), infrastructure (Azure), and business applications (Dynamics) creates ecosystem lock-in that competitors struggle to penetrate. Microsoft’s ability to bundle offerings and leverage existing enterprise relationships makes it a formidable competitor in any category it enters.

Salesforce remains the CRM category leader, having essentially defined the SaaS model for enterprise software. The company’s expansion beyond CRM into marketing automation (Marketing Cloud), analytics (Tableau), and platform services (Force.com) has created a comprehensive customer success ecosystem. The Salesforce AppExchange pioneered the SaaS marketplace concept, demonstrating how platforms can extend their value through third-party developers.

Oracle and SAP have successfully transitioned their legacy on-premise businesses to cloud delivery, though they continue to face competition from native SaaS alternatives unburdened by legacy architecture. Both companies have invested heavily in AI capabilities to differentiate their offerings and justify premium pricing.

Google Workspace maintains strong position in productivity and collaboration, while Amazon Web Services dominates the infrastructure layer that powers much of the SaaS ecosystem. These hyperscalers benefit from massive R&D budgets, global infrastructure, and the ability to cross-sell across their extensive product portfolios.

Emerging Category Leaders:

Atlassian has built a dominant position in team collaboration and project management, serving software teams and expanding into broader enterprise use cases. The company’s products—Jira, Confluence, and Trello—have become standard tools for agile development and team coordination. Atlassian’s low-touch sales model and transparent pricing disrupted traditional enterprise software sales approaches.

Chargebee has emerged as a preferred subscription billing and revenue management platform, enabling SaaS companies to automate billing complexity including proration, tax calculation, and revenue recognition. As pricing models become more complex with usage-based components, Chargebee’s value proposition strengthens.

Qualtrics pioneered the experience management category, capturing customer, employee, and product feedback at scale. The company’s IPO and subsequent trading demonstrated the market appetite for specialized SaaS solutions that address specific enterprise needs with comprehensive capabilities.

Zoom, Slack, and Notion represent the new breed of workplace collaboration tools that achieved massive adoption through superior user experience and viral growth mechanics. These products spread organically within organizations before official procurement, demonstrating the power of bottom-up adoption in the SaaS era.

AI-Native Disruptors:

New entrants built specifically for the AI era are challenging incumbents across categories. These companies leverage foundation models to deliver capabilities impossible with traditional software architecture. The most successful—like Anthropic, OpenAI’s enterprise offerings, and specialized AI agents—achieve explosive growth by solving problems that simply couldn’t be addressed before large language models became commercially viable.

The threat to incumbents is real: AI-native companies can enter markets with fundamentally different economics, automating work that previously required human labor. Traditional SaaS companies must evolve their architectures and value propositions to compete, often requiring significant platform reinvestment.

Vertical Specialists:

Industry-specific SaaS companies are capturing market share from generalist competitors by delivering superior value through deep domain expertise. Whether it’s Toast for restaurants, Shopify for e-commerce, Procore for construction, or Veeva for life sciences, these vertical solutions understand their industries’ unique workflows, compliance requirements, and business models.

The vertical SaaS playbook—start narrow, dominate a niche, then expand—has proven repeatable across dozens of industries. Success creates significant barriers to entry because generalist competitors struggle to match the depth of industry knowledge embedded in the product and the trust relationships built with industry participants.

Challenges and Pain Points

Despite robust growth projections, the SaaS industry faces significant challenges that will shape competitive dynamics through the remainder of the decade. Companies that navigate these challenges effectively will capture disproportionate value; those that fail risk obsolescence.

1. Customer Acquisition Cost Inflation

The median B2B SaaS company now spends $2.00 to generate $1.00 in new ARR—a metric that would have been considered disastrous just years ago. Customer acquisition costs have surged to $1,200 per customer on average, representing a 60% increase over five years. CAC payback periods have extended to 15-18 months, straining cash flow and requiring larger capital reserves to fund growth.

This inflation stems from multiple factors: increased competition crowding every category, privacy regulations limiting targeting capabilities, ad platform algorithm changes reducing efficiency, and buyer sophistication making traditional outbound less effective. The result is that growth has become more expensive, forcing companies to choose between slower growth rates or accepting greater burn rates and dilution.

The response requires fundamental strategy shifts. Companies must achieve greater sales efficiency through better targeting, improved conversion, and product-led growth mechanics. They must maximize customer lifetime value through retention and expansion initiatives. And they must explore alternative channels—partnerships, communities, and content—that can generate demand at lower cost than paid acquisition.

