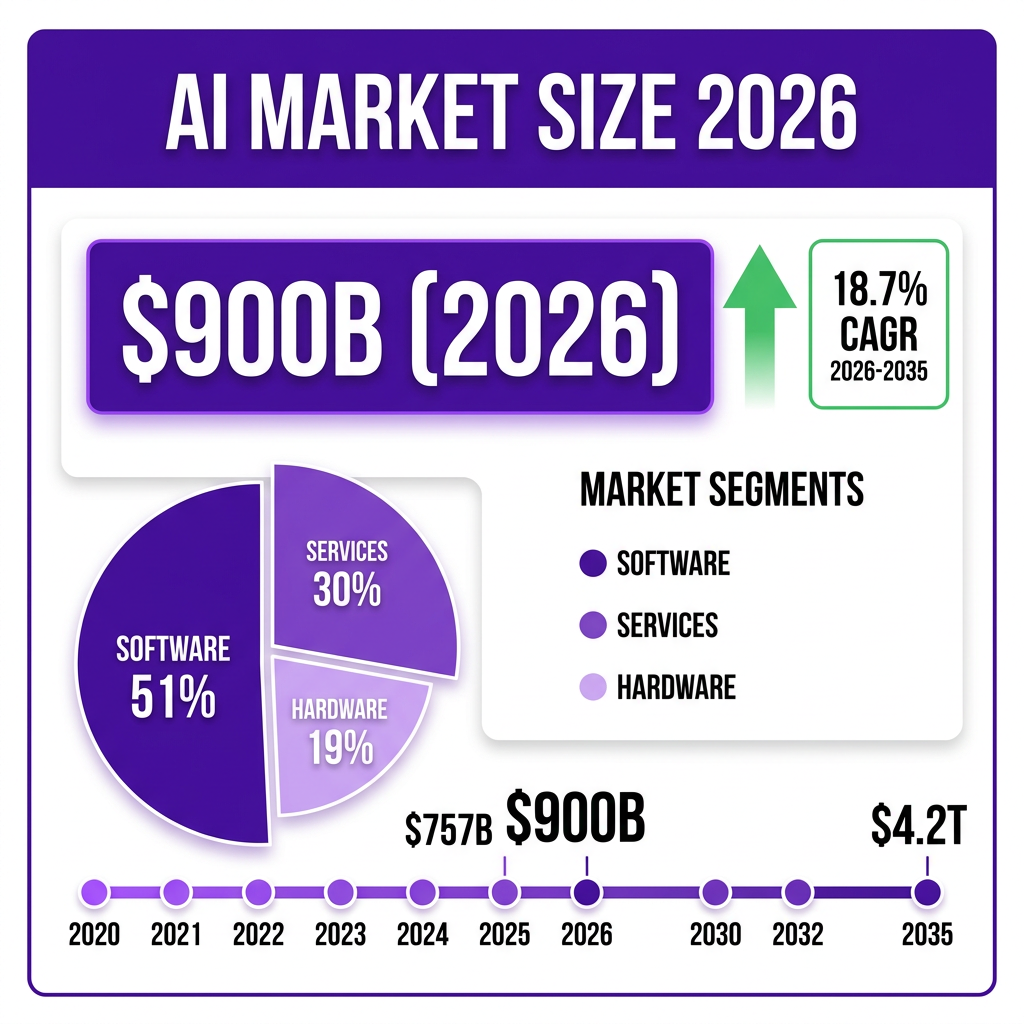

The artificial intelligence market has reached an inflection point. In 2026, the global AI market is valued at approximately $900 billion, representing a staggering 18.7% increase from 2025’s $757.58 billion. This isn’t just another tech boom—it’s a fundamental restructuring of how businesses operate, compete, and create value.

What’s driving this explosive growth? Four of the five largest venture rounds ever recorded closed in Q1 2026 alone. OpenAI raised $122 billion. Anthropic secured $30 billion. xAI captured $20 billion. Waymo landed $16 billion. Collectively, these four companies raised $188 billion—representing 65% of all global venture investment in the quarter.

But the AI story extends far beyond Silicon Valley’s frontier labs. From healthcare diagnostics to autonomous vehicles, from enterprise automation to creative tools, AI has permeated every industry vertical. The question for business leaders is no longer whether to adopt AI, but how quickly they can scale it across their organizations.

Market Overview: The $900 Billion AI Ecosystem

The global artificial intelligence market has evolved from experimental technology to mission-critical infrastructure in less than a decade. According to Precedence Research, the market size reached $757.58 billion in 2025 and is projected to hit $900 billion in 2026. Looking ahead, analysts forecast the market will reach an astounding $4.22 trillion by 2035, growing at a compound annual growth rate (CAGR) of 18.73%.

