The artificial intelligence market has reached an inflection point in 2026. What began as experimental technology has transformed into a $539 billion global industry that is fundamentally reshaping how businesses operate, compete, and create value. With 88% of organizations worldwide now using AI in at least one business function—up from just 55% in 2023—the technology has moved from the periphery to the center of corporate strategy. This shift represents one of the most rapid technology adoptions in business history, comparable to the internet’s commercialization in the 1990s but occurring at an even faster pace.

This isn’t just another technology trend. The AI market is growing at a compound annual growth rate of 19-29%, with projections indicating it will reach $757 billion by 2027 and an astounding $1.675 trillion by 2031. To put this in perspective, that’s a 17.7× expansion from the $94.8 billion market size recorded in 2020. The implications are staggering: AI’s share of new unicorn births has surged from 6% in 2015 to 53% in 2025, and venture capital investment in AI startups now accounts for the majority of global VC dollars. For business leaders, investors, and technology professionals, understanding the AI market landscape is no longer optional—it’s essential for staying competitive in an increasingly AI-driven economy.

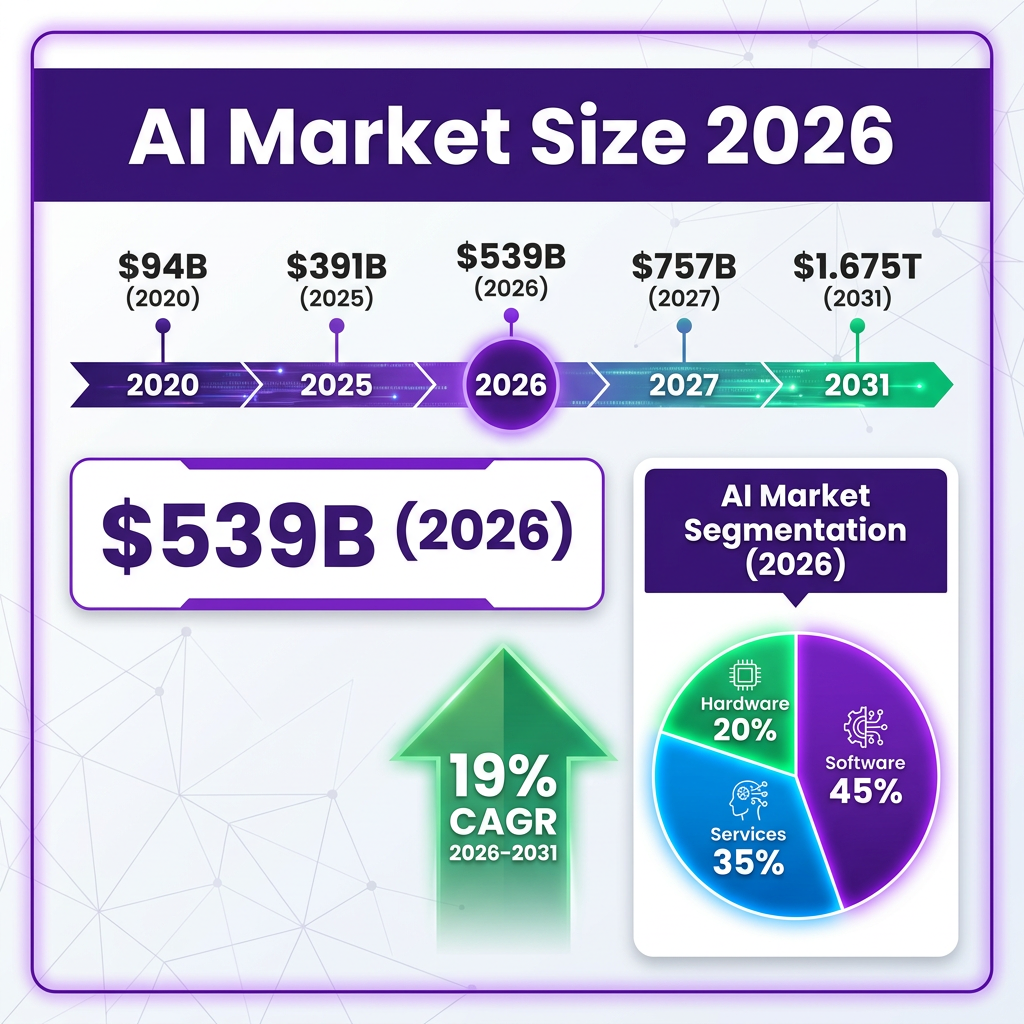

Market Overview: The $539 Billion AI Ecosystem

The global artificial intelligence market has experienced unprecedented expansion, with the market size estimated at $390.91 billion in 2025 and expected to reach $539.45 billion in 2026. This represents year-over-year growth of approximately 38%, making AI one of the fastest-growing technology sectors in history. The trajectory shows no signs of slowing, with multiple research firms projecting sustained double-digit growth through the end of the decade and beyond. By 2031, Statista Market Insights forecasts the AI market will reach $1.675 trillion—a remarkable expansion that underscores the technology’s transformative potential.

Several interconnected factors are driving this explosive growth. First, enterprise adoption has accelerated dramatically as organizations move beyond the experimental phase. Companies are no longer asking whether to implement AI but how to scale it effectively across their operations to drive measurable business outcomes. Second, the technology itself has matured significantly—large language models, computer vision systems, and predictive analytics tools have reached production-grade reliability, making them suitable for mission-critical applications. Third, the cost of AI implementation has decreased substantially while accessibility has increased, democratizing access to capabilities that were once reserved for tech giants with massive R&D budgets.

The market is segmented across multiple dimensions, each telling a different story about how AI is being deployed and monetized. By component, software dominates with approximately 45% of market share, followed by services at 35% and hardware at 20%. The software segment includes AI platforms, applications, and development tools that enable organizations to build and deploy AI solutions. The services segment encompasses consulting, implementation, and managed services that help enterprises navigate the complexities of AI adoption. The hardware segment, while smaller in percentage terms, is experiencing explosive growth as demand for AI-optimized chips, servers, and data center infrastructure surges.