2. SaaS Sprawl and Tool Fatigue

Enterprises now manage an average of 291 SaaS applications, many overlapping in functionality, underutilized relative to their potential, and poorly integrated with each other. This sprawl creates security vulnerabilities through unmanaged access, compliance risks from shadow IT, and budget bloat from redundant subscriptions. IT departments are responding with SaaS management platforms and aggressive consolidation initiatives.

For vendors, this means increased churn risk as customers rationalize their tool stacks during renewal cycles. Point solutions that solve narrow problems face particular pressure as enterprises prefer comprehensive platforms that reduce vendor management overhead. The winners will be either category-defining platforms that serve as systems of record or deeply integrated specialists that resist consolidation through unique capabilities and tight workflow integration.

The sprawl challenge also creates opportunities. SaaS management platforms like Zylo, Productiv, and Torii help enterprises discover, manage, and optimize their application portfolios. Integration platforms like Zapier, Workato, and MuleSoft connect disparate systems, enabling workflows that span multiple SaaS applications. These infrastructure plays benefit from the very sprawl they help manage.

3. Pricing Pressure and Inflation

SaaS pricing inflation is running at nearly 5× general market inflation rates, with vendors raising prices consistently to maintain growth and offset acquisition cost increases. Enterprise buyers are pushing back against relentless price increases, demanding greater value demonstration and exploring alternatives including open-source, self-hosted solutions, and competitive switching.

In some sectors, aggressive discounting has reset pricing expectations across entire categories. Buyers have become more sophisticated in negotiations, benchmarking prices against peers and demanding transparency in pricing models. The shift to usage-based pricing, while beneficial long-term, creates revenue unpredictability that complicates financial planning and may affect valuation multiples.

Vendors must navigate this carefully. Price increases must be justified by demonstrated value and feature expansion. Usage-based models require sophisticated tooling to help customers forecast and control spending. And vendors must be prepared to defend their pricing against competitive alternatives that may offer lower cost with acceptable functionality.

4. AI Disruption Risk

Artificial intelligence represents both the greatest opportunity and the greatest existential threat facing SaaS companies. According to Gartner, 35% of point-product SaaS tools will be absorbed into larger agent ecosystems or replaced entirely by AI agents by 2030. Companies whose core value proposition is simple workflow automation, data presentation, or content generation face particular risk as AI makes these capabilities trivial to implement.

The challenge is determining where AI enhances value versus where it eliminates the need for a standalone product. A tool that simply moves data between systems may be replaced by an AI agent that performs the same function without dedicated software. Conversely, tools that leverage AI to deliver new capabilities—predictive analytics, natural language interfaces, autonomous decision-making—can capture significant value.

Companies must evolve their offerings to leverage AI capabilities while maintaining differentiation that prevents commoditization. This requires significant investment in AI talent, infrastructure, and product development. It also requires strategic clarity about what value the company provides that AI cannot easily replicate—domain expertise, data network effects, regulatory compliance, or human judgment.

Opportunities and Growth Strategies

Within these challenges lie substantial opportunities for companies that execute strategically. The following growth strategies have demonstrated effectiveness across market conditions and competitive environments:

1. Expansion Revenue Focus

Top-performing SaaS companies generate 40%+ of new ARR from existing customers through upsells, cross-sells, and usage expansion. This expansion revenue is significantly more profitable than new customer acquisition, with minimal incremental sales and marketing cost. The economics are compelling: a dollar of expansion revenue might cost $0.20 to acquire versus $2.00 for new customer revenue.

Companies should design products with natural expansion triggers—usage limits, feature tiers, seat-based pricing—that encourage customers to grow their spend as they derive more value. They should invest in customer success to drive adoption and identify expansion opportunities. And they should build analytics that help customers understand and maximize their value from the platform.

Net Revenue Retention (NRR) above 100% has become the hallmark of SaaS quality. Companies achieving 120%+ NRR can sustain growth even with modest new customer acquisition, creating resilient businesses less dependent on expensive marketing channels. Public market investors heavily weight NRR in valuation models, making it a critical metric for any SaaS company with IPO aspirations.

2. International Expansion

While North America represents the largest SaaS market, the highest growth rates are in Asia-Pacific, Latin America, and emerging markets. Companies that localize effectively—beyond simple translation to cultural adaptation, local compliance, and regional support—can capture first-mover advantages in underpenetrated markets.

International expansion also provides diversification benefits, reducing dependence on any single economic region or currency. The most successful global SaaS companies build regional teams that understand local business practices, can support customers in native languages and time zones, and navigate regulatory requirements specific to each jurisdiction.

Key considerations for international expansion include data residency requirements (particularly in Europe and China), payment methods preferred in each region, and competitive dynamics that may differ from home markets. Companies should prioritize markets based on market size, competitive intensity, and cultural fit with their product.