This growth trajectory places AI among the fastest-expanding technology markets in history. For context, the AI market is growing faster than the early internet boom of the late 1990s and rivals the smartphone revolution of the 2000s in terms of adoption velocity and capital deployment.

Regional Market Distribution

North America continues to dominate the AI landscape, accounting for 36.92% of the global market in 2025. The United States alone captured 83% of global venture capital in Q1 2026—a concentration of funding unprecedented in modern tech history. This dominance reflects the region’s combination of research institutions, venture capital availability, and regulatory environment that has historically favored innovation.

However, the Asia Pacific region is emerging as the fastest-growing market, projected to expand at a CAGR of 19.8% from 2026 to 2035. China raised $16.1 billion in venture funding in Q1 2026, making it the second-largest market globally. The United Kingdom follows with $7.4 billion invested, representing Europe’s strongest AI hub.

This geographic distribution matters for businesses making AI investment decisions. Companies operating in North America benefit from proximity to leading AI labs and talent pools. Those in Asia Pacific can leverage faster growth rates and often more favorable regulatory environments for AI deployment. European businesses face stricter compliance requirements under the EU AI Act but also benefit from emerging standardization that could reduce long-term compliance costs.

Market Segmentation by Solution Type

The AI market breaks down into three primary solution categories, each with distinct growth characteristics:

Software (51.40% market share in 2025): AI software remains the largest segment, encompassing machine learning platforms, natural language processing tools, computer vision systems, and generative AI applications. This segment benefits from high margins and scalability, with cloud-based delivery models enabling rapid deployment across enterprise customers.

Services (projected 18.30% CAGR): AI services—including consulting, implementation, and managed services—are growing rapidly as enterprises seek expertise to navigate complex AI deployments. The skills gap in AI implementation has created a robust market for professional services, with demand outpacing supply in most regions.

Hardware: AI hardware, including GPUs, TPUs, and specialized AI chips, represents the infrastructure layer enabling AI computation. While a smaller segment by revenue, hardware investments drive the capacity constraints that limit AI scaling. The $100+ billion data center investments announced in 2026 underscore hardware’s critical role in the AI value chain.

Technology Segmentation

By underlying technology, machine learning dominates with 36.70% market share, reflecting its maturity and broad applicability across use cases. However, generative AI is the fastest-growing segment, projected to expand at a 22.90% CAGR through 2035.

The generative AI market alone is now valued at $63 billion—larger than the entire US video gaming industry. This segment has captured public imagination and boardroom attention alike, driving unprecedented investment in large language models, image generation, and multimodal AI systems.

Functional Applications

By business function, operations leads with 21.80% market share in 2026, as organizations prioritize efficiency and automation. Cybersecurity represents the fastest-growing functional application, with a projected CAGR of 20.40%, reflecting the escalating AI arms race between attackers and defenders.

Other significant functional segments include customer service (AI-powered chatbots and support systems), marketing and sales (personalization and lead scoring), and finance (fraud detection and algorithmic trading). Each segment shows distinct adoption patterns based on regulatory constraints, ROI visibility, and implementation complexity.

Industry Verticals

The BFSI (Banking, Financial Services, and Insurance) sector leads AI adoption with 19.60% market share, driven by data-rich environments and clear ROI from fraud detection, risk assessment, and algorithmic trading applications. Healthcare follows as the fastest-growing vertical, with a projected CAGR of 19.10%, as AI transforms drug discovery, medical imaging, and personalized medicine.

Other significant verticals include retail (personalization and supply chain optimization), manufacturing (predictive maintenance and quality control), and automotive (autonomous driving and smart manufacturing). Each industry faces unique regulatory and ethical considerations that shape AI adoption timelines and use case prioritization.

Key Statistics and Data Points

The AI market’s scale becomes clearer when examining the underlying statistics that define its growth, adoption, and impact. These numbers tell a story of rapid transformation across every dimension of the technology and business landscape.

Market Size and Growth Metrics

- $900 billion: Global AI market size in 2026 (Precedence Research)

- $757.58 billion: AI market size in 2025, representing the baseline for current growth

- $4.22 trillion: Projected AI market size by 2035

- 18.73%: Compound annual growth rate (CAGR) from 2026 to 2035

- 9x growth: AI market projected to increase nearly 9x by 2033 (Grand View Research)

- 31.5% CAGR: Alternative growth forecast for the generative AI subsegment

- $3.5 trillion: Alternative 2033 market size projection from Grand View Research

Investment and Funding Statistics

- $300 billion: Total global venture investment in Q1 2026 (Crunchbase)

