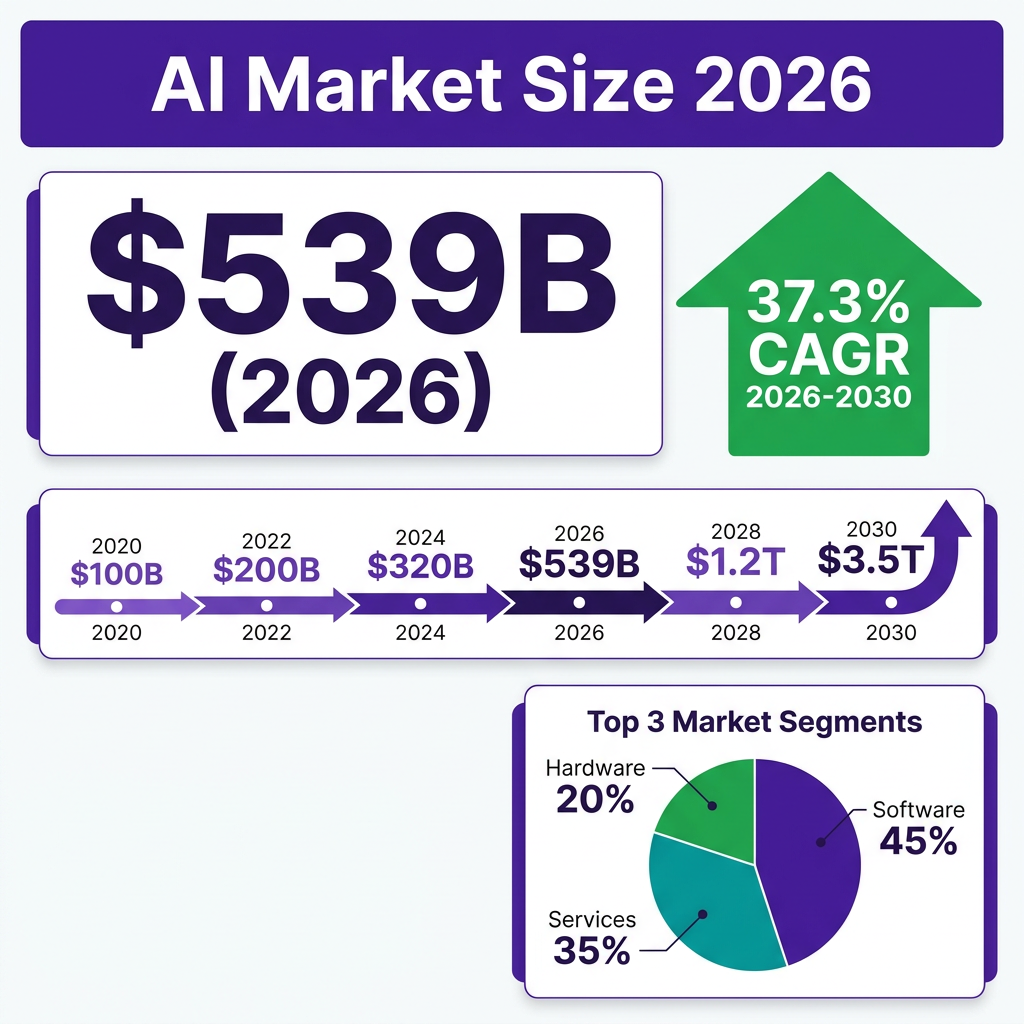

The artificial intelligence market has reached an unprecedented inflection point in 2026. What began as experimental technology just a few years ago has now become the single largest driver of technological transformation across every industry sector. The numbers tell a compelling story: the global AI market is projected to reach $539.45 billion in 2026, representing a staggering 37.3% year-over-year growth from $390.91 billion in 2025. This is not just another tech trend—it is the foundation of the next industrial revolution.

What is particularly striking about this moment is the sheer scale of capital flowing into AI. Global AI investment reached $202.3 billion in 2025, representing 50% of all venture capital deployed worldwide—a concentration unprecedented in technology investment history. OpenAI’s valuation trajectory from $157 billion to a targeted $830 billion in just fourteen months, Anthropic’s revenue explosion from $87 million to $7 billion annualized in under two years, and Nvidia’s ascent to become the world’s most valuable company at $4.4 trillion market capitalization all point to an industry operating at scales that demand rigorous examination.

