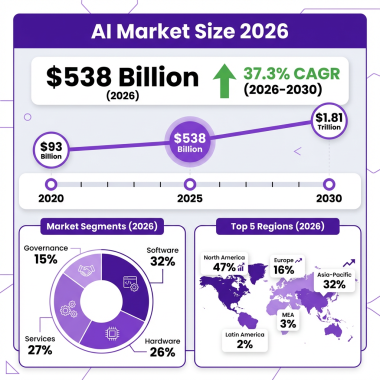

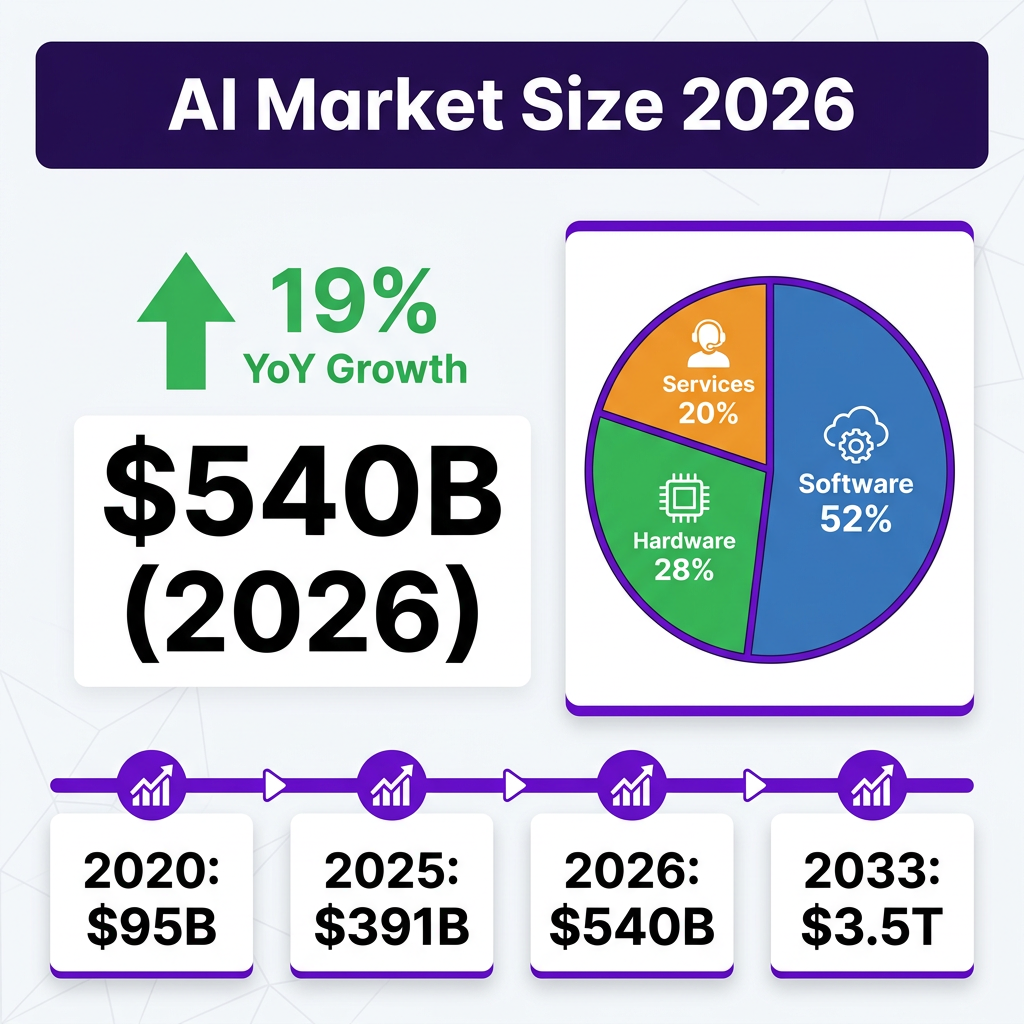

The artificial intelligence market has crossed a historic threshold in 2026. With global revenues hitting $539.5 billion—representing a 19% year-over-year surge from $390.9 billion in 2025—AI has cemented its position as the fastest-growing technology sector in human history. This is not speculative hype or venture capital froth. This is measurable, documented economic transformation happening across every industry, every geography, and every business function.