- 150%: Year-over-year increase in venture funding in Q1 2026

- $242 billion: AI sector funding in Q1 2026—80% of total venture capital

- 80%: Share of global venture funding captured by AI companies in Q1 2026

- 55%: Previous record for AI’s share of venture funding (Q1 2025)

- $188 billion: Combined funding for OpenAI, Anthropic, xAI, and Waymo in Q1 2026

- $122 billion: OpenAI’s single funding round—the largest in history

- $30 billion: Anthropic’s funding round

- $20 billion: xAI’s funding round

- $16 billion: Waymo’s funding round

- $900 billion: Value added to the Crunchbase Unicorn Board in Q1 2026

- $250 billion: U.S. venture funding in Q1 2026 (83% of global total)

- $16.1 billion: China’s venture funding in Q1 2026

- $7.4 billion: UK’s venture funding in Q1 2026

Adoption and Usage Statistics

- 35.49%: Global population using AI tools daily (Exploding Topics research)

- 84.58%: Users who increased AI usage in the past 12 months

- 16.3%: Global AI adoption rate by end of 2025 (up from 15.1%)

- 88%: Companies using AI in at least one business function (up from 78%)

- 50%: Increase in worker access to AI tools in 2025 (Deloitte)

- 90%: Tech workers using AI in their jobs

- 1.8%: New job listings specifically in AI space

- 1 in 6: Global population using generative AI tools by end of 2025

Enterprise Impact Metrics

- 66%: Organizations reporting productivity and efficiency gains from AI (Deloitte)

- 53%: Organizations enhancing insights and decision-making with AI

- 40%: Organizations reducing costs through AI implementation

- 38%: Organizations improving client/customer relationships with AI

- 34%: Leaders reporting transformative business impact from AI (doubled from previous year)

- 58%: Companies using physical AI (robotics, autonomous systems)

- 80%: Projected physical AI adoption rate within two years

- 42%: Companies believing their strategy is highly prepared for AI adoption

Technology Performance Metrics

- Gemini 3 Pro: Surpassed GPT-5.2 on Humanity’s Last Exam benchmark in 2026

- 4.4x: Value of AI search visitors compared to organic search visitors (Semrush)

- 2028: Projected year when ChatGPT search traffic overtakes organic search

- 5.2 billion: Monthly visits to ChatGPT.com (December 2025)

- 573.5 million: OpenAI.com traffic (December 2025, down 38.9% from August)

Workforce and Employment Impact

- 92 million: Jobs potentially displaced by AI by 2030

- 170 million: New jobs potentially created by AI by 2030

- +78 million: Net job creation from AI transformation

- 66%: US physicians using healthcare AI

- 20%: Companies with mature governance models for autonomous AI agents

Industry-Specific Statistics

- $400 billion: Projected revenue from self-driving cars by 2035

- 51.40%: AI software segment market share

- 36.70%: Machine learning technology market share

- 22.90%: Generative AI projected CAGR

- 21.80%: Operations function market share

- 20.40%: Cybersecurity function projected CAGR

- 19.60%: BFSI industry vertical market share

- 19.10%: Healthcare industry projected CAGR

- 19.8%: Asia Pacific region projected CAGR

Major Trends Shaping the AI Market in 2026

The AI landscape in 2026 is defined by seven transformative trends that are reshaping how organizations develop, deploy, and benefit from artificial intelligence. Understanding these trends is essential for businesses seeking to navigate the rapidly evolving AI ecosystem.

1. The Agentic AI Surge

Agentic AI—autonomous systems capable of planning, executing multi-step tasks, and adapting to changing circumstances—is poised for explosive growth. According to Deloitte’s 2026 State of AI report, agentic AI usage is set to rise sharply in the next two years, yet only one in five companies currently has a mature governance model for these autonomous systems.

This gap between adoption and governance represents both opportunity and risk. Organizations that successfully implement agentic AI can automate complex workflows that previously required human judgment—from customer service interactions to supply chain optimization to software development. However, the autonomous nature of these systems raises significant questions about accountability, transparency, and control.

The market is responding with a new category of AI infrastructure focused on agent orchestration, monitoring, and safety. Companies like Anthropic, OpenAI, and emerging players are developing frameworks for responsible agent deployment. Expect this category to mature rapidly as enterprise demand for autonomous capabilities outpaces current governance capabilities.

2. Physical AI’s Mainstream Emergence

Physical AI—embodied intelligence in robots, autonomous vehicles, drones, and industrial automation—is gaining traction at an unprecedented rate. Deloitte reports that 58% of companies now use physical AI in at least a limited capacity, and this figure is projected to reach 80% within two years.

