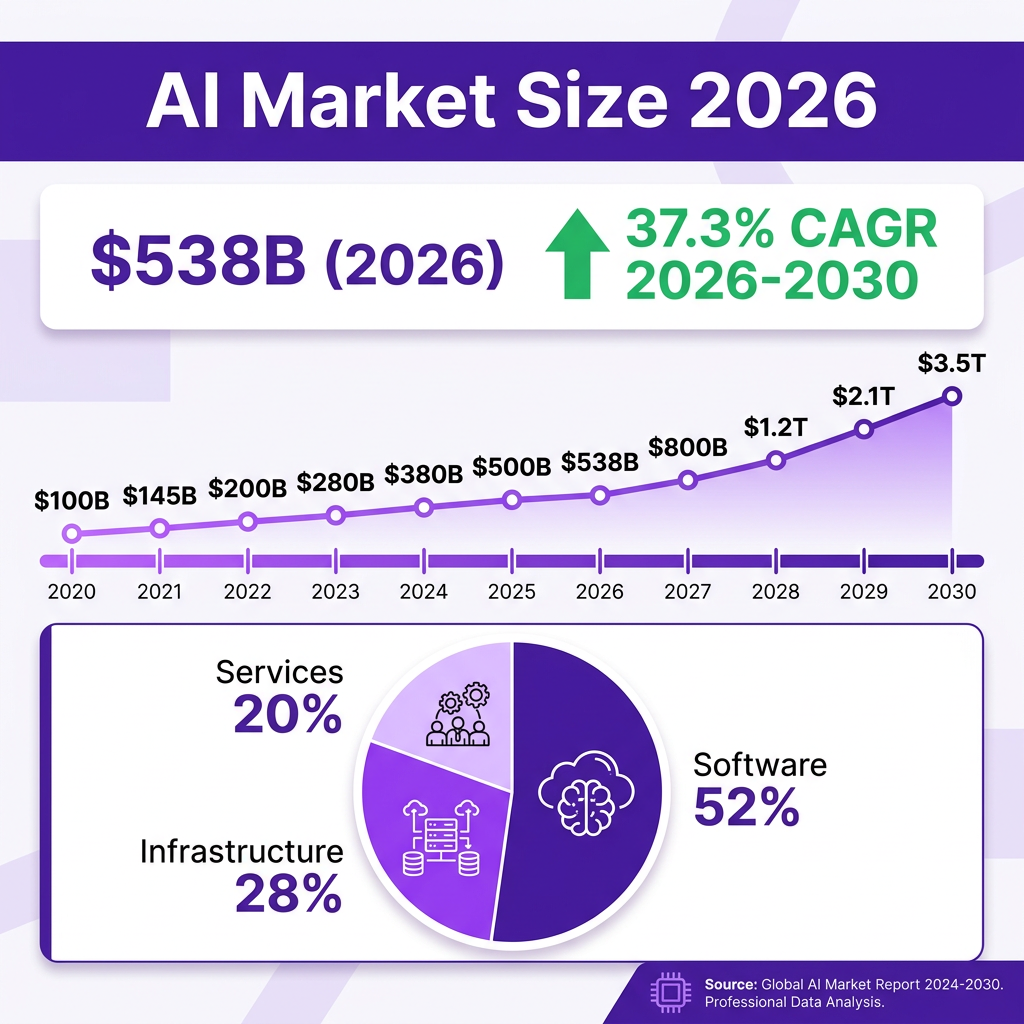

The artificial intelligence market has reached an inflection point in 2026. With a global valuation of $538 billion and a staggering 37.3% year-over-year growth rate, AI has transitioned from experimental technology to the backbone of modern enterprise operations. Nearly 1.8 billion people have now used some form of AI tool, and 72% of enterprises report having at least one AI workload in production. This represents a fundamental shift in how businesses operate, compete, and create value in the digital economy.

What started as curiosity about ChatGPT’s ability to count letters in “strawberry” has evolved into a fundamental restructuring of how businesses operate, compete, and create value. The AI market is no longer just about large language models—it is about agentic AI systems that can autonomously complete complex tasks, enterprise automation at massive scale, and the trillion-dollar infrastructure powering this technological revolution. The implications extend far beyond Silicon Valley, touching every industry, every job function, and every aspect of modern life.

Market Overview: The $538 Billion AI Ecosystem

The global artificial intelligence market has experienced unprecedented expansion, growing from $390.91 billion in 2025 to $538 billion in 2026. This represents a compound annual growth rate (CAGR) of 37.3%, making AI one of the fastest-growing technology sectors in history. To put this growth in perspective, the AI market is expanding faster than the early internet, faster than mobile computing, and faster than cloud computing in their respective growth phases. By 2033, market analysts project the AI industry will reach nearly $3.5 trillion, fundamentally reshaping the global economy and creating new categories of businesses that do not exist today.

