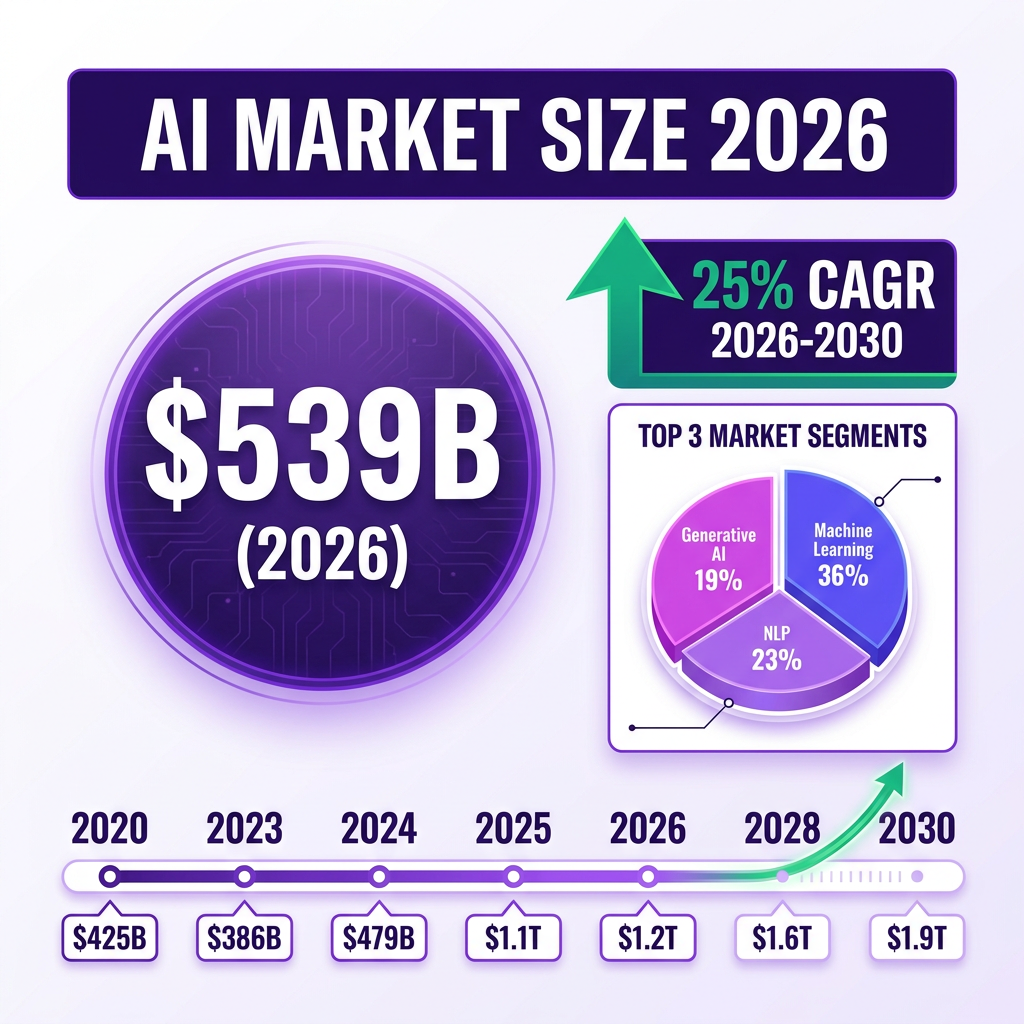

The artificial intelligence market has reached an inflection point in 2026. What began as experimental technology just a few years ago has now become the backbone of enterprise transformation across every industry. The numbers tell a compelling story: the global AI market is projected to reach $539.45 billion in 2026, representing a staggering 19% year-over-year growth from $390.91 billion in 2025. But this is just the beginning. By 2030, industry analysts forecast the market will exceed $2.1 trillion, driven by unprecedented enterprise adoption, breakthrough generative AI capabilities, and the emergence of agentic AI systems that can autonomously complete complex workflows.