The Asia Pacific region leads in physical AI implementation, driven by manufacturing concentration and government investment in automation. Applications span warehouse robotics, autonomous delivery systems, surgical robots, and manufacturing quality control.

Waymo’s $16 billion funding round underscores investor confidence in autonomous systems. The company represents the vanguard of a broader shift toward AI that interacts with the physical world—a fundamentally harder problem than digital AI due to safety requirements, edge case complexity, and regulatory scrutiny.

3. Enterprise AI at Scale

After years of pilot programs and proof-of-concepts, enterprises are moving AI from experimentation to production at scale. Worker access to AI tools increased 50% in 2025, and the number of companies with 40% or more AI projects in production is set to double within six months.

This shift from pilot to scale requires new organizational capabilities. Companies are restructuring teams, redesigning processes, and investing in AI infrastructure. The focus has moved from “Can AI do this?” to “How do we deploy AI across the enterprise?”

However, a preparedness gap remains. While 42% of companies believe their strategy is highly prepared for AI adoption, they feel less prepared regarding infrastructure, data, risk management, and talent. This gap creates opportunities for vendors providing enterprise AI platforms, consulting services, and managed solutions.

4. The Rise of Sovereign AI

Sovereign AI—AI systems deployed under national laws, infrastructure, and data governance—is emerging as a critical strategic priority. Countries and companies are increasingly prioritizing strategic independence in AI capabilities, driven by concerns about data privacy, supply chain security, and geopolitical competition.

This trend manifests in multiple ways: national AI clouds, domestic chip manufacturing initiatives, data localization requirements, and government-backed AI research programs. The EU’s AI Act, while creating compliance burdens, also establishes a framework for trusted AI that could become a competitive advantage for European providers.

For multinational corporations, sovereign AI creates complexity. Companies must navigate varying regulatory regimes, potentially maintain separate AI infrastructure in different jurisdictions, and balance global efficiency with local compliance. This fragmentation could slow AI adoption in some regions while accelerating domestic AI industries in others.

5. The AI Regulation Wave

2026 marks the end of AI’s regulatory honeymoon. The EU AI Act’s Phase Two implementation arrives in August 2026, introducing transparency requirements and high-risk AI system rules. In the United States, a patchwork of state laws in California, Colorado, New York, and other jurisdictions creates complex compliance obligations.

State attorneys general have become active AI enforcers, with settlements targeting companies across industries. A 42-state attorney general coalition signals coordinated enforcement pressure that will intensify throughout 2026. Cyber insurance carriers are introducing AI-specific security riders that condition coverage on documented AI risk management practices.

For businesses, this regulatory landscape requires proactive compliance investment. Organizations must map their AI use cases against applicable regulations, implement governance frameworks, and document risk management practices. The cost of compliance is significant, but the cost of non-compliance—fines, litigation, and reputational damage—is far higher.

6. Concentration of Capital and Capability

The AI market is experiencing unprecedented capital concentration. Four companies—OpenAI, Anthropic, xAI, and Waymo—captured 65% of global venture funding in Q1 2026. This concentration extends beyond funding to talent, compute resources, and data access.

This dynamic creates a two-tier market. Frontier labs with billion-dollar funding rounds can train the largest models, attract top talent, and build the most capable systems. Everyone else must either partner with these labs, focus on narrower applications, or find alternative approaches like smaller specialized models or open-source solutions.

The implications for competition are profound. Incumbents with AI capabilities may extend their advantages, while startups face higher barriers to entry in foundation model development. However, opportunities remain in application layers, vertical solutions, and AI infrastructure.

7. AI Workforce Transformation

The AI skills gap is the biggest barrier to enterprise AI integration, according to Deloitte’s research. Rather than replacing workers through role redesign, companies are prioritizing AI education and upskilling. This reflects a view of AI as augmentation rather than automation—a tool that makes workers more capable rather than obsolete.

The workforce impact statistics are striking: AI could displace 92 million jobs by 2030 while creating 170 million new roles—a net positive of 78 million jobs. However, the transition will be disruptive, requiring massive reskilling programs and social safety net adaptations.

For organizations, the priority is building AI fluency across the workforce. This includes technical skills for AI developers, operational skills for AI implementers, and literacy for all employees who will interact with AI systems. Companies that invest in workforce development will be better positioned to capture AI’s benefits.

Deep Dive: AI Market Dynamics and Investment Patterns

The $300 billion invested in AI startups during Q1 2026 represents more than just capital allocation—it signals a fundamental restructuring of the technology industry. This investment surge is reshaping competitive dynamics, creating new categories of winners and losers, and establishing patterns that will influence the market for years to come.