NVIDIA, the dominant player in AI hardware, controls an estimated 81% of the AI data center chip market. The company posted $44.1 billion in Q1 FY2026 revenue—a staggering 69% year-over-year jump—with data center sales making up 90% of total revenue. This performance reflects the insatiable demand for GPU computing power needed to train and run large AI models. AMD has emerged as the primary challenger, with its MI300X accelerator capturing roughly 10% of the AI accelerator market by 2026, up from about 5% in 2024. The hardware market dynamics illustrate how AI is reshaping the entire technology stack, from silicon to software.

By technology type, machine learning and deep learning continue to lead in terms of overall market size, but generative AI has emerged as the fastest-growing segment. The global generative AI market, valued at $22.2 billion in 2025, is projected to reach $29.6 billion in 2026 and $324.7 billion by 2033, representing a CAGR of approximately 35-43% depending on the research firm. This segment alone is attracting disproportionate investment and attention, with generative AI use cases projected to create $434 billion in annual value for enterprises by 2030. The applications span content creation, code generation, drug discovery, customer service, and countless other use cases that were unimaginable just a few years ago.

Geographically, the United States maintains clear market leadership, with the U.S. AI market valued at $146.09 billion in 2024 and projected to reach approximately $851.46 billion by 2034, growing at a CAGR of 19.33%. More than 80% of global private investment in AI flows to U.S. firms, underscoring the country’s dominance as an AI funding destination. This concentration reflects the strength of U.S. technology companies, the depth of venture capital markets, and the availability of top AI research talent. China ranks second globally, with the two countries accounting for over half of all AI VC deals worldwide. Chinese AI companies have made significant strides, with models like DeepSeek-R1 demonstrating capabilities competitive with Western offerings. Europe is accelerating its AI capabilities, with the EU AI Act providing a comprehensive regulatory framework that aims to balance innovation with safety and ethical considerations.

Key Statistics and Data Points

The numbers behind the AI market tell a compelling story of rapid transformation and massive economic opportunity. Here are the critical statistics that define the AI landscape in 2026, organized by category for clarity:

Market Size and Growth Metrics: The global AI market reached $514.5 billion in revenue in 2026, representing a 19% increase from $390.9 billion in 2025. Between 2024 and 2032, the market is expected to grow at a CAGR of 29.2% according to Exploding Topics research. The generative AI segment is growing even faster, with a projected CAGR of 43.4% that will take it to $890.59 billion by 2032 according to MarketsandMarkets. Looking further ahead, the AI market is projected to reach $1.675 trillion by 2031—a 17.7× expansion from the $94.81 billion recorded in 2020.