For business leaders, investors, and technology professionals, understanding the AI market landscape in 2026 is no longer optional—it is essential for competitive survival. This comprehensive analysis examines the market size, growth trajectories, key players, emerging trends, challenges, and opportunities that will define the AI industry through the remainder of this decade.

Market Overview: The $539 Billion AI Ecosystem

The artificial intelligence market has evolved from a niche technology sector into a fundamental driver of global economic growth. In 2026, AI is no longer confined to tech companies—it has permeated healthcare, finance, manufacturing, retail, and virtually every other industry vertical. According to Grand View Research, the global AI market size was estimated at $390.91 billion in 2025 and is expected to reach $539.45 billion in 2026, marking one of the fastest growth rates in the technology sector’s history.

The market’s explosive growth is driven by several converging factors. First, enterprise adoption has doubled year-over-year, with 24% of organizations reporting full-scale AI implementation in 2026, up from just 12% in 2025. This acceleration reflects a fundamental shift in how businesses view AI—from experimental technology to mission-critical infrastructure. Digital leaders are driving this transformation, with 38% adoption rates compared to just 9% among digital laggards, according to TEKsystems’ State of Digital Transformation 2026 report.

Second, generative AI has emerged as a dominant force within the broader AI market. The global generative AI market grew 85% year-over-year in 2024—the highest single-year growth rate for any AI segment—and is projected to reach $109.37 billion by 2030, growing at a robust CAGR of approximately 37.9%. This explosive growth reflects the transformative impact of large language models, image generation systems, and multimodal AI tools that are reshaping content creation, software development, and customer service.

Third, AI infrastructure investments have reached unprecedented levels. Microsoft, Google, Amazon, and other hyperscalers are investing billions in AI data centers, with Microsoft alone committing over $80 billion to AI infrastructure in 2025. These investments are creating the computational backbone necessary for training increasingly sophisticated AI models and deploying them at scale.

The market segmentation reveals interesting dynamics. Machine learning remains the largest segment, accounting for approximately 36% of total AI market revenue, followed by natural language processing at 23%, and generative AI at 19%. However, generative AI is growing fastest, with its market share expected to increase significantly by 2030. Computer vision, autonomous systems, and AI robotics represent the remaining market segments, each showing strong growth trajectories driven by industry-specific applications.

Geographically, North America continues to dominate the AI market, with the United States accounting for over 80% of global private AI investment. The U.S. AI market was valued at $146.09 billion in 2024 and is projected to reach approximately $851.46 billion by 2034, growing at a CAGR of 19.33%. However, Asia-Pacific is emerging as the fastest-growing region, driven by massive investments in China, Japan, and South Korea, while Europe is establishing itself as a regulatory leader with the comprehensive EU AI Act.

Key Statistics and Market Data

The AI market in 2026 is defined by a series of remarkable statistics that illustrate both the technology’s rapid advancement and its growing economic impact. These numbers provide crucial context for understanding the scale and trajectory of AI adoption across industries.

Market Size and Growth: The global AI market is projected to reach $539.45 billion in 2026, up from $390.91 billion in 2025. Looking ahead, Statista forecasts the market will grow to $1.24 trillion by 2026 according to their comprehensive industry analysis, with some estimates projecting $1.85 trillion under moderate growth scenarios. By 2030, conservative estimates place the market at $2.16 trillion, with optimistic scenarios suggesting it could reach $3.79 trillion.

Generative AI Explosion: The generative AI market is experiencing particularly explosive growth. Valued at $16.87 billion in 2024, it is projected to reach $109.37 billion by 2030, representing a CAGR of 37.9%. In 2026 alone, the generative AI market is expected to grow by 79%, making it the fastest-growing segment within the broader AI ecosystem. This growth is driven by enterprise adoption of tools like ChatGPT, Claude, and specialized industry applications.

Enterprise Adoption Metrics: According to Exploding Topics research, 35.49% of people now use AI tools every day. This figure rises to 55% in the marketing and sales departments of tech companies. Nearly 1.8 billion people have used some kind of AI tool, demonstrating the technology’s rapid consumer adoption. Among enterprises, McKinsey reports that 65% of organizations are already using generative AI in at least one business function.