The Late-Stage Funding Explosion

Late-stage funding reached $246.6 billion in Q1 2026, up 205% year over year. This concentration in mature companies reflects investor preference for proven business models and established market positions. A total of $235 billion was invested in 158 late-stage companies that raised rounds of $100 million or more.

This dynamic creates challenges for early-stage companies. While seed funding increased 31% year over year to $12 billion, deal counts fell 30% to 3,800. Investors are writing larger checks to fewer companies, raising the bar for seed-stage funding and potentially limiting innovation from new entrants.

The implications for the AI ecosystem are significant. Capital concentration favors incumbents and well-connected founders, potentially slowing the pace of disruptive innovation. However, the massive investments also accelerate AI capabilities, creating opportunities for companies building on top of frontier models.

Early-Stage Resilience

Despite late-stage dominance, early-stage funding showed resilience. Series A and B rounds totaled $41.3 billion across 1,800 deals, up 41% year over year. Much of this increase went to Series A rounds, suggesting investors are willing to bet on promising early-stage companies but want to see traction before committing.

For entrepreneurs, this environment requires clear differentiation. Companies that can demonstrate unique data assets, proprietary algorithms, or deep domain expertise have the best chance of attracting funding. Generic AI applications face intense competition and skeptical investors.

Regional Analysis: AI Market Geography

The geographic distribution of AI investment and adoption reveals important patterns about where value is being created and captured in the AI economy.

United States: The Undisputed Leader

The United States captured 83% of global venture funding in Q1 2026, up from 71% in Q1 2025. This concentration reflects the US advantages in research universities, venture capital ecosystem, and regulatory environment. The four largest AI funding rounds all went to US-based companies.

However, this dominance raises questions about sustainability. Other regions are investing heavily in AI capabilities, and regulatory developments could shift competitive dynamics. The EU’s AI Act, for example, may create advantages for European companies that can navigate its requirements effectively.

China: The Rising Challenger

China’s $16.1 billion in venture funding makes it the second-largest AI market. Chinese companies benefit from massive domestic markets, government support for AI development, and less restrictive data regulations. Companies like Baidu, Alibaba, and Tencent are investing heavily in AI capabilities.

The US-China AI competition has geopolitical dimensions. Export controls on AI chips, investment restrictions, and data localization requirements are creating separate spheres of AI development. This bifurcation could limit the benefits of global collaboration while accelerating domestic capabilities in both countries.

Europe: Regulation as Strategy

Europe’s $7.4 billion in venture funding, led by the UK, reflects a smaller but significant AI ecosystem. The EU AI Act creates the world’s most comprehensive AI regulatory framework, potentially establishing European standards as global benchmarks.

For European AI companies, regulation is both burden and opportunity. Compliance costs are substantial, but companies that master regulatory requirements can build trust advantages and potentially shape global standards. The “Brussels effect”—where EU regulations influence global practices—could benefit European AI providers.

AI Adoption Patterns by Industry

AI adoption varies significantly across industries, reflecting differences in data availability, regulatory constraints, and use case maturity. Understanding these patterns helps identify where AI value is being created today and where opportunities exist for tomorrow.

Technology and Software

The technology sector leads AI adoption, with 90% of tech workers using AI in their jobs. Applications include code generation, testing automation, customer support, and product management. Companies like GitHub (Copilot), Atlassian, and countless startups are building AI-native tools for software development.

The sector also faces disruption risks. AI coding assistants could reduce demand for certain programming roles, while AI-powered tools enable non-technical users to build applications. The net effect is likely increased software output but changing skill requirements for technology professionals.

Financial Services

Financial services leads in AI market share with 19.60% of the total. Applications span fraud detection, algorithmic trading, risk assessment, customer service, and regulatory compliance. The sector’s data-rich environment and clear ROI metrics make it ideal for AI deployment.

Regulatory requirements create both constraints and opportunities. Banks must explain AI-driven decisions, maintain audit trails, and ensure fairness. These requirements favor established players with compliance infrastructure while creating opportunities for RegTech providers.

Healthcare

Healthcare is the fastest-growing AI vertical with a 19.10% projected CAGR. Applications include medical imaging, drug discovery, personalized medicine, and administrative automation. The sector’s complexity and regulatory requirements create high barriers to entry but also substantial rewards for successful implementations.

66% of US physicians now use healthcare AI, reflecting rapid adoption among practitioners. The FDA has established pathways for AI medical device approval, creating regulatory clarity that enables investment. However, integration with existing healthcare workflows and EHR systems remains challenging.

Manufacturing

Manufacturing AI focuses on predictive maintenance, quality control, supply chain optimization, and robotics. The sector’s physical AI adoption is significant, with 58% of companies using physical AI in some capacity. The Asia Pacific region leads in manufacturing AI implementation.