Enterprise Adoption Statistics: 88% of organizations worldwide now use AI in at least one business function, up from 55% in 2023—a remarkable 33-percentage-point jump in just two years. This adoption rate varies by industry, with technology companies leading at over 90% and traditional industries like manufacturing and healthcare following but catching up rapidly. 35.49% of people now use AI tools every day in their personal or professional lives, and nearly 1.8 billion people globally have used some kind of AI tool. In marketing and sales departments of tech companies specifically, AI adoption reaches 55%, demonstrating how knowledge work is being transformed.

Investment and Funding Data: Global annual value of VC investments in AI firms rose dramatically from approximately $8.3 billion in 2012 to $258.7 billion in 2025 according to OECD data. AI startups now attract a majority of global VC dollars at 53%, meaning AI receives more venture funding than all other technology categories combined. Combined Big Tech AI spending is projected at $725 billion in 2026, covering infrastructure, research, and talent acquisition. Tech megacaps including Microsoft, Google, Amazon, and Meta are expected to invest over $300 billion collectively in AI infrastructure alone.

Company-Specific Performance Metrics: OpenAI, the creator of ChatGPT, grew from $1 billion revenue in 2023 to $3.7 billion in 2024—a 270% increase that likely represents the fastest growth rate ever achieved by a company at that scale. The company is projected to reach $12.7 billion in revenue in 2025 and potentially $100 billion by 2027. NVIDIA controls 81% of the AI data center chip market, with AMD holding roughly 10% and other players including Intel and custom chip makers making up the remainder. ChatGPT’s share of global AI chatbot traffic dropped from 87% in January 2025 to 64-68% by January 2026 as competition from Google Gemini, Anthropic Claude, and other alternatives intensified.

Economic Impact Projections: AI is projected to add $15.7 trillion to the global economy by 2030 according to PwC analysis, making it one of the most significant economic opportunities in history. Organizations using AI for over three years document a 25% reduction in cost per contact in customer service operations, with a 30% drop for those applying generative AI to one or two customer service use cases. In the telecommunications industry, 99% of respondents in NVIDIA’s State of AI survey said AI helped improve employee productivity, with a quarter reporting major or significant improvement.

Regional Market Distribution: The United States captures over 80% of global private AI investment, reflecting the concentration of leading AI companies and venture capital firms. The U.S. AI market specifically is projected to reach $851.46 billion by 2034. China and the U.S. together account for over half of worldwide AI VC deals, with China investing heavily in AI as a national strategic priority. The UK, Canada, and Israel follow as significant AI investment destinations, each with strong research universities and startup ecosystems.

Technology Segment Breakdown: The AI software market is structured into six technology categories: machine learning, natural language processing, computer vision, speech recognition, robotics, and expert systems. IT infrastructure and hosting have attracted the most VC investment since 2023, jumping to $47.4 billion in 2024 as cloud providers expand their AI capabilities. Marketing, advertising, and creative applications accounted for 46% of enterprise value creation from generative AI in 2023, highlighting the immediate commercial impact of content-generation capabilities.

Workforce and Usage Statistics: AI is reshaping job markets globally, with 35.49% of people using AI tools daily according to Exploding Topics research. The technology is creating new roles including AI trainers, prompt engineers, and AI ethics specialists while automating routine tasks in other positions. Skills gaps remain a primary barrier to AI implementation, cited by over half of organizations surveyed by Gallagher in their 2026 AI Adoption and Risk Survey. The demand for AI talent far outstrips supply, driving up salaries and creating recruitment challenges for organizations of all sizes.

Major Trends Shaping AI in 2026

The AI landscape is evolving at a breathtaking pace, with several key trends defining the market in 2026. These trends reflect both technological advances and shifting business priorities as organizations move from experimentation to production-grade AI deployment at scale.

1. The Agentic AI Surge: Autonomous agents and agentic AI have surged 31.5% year-over-year as a top technology priority, claiming the #1 spot for 17.1% of IT decision-makers according to Futurum Group research. These AI systems can act independently, making decisions and taking actions without human intervention for each individual step. Unlike traditional AI tools that respond to specific prompts, agentic AI can pursue goals over extended periods, breaking complex tasks into subtasks and executing them autonomously. The shift from passive AI tools to active AI agents represents a fundamental change in how businesses deploy artificial intelligence, enabling automation of complex workflows that previously required human judgment and intervention.