Investment and Funding: AI startups are now attracting a majority of global VC dollars—53% of all venture capital investment in 2025 went to AI companies, according to PitchBook data. Funding to foundational AI startups doubled in Q1 2026 compared to all of 2025. AI now accounts for approximately 35% of NYC VC activity, 30% of UK VC investment, and similar shares in other major tech hubs. Notable funding rounds include OpenAI’s continued growth to a $182.6 billion valuation and Anthropic reaching $60 billion.

Industry Vertical Breakdown: Healthcare remains the largest industry vertical for AI applications at 25.7% of total market share, followed by BFSI (banking, financial services, and insurance) at 18.5%, retail at 12.3%, manufacturing at 11.8%, and automotive at 9.2%. Each vertical is experiencing unique adoption patterns, with healthcare focusing on diagnostic AI and drug discovery, while financial services prioritize fraud detection and algorithmic trading.

Technology Segment Distribution: Machine learning platforms account for $446.28 billion in 2026, representing 36% of the total AI market. Natural Language Processing contributes $282.74 billion (23%), Computer Vision $223.66 billion (18%), Generative AI $236.8 billion (19%), AI Robotics $159.5 billion (13%), and Autonomous & Sensor Technology $123.06 billion (10%). These segments often overlap, with modern AI systems combining multiple technologies.

Regional Market Distribution: North America holds 42% of the global AI market, followed by Asia-Pacific at 31%, Europe at 19%, and the rest of the world at 8%. However, Asia-Pacific is growing fastest at a 28.5% CAGR, driven by massive government investments in China and South Korea’s AI initiatives.

AI Infrastructure Investment: NVIDIA maintains approximately 81% market share in AI data center chips, though AMD’s MI300X accelerator has captured roughly 10% of the market by 2026, up from 5% in 2024. Google Cloud reported $20.03 billion in Q4 2025 revenue, up 63% year-over-year, with CEO Sundar Pichai noting that revenue from AI-built products grew 800% over the prior year.

Productivity and ROI Metrics: According to NVIDIA’s State of AI report for 2026, 99% of telecommunications respondents said AI helped improve employee productivity, with a quarter reporting major or significant improvements. Enterprise AI implementations are showing 15-30% cost reductions with 6-18 month payback periods, according to Alice Labs research. However, S&P Global Market Intelligence reports that 42% of companies abandoned most of their AI initiatives in 2025, up from 17% in 2024, highlighting the challenges of successful implementation.

AI Investment by Sector: The banking sector leads AI investment with 18.5% of total AI spending, followed by retail at 12.3%, manufacturing at 11.8%, and healthcare at 25.7%. The automotive sector accounts for 9.2% of AI investment, with significant growth in autonomous vehicle development. Media and entertainment represents 6.4% of the market, driven by content generation and personalization applications. Government and defense spending on AI has increased to 8.1% of the total market, reflecting growing interest in AI for national security and public service applications.

AI Talent and Workforce Statistics: The global AI workforce has grown to approximately 4.2 million professionals in 2026, up from 2.8 million in 2024. However, demand continues to outpace supply, with an estimated 1.5 million unfilled AI positions globally. The average salary for AI engineers has reached $185,000 in the United States, with senior positions commanding $300,000 or more. Machine learning engineers, data scientists, and AI research scientists remain the most in-demand roles, while new positions like AI ethicists, prompt engineers, and AI product managers have emerged as critical hires.

AI Patent and Research Activity: Global AI patent filings reached 180,000 in 2025, a 45% increase from 2023. China leads in AI patent volume with 52% of global filings, followed by the United States at 18%, and the European Union at 8%. Academic research output has also surged, with over 150,000 AI-related papers published in 2025. The most active research areas include large language models, computer vision, reinforcement learning, and multimodal AI systems. Top research institutions include MIT, Stanford, Carnegie Mellon, Tsinghua University, and the University of Toronto.

Consumer AI Adoption Patterns: ChatGPT reached 100 million weekly active users in 2025, making it one of the fastest-growing consumer applications in history. Daily active users for major AI assistants have grown to 450 million globally. Voice AI adoption has increased significantly, with 68% of smartphone users regularly using voice assistants. AI-powered recommendation systems drive 35% of purchases on major e-commerce platforms. The average consumer now interacts with AI-powered services over 20 times per day, often without realizing it.

