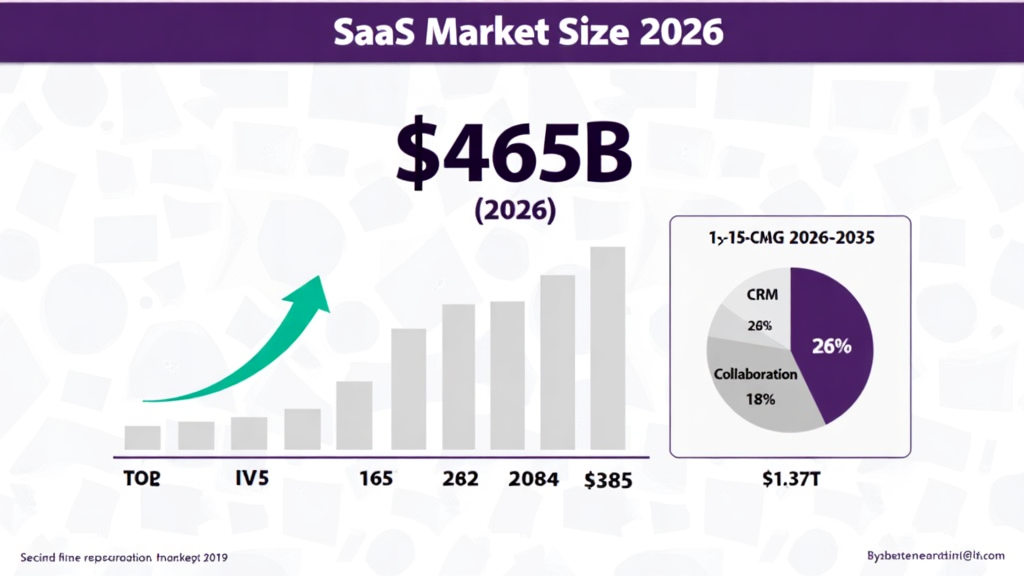

The global Software as a Service (SaaS) market has reached an inflection point in 2026. With a market valuation of $465.03 billion and projections pointing toward $1.37 trillion by 2035, SaaS has evolved from a convenient alternative to on-premise software into the dominant model for enterprise and consumer applications alike. The industry is growing at a compound annual growth rate (CAGR) of 12.85%, a figure that reflects not just market expansion but a fundamental restructuring of how businesses consume technology.

This is not just another tech trend. SaaS now commands 72% of all enterprise software spending according to IDC, having displaced traditional perpetual license models across virtually every industry vertical. The average company now uses 106 SaaS applications—down from a peak of 130 in 2022, but representing a far more strategic and consolidated approach to software procurement. What we are witnessing is not saturation; it is maturation.

The SaaS industry has fundamentally transformed how businesses operate. From customer relationship management to human resources, from financial planning to project management, nearly every business function now has specialized SaaS solutions delivering capabilities that were once only available to the largest enterprises with massive IT budgets. This democratization of enterprise-grade software has leveled the playing field, allowing startups and small businesses to compete with established players using the same tools and technologies.

In this comprehensive analysis, we will explore the current state of the SaaS market in 2026, examining the key statistics that define the industry, the trends shaping its future, the major players competing for market share, and the challenges and opportunities facing both vendors and customers. Whether you are a SaaS founder seeking to understand your competitive landscape, an investor evaluating opportunities, or a business leader making software procurement decisions, this report provides the data and insights you need to navigate the evolving SaaS ecosystem.

Market Overview: The $465 Billion Ecosystem

The SaaS market’s trajectory from 2020 to 2035 tells a story of explosive growth tempered by increasing sophistication. In 2020, the global SaaS market was valued at approximately $157 billion. By 2025, that figure had more than doubled to $408.21 billion. The 2026 valuation of $465.03 billion represents a 14% year-over-year increase, and industry analysts project this growth will accelerate as artificial intelligence integration becomes standard across platforms.

The growth story of SaaS is one of the most remarkable in technology history. What began as a novel delivery model for simple applications like email and calendaring has evolved into the primary way businesses consume software of all types. The COVID-19 pandemic accelerated this transition dramatically, as remote work requirements forced companies to rapidly adopt cloud-based collaboration tools. While the emergency phase of that transition has passed, the structural changes it created have become permanent features of the business landscape.