The market composition reveals three dominant segments that together form the complete AI value chain. AI software commands the largest share at 52% of total spending, encompassing everything from machine learning platforms to natural language processing tools, computer vision systems, and robotic process automation. This software layer includes both horizontal platforms that can be applied across industries and vertical solutions tailored to specific sectors like healthcare, finance, and manufacturing.

Infrastructure represents 28% of the market, driven by massive investments in data centers, GPUs, TPUs, and specialized AI accelerators. This infrastructure layer has become critically important as training large AI models requires enormous computational resources. Companies are investing billions in building AI-optimized data centers, with Microsoft alone committing $80 billion to AI infrastructure in 2025. The demand for AI compute has created supply constraints, with wait times for GPU clusters extending months into the future.

Services round out the remaining 20%, including consulting, implementation, managed AI services, and training. As organizations struggle to implement AI effectively, the services market has exploded. Consulting firms like McKinsey, Deloitte, and Accenture have built massive AI practices, while specialized AI consultancies have emerged to serve mid-market companies. The talent shortage in AI has made these services essential for organizations that cannot hire sufficient in-house expertise.

Regional distribution shows the United States maintaining its leadership position, with the US AI market valued at approximately $47 billion. American companies attracted over 80% of global private AI investment in 2025, underscoring the country’s dominance in AI innovation and venture capital deployment. The concentration of leading AI labs—OpenAI, Anthropic, Google DeepMind, and Meta AI—in the United States has created a self-reinforcing ecosystem of talent, capital, and research.

However, China’s AI sector continues to grow rapidly, with companies like DeepSeek-R1 demonstrating competitive capabilities in reasoning models. Chinese AI companies benefit from massive domestic data sets, government support, and a large pool of engineering talent. The geopolitical competition in AI has become a central focus for both countries, with export controls on AI chips and restrictions on technology transfer shaping the competitive landscape.

The generative AI subsegment deserves special attention as the fastest-growing category within AI. Growing at a CAGR of 29%, the generative AI market is expected to expand from $37.1 billion in 2024 to $220 billion by 2030. Marketing, advertising, and creative applications account for 46% of enterprise value creation from generative AI, highlighting how businesses are leveraging these tools for content creation, design, and customer engagement. But the applications extend far beyond creative work to include code generation, document analysis, customer service automation, and scientific research.

Healthcare remains the largest industry vertical for AI applications, capturing 25.7% of total AI spending. From drug discovery to diagnostic imaging, AI is revolutionizing medical research and patient care. Pharmaceutical companies are using AI to identify promising drug candidates faster and cheaper than traditional methods. Hospitals are deploying AI for radiology, pathology, and early disease detection. Financial services, retail, manufacturing, and automotive sectors follow closely, each developing sophisticated AI implementations tailored to their specific operational challenges.

Key Statistics and Data Points

The AI industry’s growth is supported by compelling data across multiple dimensions. Understanding these statistics is essential for businesses making investment decisions, policymakers crafting regulations, and investors evaluating opportunities. Here are the most significant statistics defining the AI landscape in 2026:

Market Size and Growth: The global AI market reached $538 billion in 2026, up from $390.91 billion in 2025, representing a 37.3% growth rate. The generative AI market specifically stands at $63 billion according to Statista, while the broader AI software market continues to expand at double-digit rates. The wearable AI market is projected to reach $303 billion by 2035, demonstrating AI’s penetration into consumer hardware. AI chipsets alone represent a market expected to hit $931 billion by 2034, highlighting the infrastructure investment driving the industry.

Adoption Rates: 72% of enterprises now have at least one AI workload in production, up significantly from previous years. This represents a tipping point where AI has moved from experimental to operational for most large organizations. 35.49% of people use AI tools every day for work or personal tasks, indicating mainstream consumer adoption. The average enterprise runs 4.2 AI models in production, compared to just 1.9 in 2023, showing how organizations are expanding their AI capabilities. Global spending on AI systems is forecast to surpass $301 billion in 2026 according to IDC.

Enterprise Usage Patterns: 100% of industries are increasing AI usage according to PwC research, indicating universal adoption across sectors. 78% of organizations use AI in at least one business unit, showing deep penetration into corporate operations. However, over 50% of companies report gaining no measurable value yet from their AI investments, highlighting the implementation challenges many organizations face. This gap between adoption and value realization represents both a risk and an opportunity. 63% of AI users turn to the technology primarily for research and question-answering, making information retrieval the dominant use case.