Market Overview: The $539 Billion AI Ecosystem

The artificial intelligence market in 2026 represents one of the fastest-growing technology sectors in human history. According to Grand View Research, the market size was estimated at USD 390.91 billion in 2025 and is expected to reach USD 539.45 billion in 2026. This explosive growth trajectory shows no signs of slowing, with projections indicating the market will reach $3.5 trillion by 2033, growing at a compound annual growth rate (CAGR) of 37.3% from 2026 to 2033.

The market’s composition reveals important insights about where value is being created. Software dominates with approximately 45% of market share, followed by services at 35%, and hardware at 20%. This distribution reflects the maturation of AI from purely research-based endeavors into production-ready enterprise solutions. Companies are no longer just experimenting with AI—they are deploying it at scale across their operations.

Geographic distribution shows the United States maintaining a dominant position, with U.S. private AI investment reaching $285.9 billion in 2025—23.1 times China’s $12.4 billion and 48.5 times the UK’s $5.9 billion. The U.S. led with 1,953 newly funded AI companies in 2025, more than 10 times the next country (China: 161). This concentration of investment and innovation activity creates a self-reinforcing cycle that continues to accelerate American AI leadership.

The generative AI segment deserves special attention as the fastest-growing subsector. The global generative AI market reached USD 43.87 billion in 2023 and is experiencing explosive growth. Generative AI private investment grew over 200% in 2025 and captured nearly half of all private AI funding. This reflects the transformative impact of large language models and image generation technologies on content creation, software development, and creative industries.

Looking at the technology stack, deep learning and machine learning continue to dominate, but we are seeing rapid growth in natural language processing (NLP), computer vision, and emerging areas like multi-modal AI that can process text, images, audio, and video simultaneously. The function-based segmentation shows particularly strong growth in cybersecurity, finance and accounting, human resource management, legal and compliance, operations, sales and marketing, and supply chain management applications.

Key Statistics and Data Points

The AI industry’s growth is best understood through the lens of concrete data points that reveal the scale and scope of transformation occurring across the global economy. Here are the most significant statistics defining the AI landscape in 2026:

Market Size and Growth: The global AI market will generate $514.5 billion to $539.45 billion in revenue in 2026, representing a 19-37.3% jump from 2025 levels. Alternative estimates from Precedence Research suggest the market could reach $900 billion in 2026, while ABI Research projects AI software alone will reach $467 billion. The variation in estimates reflects different methodological approaches, but all sources agree on one thing: unprecedented growth.

Investment and Funding: Global AI investment hit $202.3 billion in 2025, representing 50% of all venture capital deployed worldwide. A record $40 billion AI deal lifted venture capital investment to its strongest quarter since Q1 2022. Funding to foundational AI startups doubled in Q1 2026 versus all of 2025. OpenAI, Anthropic, and xAI alone raised over $160 billion between them in the past 12 months.

Adoption Metrics: 35.49% of people now use AI tools every day, rising to 55% in marketing and sales departments of tech companies. Nearly 1.8 billion people have used some kind of AI tool. 94% of marketers plan to use AI for content creation in 2026. Companies plan to double AI spending in 2026, to approximately 1.7% of revenues. 42% of CFOs plan to increase AI investment by over 30% within two years.

Enterprise Deployment: The massive middle of the enterprise bell curve is moving from experimentation to production-grade systems. Data-center-related investment accounted for 25% of annual U.S. GDP growth in 2025. Tech megacaps are projected to invest over $300 billion in AI infrastructure. IT continued to dominate the VC ecosystem, representing 74% of investment and accounting for seven of the top 10 deals.

Developer and Technical Metrics: AI code share—the percentage of code that is AI-generated—has become a key metric for development teams. AI suggestion acceptance rates range from less than 20% (needs improvement) to 35-45% (top performers). Code churn has risen from a 3.3% baseline in 2021 to 5.7-7.1% in 2024-2025 as AI-generated code requires more refactoring.

Content and Marketing: Content velocity has increased dramatically with AI assistance. Cost per article has decreased while output volume has multiplied. Time to publish has been compressed from weeks to days. Organic traffic per post shows mixed results, with quality remaining the differentiating factor. AI citation rates in search are becoming a new metric of visibility.

Trust and Perception: Only 8.5% of people believe they can “always trust” AI Overviews when searching online. This trust gap represents both a challenge and an opportunity for companies building AI products. The organizations that solve the trust problem will capture disproportionate market share.

IPO Pipeline: A promising IPO pipeline is developing for 2026, with many AI companies reaching the scale and maturity required for public markets. This transition from private to public markets will bring new transparency, governance requirements, and valuation benchmarks to the industry.