The United States remains the dominant geographic market, accounting for $141.06 billion of global SaaS revenue in 2026. North American enterprises were early adopters of cloud computing, and this head start has translated into sustained market leadership. The region benefits from a mature venture capital ecosystem that has funded thousands of SaaS startups, a large base of enterprise customers with sophisticated software needs, and a regulatory environment that has generally been supportive of cloud computing adoption.

However, the Asia-Pacific region is emerging as the fastest-growing market, with China, India, and Southeast Asian nations driving adoption among small and medium enterprises seeking affordable, scalable software solutions. The Asia-Pacific SaaS market is growing at nearly 18% annually, outpacing both North America and Europe. This growth is driven by rapid digital transformation in developing economies, increasing internet penetration, and a growing base of technology-enabled small businesses.

Europe represents the second-largest regional market, with particular strength in fintech SaaS, regulatory compliance software, and privacy-focused solutions driven by GDPR requirements. The European SaaS market benefits from a highly educated workforce and strong digital infrastructure, though regulatory complexity remains a challenge for vendors seeking to operate across multiple jurisdictions. The European Union’s emphasis on data sovereignty has created opportunities for regional SaaS providers that can guarantee data remains within EU borders.

The market segmentation reveals interesting dynamics that reflect how businesses actually use software. Customer Relationship Management (CRM) software commands the largest share at approximately 28% of total SaaS revenue, led by Salesforce’s continued dominance. The CRM category has expanded beyond simple contact management to encompass sales automation, marketing automation, customer service, and analytics—creating a massive addressable market that continues to grow as businesses prioritize customer experience.

Enterprise Resource Planning (ERP) systems account for 22% of the SaaS market, with cloud-native solutions like Workday and legacy vendors’ cloud migrations competing for market share. The ERP category has been slower to move to the cloud than other categories due to the complexity of implementation and the critical nature of the data involved. However, the shift is now well underway, with most large enterprises planning to move their core ERP systems to cloud platforms within the next five years.

Collaboration and communication tools represent 18% of the market—a segment that exploded during the pandemic and has maintained elevated demand as hybrid work becomes permanent. The category has seen intense competition, with Microsoft Teams, Slack, Zoom, and Google Workspace battling for market share. The integration of these tools with broader productivity suites has become a key competitive battleground.

Human Capital Management (HCM) SaaS, Business Intelligence & Analytics, and industry-specific vertical solutions comprise the remaining market share. What is notable is the rapid growth of vertical SaaS—industry-specific solutions that address unique workflows and compliance requirements. The vertical SaaS market is projected to reach $157.4 billion by 2027, growing at a 23.9% CAGR that significantly outpaces horizontal SaaS categories. This growth reflects the limitations of one-size-fits-all software and the value of solutions built specifically for particular industries.

Key Statistics and Data: The Numbers Behind the Growth

Understanding the SaaS market requires diving deep into the metrics that define success and failure in this unique business model. Unlike traditional software companies that recognized revenue upfront, SaaS businesses operate on subscription economics where customer acquisition cost, retention rates, and lifetime value determine viability. These metrics tell a story of an industry that has matured rapidly, with increasing competition driving up acquisition costs and putting pressure on retention rates.

Company Count and Market Density: As of 2026, there are over 33,200 SaaS companies globally—a 32% increase from 25,000 companies in 2021. The United States hosts approximately 12,400 of these companies, representing the densest concentration of SaaS innovation worldwide. This proliferation of vendors has created both opportunities and challenges: customers benefit from specialized solutions for virtually every use case, but software sprawl and integration complexity have become significant pain points. The sheer number of SaaS companies has made differentiation increasingly difficult, with vendors struggling to stand out in crowded categories.

Application Proliferation: Companies now use an average of 106 SaaS applications, though this represents an 18% decline from the 2022 peak of 130 applications. This reduction reflects a maturation in how organizations approach software procurement—moving from unchecked proliferation to strategic consolidation. IT departments have become more involved in SaaS governance, with studies showing that over half of SaaS applications in use are now managed by IT teams rather than individual business units. This shift toward governance reflects the realization that unmanaged SaaS sprawl creates security risks, compliance issues, and unnecessary costs.