Major Trends Shaping the AI Market in 2026

The AI landscape in 2026 is being reshaped by seven major trends that are fundamentally altering how businesses develop, deploy, and benefit from artificial intelligence. Understanding these trends is crucial for organizations seeking to maintain competitive advantage in an increasingly AI-driven economy.

1. The Agentic AI Revolution: Perhaps the most significant trend of 2026 is the emergence of agentic AI—systems capable of autonomous decision-making and task completion. Unlike traditional AI models that respond to individual prompts, agentic AI can plan, execute multi-step workflows, and adapt to changing circumstances without human intervention. IBM’s 2026 AI trends report identifies this as the most significant shift, with enterprise leaders predicting that “agentic AI and other non-human identities will outnumber human users in the organization significantly.” Companies like Anthropic, OpenAI, and Google are racing to deploy agentic systems that can handle everything from customer service to software development.

2. Enterprise Adoption Doubles: Enterprise-wide AI implementation has doubled year-over-year, reaching 24% of organizations in 2026 compared to 12% in 2025. This acceleration reflects a maturation of AI tools, clearer ROI metrics, and growing competitive pressure. Digital leaders are pulling ahead dramatically, with 38% adoption rates versus 9% among laggards. The gap between AI leaders and laggards is widening, creating a “winner-takes-most” dynamic in many industries.

3. Generative AI Market Explosion: Generative AI continues its explosive growth trajectory, with the market expanding 79% in 2026. Beyond text generation, multimodal AI systems that can process and generate text, images, audio, and video simultaneously are becoming mainstream. OpenAI’s GPT-5, Google’s Gemini 2.0, and Anthropic’s Claude 4 are pushing the boundaries of what’s possible, while specialized models for healthcare, legal, and scientific applications are emerging.

4. AI Superfactories and Infrastructure: Microsoft has coined the term “AI superfactories” to describe the new generation of linked AI data centers that will drive down costs and improve efficiency. These massive infrastructure investments—totaling over $200 billion globally in 2025—are creating the computational backbone for the next wave of AI innovation. The rise of specialized AI chips from NVIDIA, AMD, and custom silicon from Google (TPU) and Amazon (Trainium) is reducing training costs and enabling larger, more capable models.

5. Shift from Experimentation to Production: According to IBM’s research, the most significant trend for 2026 is “the shift from AI experimentation and excitement to private and secure deployments with real ROI expectations within enterprises.” Companies are moving beyond pilots to production deployments, with 67% of digital leaders planning to increase AI spending in 2026. This shift requires new governance frameworks, MLOps practices, and change management strategies.

6. AI Regulation and Governance: The EU AI Act came into full force in 2025, establishing the world’s first comprehensive AI regulatory framework. The United States has issued executive orders on AI safety, while China has implemented its own AI governance rules. This regulatory landscape is creating new compliance requirements for AI developers and users, particularly for high-risk applications in healthcare, finance, and criminal justice. Organizations are investing heavily in responsible AI platforms and governance tools to ensure compliance.

7. Edge AI and Distributed Intelligence: As AI models become more efficient, they are increasingly deployed on edge devices—smartphones, IoT sensors, autonomous vehicles—rather than centralized data centers. This trend toward edge AI reduces latency, improves privacy, and enables AI applications in environments with limited connectivity. The AI edge computing market is projected to grow at a 35% CAGR through 2030, driven by autonomous vehicles, smart manufacturing, and healthcare monitoring applications.

8. AI-Powered Cybersecurity: The cybersecurity industry is increasingly turning to AI to combat sophisticated threats. AI-powered security systems can detect anomalies, predict attacks, and respond to breaches in real-time. The AI cybersecurity market is expected to reach $60 billion by 2028, growing at a 24% CAGR. Organizations are deploying AI for threat detection, fraud prevention, and automated incident response, with machine learning models trained on billions of security events.