Major Trends Shaping AI in 2026

The AI landscape in 2026 is defined by seven major trends that are reshaping how businesses and consumers interact with artificial intelligence. These trends represent the maturation of AI from experimental technology to essential infrastructure.

1. The Shift from Vibe to Value: ROI-Focused AI Deployment

The most significant trend for 2026 is the disciplined march to value. Companies are moving beyond AI experimentation and excitement to private and secure deployments with real ROI expectations. According to PwC’s AI predictions, the massive middle of the enterprise bell curve is shifting from experimentation to production-grade systems. This means AI projects now require clear business cases, measurable outcomes, and direct connections to revenue or cost savings.

Organizations are implementing orchestration layers that accelerate impact by industrializing innovation—putting ideas into production with continuous monitoring. This trend is driven by CFOs and boards demanding accountability for AI investments. The companies getting the most out of AI in 2026 are not only asking whether AI works, but how it connects directly to business outcomes across productivity, service quality, decision speed, customer experience, risk reduction, and revenue generation.

2. Agentic AI and Autonomous Systems

Agentic AI—systems that can act autonomously to accomplish complex goals—is moving from concept to reality. According to industry experts, agentic AI and other non-human identities will outnumber human users in organizations significantly in the coming years. Proof points and real-world benchmarks are setting the pace for agentic AI adoption.

These AI agents can tackle complex enterprise workflows, going beyond simple chatbots to handle multi-step processes that previously required human intervention. Examples include AI systems that can automate code migration from legacy to cloud platforms, reducing project durations by up to two years, or autonomous AI control for HVAC systems that increases comfort by 25% while reducing energy consumption by over 6%.

3. Generative AI Maturity and Specialization

Generative AI has moved beyond the hype phase into practical, specialized applications. The technology is addressing enterprise challenges through knowledge copilots that connect multiple internal data sources. Generative AI is now being deployed across marketing, supply chain, product development, legal operations, and risk management—not just IT teams.

The focus has shifted from general-purpose models to specialized solutions trained on domain-specific data. This specialization delivers better accuracy, lower costs, and improved compliance with industry regulations. Companies are discovering that smaller, fine-tuned models often outperform large general models for specific business tasks.

4. AI Infrastructure and Compute Investment Boom

The AI infrastructure market is experiencing unprecedented investment. AI firms working on IT infrastructure and hosting attracted $47.4 billion in VC investment in 2024, overtaking other industries. Data-center-related investment accounted for 25% of annual U.S. GDP growth in 2025. Tech megacaps are projected to invest over $300 billion in AI infrastructure.

This infrastructure boom reflects the reality that AI capabilities are constrained by compute availability. Companies are investing in specialized AI chips, high-performance computing clusters, and edge computing infrastructure to support AI deployment at scale. The AI chipsets market alone is projected to reach USD 931.26 billion by 2034.

5. Multi-Modal AI and Unified Interfaces

AI systems that can process and generate text, images, audio, and video simultaneously are becoming mainstream. Multi-modal AI enables more natural human-computer interaction and opens new application possibilities across creative industries, healthcare diagnostics, and autonomous systems.

This trend is particularly important for enterprise applications where information exists in multiple formats. A multi-modal AI can analyze a contract (text), review product images (vision), and listen to customer calls (audio) to provide comprehensive insights that were previously impossible to achieve with single-modality systems.

6. Edge AI and Distributed Intelligence

Moving AI processing from centralized cloud servers to edge devices is enabling real-time applications with lower latency and improved privacy. Edge AI is critical for autonomous vehicles, industrial automation, healthcare monitoring, and consumer electronics. The AI in hardware market is projected to reach USD 210.50 billion by 2034.

This distributed approach to AI reduces bandwidth requirements, improves response times, and addresses data privacy concerns by keeping sensitive information on local devices. As edge computing hardware becomes more powerful, we expect to see increasingly sophisticated AI capabilities deployed at the edge.

7. AI Regulation and Governance Frameworks

As AI becomes more powerful and pervasive, governments worldwide are implementing regulatory frameworks. The EU AI Act, various U.S. state regulations, and China’s AI governance rules are creating a complex compliance landscape. Companies must now consider regulatory requirements as a fundamental part of AI strategy.

This trend is driving investment in AI governance tools, explainability solutions, and bias detection systems. Organizations that proactively address regulatory requirements will have a competitive advantage as compliance becomes a prerequisite for market access.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a mix of established technology giants and rapidly scaling startups. Understanding the competitive landscape requires examining both the infrastructure providers building the foundation and the application companies creating user-facing solutions.