Consider this: AI’s share of new unicorn births has exploded from just 6% in 2015 to 53% in 2025. Corporate AI adoption has jumped from 55% to 88% in just two years. And generative AI alone—a category that barely existed three years ago—is projected to grow from $37.87 billion in 2024 to $442 billion by 2031. These are not projections from AI enthusiasts. These are figures from IDC, McKinsey, Gartner, and Statista Market Insights.

What is driving this unprecedented growth? The answer is multifaceted: the maturation of large language models, the emergence of agentic AI systems capable of autonomous decision-making, the proliferation of AI coding assistants transforming software development, and the relentless expansion of enterprise use cases. But perhaps most importantly, 2026 marks the year AI transitioned from experimental technology to business infrastructure.

Market Overview: The $540 Billion AI Ecosystem

The global AI market’s trajectory defies conventional growth patterns. According to Grand View Research, the market stood at $390.9 billion in 2025 and is projected to reach $539.5 billion in 2026—a figure that will expand to an astonishing $3.497 trillion by 2033. This represents a compound annual growth rate (CAGR) of approximately 30.5%, a pace rarely seen in markets of this magnitude.

To understand the scale of this transformation, we need to look at the historical context. In 2020, the global AI market was valued at just $94.81 billion according to TechnologyChecker.io’s comprehensive analysis. By 2031, Statista Market Insights forecasts it will reach $1.675 trillion—representing a 17.7× expansion in just over a decade. This growth trajectory reframes every adjacent conversation about technology investment, workforce transformation, and competitive advantage.

The market segmentation reveals where value is being created. According to multiple research sources including Precedence Research and Grand View Research, AI software accounts for approximately 52% of total AI spending, with infrastructure (hardware) and services splitting the remainder. This software dominance reflects AI’s evolution from specialized hardware-dependent applications to cloud-deployed, API-accessible services that can be integrated into existing business processes with minimal friction.

Geographic distribution tells its own story. The United States continues to dominate AI investment, with over 80% of global private investment in AI flowing to US firms according to OECD data. However, China’s AI market is growing rapidly, with ByteDance alone considering AI capital expenditures of up to $70 billion. Europe, while lagging in absolute terms, is carving out a distinctive position in AI regulation and “sovereign AI” initiatives focused on data privacy and local control.

The AI chip market deserves special attention. NVIDIA, the dominant player in AI accelerators, holds approximately 80-81% of the AI data center chip market according to IDC and Silicon Analysts. The company’s data center revenue reached an extraordinary $193.7 billion in FY2026. AMD has emerged as the primary challenger, capturing roughly 5-7% market share with estimated Instinct GPU revenue of $7-8 billion. But the more significant competitive threat may come from custom silicon—Broadcom’s AI ASIC revenue exceeded $20 billion in FY2025, and Google, Amazon, and Microsoft continue investing heavily in their own chip designs.

Key Statistics and Data Points

The AI market in 2026 is defined by numbers that would have seemed fantastical just a few years ago. Here are the critical data points that every business leader, investor, and technologist should understand:

Market Size and Growth:

- Global AI market size 2026: $539.5 billion (Grand View Research)

- Global AI market size 2025: $390.9 billion

- Projected 2033 market size: $3.497 trillion

- Compound Annual Growth Rate (CAGR): 30.5%

- Year-over-year growth 2025-2026: 19%

- Global AI spending forecast 2026: $301 billion (IDC)

- Alternative AI spending estimate: $2.59 trillion (Gartner, including indirect AI-enabled spending)

Enterprise Adoption:

- Organizations using AI in at least one function: 88% (McKinsey 2025)