2. Enterprise Production Shift: Organizations are decisively moving from AI experimentation to production-grade deployments with real ROI expectations. As David Lanstein, Cofounder and CEO of Atolio, told IBM Think: “The most significant trend we see emerging next year is the shift from AI experimentation and excitement to private and secure deployments with real ROI expectations within enterprises.” Companies are no longer satisfied with pilot projects and proofs-of-concept; they demand measurable business outcomes, quantitative ROI measurement, and seamless integration with existing enterprise systems. This shift is driving demand for enterprise-grade AI platforms that offer security, compliance, and reliability.

3. Reasoning Models Rise: The emergence of reasoning models from Chinese frontier labs like DeepSeek-R1 has taken the market by storm, challenging the assumption that Western companies have an insurmountable lead in AI capabilities. These models can think through problems step-by-step, showing their work and providing more reliable outputs for complex tasks requiring logic and analysis. The competition in reasoning capabilities is intensifying, with OpenAI’s o-series models, Google’s Gemini, and Chinese labs all racing to develop more sophisticated reasoning systems. This trend promises to make AI more trustworthy for high-stakes applications in fields like law, medicine, and engineering.

4. AI Superfactories: Microsoft and other technology giants are building linked AI “superfactories”—global networks of data centers optimized specifically for AI workloads. As Microsoft explains, “Next year will see the rise of flexible, global AI systems—a new generation of linked AI superfactories—that will drive down costs and improve efficiency.” These facilities represent massive capital investments in the billions of dollars and will enable the next generation of AI capabilities by providing the computational infrastructure needed to train and run increasingly large models. The infrastructure race is accelerating globally, with significant implications for energy consumption, data sovereignty, and competitive advantage.

5. Private and Secure Deployments: Enterprises are increasingly prioritizing data privacy and security in their AI implementations. The shift toward on-premise and private cloud AI deployments reflects growing concerns about data sovereignty, regulatory compliance, and competitive advantage. Organizations want the benefits of AI—automated analysis, content generation, predictive insights—without exposing sensitive proprietary data to third-party systems or public APIs. This trend is driving demand for private AI infrastructure, on-premise large language models, and hybrid deployment options that balance performance with security.

6. Multimodal Competition: AI systems that can process and generate multiple types of content—text, images, audio, video, and code—are becoming the new standard rather than a premium feature. The competition in multimodal AI is intensifying, with models like GPT-5, Claude 4, Gemini Ultra, and open-source alternatives all expanding their capabilities beyond text. This trend is opening entirely new use cases in creative industries, healthcare imaging, autonomous vehicles, and education. The ability to work across modalities makes AI more versatile and accessible to users who think visually or prefer voice interaction.

7. Vibe Coding and Personal Software: The concept of “vibe coding”—using AI to create software through natural language descriptions rather than traditional programming—is moving from prototypes into production environments. Non-technical users can now build custom applications, automations, and tools without learning to code in Python, JavaScript, or other languages. This democratization of software development is creating a new category of “personal software” tailored to individual needs and workflows. As one analyst noted, “Vibecoding and personal software will move from prototypes into production across non-technical enterprise functions and bespoke consumer apps.”

Key Players and Competitive Landscape

The AI market is dominated by a mix of established technology giants and well-funded emerging startups, each competing across different layers of the AI stack—from specialized hardware infrastructure to end-user applications.

NVIDIA: The undisputed leader in AI hardware, NVIDIA controls an estimated 81% of the AI data center chip market according to IDC. The company’s GPUs have become the standard for training and running AI models, with its CUDA software ecosystem creating significant switching costs for customers. With Q1 FY2026 revenue of $44.1 billion (up 69% YoY) and data center sales comprising 90% of total revenue, NVIDIA’s market position appears unassailable in the near term. The company’s H100 and newer Blackwell chips are the workhorses of the AI revolution, powering everything from OpenAI’s GPT models to enterprise custom deployments. NVIDIA’s dominance extends beyond hardware to software platforms, networking equipment, and AI development tools.