Investment and Funding: AI startups attracted a majority of global VC dollars in 2025 at 53% of total venture capital investment, making AI the dominant category in venture funding. Q1 2026 shattered venture funding records, pushing startup investment to $300 billion globally. Tech megacaps are projected to invest over $300 billion in AI infrastructure in 2026, with Microsoft, Google, Amazon, and Meta leading the spending. Early-stage AI VC deals consistently account for a quarter of total AI investment value, showing continued interest in new AI companies.

Technology Infrastructure: NVIDIA maintains an 81% market share in AI data center chips, making it the dominant player in AI hardware. AMD’s MI300X accelerator captured roughly 10% of the AI accelerator market by 2026, up from about 5% in 2024, showing successful competition. Google Cloud revenue hit $20.03 billion in recent quarters, up 63%, with AI-built products growing 800% year-over-year. AI-related cloud spending is driving significant growth across AWS, Microsoft Azure, and Google Cloud Platform, with AI workloads becoming a primary growth driver for cloud providers.

Productivity and ROI: 99% of telecommunications respondents reported AI helped improve employee productivity, with a quarter citing major or significant improvements. AI drives productivity gains across every industry, with measurable impacts on both revenue growth and cost reduction. Nasdaq built an AI platform that improved functionality and user experience while streamlining internal work processes. Companies are increasingly shifting ROI measurement from productivity metrics to direct P&L impact, showing how AI is moving from cost center to profit driver.

Consumer Adoption: ChatGPT now handles over 5 billion monthly visits, making it one of the most visited websites globally. Cooking and meal planning is the top “life situation” AI use case among consumers, followed by writing assistance and research. Nearly 1.8 billion people have used some kind of AI tool, representing approximately 22% of the global population. This consumer familiarity with AI is driving enterprise adoption as employees bring AI tools into the workplace.