- Enterprises with at least one AI workload in production: 72% (McKinsey Q1 2026)

- Average number of AI models in production per enterprise: 4.2 (Gartner)

- Businesses using AI in at least one capacity: 91% (Azumo)

- Enterprises expected to use generative AI in production by 2026: 80%+ (Gartner)

Generative AI Specific:

- Generative AI market size 2025: $53.7 billion (Global Market Insights)

- Generative AI market size 2026: $83.3 billion

- Projected generative AI market 2035: $988.4 billion

- Generative AI CAGR 2026-2035: 31.6%

- Text generation segment market share: 48%

- Cloud deployment segment share: 73.8%

Productivity and ROI:

- Workers using AI save average of 5.4% of weekly work hours

- AI-enabled operations productivity gains: up to 40% (McKinsey)

- Cost per contact reduction with AI: 25% for veteran organizations

- AI customer service ticket resolution cost: $0.46 vs $4.18 human-handled (9× cheaper)

- Code review agent cost per PR: $0.72 vs $48 senior engineer time (66× cheaper)

- Median payback period for customer service AI: 4.1 months

- Median payback period for marketing operations AI: 6.7 months

Market Concentration:

- NVIDIA AI data center chip market share: 80-81%

- AMD AI accelerator market share: 5-7%

- ChatGPT share of AI chatbot traffic (Jan 2026): 64-68% (down from 87% in Jan 2025)

- AI startups’ share of global VC dollars: 53% (PitchBook)

- US share of global private AI investment: 80%+

Valuation Milestones:

- Anthropic valuation (May 2026): $965 billion

- OpenAI valuation (March 2026): $852 billion

- SpaceXAI (merged entity) valuation: $1.25 trillion

- Anthropic annualized revenue run-rate: $47 billion

Major Trends Shaping the AI Market in 2026

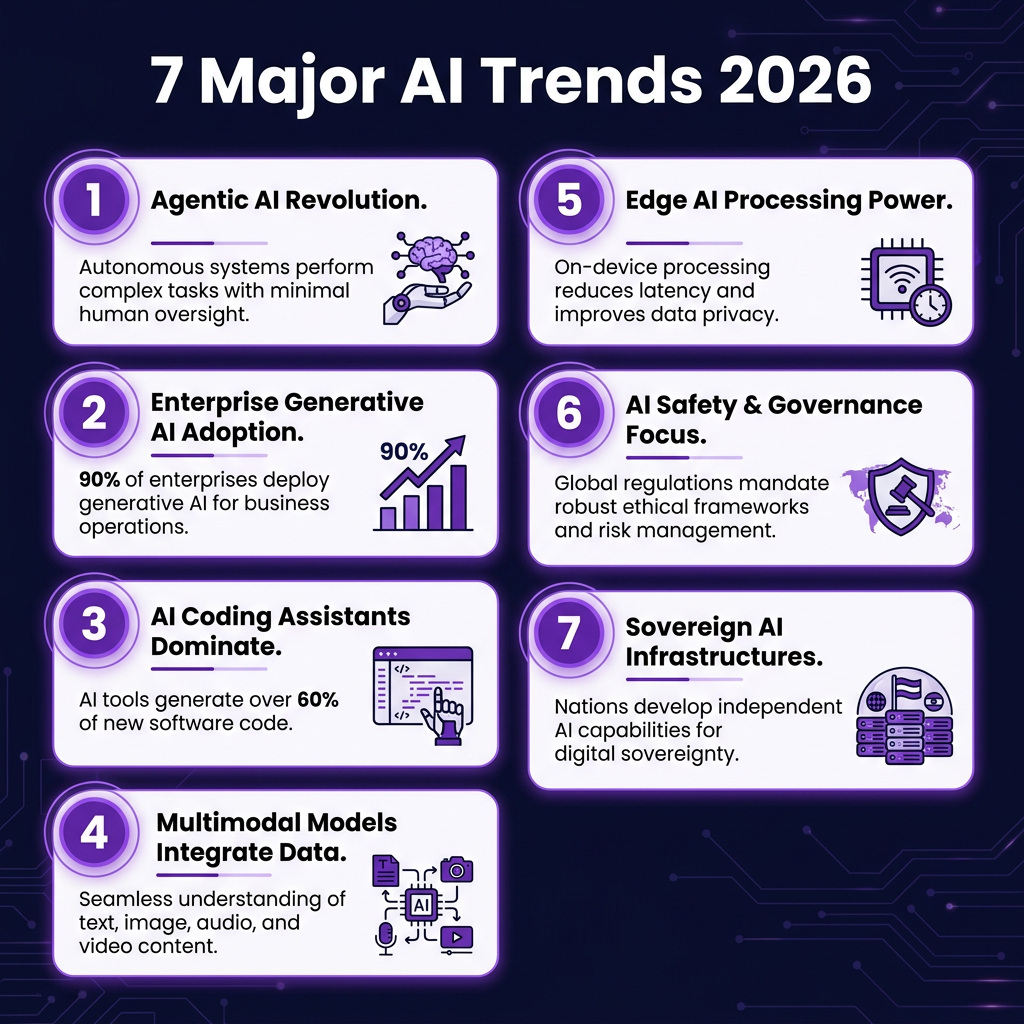

The AI landscape in 2026 is being shaped by seven dominant trends that are transforming how businesses adopt, deploy, and benefit from artificial intelligence. Understanding these trends is essential for anyone seeking to navigate this rapidly evolving market.

1. The Rise of Agentic AI

The most significant trend in 2026 is the emergence of agentic AI—systems that do not just respond to prompts but can plan, make decisions, trigger actions, and coordinate across systems with minimal human supervision. According to AI Handbook’s comprehensive analysis, agentic systems represent a fundamental shift from AI as a productivity assistant to AI as a workflow participant.

Google’s unveiling of Antigravity 2.0 at its 2026 developer conference exemplifies this trend—the system can “orchestrate multiple agents to execute tasks in parallel, such as having one agent code a website while another generates brand assets.” Microsoft, Anthropic, and OpenAI have all released agentic capabilities, with enterprise adoption accelerating rapidly. Bain’s Agentic AI Benchmark 2026 shows vendor-deployed agents reaching positive ROI 2.4× faster than custom builds.

2. Generative AI Becomes Enterprise Infrastructure

Generative AI has transitioned from experimental technology to core business infrastructure. According to Softweb Solutions, over 80% of enterprises are expected to use generative AI in a production environment by 2026. McKinsey reports productivity gains of up to 40% in AI-enabled operations.

This shift is characterized by several sub-trends: the integration of generative AI into existing enterprise applications rather than standalone tools; the rise of enterprise copilots embedded in productivity software; and the development of internal knowledge systems using retrieval-augmented generation (RAG) architectures. Organizations are no longer asking whether to adopt generative AI, but how to scale it responsibly across their operations.

3. AI Coding Assistants Transform Software Development

AI coding assistants have become the most rapidly adopted category of enterprise AI tools. According to CNBC’s reporting on the competitive landscape, Anthropic’s Claude Code has captured significant market share among developers for code generation—more than double OpenAI’s 21% in some segments. Companies like MongoDB have rolled out three generative AI tools including Claude Code to their engineers.

The impact extends beyond productivity metrics. AI coding assistants are changing the nature of software development itself—enabling developers to focus on architecture and problem-solving while AI handles routine implementation. This trend is driving the “vibe coding” movement, where developers describe intent in natural language and AI generates functional code.

4. Multimodal Models and Unified AI

The boundaries between text, image, audio, and video AI are dissolving. Leading models in 2026 are inherently multimodal—capable of understanding and generating content across modalities within a single architecture. This unification is enabling new use cases: generating video scripts from text prompts, creating interactive 3D environments from descriptions, and analyzing complex documents containing mixed media.