OpenAI: The creator of ChatGPT remains the most prominent AI startup globally, with revenue growing from $1 billion in 2023 to $3.7 billion in 2024—a 270% increase that represents likely the fastest growth rate ever achieved by a company at that scale. The company is projected to reach $12.7 billion in revenue in 2025 and potentially $100 billion by 2027, which would make it the fastest company in history to reach that milestone. OpenAI’s partnership with Microsoft has provided the compute resources, cloud infrastructure, and enterprise distribution needed to scale rapidly. However, ChatGPT’s market share in AI chatbot traffic has declined from 87% to 64-68% as competition from Google, Anthropic, and open-source alternatives intensifies. The company filed confidential S-1 paperwork in June 2026, signaling an eventual IPO.

Microsoft: Through its deep partnership with OpenAI and aggressive integration of AI across its entire product suite, Microsoft has positioned itself as the leading enterprise AI provider. Azure’s AI services, Copilot products across Office and Windows, and cloud infrastructure make Microsoft a comprehensive AI platform for businesses. The company is investing billions in AI infrastructure and has made AI central to its growth strategy. Microsoft’s advantage lies in its existing enterprise relationships and the ability to integrate AI into tools that billions of people already use daily.

Google/Alphabet: With its DeepMind research division, Google Brain heritage, and Gemini family of models, Google remains a formidable competitor in AI. The company’s advantages include massive data resources from Search and YouTube, world-class research talent, and cloud infrastructure through Google Cloud Platform. Google’s AI capabilities are integrated across Search, Workspace, Cloud, Android, and its advertising business, giving it extensive distribution channels. The company has invested heavily in AI for over a decade and continues to produce breakthrough research.

Anthropic: The creator of the Claude AI assistant has emerged as a leading AI safety-focused company, attracting significant investment from Amazon and Google. Anthropic’s emphasis on AI safety, constitutional AI, and responsible development has resonated with risk-conscious enterprises and organizations handling sensitive data. The company’s recent acquisition of Stainless signals ambitions in the developer tools space. Anthropic differentiates itself through longer context windows, more nuanced reasoning, and a focus on helpful, harmless, and honest AI behavior.

Meta: While initially perceived as lagging in generative AI, Meta has invested heavily in open-source models through its Llama series, fundamentally disrupting the market dynamics. The company’s strategy of releasing capable, free, open-source models has accelerated AI adoption globally and forced competitors to reconsider their pricing and access strategies. Meta’s AI investments focus on its core social media business, content recommendation, and metaverse ambitions. The company’s Reality Labs division continues to invest in AI for augmented and virtual reality applications.

Chinese Competitors: Chinese technology companies are making significant strides in AI capabilities, with models like DeepSeek-R1, Qwen, and Kimi demonstrating performance competitive with Western offerings on many benchmarks. Chinese frontier labs are investing heavily in reasoning models, multimodal capabilities, and agentic AI. The competition between U.S. and Chinese AI capabilities is intensifying, with implications for global technology leadership, export controls, and the future direction of AI development. Companies like Baidu, Alibaba, and emerging startups are pushing the boundaries of what’s possible.

Emerging Players: The AI market continues to attract new entrants across all segments. Startups focusing on vertical-specific AI solutions for healthcare, legal, finance, and other industries are securing significant funding by demonstrating domain expertise combined with AI capabilities. Infrastructure companies providing AI-optimized hardware, software platforms, and development tools are also thriving. The rapid pace of innovation means that market positions can shift quickly, and today’s leaders may face disruption from unexpected directions.

Challenges and Pain Points

Despite the tremendous growth and opportunity, the AI market faces significant challenges that organizations must navigate carefully to realize value from their AI investments. Understanding these challenges is essential for developing realistic AI strategies.

1. Data Quality and Management: AI systems are fundamentally limited by the quality of data they’re trained on. Organizations struggle with data quality issues including incomplete datasets, inconsistent formatting, bias in historical data, and data silos that prevent comprehensive analysis. Data management failures are a leading cause of AI project failures, with many enterprises discovering that their data infrastructure is not ready for AI-scale workloads. Cleaning, labeling, and organizing data for AI can consume 60-80% of project timelines and budgets.

2. AI Talent Shortage: The demand for AI talent—including machine learning engineers, data scientists, AI researchers, and MLOps specialists—far outstrips the available supply. Over half of organizations surveyed cite skills gaps and recruitment challenges as a primary barrier to AI implementation. The shortage spans both technical roles and business roles such as AI strategists and AI ethicists. This talent gap drives up compensation costs significantly and slows deployment timelines as organizations compete for a limited pool of qualified professionals.