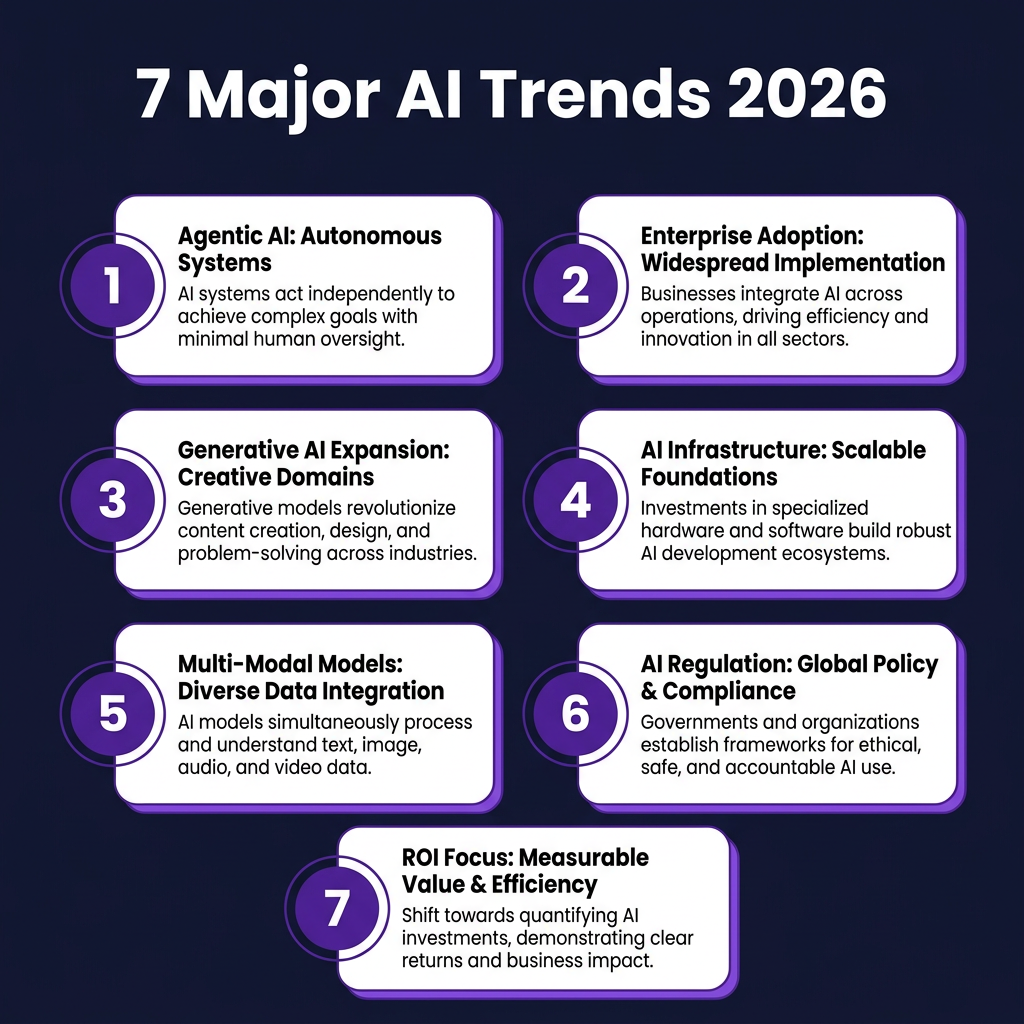

Major Trends Shaping AI in 2026

The AI landscape is evolving rapidly, with seven major trends defining the industry’s trajectory in 2026. These trends represent both technological developments and shifts in how organizations approach AI implementation. Understanding these trends is essential for businesses looking to leverage AI effectively and for investors evaluating opportunities in the space.

1. The Rise of Agentic AI

Agentic AI—systems capable of autonomous decision-making and action—has emerged as the fastest-growing technology priority among enterprises, surging 31.5% in adoption according to Futurum Research. Unlike traditional AI models that respond to prompts, agentic AI can initiate actions, manage workflows, and complete complex multi-step tasks without human intervention. This represents a fundamental shift from AI as a tool to AI as an autonomous worker.

Companies like Atolio are pioneering private and secure deployments with real ROI expectations, while AuthMind predicts that agentic AI and other non-human identities will soon outnumber human users in organizations. The implications are profound: businesses will need to manage fleets of AI agents alongside human employees, with different governance, security, and performance management requirements.

Agentic AI is already being deployed for customer service, where AI agents can handle complete support interactions from initial contact through resolution. In software development, agentic AI can write code, run tests, debug issues, and deploy updates autonomously. In sales, AI agents can research prospects, craft personalized outreach, and manage follow-up sequences. These applications are just the beginning of what agentic AI will enable.

2. Enterprise Production Deployment

The shift from AI experimentation to production-grade systems represents a fundamental maturation of the market. After years of pilots and proofs-of-concept, enterprises are now demanding AI systems that can operate reliably at scale, integrate with existing infrastructure, and deliver measurable business value. As Tomás Hernando Kofman of Not Diamond notes, “The massive middle of the enterprise bell curve begins to move from experimentation to production-grade systems.”

This transition requires orchestration layers that can industrialize innovation, putting ideas into production with continuous monitoring. Enterprises are reserving 20-30% of their AI budgets for exploratory use cases while focusing the majority on proven, scalable implementations. The emphasis has shifted from “what’s possible with AI” to “what works reliably in production.”

Production deployment brings new challenges around reliability, observability, and governance. Organizations need to monitor AI systems for drift, bias, and performance degradation. They need processes for updating models without disrupting operations. And they need clear accountability when AI systems make mistakes. These operational requirements are driving demand for AI infrastructure and tooling.

3. Generative AI Value Creation

Generative AI use cases are projected to create $434 billion in value for enterprises annually by 2030. Marketing, advertising, and creative applications lead this value creation, but code generation, document processing, and customer service automation are rapidly catching up. The technology has moved beyond novelty to become a core productivity tool integrated into daily workflows.

Companies like FanDuel generate millions of impressions through AI-powered chatbots, while K&L Wines saves 14+ hours daily with 99% accurate AI SKU matching. These examples demonstrate how generative AI can deliver both top-line growth and bottom-line efficiency. The key is identifying high-value use cases where generative AI can augment human capabilities rather than simply replacing them.

The generative AI market is also seeing rapid innovation in model capabilities. Multimodal models that can process and generate text, images, audio, and video are enabling new applications. Models with larger context windows can analyze entire documents or codebases. And improvements in reasoning capabilities are making generative AI suitable for more complex tasks.

4. AI Infrastructure Investment

Microsoft’s concept of AI “superfactories”—linked global AI systems that drive down costs and improve efficiency—represents the next evolution of AI infrastructure. These massive data center complexes require unprecedented capital investment, with tech giants collectively committing over $300 billion to AI infrastructure in 2026. The scale of this investment rivals the build-out of the electrical grid or the interstate highway system.

The focus is on flexible, global systems that can handle the computational demands of increasingly sophisticated AI models while maintaining cost efficiency. This includes not just GPUs but also networking equipment, power systems, cooling infrastructure, and specialized AI accelerators. The companies that control this infrastructure will have significant competitive advantages in the AI era.

Energy consumption has become a critical consideration, with AI data centers requiring massive amounts of electricity. This is driving investment in renewable energy, nuclear power, and more efficient cooling systems. Some analysts project that AI could consume 3-4% of global electricity by 2030, creating both environmental challenges and opportunities for energy companies.