3. Ecosystem and Platform Strategy

Building platforms that enable third-party developers and integrations creates powerful network effects that defend against competition. The most valuable SaaS companies function as ecosystems rather than isolated applications—Salesforce’s AppExchange, Shopify’s app marketplace, and Slack’s integration directory demonstrate this model’s power.

Platform strategies require investment in developer experience, documentation, and partner support. The payoff is a defensive moat—customers become embedded in an ecosystem that becomes increasingly valuable as more integrations and applications are added. Switching costs rise as customers build workflows that span multiple integrated tools.

The platform approach also enables revenue diversification. Marketplaces can generate transaction fees from third-party sales. Partner programs can create referral revenue streams. And platform data can inform product development and identify new market opportunities.

4. Vertical Market Dominance

For companies not positioned to build horizontal platforms, vertical market dominance offers an attractive alternative. By solving industry-specific problems more completely than generalist competitors, vertical SaaS companies can achieve high market share in defined segments with superior unit economics.

The vertical playbook involves deep domain expertise, industry partnerships, and features that address sector-specific compliance and workflow requirements. Success creates significant barriers to entry—generalist competitors struggle to match the depth of industry knowledge embedded in the product.

Vertical SaaS companies often benefit from industry-specific sales channels and trade show presence. They can develop thought leadership through industry publications and associations. And they can build data advantages through industry-specific benchmarks and analytics that generalist competitors cannot replicate.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes possible in the current SaaS environment. These case studies demonstrate different paths to success across funding models, growth strategies, and market approaches.

Case Study 1: NeuroFlow AI – $0 to $100M ARR in 18 Months

NeuroFlow AI represents the explosive potential of AI-native SaaS when product-market fit aligns with viral distribution mechanics. Starting with $500K in seed funding, the company achieved $100M ARR in just 18 months by making AI agents the core product rather than a feature add-on. Their growth strategy centered on a viral freemium model—any user could create a basic agent for free, but sharing it with 3+ team members unlocked collaborative features.

This product-led growth engine drove organic adoption while the company built enterprise sales capabilities to capture larger contracts. The lesson for other SaaS companies is clear: AI-native products can achieve growth velocities impossible for traditional SaaS when the product itself creates viral distribution mechanics. The key was making the AI capability central to the value proposition, not peripheral.

Case Study 2: EcoTrack Analytics – Bootstrapped to $20M ARR

EcoTrack Analytics demonstrates that venture capital is not required for SaaS success. The bootstrapped company reached $20M ARR without external funding by weaponizing community-driven customer acquisition in the sustainability niche. Rather than competing for expensive paid advertising, EcoTrack built a content and community engine that established thought leadership and generated organic demand.

The company’s success highlights the micro-SaaS opportunity—solving specific problems for passionate audiences can generate substantial revenue with minimal capital requirements. Profitability from month one provided strategic flexibility that VC-backed competitors lacked. The founders maintained full control and avoided the growth-at-all-costs pressure that leads many funded companies astray.

Case Study 3: TripleDart Agency Client Results

TripleDart’s work with multiple SaaS clients demonstrates effective growth strategies in practice. With Signeasy, they achieved 800 monthly sessions with 60-68% consistent growth through LLM visibility optimization. For Airbase, strategic PPC campaigns boosted pipeline by 6×. EmailOctopus improved purchases by 40% and signups by 15% through targeted optimization.

These results illustrate that disciplined execution across SEO, paid acquisition, and conversion optimization can drive substantial growth even in competitive markets. The key is systematic testing, measurement, and optimization rather than reliance on any single channel. Diversified acquisition strategies provide resilience against algorithm changes and competitive pressure.

Future Outlook and Predictions

The SaaS industry’s trajectory through 2030 and beyond will be shaped by several converging forces. Understanding these trends enables companies to position themselves for the opportunities ahead.

Market Size Projections

By 2030, the SaaS market will reach approximately $819 billion according to Grand View Research, with Precedence Research projecting $1.37 trillion by 2035. This growth will be driven by continued enterprise digitization, SMB adoption, and the emergence of new software categories enabled by AI and other emerging technologies.

The B2B SaaS segment will likely grow faster than the overall market, with Mordor Intelligence projecting a 26.24% CAGR through 2031. As more business functions digitize—from legal and compliance to manufacturing and logistics—vertical SaaS opportunities will multiply. Every industry will have its specialized software stack.

Agentic AI Disruption

Gartner predicts that by 2035, agentic AI could drive approximately 30% of enterprise application software revenue, surpassing $450 billion. This represents a fundamental shift from software as a tool to software as an autonomous agent capable of executing complex workflows with minimal human oversight.