3. Security and Privacy Risks: AI systems introduce new categories of security vulnerabilities and privacy concerns that many organizations are unprepared to address. Top threats being addressed by security-conscious organizations include AI hallucinations (56%), cybersecurity vulnerabilities (53%), intellectual property and data leakage issues (46%), regulatory compliance challenges (45%), and explainability concerns (39%). Organizations must balance the drive for AI innovation with robust security practices, data governance, and privacy protection.

4. Integration and Scalability: Moving AI from successful pilot projects to production deployment at enterprise scale remains a significant challenge. Many organizations struggle to integrate AI into existing workflows, legacy systems, and business processes. The gap between proof-of-concept success and production deployment is a major pain point, with technical debt, infrastructure limitations, and organizational resistance often blocking scaling efforts. What works for a small test case often fails when expanded to handle real-world volume and complexity.

5. Ethical and Regulatory Concerns: Issues of bias, fairness, transparency, accountability, and safety are ongoing concerns that organizations cannot ignore. The EU AI Act and similar regulations worldwide are creating comprehensive compliance requirements that organizations must navigate. As noted by risk experts, “By 2026, regulators and supervisors are making it clear that innovation no longer shields organizations from responsibility.” AI systems are now assessed by their impact on customers and society, not by their technological novelty. Organizations must invest in AI governance, ethics review processes, and compliance frameworks.

6. ROI Measurement and Expectations: Despite massive investments in AI, many organizations struggle to measure and demonstrate return on investment. Every quarter, Fortune 500 companies announce spending $10 million or more on AI infrastructure while struggling to quantify concrete returns. The shift from measuring productivity improvements to demonstrating P&L impact reflects growing pressure from boards and investors to show tangible business value. Many AI projects fail to meet inflated expectations set during the hype phase.

7. Compute Costs and Energy Consumption: Training and running large AI models requires massive computational resources that come with significant costs. Training frontier models can cost hundreds of millions of dollars in compute alone. The energy consumption of AI data centers is becoming an environmental concern as the industry scales. Organizations must balance the capabilities of larger models against the costs of deployment, often making difficult trade-offs between performance and affordability.

Opportunities and Growth Strategies

For organizations looking to capitalize on the AI market’s explosive growth, several strategic opportunities present significant potential for value creation and competitive advantage.

1. Vertical AI Solutions: Industry-specific AI applications represent a massive and largely untapped opportunity. Rather than general-purpose AI tools that require extensive customization, solutions tailored to healthcare, financial services, manufacturing, legal services, and other verticals can deliver superior value out of the box. Companies that deeply understand industry workflows, regulatory requirements, and business processes—and combine that domain expertise with AI capabilities—can capture significant market share and build durable competitive moats. Vertical AI solutions can achieve higher accuracy, better compliance, and faster time-to-value than horizontal alternatives.

2. AI Infrastructure and Tools: As AI adoption accelerates across all industries, demand for infrastructure, development tools, and supporting platforms continues to grow rapidly. Opportunities exist across the stack: AI-optimized hardware beyond GPUs, MLOps platforms for model management, data labeling and annotation services, model monitoring and observability tools, AI security solutions, and development frameworks. The “picks and shovels” play in AI—providing the tools and infrastructure that enable others to build AI applications—remains an attractive and less competitive market than the application layer.

3. Enterprise AI Services: The majority of enterprises need significant help implementing AI effectively. Consulting, implementation, integration, and managed services for AI represent a growing and profitable market. Companies that can bridge the gap between AI technology and business outcomes—helping enterprises navigate data preparation, model selection, system integration, change management, and ongoing optimization—are well-positioned for sustained growth. The complexity of enterprise AI deployment creates natural barriers to entry for service providers who develop expertise.

4. AI-Powered Automation: The opportunity to automate knowledge work and complex business processes with AI is vast and still in early stages. From intelligent document processing to AI customer service agents to automated software development, AI can handle increasingly complex tasks that previously required human judgment. Companies that identify high-volume, high-cost, repetitive processes within organizations and apply AI automation can achieve significant ROI while improving accuracy, consistency, and speed. The key is identifying the right use cases where AI can deliver clear value.