Growth Rate Benchmarks: According to SaaS Capital’s 2025 survey of private B2B SaaS companies, the median revenue growth rate settled at 26% in 2024, down from 30% in 2023. This deceleration reflects market maturation and increased competition, but top-quartile companies continue to achieve 50%+ growth rates. For companies with ARR between $1M and $30M, the top 25% achieved 62.1% growth—still impressive, though down from 78.9% in 2021. The decline in growth rates reflects both the law of large numbers and increasing competition in most categories.

Customer Acquisition Economics: The median B2B SaaS company now spends $2.00 in sales and marketing to acquire every $1.00 of new ARR—a figure that has risen significantly as competition intensifies. Average customer acquisition costs have reached $1,200 per customer, marking a 60% increase over five years. These rising costs have forced SaaS companies to focus intensely on efficient growth metrics. The increase in CAC reflects multiple factors: more competition for buyer attention, higher customer expectations for sales and onboarding experiences, and the end of the zero-interest-rate era that previously subsidized aggressive growth investments.

Retention and Expansion: Net Revenue Retention (NRR) has compressed to 101% across all private B2B SaaS companies, though top performers maintain 120-130%. The Rule of 40—combining growth rate and profit margin—has become the gold standard for SaaS valuation, with companies targeting a combined score above 40%. Monthly churn rates below 1% (annualized below 12%) are considered excellent, while rates above 3% monthly signal serious product-market fit issues. The compression in NRR reflects both increased competition and the maturity of many SaaS categories.

Unit Economics: Healthy SaaS companies maintain LTV:CAC ratios above 3:1, with 5:1+ indicating exceptional efficiency. CAC payback periods under 12 months are typical targets, though enterprise-focused companies with higher ACVs may extend to 18 months. Gross margins of 70-85% remain standard for SaaS businesses, reflecting the inherent scalability of software delivery. These unit economics have become increasingly important to investors, who have shifted from “growth at all costs” to demanding clear paths to profitability.

AI-Native SaaS Performance: Perhaps the most striking data point from 2026 is the performance divergence between AI-native SaaS companies and traditional SaaS. AI-native SaaS companies are raising at 40% higher valuations than traditional SaaS, with median Series B valuations hitting $175 million in Q3 2025—a 38% year-over-year increase. Some AI-native companies have achieved $3M ARR within their first year and scaled to $100M by year four, far outpacing traditional SaaS growth timelines. This premium reflects investor belief that AI-native architecture enables fundamentally better products and business models.

Major Trends Shaping SaaS in 2026

The SaaS landscape of 2026 is being reshaped by seven major trends that are fundamentally altering how software is built, sold, and consumed. These trends represent both opportunities for growth and challenges that vendors must navigate to remain competitive. Understanding these trends is essential for anyone participating in the SaaS ecosystem, whether as a vendor, customer, or investor.

1. AI-Native Architecture Becomes Default

AI is no longer a feature bolted onto existing products—it is becoming the foundational architecture for new SaaS applications. According to a Salesforce CIO survey, AI adoption in enterprises has jumped over 280%, with “agentic” AI (multi-agent systems that act autonomously rather than just responding to prompts) identified as a core 2026 priority. The Global AI-Created SaaS Market is expected to reach $142.02 billion in 2026 and grow to $1.05 trillion by 2033 at a 39.6% CAGR.

This shift represents more than technological advancement; it is a business model transformation. AI-native SaaS companies can deliver outcomes rather than just tools, commanding premium pricing and achieving faster time-to-value. Machine learning now contributes 42.3% of AI-created SaaS market value, with natural language processing and computer vision following as key technology segments. The implications are profound: AI-native companies are not just building better versions of existing software; they are creating entirely new categories of solutions that were previously impossible.

2. Vertical SaaS Acceleration

Horizontal SaaS platforms that serve multiple industries are facing increasing competition from vertical solutions purpose-built for specific sectors. The vertical SaaS market is growing at 23.9% CAGR—roughly double the pace of many horizontal segments. Industries like construction, healthcare, legal services, and agriculture are seeing specialized SaaS solutions that address unique workflows, compliance requirements, and integration needs that generic platforms cannot match.

Vertical AI SaaS companies for healthcare, legal, and financial services have raised the largest early-stage rounds, with median Series A sizes of $22 million versus $15 million for traditional horizontal SaaS. This premium reflects investor confidence that vertical specialization creates stronger moats and higher customer lifetime values. The success of vertical SaaS demonstrates that deep industry expertise can be more valuable than broad horizontal capabilities.