The transition will not be smooth—Gartner also predicts that over 40% of agentic AI projects may be cancelled by 2027 due to escalating costs, unclear business value, or inadequate risk controls. Companies must navigate this transition carefully, investing in AI capabilities while maintaining focus on measurable customer outcomes.

Consolidation and Category Definition

The SaaS market will see continued consolidation as larger platforms acquire point solutions to expand their capabilities. Companies that fail to achieve category leadership or deep vertical integration face acquisition or obsolescence. The winners will be either comprehensive platforms that serve as operating systems for business functions or deeply specialized solutions that resist consolidation through unique domain expertise.

Global Market Maturation

While North America currently dominates SaaS revenue, international markets will capture increasing share. Europe’s regulatory environment (GDPR, AI Act) will drive innovation in privacy-preserving and compliant SaaS. Asia-Pacific’s rapid digitization will create massive new markets. The most successful global SaaS companies will build regional capabilities rather than simply exporting US-centric products.

Key Takeaways

- The global SaaS market reached $465.03 billion in 2026 and is projected to grow to $1.37 trillion by 2035 at a 12.85% CAGR

- 99% of organizations now use SaaS applications, with enterprises managing an average of 291-371 apps each

- AI-native SaaS is the dominant trend, with 75% of companies embedding AI and AI-native startups raising at 40% higher valuations

- Usage-based pricing has overtaken flat subscriptions, with 80% of companies now offering consumption-based models

- Customer acquisition costs have increased 60% over five years, making retention and expansion revenue critical for sustainable growth

- Vertical SaaS and micro-SaaS represent the highest-growth segments, with vertical solutions raising larger rounds and micro-SaaS growing at 30% annually

- The future belongs to companies that can build platform ecosystems, achieve vertical dominance, or leverage AI to deliver previously impossible capabilities

Sources and Citations

- Precedence Research – Software as a Service (SaaS) Market Size and Forecast 2026-2035: https://www.precedenceresearch.com/software-as-a-service-market

- Mordor Intelligence – B2B SaaS Market Size and Share Analysis 2026-2031: https://www.mordorintelligence.com/industry-reports/b2b-saas-market

- Grand View Research – Software as a Service Market Size Report 2030: https://www.grandviewresearch.com/industry-analysis/saas-market-report

- Statista – Software as a Service Worldwide Market Forecast: https://www.statista.com/outlook/tmo/public-cloud/software-as-a-service/worldwide

- Quantumrun – SaaS Industry Growth Statistics 2026: https://www.quantumrun.com/consulting/saas-industry-growth-statistics/

- DemandSage – SaaS Statistics 2026: https://www.demandsage.com/saas-statistics/

- Gartner – Agentic AI Predictions and Strategic Forecasts: https://www.gartner.com/en/newsroom/press-releases/

- OpenView SaaS Benchmarks 2026: https://www.openview.com/saas-benchmarks

- Eagle Rock CFO – SaaS Finance Metrics Benchmarks: https://www.eaglerockcfo.com/blog/research/saas-finance-metrics-benchmarks

- Prospeo – SaaS Industry Benchmarks 2026: https://prospeo.io/s/saas-industry-benchmarks

- Dodo Payments – SaaS Industry Report 2025-2026: https://dodopayments.com/blogs/saas-report-trends-2025-2026

- Zylo – 2026 SaaS Management Index: https://zylo.com/blog/saas-predictions-for-2026

- Innovecs – Top 7 SaaS Trends Shaping Business in 2026: https://innovecs.com/blog/the-top-7-saas-trends/

- SAAS FOURM – Case Studies: SaaS Success Stories from 2026: https://www.saasfourm.com/case-studies-saas-success-stories-from-lessons-from-explosive-growth/

- VC Mapping – SaaS Investors and Venture Capital Firms 2026: https://vc-mapping.gilion.com/venture-capital-firms/saas-investors

About the Author: This comprehensive market analysis was prepared by the research team at Fungies.io, a leading merchant of record platform serving SaaS companies and digital product sellers globally. Fungies.io enables software businesses to accept payments worldwide without the complexity of tax compliance, payment processing, or checkout development.

Disclaimer: Market data and projections cited in this report are based on publicly available research from industry analysts. Actual market performance may vary. This report is for informational purposes only and does not constitute investment advice.

Related Reading: For more insights on SaaS growth strategies, payment optimization, and global expansion, explore our additional research reports on the Fungies.io blog. Our analysis covers merchant of record solutions, payment gateway comparisons, and tax compliance strategies for digital businesses operating across borders.