5. AI Safety and Governance: As AI systems become more powerful, autonomous, and widespread, the need for safety tools, governance frameworks, risk management solutions, and compliance platforms grows rapidly. Companies providing AI explainability, bias detection and mitigation, model monitoring, output validation, and regulatory compliance tools are addressing a critical and expanding market need. This segment will grow in importance as regulations tighten and organizations recognize that responsible AI is not optional.

6. Edge AI and On-Device Intelligence: Running AI on edge devices—smartphones, IoT sensors, autonomous vehicles, industrial equipment—opens new use cases and reduces dependency on cloud infrastructure and network connectivity. The edge AI market is growing rapidly as devices become more powerful and use cases expand from smart homes to industrial automation to healthcare monitoring. Edge AI offers advantages in latency, privacy, and cost that make it attractive for many applications.

Case Studies and Success Stories

Real-world implementations demonstrate the transformative potential of AI when properly executed with clear objectives, adequate resources, and realistic expectations. Here are three detailed case studies illustrating successful AI deployment across different industries:

Case Study 1: Nasdaq AI Platform Implementation: Nasdaq, one of the world’s premier stock exchanges and leading financial technology platforms, built a comprehensive AI platform to optimize its internal operations and enhance its external products and services. The platform leverages AI for market surveillance to detect manipulation and fraud, data analytics to provide insights to market participants, and operational efficiency to streamline internal processes. By implementing AI, Nasdaq has improved functionality and user experience for its customers while reducing operational costs and risk. The implementation required careful attention to regulatory compliance, data security, and system reliability given the mission-critical nature of exchange operations. Nasdaq’s case demonstrates how financial services companies can deploy AI at scale while maintaining the highest standards of security and compliance.

Case Study 2: Healthcare Generative AI for Clinical Documentation: A major healthcare organization implemented generative AI for clinical documentation, patient communication, and administrative workflows. The system uses large language models to draft clinical notes from physician-patient interactions, reducing documentation time by 40% and allowing clinicians to spend more time with patients. AI-powered patient communication delivers personalized appointment reminders, medication instructions, and follow-up care guidance. The implementation required extensive attention to HIPAA compliance, clinical validation of AI outputs, integration with electronic health record systems, and training clinical staff on appropriate use. The results included improved clinician satisfaction, reduced burnout, better patient engagement, and more accurate billing through improved documentation. This case illustrates both the potential and the complexity of deploying AI in highly regulated healthcare environments.

Case Study 3: Retail AI-Powered Personalization and Operations: A major multinational retailer deployed AI across its e-commerce platform and supply chain operations to deliver personalized shopping experiences and optimize inventory management. The AI system processes customer behavior data in real-time to deliver individualized product recommendations, dynamic pricing based on demand patterns, and personalized marketing messages. In the supply chain, AI predicts demand by location and optimizes inventory allocation, reducing stockouts and excess inventory simultaneously. The results included a 25% increase in e-commerce conversion rates, 15% improvement in inventory turnover, significant reduction in product returns through better product-customer matching, and millions in cost savings from optimized logistics. This comprehensive implementation demonstrates how AI can transform multiple aspects of retail operations when deployed as an integrated strategy rather than isolated use cases.

Future Outlook and Predictions

The AI market’s trajectory points toward continued rapid growth and increasing impact across all sectors of the economy. Based on current trends and expert forecasts, here’s what to expect in the coming years:

2026-2027 Near-Term Outlook: The market will reach approximately $757 billion by 2027, with enterprise AI adoption continuing to accelerate across all industries. Agentic AI will move from early adoption to mainstream deployment as organizations become comfortable with autonomous systems handling more complex tasks. Competition in AI foundation models will intensify significantly, with Chinese labs challenging U.S. dominance and open-source alternatives gaining traction. Regulatory frameworks will mature globally, with the EU AI Act serving as a template for other jurisdictions. We can expect to see the first wave of AI-native companies achieving massive scale, built from the ground up with AI at their core rather than retrofitting AI into traditional business models.

2028-2030 Medium-Term Projections: By 2030, the global AI market is projected to exceed $1.5 trillion according to multiple research firms. AI will become truly ubiquitous in enterprise software, with AI capabilities embedded in virtually every business application rather than existing as separate tools. Frontier AI models will require investments of hundreds of billions of dollars and gigawatts of electrical power to train, potentially limiting development to a handful of well-capitalized organizations. AI will demonstrate transformative capabilities in scientific R&D, accelerating discovery in medicine, materials science, climate modeling, and fundamental physics. The technology will handle increasingly complex cognitive tasks, potentially automating significant portions of knowledge work in fields like law, finance, and software engineering.