3. Usage-Based and Consumption Pricing

The traditional per-seat subscription model is being supplemented—and in some cases replaced—by usage-based pricing that aligns vendor revenue with customer value realization. This shift is particularly pronounced in infrastructure SaaS, AI services, and API-first products where consumption varies significantly across customers. Usage-based pricing better reflects the value customers receive, but it also introduces complexity in forecasting and budgeting.

However, this trend brings challenges. A Zylo survey found that 78% of IT leaders experienced unexpected costs from usage-based or AI-driven pricing models in 2025. Only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically, leaving most companies vulnerable to cost volatility. The most sophisticated SaaS vendors are responding with hybrid models that combine predictable base fees with usage-based overages, balancing customer desire for cost control with vendor revenue stability.

4. Product-Led Growth (PLG) Maturation

Product-led growth has evolved from a startup strategy to the dominant go-to-market motion for SaaS companies of all sizes. In 2026, 81% of B2B buyers make vendor decisions before engaging sales teams, making the product experience the primary driver of acquisition and conversion. Mixpanel’s 2026 State of Digital Analytics report, analyzing behavior across 12,000+ companies, named product as the new primary growth channel.

Leading B2B companies now anchor their growth strategies on in-product signals like feature adoption, time-to-value, and activation rates. The most successful PLG implementations combine self-service adoption with intelligent sales assistance triggered by product usage patterns—what industry analysts call “product-led sales.” This hybrid approach allows companies to serve a broad base of self-service customers while providing high-touch support to enterprise prospects.

5. Platform Consolidation and Suite Expansion

After years of best-of-breed proliferation, enterprises are consolidating around integrated platforms that reduce complexity and improve data flow across applications. Microsoft, Salesforce, and other platform giants are leveraging their ecosystems to capture expanding share of wallet, while point solution vendors face increasing pressure to demonstrate clear differentiation. This consolidation reflects buyer fatigue with managing dozens of separate vendors and integrations.

This consolidation trend has driven significant M&A activity, with larger SaaS companies acquiring specialized tools to round out their offerings. The March 2026 acquisition of BetterCloud by CoreStack exemplifies this trend, combining SaaS management expertise with AI-native cloud governance to create what the companies term an “Agentic Governance Operating System.”

6. AI Governance and Trust Infrastructure

As AI becomes embedded across SaaS applications, governance and trust have emerged as critical concerns. Enterprises need visibility into how AI models make decisions, assurance that sensitive data remains protected, and mechanisms to ensure compliance with evolving regulations. SaaS vendors are responding with transparency tools, audit trails, and AI-specific security features. Trust has become a key differentiator, particularly for enterprise buyers.

The concept of “shadow AI”—unauthorized AI tool usage by employees—has become a significant concern, with IT leaders struggling to maintain governance as AI capabilities proliferate across applications. Unified SaaS management platforms that provide visibility and control across cloud, SaaS, and AI systems are emerging as essential infrastructure for enterprise IT.

7. Embedded Finance and Fintech Integration

SaaS platforms are increasingly embedding financial services directly into their offerings, from payment processing and lending to insurance and payroll. This trend, often called “embedded finance,” creates new revenue streams for SaaS vendors while providing seamless experiences for customers who prefer consolidated platforms over multiple vendor relationships. The integration of financial services into business software represents a massive opportunity for SaaS companies.

Key Players and Competitive Landscape

The SaaS competitive landscape in 2026 is characterized by platform giants with expanding ecosystems, specialized vertical players with deep industry expertise, and AI-native challengers disrupting established categories. Understanding this competitive dynamic is essential for both vendors positioning their offerings and buyers evaluating their technology portfolios.

Microsoft leads the overall SaaS market, leveraging its Office 365 and Azure ecosystems to capture enterprise spending across productivity, collaboration, and infrastructure categories. The company’s aggressive AI integration through Copilot features across its product suite has strengthened its competitive position, with enterprise adoption of AI-powered features driving increased per-user revenue.

Salesforce maintains its position as the dominant CRM platform while expanding into adjacent categories through organic development and acquisition. The company’s Einstein AI platform and industry-specific cloud solutions demonstrate how horizontal platforms can compete with vertical specialists through configurability and ecosystem depth.