5. Multi-Modal AI Expansion

AI systems are increasingly capable of processing and generating multiple types of data—text, images, audio, and video—simultaneously. This multi-modal capability enables more natural human-computer interaction and opens new application areas. Users can ask AI systems to analyze a video, generate an image from a text description, or create audio content from written scripts.

From generating product design variations to creating digital twin simulations that test variations in hours rather than weeks, multi-modal AI is accelerating innovation across industries. In healthcare, multi-modal AI can analyze medical images alongside patient records and genetic data. In manufacturing, it can combine sensor data with visual inspection to predict equipment failures. The ability to work across data types makes AI more powerful and applicable to real-world problems.

6. AI Regulation and Governance

As AI capabilities advance, regulatory frameworks are evolving to address ethical concerns, data privacy, and safety. The European Union’s AI Act and similar legislation worldwide are creating compliance requirements that shape how AI systems are developed and deployed. Organizations are establishing AI governance frameworks, with 78% of organizations using AI in at least one business unit now having formal AI policies in place.

Ethics has become the defining issue for AI’s future, with institutions like Darden’s LaCross Institute for Ethical Artificial Intelligence in Business leading research and education efforts. Companies are appointing Chief AI Ethics Officers, establishing AI review boards, and implementing responsible AI principles. The organizations that get ahead of regulation will have competitive advantages as compliance requirements increase.

7. ROI Measurement Evolution

Enterprise AI ROI measurement is shifting from productivity metrics to direct P&L impact. Companies are moving beyond measuring time saved or tasks automated to tracking revenue growth, cost reduction, and competitive advantage. This evolution reflects AI’s maturation from experimental technology to core business infrastructure.

However, the gap between AI leaders and laggards is widening, with top performers moving into advanced techniques while others struggle with basic implementation. Companies that successfully measure and optimize AI ROI are reinvesting in more sophisticated capabilities, creating a virtuous cycle of improvement. Those that cannot demonstrate value risk having their AI budgets cut.

Key Players and Competitive Landscape

The AI market is dominated by a mix of established technology giants and emerging innovators, each carving out distinct positions in the value chain. Understanding this competitive landscape is essential for businesses selecting AI partners and for investors evaluating opportunities. The market structure is still evolving, with new entrants challenging incumbents and partnerships reshaping competitive dynamics.

Foundation Model Leaders

OpenAI remains the most recognized name in consumer AI, with ChatGPT handling over 5 billion monthly visits. The company has completed its transition to a for-profit structure, with Microsoft now holding a 27% stake. OpenAI’s GPT models continue to set benchmarks for natural language understanding and generation. The company’s API business serves millions of developers, while its enterprise offerings target large organizations with advanced security and compliance features.

OpenAI’s strategy focuses on building increasingly capable general-purpose AI systems while developing specialized products for specific use cases. The company faces the challenge of monetizing its massive research investments while competing with open-source alternatives and other well-funded labs. Its partnership with Microsoft provides both capital and cloud infrastructure, but also creates dependencies.

Anthropic has established itself as a leader in AI safety and alignment, with its Claude models offering competitive capabilities alongside strong ethical frameworks. The company’s focus on constitutional AI and responsible development has attracted significant enterprise interest, particularly among organizations concerned about AI risks. Anthropic’s research on AI safety has influenced the broader industry and informed regulatory discussions.

Anthropic has taken a different approach to commercialization than OpenAI, emphasizing enterprise partnerships and API access over consumer products. The company has raised billions in funding from Google and other investors, giving it the resources to compete with larger labs. Its emphasis on safety and reliability resonates with risk-conscious enterprise buyers.

Google DeepMind combines Google’s research capabilities with DeepMind’s breakthrough achievements in areas like protein folding. Alphabet CEO Sundar Pichai reported that revenue from AI-built products grew 800% over the prior year, with Google Cloud hitting $20.03 billion in revenue, up 63%. Google’s advantage lies in its massive data resources, distribution through Search and Workspace, and deep research expertise.

Google has integrated AI throughout its product portfolio, from Search to Gmail to Google Cloud. The company’s Gemini models compete directly with GPT-4 and Claude, while its specialized models target specific domains like healthcare and scientific research. Google’s challenge is maintaining its search dominance as AI changes how people find information.

Infrastructure Providers

NVIDIA dominates AI hardware with an 81% market share in AI data center chips. The company’s GPUs are the de facto standard for training and running large AI models, with demand consistently outstripping supply. NVIDIA’s annual “State of AI” reports have become essential reading for understanding industry adoption patterns. The company has expanded beyond hardware to offer software platforms, development tools, and cloud services.

NVIDIA’s competitive moat includes not just hardware performance but also the CUDA software ecosystem, which has become the standard for AI development. The company continues to innovate, with each new GPU generation offering significant performance improvements. However, it faces growing competition from AMD, custom silicon from cloud providers, and specialized AI chips.