Infrastructure and Foundation Model Leaders

OpenAI remains the most prominent AI company, with a valuation trajectory from $157 billion to a targeted $830 billion in fourteen months. Their GPT models and ChatGPT product have become synonymous with generative AI for consumers and enterprises. The company’s revenue growth has been explosive, driven by API usage and premium subscriptions.

Anthropic has emerged as a major competitor, with revenue exploding from $87 million to $7 billion annualized in under two years. Their Claude models are particularly strong in reasoning tasks and long-context understanding. The company’s focus on AI safety and constitutional AI has attracted enterprise customers concerned about responsible AI deployment.

Nvidia has become the world’s most valuable company at $4.4 trillion market capitalization, cementing its position as the dominant provider of AI chips and infrastructure. Their GPUs are the standard for AI training and inference, and the company continues to innovate with specialized AI accelerators.

Google DeepMind and Microsoft represent the big tech incumbents with significant AI investments. Google’s Gemini models and Microsoft’s Copilot products demonstrate how AI is being integrated into existing productivity and search ecosystems. These companies have the advantage of massive distribution channels and existing enterprise relationships.

xAI, founded by Elon Musk, has raised substantial funding and is positioning itself as a challenger in the foundation model space. The company’s Grok model and focus on “truth-seeking” AI represents a differentiated approach to model development.

Application and Vertical AI Companies

Beyond the foundation model providers, a robust ecosystem of application-layer companies is emerging. ElevenLabs ($800M valuation) leads in voice generation software. Midjourney dominates image generation with a unique community-driven approach. Notion ($330M raised) has successfully integrated AI into productivity software.

The Forbes AI 50 list highlights the most promising AI companies, including Gamma ($91M raised) for AI graphic design tools. These companies demonstrate that significant value creation is occurring at the application layer, where AI capabilities are packaged into user-friendly products solving specific problems.

Enterprise AI companies are also gaining traction, with firms like Cohere, Adept, and Character.AI raising substantial funding to pursue specific market opportunities. The diversity of approaches reflects the breadth of AI applications across industries.

Challenges and Pain Points

Despite the tremendous growth and opportunity, the AI industry faces significant challenges that could impact its trajectory. Understanding these pain points is essential for anyone investing in or deploying AI solutions.

1. Data Quality and Management

AI systems are only as good as the data they are trained on. Data quality and data management failures represent one of the most common causes of AI project failure. Organizations struggle with data silos, inconsistent formats, missing values, and biased training datasets. The challenge is compounded by privacy regulations that limit data access and sharing.

Real-world examples illustrate the severity of this challenge. A large language model used in a U.S. courtroom cited six cases that did not exist, demonstrating how AI can generate confident but false information when trained on incomplete or erroneous data. Companies must invest in robust data pipelines, quality assurance processes, and governance frameworks to address these issues.

2. AI Talent Shortage

The demand for AI expertise far exceeds supply. AI talent shortage and delivery risk affects organizations of all sizes. Companies compete fiercely for machine learning engineers, data scientists, and AI product managers. This shortage drives up costs and can delay or derail AI initiatives.

The talent gap extends beyond technical roles. Organizations also need professionals who can bridge the gap between AI capabilities and business requirements—translating technical possibilities into practical applications. This combination of technical and domain expertise is particularly scarce.

3. Hallucinations and Reliability

AI systems, particularly large language models, are prone to generating confident but false information—a phenomenon known as hallucinations. This creates risks in legal, medical, and financial applications where accuracy is critical. Human review for high-stakes outputs adds cost and latency, partially offsetting the efficiency benefits of AI automation.

The reliability challenge extends to model consistency. AI systems may produce different outputs for similar inputs, making it difficult to integrate them into deterministic business processes. Organizations must develop monitoring systems and fallback procedures to manage these reliability issues.

4. Security and Privacy Risks

AI systems introduce new security and privacy risks. Sensitive training data can be extracted from models through prompt injection attacks. External cyberattacks can manipulate model outputs. Data breaches expose not just traditional information but also the intellectual property embedded in AI models.

Privacy-first data practices and access controls are essential, but implementing them while maintaining model performance is challenging. Organizations must balance the benefits of AI personalization against privacy requirements and customer expectations.

5. Integration and Scalability

Moving AI from pilot projects to production at scale presents significant challenges. Integration failures occur when AI systems do not connect properly with existing enterprise systems and workflows. Scalability issues emerge when models that performed well in controlled environments struggle with real-world data volumes and variety.

Many organizations find that pilot projects refuse to scale due to data pipeline limitations, computational costs, or maintenance requirements. The gap between proof-of-concept and production deployment remains a major bottleneck in AI adoption.