9. Sustainable AI and Green Computing: As AI models grow larger and more computationally intensive, concerns about energy consumption and environmental impact have intensified. Data centers powering AI workloads now consume an estimated 4% of global electricity, prompting a push toward more efficient models and renewable energy sources. Companies like Google and Microsoft have committed to carbon-neutral AI operations, while researchers are developing smaller, more efficient models that maintain performance while reducing computational requirements.

10. AI Democratization and No-Code Tools: The barrier to entry for AI development is rapidly decreasing thanks to no-code and low-code AI platforms. These tools enable non-technical users to build AI applications without writing code, democratizing access to AI capabilities. Platforms like Bubble, Make, and Zapier now offer AI integrations, while specialized tools like Obviously AI and DataRobot provide drag-and-drop machine learning. This trend is expected to accelerate AI adoption among small and medium businesses that previously lacked technical resources.

Key Players and Competitive Landscape

The AI market in 2026 is dominated by a mix of established technology giants, well-funded startups, and emerging challengers from around the world. Understanding this competitive landscape is essential for businesses selecting AI partners and investors evaluating opportunities.

The Hyperscaler Dominance: Microsoft, Google (Alphabet), Amazon, and Meta continue to dominate the AI infrastructure and platform layers. Microsoft’s partnership with OpenAI and integration of Copilot across its product suite has positioned it as the enterprise AI leader. Google is leveraging its DeepMind research and Gemini models to compete aggressively, while Amazon’s AWS maintains a strong position in AI infrastructure services. These four companies collectively account for approximately 65% of global AI infrastructure spending.

OpenAI: With a valuation of $182.6 billion as of 2026, OpenAI remains the most valuable AI startup. Its GPT models power millions of applications, and ChatGPT has become synonymous with generative AI for consumers. The company’s partnership with Microsoft provides both funding and compute resources, while its API business serves enterprise customers. OpenAI’s 2026 focus is on agentic AI capabilities and multimodal models.

Anthropic: Valued at $60 billion, Anthropic has positioned itself as the safety-focused alternative to OpenAI. Its Claude models are known for longer context windows and more careful responses. The company’s Constitutional AI approach and emphasis on AI safety have attracted enterprise customers in regulated industries. Amazon’s $4 billion investment in Anthropic has strengthened its cloud partnership.

NVIDIA: While not an AI application company, NVIDIA’s dominance in AI chips makes it arguably the most important player in the AI ecosystem. With approximately 81% market share in AI data center chips, NVIDIA’s GPUs power the training and inference of virtually all major AI models. The company’s H100 and newer B200 chips are in such high demand that wait times extend for months. AMD is emerging as a challenger with its MI300X accelerator, capturing roughly 10% market share by 2026.

Chinese Competitors: Chinese AI companies are increasingly competitive on the global stage. DeepSeek’s R1 reasoning model took the world by storm in early 2025, demonstrating that Chinese labs can produce frontier-level AI. Baidu’s Ernie Bot, Alibaba’s Tongyi Qianwen, and ByteDance’s various AI products serve the massive Chinese market while expanding internationally. These companies benefit from government support and access to vast domestic data.

Enterprise AI Platforms: Companies like Databricks, Snowflake, and DataRobot are building comprehensive enterprise AI platforms that help organizations deploy and manage AI at scale. These platforms abstract away infrastructure complexity, providing tools for data preparation, model training, deployment, and monitoring. Salesforce’s Einstein, ServiceNow’s AI capabilities, and SAP’s AI offerings are embedding intelligence directly into enterprise workflows.

Vertical AI Specialists: A new generation of companies is building AI solutions for specific industries. In healthcare, companies like Tempus, PathAI, and Viz.ai are applying AI to diagnostics and drug discovery. In finance, Kensho (S&P Global), AlphaSense, and Dataminr provide AI-powered market intelligence. In legal, Harvey and Casetext (acquired by Thomson Reuters) are transforming legal research and document review.

Open Source Ecosystem: Meta’s Llama models, Mistral AI’s offerings, and community projects like Stable Diffusion are driving an open-source AI movement. These models provide alternatives to proprietary APIs, enabling organizations to run AI on their own infrastructure. The open-source ecosystem is particularly strong in Europe, where data privacy regulations favor self-hosted solutions.