Google’s Gemini 3.5 Flash, released in 2026, exemplifies this trend with what the company describes as “frontier performance for agents and coding” across text, image, and video understanding. OpenAI’s GPT-5 and Anthropic’s Claude Opus 4.8 similarly offer native multimodal capabilities.

5. Edge AI and Distributed Intelligence

While much attention focuses on large cloud-based models, a parallel trend is driving AI to the edge. Small language models (SLMs) and specialized edge AI chips are enabling AI deployment in cost, latency, and privacy-constrained environments. This is particularly important for applications in manufacturing, healthcare, and autonomous systems where real-time processing is essential.

The emergence of efficient model architectures—quantized models running on consumer hardware, specialized AI accelerators in smartphones and IoT devices—is democratizing access to AI capabilities. MarketsandMarkets identifies small language models and edge AI as one of the key opportunities in the AI market.

6. AI Safety, Governance, and Regulation

As AI capabilities advance, so do concerns about safety, bias, and misuse. According to WitnessAI’s analysis of AI governance challenges, 88% of organizations report regular use of AI in at least one business function, but many have yet to define oversight roles for it. This gap between adoption and accountability represents significant enterprise risk.

Top generative AI threats being addressed include hallucinations (56%), cybersecurity (53%), intellectual property issues (46%), regulatory compliance (45%), and explainability (39%). The EU AI Act, implemented in 2024-2025, is setting global standards for AI regulation, with other jurisdictions following suit. Enterprises are increasingly investing in AI governance platforms and safety hardware as distinct commercial segments.

7. Sovereign AI and Geopolitical Fragmentation

The final major trend is the emergence of “sovereign AI”—national and regional initiatives to develop AI capabilities independent of US and Chinese technology. The EU, UK, Japan, India, and Middle Eastern nations are investing billions in domestic AI infrastructure, driven by concerns about data sovereignty, supply chain security, and strategic autonomy.

This trend is creating both opportunities and challenges for AI vendors. On one hand, it expands the addressable market for AI infrastructure. On the other, it fragments the global AI landscape into competing ecosystems with different standards, regulations, and technical requirements. MarketsandMarkets identifies sovereign AI hardware investment as creating structural long-term demand across all geographies.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a small number of extraordinarily valuable companies, but the competitive landscape is more nuanced than market caps suggest. Understanding the positioning of key players requires examining multiple layers of the AI stack.

The Foundation Model Leaders

Anthropic has emerged as the most valuable AI startup, with a $965 billion valuation following its $65 billion Series H financing round in May 2026. The company’s Claude models have gained significant traction in enterprise markets, particularly for coding and reasoning tasks. Anthropic’s focus on AI safety and constitutional AI has differentiated it in a crowded market. The company reported a $47 billion annualized revenue run-rate and has filed confidentially for an IPO expected in late 2026.

OpenAI, valued at $852 billion after a $122 billion funding round, remains the most recognized AI brand. ChatGPT’s dominance in consumer AI—despite market share declining from 87% to 64-68%—gives OpenAI unmatched distribution. The company’s partnership with Microsoft and integration into Office 365 and Azure provides enterprise reach that competitors struggle to match.

Google (Alphabet) continues to leverage its research leadership and infrastructure advantages. The Gemini model family, particularly Gemini 3.5 Flash, competes effectively on benchmarks. Google’s control of Android, Chrome, and Search provides distribution channels that pure-play AI companies cannot replicate. The company’s custom TPU chips also reduce inference costs compared to NVIDIA-dependent competitors.

Microsoft has successfully positioned itself as the enterprise AI platform, integrating OpenAI models into Copilot products across its productivity suite. The company’s Azure AI services generate substantial revenue, and its enterprise relationships give it advantages in B2B AI deployment. Microsoft’s investment in OpenAI—reportedly over $13 billion—has proven to be one of the most successful strategic partnerships in technology history.