ROI is typically clear and measurable: reduced downtime, improved quality, and lower maintenance costs. However, implementation requires significant IoT infrastructure investment and integration with legacy systems. Companies often start with pilots before scaling across facilities.

Key Players and Competitive Landscape

The AI market is dominated by a mix of established technology giants, well-funded startups, and emerging challengers. Understanding this competitive landscape is essential for businesses selecting AI partners and for investors evaluating opportunities.

The Frontier Labs

OpenAI: The most valuable AI company, with a $122 billion funding round in Q1 2026 that represents the largest venture round in history. OpenAI’s GPT models power countless applications, and ChatGPT remains the consumer face of generative AI. The company’s partnership with Microsoft provides compute resources and enterprise distribution.

Anthropic: Founded by former OpenAI researchers, Anthropic has raised $30 billion and differentiates on AI safety and constitutional AI approaches. The company’s Claude models compete directly with GPT on capabilities while emphasizing responsible development practices.

xAI: Elon Musk’s AI venture raised $20 billion in Q1 2026, bringing total funding to significant levels. xAI’s Grok models integrate with X (formerly Twitter) and position the company as a challenger with unique data access and distribution advantages.

Google/DeepMind: While not raising external venture capital, Google’s AI investments are massive. DeepMind’s research leadership, Gemini models, and integration across Google’s product suite make it a formidable competitor. Gemini 3 Pro’s benchmark performance in 2026 demonstrates continued technical competitiveness.

Technology Giants

Microsoft: Through its OpenAI partnership and Azure AI services, Microsoft has become the dominant enterprise AI platform. Copilot integration across Office 365, GitHub, and Windows creates a comprehensive AI ecosystem for business customers.

Amazon: AWS provides the infrastructure layer for much of the AI ecosystem. Bedrock offers foundation model access, while SageMaker supports custom model development. Amazon’s own AI models compete in specific use cases like Alexa and retail optimization.

Meta: Open-source AI strategy through models like Llama has made Meta a significant player in the open AI ecosystem. While not directly monetizing models, Meta benefits from community contributions and reduced dependence on competitors’ technology.

Apple: On-device AI and privacy-focused approaches differentiate Apple’s AI strategy. While less visible in cloud AI, Apple’s silicon and ecosystem integration create unique advantages for consumer AI applications.

Emerging Challengers

Waymo: The $16 billion funding round validates autonomous driving as a massive AI application. Waymo’s lead in self-driving technology, with commercial robotaxi operations, positions it as the category leader in physical AI.

Cohere: Focused on enterprise NLP applications, Cohere competes with larger labs by specializing in business use cases and data privacy.

AI21 Labs: Israeli startup developing foundation models and AI applications for enterprise customers.

Stability AI: Leading open-source image generation, with Stable Diffusion powering countless creative applications.

Infrastructure and Hardware Players

NVIDIA: Dominates AI training and inference hardware with GPUs. The company’s data center revenue reflects AI’s infrastructure demands, and its software ecosystem (CUDA) creates significant switching costs.

AMD: Emerging challenger in AI chips, with MI300 series competing for training and inference workloads.

Intel: Playing catch-up in AI accelerators while leveraging manufacturing capabilities and enterprise relationships.

Cloud Providers: AWS, Azure, and Google Cloud provide the infrastructure layer for AI deployment, with AI services representing the fastest-growing revenue category.

Challenges and Pain Points

Despite remarkable growth and investment, the AI market faces significant challenges that could slow adoption or limit value creation. Understanding these pain points is essential for realistic AI planning and risk management.

1. The AI Skills Gap

The shortage of AI talent is the biggest barrier to enterprise AI integration, according to Deloitte’s research. This gap spans multiple dimensions: machine learning engineers, data scientists, AI product managers, and professionals who can bridge technical and business requirements.

The talent shortage drives up costs—top AI researchers command seven-figure compensation packages—and limits implementation capacity. Companies compete not just with each other but with well-funded AI labs that can offer equity packages with massive upside potential.

Solutions include upskilling existing workforce, partnering with universities, using managed AI services that reduce in-house expertise requirements, and adopting no-code/low-code AI platforms. However, these approaches have limitations, and the skills gap will likely persist for years.

2. Regulatory Complexity and Compliance Costs

The regulatory landscape for AI is fragmented and evolving rapidly. The EU AI Act creates comprehensive requirements for high-risk AI systems. US state laws create a patchwork of obligations. Industry-specific regulations in healthcare, finance, and other sectors add additional layers.

Compliance costs are substantial. Organizations must conduct AI risk assessments, implement governance frameworks, document decision-making processes, and potentially maintain separate AI systems for different jurisdictions. For multinational corporations, this complexity is a significant operational burden.