Adobe continues to dominate creative and document SaaS, with its Creative Cloud and Document Cloud platforms representing the gold standard for creative professionals. The company’s expansion into marketing automation and customer experience management through the Adobe Experience Cloud demonstrates successful category expansion.

ServiceNow has emerged as a platform giant in IT service management and workflow automation, with the company expanding into HR, customer service, and industry-specific workflows. The company’s platform approach enables customers to build custom applications while benefiting from underlying infrastructure and AI capabilities.

AI-Native Challengers: Beyond the established giants, a new generation of AI-native SaaS companies is achieving remarkable growth. Companies like NeuroFlow AI have demonstrated that AI-native architecture can drive explosive growth—the company reached $100M ARR in just 18 months by making AI agents the core product rather than an add-on feature.

Challenges and Pain Points

Despite the SaaS market’s impressive growth, vendors and customers alike face significant challenges that are shaping industry evolution and competitive dynamics. Understanding these pain points is essential for navigating the market successfully.

1. Skyrocketing Customer Acquisition Costs

The most pressing challenge for SaaS vendors is the relentless increase in customer acquisition costs. With CAC having risen 60% over five years to reach $1,200 per customer on average, and the median SaaS company spending $2 to acquire $1 of new ARR, the economics of growth have become increasingly challenging.

The drivers of CAC inflation are multifaceted: increased competition in every category, platform giants with massive marketing budgets raising customer expectations, and the end of cheap capital that previously subsidized aggressive customer acquisition. SaaS companies are responding by focusing on product-led growth, expansion revenue from existing customers, and partnerships that reduce direct acquisition costs.

2. Retention and Churn Pressure

Customer retention has become the defining challenge for SaaS businesses. At 3% monthly gross churn, a SaaS company loses 30% of cohort ARR each year before any expansion revenue. With median NRR compressing to 101%, many SaaS companies are barely maintaining revenue from existing customers, let alone growing it.

The causes of churn are evolving. While product-market fit issues remain significant, 68% of customer churn now happens because customers feel unappreciated—a signal that customer success and support quality are as important as product functionality. Additionally, 86% of B2B buyers will pay more for better service.

3. Cost Volatility and FinOps Complexity

The shift toward usage-based and AI-driven pricing has introduced cost volatility that many organizations are unprepared to manage. 82% of executives report significant increases in cloud, SaaS, and Gen AI costs, yet only 2% of organizations have FinOps teams that holistically manage these expenses.

For SaaS vendors, the challenge is balancing the revenue potential of usage-based models with customer demand for predictability. The most successful implementations provide transparency tools, cost alerts, and hybrid pricing that combines predictable base fees with usage-based components.

Opportunities and Growth Strategies

Amid the challenges, significant opportunities exist for SaaS companies that execute effectively. The strategies that are driving success in 2026 reflect the market’s maturation and the new realities of customer expectations and competitive dynamics.

1. Expansion Revenue as Primary Growth Engine

The most successful SaaS companies are generating approximately 40% of new ARR from existing customers through expansion—upsells, cross-sells, and usage growth. This focus on expansion addresses both the CAC challenge and the retention challenge.

Expansion revenue strategies include usage-based pricing that grows with customer success, modular product architectures that enable incremental purchases, and customer success programs that identify and act on expansion signals. Companies with NRR above 120% are achieving this primarily through systematic expansion programs.

2. AI-Powered Product Differentiation

AI integration represents the most significant opportunity for product differentiation and value creation. AI-native SaaS companies are achieving 40% higher valuations and faster growth trajectories than traditional SaaS, demonstrating the market’s appetite for intelligent automation and predictive capabilities.

The opportunity extends beyond native AI companies—established SaaS vendors can embed AI to improve existing workflows, automate routine tasks, and provide predictive insights that were previously impossible. The key is making AI a core part of the value proposition rather than a peripheral feature.

3. Vertical Market Specialization

The vertical SaaS opportunity remains substantial, with industry-specific solutions growing at nearly twice the rate of horizontal platforms. Vertical specialists can command premium pricing due to superior fit with industry workflows, achieve higher retention through deeper integration with customer operations, and face less direct competition than horizontal categories.