The Hardware Layer

NVIDIA dominates AI hardware with approximately 80-81% of the AI data center chip market. The company’s data center revenue of $193.7 billion in FY2026 represents extraordinary value capture in the AI supply chain. NVIDIA’s CUDA software ecosystem creates powerful lock-in effects that competitors struggle to overcome. The company’s Blackwell and Rubin GPU architectures continue to set performance benchmarks.

AMD has emerged as the primary challenger to NVIDIA, with its Instinct GPU line capturing 5-7% market share. The MI350X matches NVIDIA’s B200 on FP8 compute and exceeds it on memory capacity. AMD’s stock gained 114% in 2026, reflecting investor optimism about its AI prospects.

Broadcom and custom silicon represent a longer-term threat to NVIDIA’s dominance. Broadcom’s AI ASIC revenue exceeded $20 billion in FY2025. Google (TPU), Amazon (Trainium/Inferentia), and Microsoft (Maia) continue investing in custom chips that could reduce dependence on NVIDIA over time.

Emerging Players

xAI/SpaceXAI, Elon Musk’s combined entity valued at $1.25 trillion after merging SpaceX with his AI startup, represents a unique positioning combining AI capabilities with space infrastructure and satellite networks.

Cognition, an AI coding startup, raised $1 billion at a $26 billion valuation in May 2026, demonstrating investor appetite for specialized AI applications.

Chinese competitors including ByteDance, Alibaba (Qwen), and Baidu continue developing competitive models, though US export controls on advanced chips constrain their access to cutting-edge training infrastructure.

Challenges and Pain Points

Despite the extraordinary growth and optimism surrounding AI, the market faces significant challenges that temper the hype with hard realities. Understanding these pain points is essential for realistic AI strategy development.

1. The ROI Gap

The most sobering statistic in AI adoption comes from PwC’s Global CEO Survey: 56% of CEOs report zero measurable ROI from AI in the past 12 months. This disconnect between AI investment and business value realization represents the central challenge facing the industry. While AI demonstrates clear productivity gains at the task level—workers save an average of 5.4% of weekly work hours—translating these micro-efficiencies into macro business outcomes remains difficult.

The “pilot-to-production gap” is the single most cited reason agent programs miss year-one ROI. According to Digital Applied’s research, 90% of AI pilots fail to scale to production. This gap between proof-of-concept and operational deployment represents billions in wasted investment and frustrated expectations.

2. Integration with Legacy Systems

According to ISHIR’s analysis of enterprise AI adoption, integrating AI solutions with outdated systems is one of the most cited challenges. Many enterprises still operate on legacy infrastructure that was not designed for real-time data processing or AI workloads. This integration challenge causes project delays, cost overruns, and implementation failures.

The PEX Report 2025/26 found that 52% of organizations cite data quality and availability as primary barriers to AI adoption. Without strong data governance frameworks, AI models produce unreliable outputs, leading to mistrust and low adoption. The reality is that AI implementation often requires expensive, time-consuming data infrastructure modernization before value can be realized.

3. Skills and Talent Shortage

Forbes identifies skill deficits as the leading barrier to AI adoption in 2026, encompassing both “hard” technical skills (machine learning engineering, data science, MLOps) and “soft” skills (change management, AI literacy, ethical reasoning). The concentration of AI talent at a small number of companies and in specific geographic regions creates structural inequality in capability development.

This talent shortage drives up costs—AI engineers command premium salaries—and constrains the ability of organizations to build and maintain AI systems. The gap between what organizations want to implement and what they have the capability to deploy continues to widen.

4. Security and Governance Risks

According to S3 Corp’s analysis, AI security and data privacy risks rank among the top 10 AI challenges in 2026. Legacy DLP (Data Loss Prevention), CASB (Cloud Access Security Broker), and endpoint tools are structurally blind to AI-specific risks because they cannot understand conversational intent, inspect bidirectional AI traffic, or see activity in native apps and IDEs.

The gap between employee AI adoption and organizational governance creates significant exposure. Employees are using AI tools—often consumer versions without enterprise controls—to process sensitive business data. This “shadow AI” phenomenon represents a compliance and security nightmare that most organizations are only beginning to address.