6. Ethical, Legal, and Bias Risks

AI systems can perpetuate or amplify biases present in training data, leading to unfair outcomes in hiring, lending, and criminal justice applications. Algorithmic bias and discrimination represent significant reputational and legal risks for organizations deploying AI.

The lack of transparency and explainability—the “black box” problem—makes it difficult to understand why AI systems make particular decisions. This creates compliance challenges in regulated industries and undermines trust among users and stakeholders. Intellectual property and copyright questions around AI-generated content remain unresolved in many jurisdictions.

Opportunities and Growth Strategies

Despite the challenges, the AI market presents enormous opportunities for companies that can execute effectively. Here are the key growth strategies that are driving success in 2026:

1. Vertical AI Solutions

Companies are finding success by building AI solutions tailored to specific industries rather than horizontal platforms. Vertical AI addresses the unique data, workflows, and compliance requirements of sectors like healthcare, finance, legal, and manufacturing. These specialized solutions deliver better results than general-purpose AI and command premium pricing.

For example, AI systems designed specifically for pharmaceutical research can accelerate drug discovery by predicting molecular properties and identifying promising compounds. Legal AI can review contracts, conduct due diligence, and predict litigation outcomes with greater accuracy than general models. The vertical approach creates defensible competitive positions and deep customer relationships.

2. AI-Native Business Models

The most successful AI companies of 2026 are those built from the ground up around AI capabilities rather than retrofitting AI into existing products. These AI-native businesses can deliver experiences and economics that traditional competitors cannot match.

Examples include companies like Sanofi with their “AI-first” business model featuring over 1,300 use cases that accelerate development cycles. AI-native companies can automate processes that require human judgment in traditional organizations, creating structural cost advantages and faster execution.

3. AI Infrastructure and Tooling

The picks-and-shovels play in AI remains attractive. Companies providing the infrastructure, tools, and platforms that enable AI development and deployment are seeing strong demand. This includes cloud providers offering GPU instances, MLOps platforms, data labeling services, and AI safety tools.

As AI deployment scales, the need for robust infrastructure becomes critical. Companies that can solve the challenges of model monitoring, versioning, A/B testing, and rollback will capture significant value. The infrastructure layer benefits from the broad growth of AI regardless of which specific applications succeed.

4. Human-in-the-Loop AI

Rather than pursuing full automation, many successful AI implementations combine machine capabilities with human judgment. Human-in-the-loop AI systems use AI to handle routine cases while escalating complex or high-stakes decisions to human experts.

This approach addresses reliability and trust concerns while still delivering significant efficiency gains. It also creates better feedback loops for model improvement, as human corrections can be incorporated into training data. The hybrid model is particularly effective in healthcare, legal, and financial applications where errors carry high costs.

Case Studies and Success Stories

Real-world examples demonstrate how AI is delivering measurable business impact across industries. The World Economic Forum highlighted 32 AI case studies with documented business impact, showing the breadth of successful AI deployment.

Case Study 1: EXL Services – Automated Code Migration

Challenge: EXL Services needed to migrate legacy systems to cloud infrastructure, a process that typically takes years and costs millions.

Solution: By automating code migration using AI agents, EXL reduced project durations by up to two years. The AI system analyzed legacy code, identified dependencies, and generated cloud-native equivalents while preserving business logic.

Results: The automated approach delivered massive time and cost savings while reducing the risk of errors during migration. This case demonstrates how AI can tackle complex technical challenges that were previously addressed only through manual effort.

Case Study 2: Siemens – AI-Powered HVAC Automation

Challenge: Siemens sought to optimize building energy consumption while maintaining occupant comfort.

Solution: Siemens implemented autonomous AI control for HVAC systems that continuously adjusts settings based on occupancy, weather, and building thermal properties.

Results: The AI system increased comfort by 25% while simultaneously reducing energy consumption by over 6%. This dual improvement—better outcomes at lower cost—exemplifies the promise of AI optimization in physical systems.

Case Study 3: CATL – Battery Cell Design Optimization

Challenge: CATL, a leading battery manufacturer, needed to accelerate the design of new battery cells for electric vehicles.

Solution: CATL implemented a physics-informed and agentic AI platform for EV battery cell design. The system combines physical modeling with machine learning to predict performance and optimize designs.

Results: The AI platform reduced prototype cycles by almost 50%, dramatically accelerating time-to-market for new battery technologies. This case shows how AI can transform R&D processes in manufacturing industries.

Case Study 4: Hitachi Rail – Predictive Maintenance

Challenge: Hitachi Rail needed to reduce delays and maintenance costs for rail operations.