AMD has emerged as a credible challenger, with its MI300X accelerator capturing roughly 10% of the AI accelerator market by 2026, up from about 5% in 2024. This growth reflects enterprise demand for alternatives to NVIDIA’s dominant position and competitive pricing from AMD. The company’s acquisition of Xilinx has strengthened its position in adaptive computing for AI workloads.

Cloud Providers—AWS, Microsoft Azure, and Google Cloud Platform—are battling for AI workloads, with AI capabilities becoming a key differentiator in cloud services. AWS maintains market leadership, but Microsoft has leveraged its OpenAI partnership to gain significant ground, while Google Cloud’s AI-first approach is attracting enterprise customers. The cloud providers offer managed AI services that reduce the complexity of building AI applications.

Emerging Players

Databricks helps companies connect AI to their own data, addressing one of the biggest challenges in enterprise AI adoption. The company’s data intelligence platform has become essential infrastructure for organizations building custom AI solutions. Databricks’ focus on data engineering, machine learning operations, and collaborative analytics has made it a critical vendor for data-driven enterprises.

Not Diamond offers multi-model AI infrastructure that helps enterprises select the optimal AI model for each task, optimizing both performance and cost. This approach reflects growing enterprise sophistication in AI deployment, as organizations realize that different models excel at different tasks. Model routing and selection have become important capabilities for optimizing AI investments.

Chinese Labs including DeepSeek are developing competitive reasoning models that challenge Western AI dominance. DeepSeek-R1 demonstrated that sophisticated AI capabilities can be developed with different approaches to training and architecture. Chinese AI companies benefit from massive domestic markets, government support, and growing pools of research talent. The competition between US and Chinese AI capabilities has become a central geopolitical issue.

Challenges and Pain Points

Despite remarkable growth, the AI industry faces significant challenges that threaten to slow adoption and create risks for businesses and society. Addressing these challenges is essential for realizing AI’s full potential while minimizing harm. Organizations that navigate these challenges effectively will have significant competitive advantages.

1. The Implementation Gap

While 72% of enterprises have AI workloads in production, over 50% of companies report gaining no measurable value from their AI investments. This implementation gap reflects the complexity of integrating AI into existing workflows, the need for specialized talent, and the challenge of identifying high-value use cases. Many organizations are stuck in pilot purgatory, running experiments that never scale to production.

The gap between AI leaders and laggards is widening. Top performers are moving into advanced techniques like multi-modal AI, real-time personalization, and autonomous decisioning, while laggards may still be trying to get basic predictive analytics in place. This divergence has implications for competitive dynamics across industries.

2. Algorithmic Bias and Fairness

AI models perpetuate social and historical biases present in training data, causing discrimination in facial recognition, hiring decisions, lending, and healthcare. A large language model used in a US courtroom cited six cases that did not exist, demonstrating how AI can generate confident but false information with serious consequences. Addressing bias requires diverse training data, bias testing at every stage of development, and ongoing monitoring of model outputs.

The challenge of AI bias is compounded by the difficulty of defining fairness. Different stakeholders may have different notions of what constitutes fair AI decision-making. Technical approaches to debiasing AI systems are still evolving, and there are trade-offs between fairness, accuracy, and interpretability.

3. Privacy and Security Concerns

AI’s hunger for data leads to pervasive surveillance risks, mass data misuse, and potential techno-authoritarianism. Sensitive training data creates security vulnerabilities, with external cyberattacks potentially manipulating model outputs through data poisoning or adversarial examples. Organizations must implement privacy-first data practices, robust access controls, and continuous security monitoring to protect both their data and their AI systems.

The security risks extend beyond data to the AI models themselves. Model theft, reverse engineering, and extraction attacks can compromise valuable intellectual property. As AI systems become more autonomous, the potential impact of security breaches increases.

4. Explainability and Trust

Many AI models, particularly deep learning systems, cannot explain their decisions in human-understandable terms. This “black box” problem creates compliance gaps in regulated sectors and undermines trust among users and stakeholders. Explainability tools built into AI evaluation processes are essential for high-stakes applications in healthcare, finance, and legal contexts.

The tension between model performance and explainability is a persistent challenge. Often, the most accurate models are the least interpretable. Organizations must make trade-offs based on the specific requirements of each use case, with explainability being more critical for high-stakes decisions.

5. Talent Shortage

The demand for AI expertise far outstrips supply, with companies competing fiercely for data scientists, machine learning engineers, and AI strategists. This talent shortage drives up costs and slows implementation, particularly for organizations that cannot match the compensation packages offered by tech giants. Upskilling existing employees and creating AI literacy programs has become essential for enterprise AI adoption.