Success in vertical SaaS requires genuine industry expertise, not just generic software adapted with industry terminology. The best vertical SaaS companies employ industry veterans in product and customer success roles, maintain active customer advisory boards, and invest deeply in integrations with industry-specific systems.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes that define SaaS success in 2026. These case studies demonstrate how companies are navigating the market’s challenges and capitalizing on its opportunities.

Case Study 1: NeuroFlow AI — From $0 to $100M ARR in 18 Months

NeuroFlow AI represents the potential of AI-native SaaS architecture. Starting with $500K in seed funding, the company reached $100M ARR in just 18 months by making AI agents the core product rather than a feature addition. Their product-led growth engine launched with a viral freemium tier: any user could create a basic agent for free, but sharing it with 3+ team members unlocked collaborative features.

The key lessons from NeuroFlow’s success: AI-native architecture enables fundamentally different user experiences that justify premium pricing; product-led growth can achieve enterprise scale when the product delivers immediate, demonstrable value; and viral mechanics built into the product can drive acquisition more efficiently than traditional marketing.

Case Study 2: EcoTrack Analytics — Bootstrapped to $20M ARR

EcoTrack Analytics demonstrates that venture capital is not required for SaaS success. The bootstrapped company reached $20M ARR without external funding by focusing on a specific vertical—sustainability tracking for enterprises—and building a passionate community around environmental responsibility.

Their community-driven customer acquisition strategy leveraged industry events, content marketing, and customer advocacy rather than paid advertising. By deeply understanding their buyers’ motivations (both business and personal), EcoTrack achieved exceptional retention rates and organic expansion through customer referrals.

Case Study 3: DirectIQ — Content Marketing Excellence

DirectIQ’s strategic emphasis on educational content, particularly ‘how-to’ videos, demonstrates the power of customer education as a growth strategy. By investing heavily in helping customers succeed with email marketing—regardless of whether they used DirectIQ—the company built trust and authority that translated into sustained growth.

Their approach reduced support queries while increasing customer lifetime value, as educated customers were more likely to use advanced features and achieve better results. DirectIQ’s success illustrates that in a crowded SaaS market, teaching can be more effective than selling.

Future Outlook and Predictions

The SaaS market’s trajectory through 2035 will be shaped by technological evolution, changing customer expectations, and macroeconomic factors. Based on current trends and expert analysis, several predictions emerge for the industry’s future.

Market Size Projections: The global SaaS market is projected to reach $1.37 trillion by 2035, representing a 12.85% CAGR from 2026. Some analysts are even more bullish, with projections ranging up to $1.52 trillion by 2035 at a 15.4% CAGR. The difference in projections reflects varying assumptions about AI adoption rates and the pace of digital transformation in lagging industries.

AI Integration Becomes Universal: By 2030, AI capabilities will be standard across virtually all SaaS applications, not just premium tiers or specialized tools. The distinction between “AI companies” and traditional SaaS will disappear as AI becomes a fundamental infrastructure component. The AI-created SaaS market specifically is projected to reach $1.05 trillion by 2033.

Platform Consolidation Accelerates: The current fragmentation of enterprise SaaS portfolios will give way to greater consolidation as integration costs and complexity drive customers toward comprehensive platforms. This doesn’t mean point solutions will disappear—specialized tools will continue to exist—but they will increasingly operate as extensions of major platforms rather than standalone applications.

Vertical SaaS Matures: Industry-specific SaaS solutions will capture increasing market share as vertical specialization proves its value. By 2030, vertical SaaS could represent 35-40% of total SaaS revenue, up from approximately 20% today. The winners will be those who achieve genuine industry depth rather than superficial specialization.

Pricing Model Evolution: Usage-based and outcome-based pricing will become dominant models, replacing per-seat subscriptions for many categories. This shift will require vendors to develop sophisticated metering, billing, and customer communication capabilities. Companies that master value-based pricing will achieve higher margins and stronger customer relationships.

Regulatory Complexity Increases: As SaaS becomes critical infrastructure, regulatory scrutiny will intensify. Data privacy, AI governance, and industry-specific compliance requirements will create both challenges and opportunities. Vendors who invest in compliance infrastructure will gain advantage in regulated industries, while those who ignore regulatory trends will face increasing barriers to market access.