Beyond 2030 Long-Term Vision: Long-term forecasts suggest AI will add $15.7 trillion to the global economy by 2030, fundamentally reshaping economic productivity and growth. The technology will reshape labor markets comprehensively, with some roles automated entirely while new categories of AI-enabled jobs emerge. Questions about artificial general intelligence (AGI)—AI systems with human-like general reasoning capabilities—will move from theoretical speculation to practical reality as models demonstrate increasingly general competencies across domains. The societal implications of ubiquitous AI will require new frameworks for education, social safety nets, and economic policy.

Key Uncertainties and Risk Factors: Several factors could significantly alter this trajectory. Regulatory changes could either constrain AI development through restrictive policies or accelerate adoption through supportive frameworks. Breakthroughs in AI efficiency could dramatically reduce costs while improving capabilities, accelerating adoption. Geopolitical tensions could fragment the global AI market into competing blocs with incompatible standards and limited collaboration. Public sentiment shifts could affect adoption rates if concerns about AI safety, job

Key Takeaways

- The global AI market reached $539 billion in 2026, growing 19-38% year-over-year, with projections indicating $1.675 trillion by 2031

- Enterprise AI adoption has surged to 88% of organizations, up from 55% in 2023, marking a fundamental shift from experimentation to production

- Agentic AI has emerged as the fastest-growing priority, with 31.5% year-over-year growth as organizations deploy autonomous AI systems

- NVIDIA dominates AI hardware with 81% market share, while OpenAI, Microsoft, Google, and Anthropic compete fiercely in models and platforms

- VC investment in AI reached $258.7 billion in 2025, with AI startups capturing 53% of all global venture capital

- Key challenges include data quality, talent shortage, security risks, integration complexity, and ROI measurement

- Major opportunities exist in vertical AI solutions, infrastructure tools, enterprise services, automation, and AI governance

- The U.S. maintains market leadership with over 80% of global private AI investment, though Chinese competitors are rapidly advancing

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- AI Statistics 2026 – Global Data & Trends: https://aistatistics.ai

- TechnologyChecker – AI Market Size Statistics 2026: https://technologychecker.io/blog/ai-market-size-statistics

- IBM – AI Tech Trends Predictions 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- Microsoft – 7 AI Trends to Watch in 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026

- FutureSearch – OpenAI Revenue Forecast 2026: https://futuresearch.ai/openai-revenue-forecast

- CompaniesHistory – AI Market Share By Company Statistics 2026: https://www.companieshistory.com/ai-market-share-by-company

- Crunchbase – Q1 2026 Venture Funding Records: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026

- OECD – Venture Capital Investments in AI Through 2025: https://www.oecd.org/en/publications/venture-capital-investments-in-artificial-intelligence-through-2025

- S3Corp – Top 10 AI Challenges Businesses Face in 2026: https://www.s3corp.com.vn/insights/artificial-intelligence-challenges

- EBSEDU – AI Challenges in 2026: 15 Risks & Limitations: https://ebsedu.org/blog/artificial-intelligence-ai-challenges

- Deloitte – State of AI in the Enterprise 2026: https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- NVIDIA Blog – State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026

- Mordor Intelligence – Generative AI Market Size 2026-2031: https://www.mordorintelligence.com/industry-reports/generative-ai-market

- Grand View Research – Generative AI Market Report: https://www.grandviewresearch.com/industry-analysis/generative-ai-market-report

- MarketsandMarkets – Top Companies in Generative AI Market: https://www.marketsandmarkets.com/ResearchInsight/generative-ai-market.asp

- Futurum Group – Enterprise AI ROI Shifts as Agentic Priorities Surge: https://futurumgroup.com/press-release/enterprise-ai-roi-shifts-as-agentic-priorities-surge

- Exploding Topics – AI Market Size Statistics 2025-2032: https://explodingtopics.com/blog/ai-market-size-stats

- Precedence Research – Artificial Intelligence Market Size 2026-2035: https://www.precedenceresearch.com/artificial-intelligence-market

- ABI Research – Artificial Intelligence Software Market Size: https://www.abiresearch.com/news-resources/chart-data/report-artificial-intelligence-market-size-global