Solution: Hitachi implemented an AI-powered digital asset management platform for rail operations and maintenance. The system analyzes sensor data from trains and tracks to predict failures before they occur.

Results: The AI analytics platform reduced delays and lowered maintenance costs by enabling proactive rather than reactive maintenance. This application of AI in transportation demonstrates the potential for predictive capabilities in asset-intensive industries.

Future Outlook and Predictions (2026-2030)

The AI market’s trajectory suggests continued explosive growth through the end of the decade. Multiple forecasts converge on a market size of approximately $3.5 trillion by 2033, representing a compound annual growth rate of 37.3% from 2026. However, the path to this future is subject to significant uncertainty and debate among experts.

Near-Term Outlook (2026-2027)

The CEOs of OpenAI, Google DeepMind, and Anthropic have all predicted that AGI (Artificial General Intelligence) will arrive within the next 5 years. The AI 2027 scenario predicts that by early 2027, AI will be a superhuman coder, and by mid-2027, it will be a superhuman AI researcher capable of recursive self-improvement.

More conservatively, we expect 2026-2027 to bring continued maturation of enterprise AI deployment, with the majority of Fortune 500 companies having production AI systems in place. The focus will shift from model capabilities to operational efficiency, cost optimization, and responsible AI governance.

Medium-Term Projections (2027-2028)

By 2027-2028, we anticipate significant consolidation in the AI industry. The current proliferation of foundation models will likely give way to a smaller number of dominant platforms, similar to how the cloud computing market consolidated around AWS, Azure, and Google Cloud.

Regulatory frameworks will mature, creating clearer rules for AI deployment across jurisdictions. This regulatory clarity will both constrain certain applications and enable others by providing compliance roadmaps. Companies that have invested in AI governance will be well-positioned for this environment.

Long-Term Vision (2028-2030)

Looking toward 2030, the AI 2030 scenarios report from the UK government highlights the significant uncertainty surrounding AI development. Scenarios range from continued steady progress to rapid acceleration if breakthroughs in reasoning, planning, or scientific discovery occur.

By 2030, AI is likely to be deeply embedded in virtually every aspect of business and daily life. Healthcare predictions suggest AI will enable earlier detection and diagnosis of leading causes of disease, with substantial uptake of at-home health monitoring tools by individuals and healthcare systems.

The economic impact could be transformative. AI has the potential to add trillions to global GDP through productivity gains, new product categories, and improved decision-making. However, realizing this potential will require addressing the challenges of workforce transition, inequality, and governance.

Key Takeaways

- The global AI market is projected to reach $539.45 billion in 2026, growing at 37.3% CAGR to reach $3.5 trillion by 2033

- Global AI investment hit $202.3 billion in 2025, representing 50% of all venture capital deployed worldwide

- Seven major trends define AI in 2026: ROI-focused deployment, agentic AI, generative AI maturity, infrastructure investment, multi-modal AI, edge computing, and regulation

- Key players include OpenAI (targeting $830B valuation), Anthropic ($7B annualized revenue), Nvidia ($4.4T market cap), and emerging vertical AI specialists

- Major challenges include data quality, talent shortage, hallucinations, security risks, integration complexity, and ethical concerns

- Successful growth strategies focus on vertical solutions, AI-native

business models, infrastructure plays, and human-in-the-loop implementations - Real-world case studies demonstrate measurable ROI: 2-year project reductions, 25% comfort improvements, 50% prototype cycle reductions

- The future outlook suggests continued explosive growth with the potential for AGI within 5 years according to leading AI CEOs

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- Precedence Research – AI Market Size and Trends 2026-2035: https://www.precedenceresearch.com/artificial-intelligence-market

- Thunderbit – AI Growth 2026 Key Statistics: https://thunderbit.com/blog/ai-growth-key-statistics

- Noizz – AI Market Size 2026: https://noizz.io/statistics/ai-market-size-2026

- TechDogs – Top 20 AI Statistics 2026: https://www.techdogs.com/td-articles/stats/ai-statistics

- Lead with AI – 100+ AI Statistics and Trends 2026: https://www.leadwithai.co/guides/ai-statistics

- France Epargne – State of AI 2026: https://www.france-epargne.fr/research/en/state-of-ai-entering-2026

- IBM – AI Tech Trends Predictions 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- PwC – 2026 AI Business Predictions: https://www.pwc.com/us/en/tech-effect/ai-analytics/ai-predictions.html

- Waveup – Top VCs Investing in AI 2026: https://waveup.com/blog/top-vc-investing-in-ai