Key Takeaways

- The global SaaS market reached $465.03 billion in 2026 and is projected to grow to $1.37 trillion by 2035 at a 12.85% CAGR

- AI-native SaaS companies are achieving 40% higher valuations and significantly faster growth than traditional SaaS vendors

- Customer acquisition costs have risen 60% over five years, making retention and expansion revenue critical for sustainable growth

- Vertical SaaS is growing at 23.9% CAGR—nearly double the rate of horizontal platforms—as industry specialization proves its value

- Product-led growth has become the dominant go-to-market strategy, with 81% of B2B buyers making decisions before engaging sales

- Usage-based pricing is replacing per-seat models in many categories, though cost volatility remains a challenge for customers

- The average company now uses 106 SaaS applications, representing strategic consolidation from the 2022 peak of 130

- Net Revenue Retention has compressed to 101% industry-wide, making expansion revenue and churn reduction top priorities

- Microsoft, Salesforce, and Adobe lead the overall market, but AI-native challengers are disrupting established categories

- By 2035, AI capabilities will be universal across SaaS, and vertical solutions will capture 35-40% of total market revenue

Sources and Citations

- Precedence Research – Software As A Service (SaaS) Market Size, Share, and Trends 2026 to 2035: https://www.precedenceresearch.com/software-as-a-service-market

- SellersCommerce – 31 Eye-Opening SaaS Statistics In 2026: https://www.sellerscommerce.com/blog/saas-statistics

- Fortune Business Insights – Software as a Service [SaaS] Market Size, Global Report, 2034: https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222

- Zylo – 175+ Unmissable SaaS Statistics for 2026: https://zylo.com/blog/saas-statistics

- Coherent Market Insights – AI Created SaaS Market Trends, Share and Forecast, 2026-2033: https://www.coherentmarketinsights.com/industry-reports/ai-created-saas-market

- Innovecs – Top SaaS Trends in 2026: AI, Security & Growth Models: https://innovecs.com/blog/the-top-7-saas-trends

- Tridens – Top 6 SaaS Industry Trends for 2026: https://tridenstechnology.com/saas-trends

- UltraTalent – SaaS Metrics Every Founder Should Track in 2026: https://ultratalent.com/blog/saas-metrics

- Eagle Rock CFO – SaaS Benchmarks by Stage (2026): ARR, Churn, LTV:CAC: https://www.eaglerockcfo.com/blog/research/saas-finance-metrics-benchmarks

- Averi – 3 SaaS Metrics That Matter More Than MRR in 2026: https://www.averi.ai/blog/15-essential-saas-metrics-every-founder-must-track-in-2026-(with-benchmarks)

- Optifai – B2B SaaS LTV Benchmarks — 939 Companies by Segment: https://optif.ai/learn/questions/b2b-saas-ltv-benchmark

- Synergy Research Group – Microsoft Leads in SaaS Market: https://www.srgresearch.com/articles/microsoft-leads-saas-market-salesforce-adobe-oracle-and-sap-follow

- Helply – Customer Acquisition Challenges in B2B SaaS: https://helply.com/blog/customer-acquisition-challenges

- Amra & Elma – Top 20 SaaS Customer Acquisition Statistics 2026: https://www.amraandelma.com/saas-customer-acquisition-statistics

- Data-Mania – B2B SaaS Benchmarks 2026: CAC, NRR, Churn & Growth Rates: https://www.data-mania.com/blog/b2b-saas-benchmarks-2026-annual-report

- Wizard Creative Labs – PLG Strategy: The Product-Led Growth Playbook: https://www.wizardcreativelabs.com/post/plg-strategy-how-to-build-a-product-led-growth-engine-in-2026

- RevGeni – Best 2026 GTM Strategies for B2B SaaS: https://www.revgeni.ai/best-2026-gtm-strategies-for-b2b-saas

- SEOPrfy – 12 Best SaaS Marketing Strategies That Drive Growth in 2026: https://seoprofy.com/blog/saas-marketing-strategies

- SaaS Fourm – Case Studies: SaaS Success Stories from 2026: https://www.saasfourm.com/case-studies-saas-success-stories-from-lessons-from-explosive-growth

- SaaSRise – SaaS market to hit $1.5T by 2035: https://www.saasrise.com/news/saas-market-projected-to-reach-15-trillion-by-2035-fueled-by-ai-and-cloud