5. Regulatory Uncertainty

While the EU AI Act provides some clarity, global AI regulation remains fragmented and evolving. Organizations operating across jurisdictions face conflicting requirements that complicate AI deployment. The prospect of stricter regulation—particularly around high-risk AI applications—creates uncertainty that delays investment and innovation.

Opportunities and Growth Strategies

Despite the challenges, the AI market presents extraordinary opportunities for organizations that can navigate the complexity effectively. Here are the key strategic opportunities in 2026:

1. Vertical AI Applications

The most significant near-term opportunity lies in AI applications tailored to specific industries. While horizontal platforms (ChatGPT, Claude) capture attention, vertical solutions—AI for healthcare diagnostics, AI for legal document review, AI for manufacturing quality control—deliver measurable ROI by solving domain-specific problems.

Enterprise AI spend hit $37 billion in 2025—up from $1.7 billion in 2023—driven largely by vertical applications. This 6% of the global SaaS market captured in just two years demonstrates the appetite for specialized AI solutions. Companies that can combine deep domain expertise with AI capabilities are capturing significant value.

2. AI-Enabled Services Transformation

Professional services industries—consulting, legal, accounting, creative—are being transformed by AI. The opportunity is not just using AI internally but fundamentally restructuring service delivery models. AI-enabled consultants can serve more clients with better insights. AI-assisted lawyers can review contracts faster and more accurately. AI-augmented creatives can produce more variations and iterations.

The key strategy is positioning AI as augmentation rather than replacement—enhancing professional capabilities rather than eliminating professional roles. Organizations that successfully navigate this positioning will capture market share from slower-moving competitors.

3. AI Infrastructure and Tooling

The picks-and-shovels opportunity in AI remains compelling. As more organizations deploy AI, demand for infrastructure—compute, storage, networking, MLOps tools, observability platforms, security solutions—continues to grow. NVIDIA’s extraordinary revenue demonstrates the value capture possible at the infrastructure layer.

Opportunities exist across the stack: specialized AI chips for edge deployment, optimization tools for model compression and quantization, governance platforms for AI risk management, and integration tools for connecting AI to enterprise systems.

4. Small Language Models and Edge AI

While much attention focuses on the largest models, significant opportunities exist in smaller, specialized models optimized for specific tasks and deployment environments. Small language models (SLMs) can run on consumer hardware, enabling AI deployment in privacy-sensitive applications and disconnected environments.

This trend is particularly relevant for healthcare (patient data privacy), manufacturing (latency requirements), and government (security classification). Organizations that can deliver capable models with minimal resource requirements will capture segments of the market that cloud-only solutions cannot serve.

Case Studies and Success Stories

Real-world examples demonstrate how organizations are successfully deploying AI to drive business value. These case studies illustrate best practices and measurable outcomes.

Case Study 1: Nasdaq — AI Platform for Market Operations

Nasdaq, one of the world’s premier stock exchanges, built an AI platform to optimize its internal operations and enhance its external products. According to NVIDIA’s State of AI report, the platform helps improve functionality and user experience while streamlining internal work processes.

The implementation demonstrates how financial services firms can leverage AI for both customer-facing and internal applications. By building a unified AI platform rather than point solutions, Nasdaq achieved integration benefits that compound over time. The company’s approach—combining proprietary market data with AI capabilities—creates defensible competitive advantages.

Case Study 2: Snowflake — AI-Assisted Development

Snowflake, the data analytics software company, has equipped its programmers with multiple AI coding tools including Claude Code. According to CEO Sridhar Ramaswamy, programmers mainly depend on the company’s own CoCo development tool alongside Claude Code.

This multi-tool approach reflects a maturing understanding of AI capabilities—different tools excel at different tasks, and developers benefit from choice. Snowflake’s experience demonstrates that AI coding assistants can be deployed at scale in sophisticated engineering organizations without compromising code quality or security.