The talent shortage extends beyond technical roles to include AI ethicists, AI product managers, and AI-savvy business leaders. Organizations need people who can bridge the gap between technical capabilities and business value, translating AI possibilities into practical applications.

6. Environmental Impact

Training large AI models requires enormous computational resources, with significant energy consumption and carbon footprint implications. As models grow larger and more complex, their environmental impact increases. This has sparked interest in more efficient model architectures, renewable energy for data centers, and techniques for reducing the computational requirements of AI training and inference.

The environmental concerns are driving innovation in green AI, including more efficient algorithms, specialized low-power chips, and carbon-aware training schedules. Some organizations are beginning to include carbon footprint in their AI procurement criteria, creating market pressure for more sustainable AI solutions.

Opportunities and Growth Strategies

Despite challenges, the AI market presents enormous opportunities for organizations that can navigate its complexities effectively. The key is developing strategies that leverage AI’s capabilities while managing its risks. Here are the primary growth strategies we are seeing succeed in the market:

1. Enterprise AI Transformation

Organizations are leveraging AI-driven solutions to enhance operational efficiency, decision-making, and overall business value. Successful implementations require strategic planning, technology adoption, and change management. Companies that establish centralized AI offices or centers of excellence benefit from effective use of specialized expertise and collaboration across AI initiatives.

The key is moving beyond pilots to production-grade systems that deliver measurable ROI. This requires not just technology but also organizational change—new processes, new skills, and new ways of working. Companies that treat AI as a strategic transformation rather than a technology project are seeing the best results.

2. AI-Powered Customer Experience

Real-time personalization, AI-powered chatbots, and predictive customer service are transforming how businesses interact with their customers. Companies implementing these technologies report significant improvements in customer satisfaction, retention, and lifetime value. The opportunity extends beyond customer service to personalized marketing, product recommendations, and proactive support.

The most successful implementations combine AI capabilities with human judgment, using AI to handle routine interactions while escalating complex issues to human agents. This hybrid approach delivers both efficiency and quality, meeting customer expectations for fast, personalized service.

3. Industry-Specific AI Solutions

While horizontal AI platforms offer broad capabilities, industry-specific solutions often deliver superior results. Healthcare AI for drug discovery, financial AI for fraud detection, manufacturing AI for predictive maintenance, and retail AI for demand forecasting represent multi-billion dollar opportunities. Companies that combine deep industry expertise with AI capabilities are capturing significant market share.

Industry-specific AI benefits from domain-specific data, regulatory compliance built-in, and workflows tailored to sector requirements. These solutions can deliver value faster than generic platforms because they address specific, well-understood problems.

4. AI Infrastructure and Tools

The infrastructure layer of the AI stack presents enormous opportunities. Model orchestration platforms, AI development tools, data labeling services, and AI monitoring solutions are all experiencing rapid growth. Companies like Databricks that help organizations connect AI to their own data are becoming essential infrastructure providers. The AI chip market alone is projected to exceed $931 billion by 2034.

Organizations building AI infrastructure benefit from the platform effect—their tools become more valuable as more developers use them. This creates durable competitive advantages and recurring revenue streams that are attractive to investors.

Case Studies and Success Stories

Case Study 1: Nasdaq AI Platform

Nasdaq, one of the world’s premier stock exchanges and leading financial technology platforms, built an AI platform to optimize its internal operations and enhance its external products. The implementation helped improve functionality and user experience while streamlining internal work processes. By leveraging AI for market surveillance, data analysis, and operational efficiency, Nasdaq demonstrated how traditional financial institutions can harness AI to maintain competitive advantage in a rapidly evolving market.

The Nasdaq case illustrates several success factors for enterprise AI: executive sponsorship, clear use case definition, integration with existing systems, and continuous measurement of business impact. The company started with specific, high-value applications before expanding to broader AI adoption.

Case Study 2: FanDuel AI Chatbot

FanDuel generated millions of impressions with a Charles Barkley AI-powered chatbot, demonstrating the marketing potential of generative AI. The campaign combined celebrity personality with AI conversational capabilities to create engaging customer interactions at scale. This success story illustrates how consumer brands can leverage AI to create personalized, interactive marketing experiences that drive engagement and brand awareness.

The FanDuel example shows how AI can extend brand reach while maintaining authenticity. By training the AI on Charles Barkley’s actual speech patterns and personality, FanDuel created an experience that felt genuine rather than artificial. This approach to AI-powered marketing is being adopted across industries.