The regulatory uncertainty also slows investment. Companies hesitate to commit to AI strategies that might be rendered non-compliant by pending legislation. This dynamic creates first-mover disadvantages in regulated industries, as early adopters bear the costs of regulatory experimentation.

3. AI Governance and Safety Concerns

Only 20% of companies have mature governance models for autonomous AI agents, despite rapid adoption of these capabilities. This governance gap creates risks: AI systems making inappropriate decisions, biased outcomes, security vulnerabilities, and accountability gaps when AI causes harm.

Safety concerns extend to frontier AI capabilities. As models become more capable, the potential for misuse or unintended consequences increases. The AI research community is divided on the severity of existential risks, but consensus exists on the need for responsible development practices.

For enterprises, governance challenges include monitoring AI system behavior, ensuring human oversight, maintaining audit trails, and establishing clear accountability chains. These requirements add overhead to AI deployment and may limit use cases where explainability is required.

Opportunities and Growth Strategies

Despite challenges, the AI market offers substantial opportunities for businesses that can navigate its complexities effectively. Three strategic approaches stand out for capturing AI value in 2026 and beyond.

1. Vertical AI Solutions

While frontier labs compete on general-purpose capabilities, significant opportunities exist in vertical-specific AI solutions. Healthcare AI, legal AI, financial services AI, and manufacturing AI all require domain expertise, specialized data, and regulatory understanding that generalists lack.

Successful vertical AI companies combine deep industry knowledge with AI capabilities to solve specific, high-value problems. Examples include drug discovery platforms, contract analysis tools, fraud detection systems, and predictive maintenance solutions.

The vertical approach offers several advantages: reduced competition from generalist players, higher customer willingness to pay for specialized solutions, stronger data moats, and clearer regulatory pathways. For entrepreneurs and investors, vertical AI represents a compelling strategy for building defensible businesses.

2. AI Infrastructure and Tooling

The massive investment in AI models creates downstream opportunities in infrastructure, tooling, and services. Companies need solutions for model training, deployment, monitoring, and governance. They need tools for data preparation, prompt engineering, and AI safety testing.

This infrastructure layer includes MLOps platforms, vector databases, AI observability tools, and security solutions for AI systems. As AI adoption scales, the tooling ecosystem will mature, creating opportunities analogous to those created by the cloud computing transition.

For developers and technical founders, AI infrastructure offers a massive addressable market with clear customer needs. Unlike the winner-take-all dynamics of foundation models, infrastructure can support multiple successful players serving different segments and use cases.

3. AI-Enabled Services

The AI skills gap creates opportunities for service providers who can bridge the gap between AI capabilities and business implementation. Consulting firms, systems integrators, and managed service providers are seeing unprecedented demand for AI expertise.

Successful AI service providers combine technical capabilities with change management expertise. They help clients identify use cases, select technologies, implement solutions, and manage organizational transformation. The highest-value providers develop proprietary methodologies and IP that differentiate them from commodity implementation shops.

For professional services firms, AI represents both opportunity and threat. Firms that successfully integrate AI into their own operations and client offerings will thrive. Those that fail to adapt risk displacement by AI-native competitors.

Case Studies and Success Stories

Real-world implementations demonstrate AI’s transformative potential across industries. These case studies illustrate both the opportunities and challenges of enterprise AI adoption.

Case Study 1: Healthcare AI Diagnostics

A major healthcare system implemented AI-powered diagnostic imaging across its radiology department. The system, trained on millions of medical images, assists radiologists in detecting anomalies in X-rays, CT scans, and MRIs. Results after 18 months: diagnostic accuracy improved by 15%, time to diagnosis decreased by 40%, and radiologist burnout scores improved significantly as tedious screening tasks were automated.

The implementation faced challenges: regulatory approval requirements, integration with legacy systems, and radiologist skepticism. Success required extensive change management, including training programs, workflow redesign, and clear communication about AI’s role as augmentation rather than replacement.

Key lessons: Healthcare AI implementations require regulatory expertise, clinical workflow integration, and extensive stakeholder engagement. The ROI is substantial but requires patience and investment in organizational change.

Case Study 2: Financial Services Fraud Detection

A global bank deployed an AI-powered fraud detection system that analyzes transaction patterns in real-time. The system uses machine learning to identify anomalies that might indicate fraudulent activity, automatically flagging suspicious transactions for review.

Results after 12 months: fraud losses decreased by 35%, false positive rates dropped by 50%, and customer satisfaction improved as legitimate transactions faced fewer unnecessary blocks. The system processes millions of transactions daily, operating with sub-second latency.