Case Study 3: MongoDB — Multi-Tool AI Strategy

Database software maker MongoDB has rolled out three generative AI tools to its engineers, including Anthropic’s Claude Code. According to CEO CJ Desai, this multi-vendor approach provides developers with options while avoiding single-provider dependencies.

MongoDB’s strategy illustrates a broader trend: enterprises are increasingly reluctant to bet entirely on single AI vendors. By maintaining relationships with multiple providers, organizations preserve negotiating leverage and reduce concentration risk. This approach requires more sophisticated AI governance but provides strategic flexibility as the market evolves.

Future Outlook and Predictions

Looking beyond 2026, several developments will shape the AI market through 2030 and beyond. Understanding these trajectories is essential for long-term strategic planning.

Near-Term: 2026-2027

The immediate future will be characterized by the mainstreaming of agentic AI. By late 2026, agentic systems will move from early adopters to mainstream enterprise deployment. The IPOs of Anthropic (expected December 2026) and OpenAI (filed June 2026) will provide public market valuations that reset investor expectations for AI companies.

Regulatory clarity will improve as jurisdictions implement AI-specific frameworks. The EU AI Act requirements will force global enterprises to adopt compliance practices that become de facto standards. This regulatory maturation will reduce uncertainty and enable larger-scale investment.

Medium-Term: 2027-2028

By 2028, extrapolating current progress rates suggests AI models with beyond-human reasoning abilities, expert-level knowledge in every domain, and the capability to autonomously complete multi-week projects. According to 80,000 Hours analysis, this level of capability would represent a fundamental shift in AI’s economic and social impact.

The AI chip market will see increased competition as AMD, Intel, and custom silicon providers capture share from NVIDIA. This competition will drive down inference costs and accelerate AI adoption in price-sensitive applications.

Long-Term: 2028-2033

The $3.5 trillion AI market projected for 2033 implies AI becoming one of the largest sectors of the global economy. By this timeframe, AI will likely be embedded in virtually every business process, product, and service. The distinction between “AI companies” and “companies” will become meaningless—AI will be as fundamental to business operations as electricity or the internet.

Several scenarios are possible: continued incremental improvement leading to gradual economic transformation; breakthrough capabilities that accelerate adoption and create new categories of AI-native businesses; or regulatory and safety constraints that limit deployment in sensitive applications. The most likely outcome is a combination of all three—rapid advancement in some domains, careful regulation in others, and gradual integration across the economy.

Key Takeaways

- The global AI market reached $539.5 billion in 2026, growing 19% year-over-year and projected to reach $3.5 trillion by 2033.

- Enterprise AI adoption has reached 88% of organizations, with generative AI becoming core business infrastructure.

- Seven major trends are reshaping the market: agentic AI, enterprise generative AI, AI coding assistants, multimodal models, edge AI, AI safety/governance, and sovereign AI.

- The competitive landscape is dominated by Anthropic ($965B valuation), OpenAI ($852B), Google, Microsoft, and NVIDIA (80% chip market share).

- Despite the growth, 56% of CEOs report zero measurable ROI from AI investments, highlighting the implementation challenges.

- The most significant opportunities lie in vertical AI applications, AI-enabled services transformation, and AI infrastructure/tooling.

Sources and Citations

- Grand View Research – AI Market Size Report 2026

- IDC Worldwide AI Spending Guide 2026

- McKinsey Global Survey on AI 2025

- Statista Market Insights – AI Market Forecast 2031

- TechnologyChecker.io – AI Market Analysis

- Global Market Insights – Generative AI Market Report

- PitchBook – AI Venture Capital Trends 2026

- CNBC – AI Coding Assistant Market Analysis

- AI Handbook – Agentic AI Trends 2026

- Bain & Company – Agentic AI Benchmark 2026

- NVIDIA State of AI Report 2026

- Silicon Analysts – AI Chip Market Share

- WitnessAI – AI Governance Challenges

- PwC Global CEO Survey 2026

- MarketsandMarkets – AI Market Opportunities