Case Study 3: K&L Wines AI SKU Matching

K&L Wine Merchants saved 14+ hours daily with 99% accurate AI SKU matching, demonstrating AI’s potential for operational efficiency in retail. The system automated the previously manual process of matching wine SKUs across different databases and suppliers, eliminating errors and freeing staff to focus on customer service and curation. This case study shows how even specialized retailers can achieve significant ROI from targeted AI implementations.

The K&L Wines implementation succeeded because it addressed a specific, painful problem with a clear solution. Rather than trying to transform the entire business with AI, the company focused on one high-impact use case and executed it well. This targeted approach is often more successful than broad AI initiatives.

Case Study 4: Consumer Reports AI Search

Consumer Reports vectorized 90 years of trusted data into an AI search experience, making decades of research accessible through natural language queries. The implementation transformed how users interact with the organization’s extensive product testing database, improving information discovery and user satisfaction. This example demonstrates how legacy organizations can leverage AI to unlock the value of historical data assets.

The Consumer Reports case shows how AI can modernize established brands without disrupting their core value proposition. The AI search tool makes existing content more accessible rather than replacing the trusted testing methodology that defines the brand. This approach to AI augmentation rather than replacement is a model for traditional organizations.

Future Outlook and Predictions

The AI 2027 project, developed by researchers with experience at OpenAI and informed by expert feedback and forecasting methodologies, predicts that superhuman AI will have enormous impact over the next decade, exceeding that of the Industrial Revolution. The CEOs of OpenAI, Google DeepMind, and Anthropic have all predicted that artificial general intelligence (AGI) will arrive within the next 5 years.

By 2027, powerful AI systems are expected to become smarter than humans in many domains, potentially wreaking havoc on the global order or creating unprecedented prosperity, depending on how the technology is managed. The scenario represents one of many possible futures, but the trend toward increasingly capable AI systems is clear.

Looking to 2030, analysts project the AI market will reach $3.5 trillion, with generative AI alone creating $434 billion in annual enterprise value. The technology will likely permeate every aspect of business and daily life, from autonomous vehicles to personalized medicine to automated creative production. Organizations that establish strong AI capabilities now will be positioned to lead in this future landscape.

However, significant uncertainties remain. Regulatory frameworks, ethical guidelines, and safety protocols are still evolving. The concentration of AI capabilities in a small number of companies and countries raises geopolitical concerns. And the long-term impact of AI on employment, inequality, and human agency remains hotly debated.

The next five years will be critical for determining whether AI fulfills its promise of unprecedented prosperity or creates new forms of disruption and inequality. Organizations, policymakers, and individuals all have roles to play in shaping this future. The decisions made today about AI governance, investment, and deployment will have consequences that extend for decades.

Key Takeaways

- The global AI market reached $538 billion in 2026 with a 37.3% growth rate, projected to hit $3.5 trillion by 2033

- 72% of enterprises now have AI workloads in production, with the average company running 4.2 AI models

- Agentic AI has emerged as the fastest-growing priority, with autonomous systems beginning to outnumber human users in organizations

- AI startups captured 53% of global VC investment in 2025, with Q1 2026 setting records at $300 billion in startup funding

- Despite high adoption, over 50% of companies report no measurable value from AI investments, highlighting the implementation challenge

- NVIDIA maintains 81% market share in AI chips, but AMD is gaining ground with 10% market share

- Healthcare leads industry adoption at 25.7% of AI spending, followed by financial services and retail

- Enterprise ROI measurement is shifting from productivity metrics to direct P&L impact

- Ethics, bias, privacy, and explainability remain critical challenges requiring ongoing attention

- AGI may arrive within 5 years according to leading AI lab CEOs, potentially transforming the global economy

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- Noizz – AI Market Size 2026 Statistics: https://noizz.io/statistics/ai-market-size-2026

- Exploding Topics – AI Statistics January 2026: https://explodingtopics.com/blog/ai-statistics

- Crunchbase – Q1 2026 Venture Funding Records: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026/

- IBM – AI Tech Trends Predictions 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- PwC – 2026 AI Business Predictions: https://www.pwc.com/us/en/tech-effect/ai-analytics/ai-predictions.html

- Microsoft – 7 AI Trends to Watch in 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026/

- Deloitte – State of AI in the Enterprise 2026: https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- NVIDIA – State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026/

- ABI Research – AI Software Market Size Forecast: https://www.abiresearch.com/news-resources/chart-data/report-artificial-intelligence-market-size-global

- Companies History – AI Market Share by Company 2026: https://www.companieshistory.com/ai-market-share-by-company/

- Clarifai – Top AI Risks and Challenges 2026: https://www.clarifai.com/blog/ai-risks

- AI 2027 Forecast Project: https://ai-2027.com/

- New York Times – AI Forecast Predicts Storms Ahead: https://www.nytimes.com/2025/04/03/technology/ai-futures-project-ai-2027.html