- Crunchbase – Q1 2026 Record Breaking Funding: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026

- Forbes AI 50 List 2026: https://www.forbes.com/lists/ai50

- World Economic Forum – AI Case Studies: https://www.cio.com/article/4122937/davos-from-hype-to-ai-transformation-in-the-economy.html

- Simplilearn – Top 15 Challenges of AI 2026: https://www.simplilearn.com/challenges-of-artificial-intelligence-article

- Clarifai – Top AI Risks and Challenges 2026: https://www.clarifai.com/blog/ai-risks

Regional AI Market Analysis

The global AI market shows significant regional variations in adoption, investment, and regulatory approaches. Understanding these differences is crucial for companies seeking to expand their AI operations internationally.

North America: The AI Powerhouse

North America, led by the United States, continues to dominate the global AI landscape. The region accounts for the majority of global AI investment, with U.S. private AI investment reaching $285.9 billion in 2025. The concentration of leading AI companies, top-tier research universities, and abundant venture capital creates an ecosystem that is difficult to replicate elsewhere.

Silicon Valley remains the epicenter of AI innovation, hosting the headquarters of OpenAI, Anthropic, Google DeepMind, and numerous other leading companies. However, other U.S. cities including Seattle, New York, and Boston have developed significant AI clusters. Canada’s AI ecosystem, centered around Toronto and Montreal, benefits from strong government support and world-class research institutions.

The U.S. approach to AI regulation has been relatively light-touch compared to other regions, prioritizing innovation while addressing specific risks through sectoral regulations. This regulatory environment has attracted significant investment, though concerns about long-term safety and ethics continue to drive policy discussions.

China: The Rising Challenger

China represents the second-largest AI market globally, with private AI investment of $12.4 billion in 2025. While significantly smaller than U.S. investment in absolute terms, China’s AI development is notable for its strategic focus and government support. The Chinese government has made AI a national priority, with substantial funding and policy support for domestic AI companies.

Chinese AI companies have achieved significant capabilities in areas like computer vision, facial recognition, and natural language processing for Chinese language. Companies like Baidu, Alibaba, and Tencent are investing heavily in AI research and development. However, Chinese AI companies face challenges in accessing advanced semiconductors due to export restrictions, potentially limiting their ability to train the largest foundation models.

China’s approach to AI regulation emphasizes state control and social stability. The government’s AI governance framework requires algorithmic transparency and enables regulatory oversight of AI systems. This approach differs significantly from Western regulatory philosophies and creates distinct compliance requirements for companies operating in China.

Europe: Regulation-First Approach

Europe’s AI market is characterized by strong regulatory leadership. The EU AI Act, passed in 2024, represents the world’s most comprehensive AI regulation. The Act categorizes AI systems by risk level and imposes strict requirements on high-risk applications. This regulation-first approach has influenced AI policy discussions globally.

European AI investment lags behind the U.S. and China, with UK private AI investment at $5.9 billion in 2025. However, Europe has strengths in specific AI domains including robotics, industrial AI, and AI for sustainability. European research institutions continue to produce significant AI research, though commercialization often occurs elsewhere.

The European approach prioritizes human rights, privacy, and transparency in AI development. While this may slow deployment in some areas, it also creates opportunities for companies specializing in explainable AI, privacy-preserving machine learning, and AI auditing tools.

Emerging Markets

Emerging markets represent significant growth opportunities for AI adoption. Countries like India, Brazil, and Southeast Asian nations are investing in AI infrastructure and education. These markets often leapfrog traditional technology adoption patterns, moving directly to AI-enabled solutions without legacy infrastructure constraints.

India, in particular, has emerged as a significant player in AI services and talent. The country’s large English-speaking population and strong technical education system make it an attractive location for AI research and development centers. Indian AI startups are increasingly addressing both domestic and global markets.

AI Industry Segmentation Deep Dive

The AI market can be analyzed through multiple segmentation lenses, each revealing different insights about where value is being created and captured.

By Technology Type

Machine Learning remains the largest technology segment, encompassing supervised learning, unsupervised learning, and reinforcement learning applications. ML powers recommendation systems, fraud detection, demand forecasting, and countless other business applications. The maturity of ML tools and frameworks has made this technology accessible to a broad range of organizations.

Natural Language Processing (NLP) has experienced explosive growth following the success of large language models. NLP applications include chatbots, sentiment analysis, document summarization, and translation. The 2026 NLP market is characterized by rapid capability improvements and decreasing costs per token processed.

Computer Vision enables machines to interpret and understand visual information. Applications include facial recognition, autonomous vehicles, medical imaging, and quality control in manufacturing. The computer vision market benefits from the proliferation of cameras and image sensors across devices.