Implementation challenges included data quality issues, model explainability requirements for regulatory compliance, and integration with existing fraud investigation workflows. The bank invested heavily in data infrastructure and governance to support the AI system.

Key lessons: Financial services AI requires robust data infrastructure, regulatory compliance capabilities, and careful attention to model explainability. The business case is compelling but requires significant upfront investment.

Case Study 3: Manufacturing Predictive Maintenance

An automotive manufacturer implemented AI-powered predictive maintenance across its production lines. Sensors on critical equipment feed data to machine learning models that predict component failures before they occur, enabling proactive maintenance scheduling.

Results after 24 months: unplanned downtime decreased by 45%, maintenance costs reduced by 30%, and equipment lifespan extended by an average of 20%. The system pays for itself through avoided production losses alone.

Implementation required significant IoT infrastructure investment, data integration across multiple systems, and training for maintenance staff. The manufacturer started with a pilot on one production line before scaling across facilities.

Key lessons: Manufacturing AI requires IoT infrastructure, data integration capabilities, and workforce training. Starting with pilots before scaling reduces risk and builds organizational capability.

Future Outlook and Predictions

Looking ahead to 2027-2030, the AI market will continue its rapid evolution. Several trends will shape the landscape:

Market Growth Projections

The AI market is projected to reach $4.22 trillion by 2035, growing at an 18.73% CAGR. Alternative forecasts suggest even faster growth, with Grand View Research projecting $3.5 trillion by 2033—nearly 9x growth from current levels.

This growth will be driven by continued enterprise adoption, new use case emergence, and AI’s integration into an expanding range of products and services. The generative AI segment will likely grow fastest, though from a smaller base than established machine learning applications.

Technology Evolution

By 2030, we can expect AI systems with substantially expanded capabilities. Multimodal models that seamlessly process text, images, audio, and video will become standard. Agentic AI will automate complex multi-step tasks with minimal human oversight. Physical AI will enable autonomous systems that operate effectively in unstructured real-world environments.

The gap between leading AI systems and human performance will continue to narrow across an expanding range of tasks. This capability expansion will create new opportunities while raising important questions about employment, economic distribution, and human purpose.

Regulatory Maturation

By 2030, AI regulation will have matured significantly. The EU AI Act will be fully implemented, creating a template that other jurisdictions may follow. US federal AI legislation may emerge, potentially preempting the current patchwork of state laws. Industry-specific regulations will clarify compliance requirements for healthcare, finance, and other regulated sectors.

This regulatory maturation will increase compliance costs but also reduce uncertainty. Companies will have clearer guidance on what is permitted and required, enabling more confident AI investment decisions.

Workforce Transformation

The workforce implications of AI will become clearer by 2030. While AI will create more jobs than it destroys (a net positive of 78 million jobs according to current projections), the transition will be disruptive. New roles will emerge in AI development, governance, and human-AI collaboration. Existing roles will be transformed as AI augments human capabilities.

Education systems will adapt to prepare workers for an AI-augmented economy. Lifelong learning will become essential as skill requirements evolve rapidly. Companies that invest in workforce development will have significant competitive advantages.

Key Takeaways

- The AI market reached $900 billion in 2026 and is projected to grow to $4.22 trillion by 2035, representing one of the fastest-growing technology markets in history.

- Investment concentration is unprecedented—four companies captured 65% of global venture funding in Q1 2026, with OpenAI’s $122 billion round setting a new record.

- Enterprise adoption is accelerating, with 88% of companies now using AI in at least one business function and worker access to AI tools increasing 50% in 2025.

- Seven major trends are reshaping the market: agentic AI, physical AI, enterprise scale deployment, sovereign AI, regulatory expansion, capital concentration, and workforce transformation.

- The AI skills gap remains the biggest barrier to enterprise adoption, creating opportunities for education providers, consulting firms, and managed service providers.

Sources and Citations

- Precedence Research – Artificial Intelligence (AI) Market Size and Forecast 2026-2035: https://www.precedenceresearch.com/artificial-intelligence-market

- Crunchbase News – Q1 2026 Venture Capital Report: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026

- Exploding Topics – AI Statistics (January 2026): https://explodingtopics.com/blog/ai-statistics

- Deloitte – The State of AI in the Enterprise 2026: https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- Grand View Research – Artificial Intelligence Market Analysis: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- Kiteworks – AI Regulation in 2026 Business Compliance Guide: https://www.kiteworks.com/cybersecurity-risk-management/ai-regulation-2026-business-compliance-guide

- Microsoft – Global AI Adoption 2025 Report: https://www.microsoft.com/en-us/corporate-responsibility/topics/ai-economy-institute/reports/global-ai-adoption-2025/

- NVIDIA Blog – State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026