Generative AI is the fastest-growing technology segment, with applications in content creation, code generation, and design. Generative AI private investment grew over 200% in 2025, capturing nearly half of all private AI funding. The technology’s ability to create novel content rather than just analyze existing data represents a qualitative shift in AI capabilities.

Robotic Process Automation (RPA) combined with AI creates intelligent automation solutions that can handle complex, judgment-based tasks. This segment is particularly strong in financial services, healthcare administration, and back-office operations.

By Industry Vertical

Healthcare AI represents one of the most promising and challenging application areas. AI systems are being deployed for drug discovery, medical imaging analysis, personalized treatment recommendations, and administrative automation. The healthcare AI market is projected to reach $148 billion by 2030, driven by the need to improve outcomes while controlling costs.

Financial Services AI has mature applications in fraud detection, algorithmic trading, credit scoring, and customer service. Banks and insurance companies were among the earliest adopters of AI and continue to invest heavily. The sector’s focus on risk management drives demand for explainable AI solutions.

Retail and E-commerce AI powers recommendation engines, demand forecasting, inventory optimization, and personalized marketing. The competitive pressure in retail drives continuous innovation in AI applications. Visual search and virtual try-on technologies are emerging growth areas.

Manufacturing AI enables predictive maintenance, quality control, supply chain optimization, and autonomous robotics. Industrial AI applications often require edge computing capabilities to process data in real-time on the factory floor.

Transportation and Logistics AI includes autonomous vehicles, route optimization, and demand prediction. While fully autonomous passenger vehicles remain elusive, AI is being deployed in constrained environments like mining, agriculture, and highway trucking.

AI Talent and Workforce Implications

The rapid growth of the AI market has created unprecedented demand for AI talent, with significant implications for the broader workforce.

The AI talent shortage affects organizations of all sizes. Companies compete fiercely for machine learning engineers, data scientists, AI product managers, and AI ethicists. This shortage has driven compensation packages to record levels, with top AI researchers commanding salaries exceeding $1 million annually at leading companies.

Beyond technical roles, organizations need professionals who can bridge the gap between AI capabilities and business requirements. These “AI translators” understand both the technical possibilities and the practical constraints of business operations. This combination of skills is particularly scarce and valuable.

The workforce implications extend beyond the AI industry itself. AI automation is transforming job roles across industries, eliminating some tasks while creating new opportunities. The World Economic Forum predicts that AI will displace 85 million jobs by 2025 while creating 97 million new ones. The net positive outlook masks significant transition challenges for displaced workers.

Reskilling and upskilling initiatives are becoming critical organizational capabilities. Companies that invest in training their existing workforce for AI-augmented roles will have a competitive advantage in talent retention and operational flexibility. Educational institutions are racing to adapt curricula to prepare students for an AI-enabled economy.

Conclusion: The AI Transformation Is Just Beginning

The artificial intelligence market in 2026 represents a pivotal moment in technological history. With a market size of $539 billion and growth projections reaching $3.5 trillion by 2033, AI is not merely another technology trend—it is the foundational infrastructure of the next industrial revolution.

The scale of investment tells the story: $202 billion in global AI investment, representing half of all venture capital deployed worldwide. Companies like OpenAI, Anthropic, and Nvidia have achieved valuations and revenue growth that would have been unimaginable just a few years ago. This capital deployment reflects genuine conviction that AI will transform virtually every aspect of business and society.

Yet for all the progress, we remain in the early stages of AI adoption. The shift from experimentation to production deployment is just beginning for most enterprises. The challenges of data quality, talent shortage, reliability, and governance remain significant but solvable. Companies that address these challenges systematically will capture disproportionate value.

The seven trends shaping AI in 2026—ROI-focused deployment, agentic AI, generative AI maturity, infrastructure investment, multi-modal AI, edge computing, and regulation—point toward a future where AI is deeply embedded in organizational processes and daily life. The companies and individuals who understand and adapt to these trends will thrive in the AI-enabled economy.

Looking ahead, the AI market’s trajectory suggests continued explosive growth with the potential for transformative breakthroughs. Whether or not AGI arrives within the next five years as some predict, the AI capabilities already in development will reshape industries, create new business models, and change how we work and live.

The AI market analysis for 2026 reveals both tremendous opportunity and significant responsibility. As we build this technology at unprecedented scale, we must also address the challenges of bias, privacy, security, and economic disruption. The organizations that succeed will be those that harness AI’s potential while managing its risks—a balance that will define the winners in the AI era.