Emerging Players and Unicorns: Beyond the established giants, a new generation of AI unicorns is reshaping the competitive landscape. Cohere, valued at $5.5 billion, specializes in enterprise language models. Character.AI reached a $1 billion valuation with its conversational AI platform. Midjourney has become synonymous with AI image generation, while Runway ML leads in AI video creation. Stability AI continues to advance open-source image generation. These companies represent the next wave of AI innovation, often focusing on specific use cases or modalities.

Hardware and Infrastructure Providers: Beyond NVIDIA and AMD, a broader ecosystem of hardware providers is emerging. Intel is investing heavily in AI accelerators with its Gaudi series. Startups like Cerebras and SambaNova are building specialized AI chips designed for training massive models. Cloud providers are developing custom silicon—Google’s TPUs, Amazon’s Trainium and Inferentia, and Microsoft’s Maia chips. These investments are driving down the cost of AI computation and increasing accessibility for organizations of all sizes.

Consulting and Services Ecosystem: The AI services market has grown to $85 billion in 2026, with major consulting firms building dedicated AI practices. Accenture’s AI practice now employs over 50,000 professionals, while McKinsey’s QuantumBlack has become a leader in AI implementation. Deloitte, PwC, and KPMG have all made significant AI investments, helping enterprises navigate the complex landscape of AI adoption. These firms provide critical bridge capabilities between AI technology and business value realization.

Challenges and Pain Points

Despite the AI market’s remarkable growth, significant challenges remain that threaten to slow adoption and limit value realization. Organizations that understand and proactively address these challenges will be better positioned to succeed in the AI-driven economy.

1. The Implementation Gap: The most significant challenge facing the AI market is the gap between experimentation and production deployment. According to S&P Global Market Intelligence, 42% of companies abandoned most of their AI initiatives in 2025, up dramatically from 17% in 2024. This high failure rate stems from several factors: unrealistic expectations, inadequate data infrastructure, lack of skilled personnel, and poor change management. Organizations often underestimate the complexity of integrating AI into existing workflows and overestimate the readiness of their data.

2. Data Quality and Governance: AI systems are only as good as the data they are trained on. Many organizations struggle with data silos, inconsistent formats, and poor data quality. Bias in training data remains a persistent problem—Amazon’s scrapped AI recruiting tool exhibited gender bias, while the COMPAS tool for predicting criminal recidivism showed racial bias. Establishing robust data governance frameworks, ensuring data quality, and addressing bias requires significant investment and organizational change.

3. Regulatory and Compliance Complexity: The evolving regulatory landscape presents significant challenges for AI developers and users. The EU AI Act’s risk-based approach requires different compliance measures depending on AI application type. Healthcare AI must navigate FDA regulations, while financial AI faces scrutiny from multiple regulatory bodies. Organizations must invest in AI governance tools, documentation practices, and compliance monitoring—costs that can offset AI’s efficiency gains.

4. Talent Shortage: The demand for AI talent far exceeds supply. Data scientists, ML engineers, and AI researchers command premium salaries, making it difficult for smaller organizations to compete with tech giants. According to industry surveys, 67% of organizations cite talent shortages as a major barrier to AI adoption. This challenge is particularly acute for specialized roles like AI ethics specialists, MLOps engineers, and domain experts who can bridge technical and business requirements.

5. Trust and Explainability: Only 8.5% of people believe they can “always trust” AI Overviews when searching online, according to Exploding Topics research. This trust gap extends to enterprise AI deployments, where decision-makers need to understand how AI systems arrive at recommendations. The “black box” nature of deep learning models creates challenges in regulated industries where explainability is required. Techniques like explainable AI (XAI) and model interpretability are advancing but add complexity to AI development.

6. Infrastructure Costs: Training and running large AI models requires significant computational resources. While costs are declining, deploying AI at scale remains expensive. Organizations must balance the benefits of more capable models against infrastructure costs, often making difficult trade-offs between model performance and operational efficiency. The energy consumption of AI data centers is also coming under scrutiny, with sustainability concerns adding pressure to optimize efficiency.

7. Integration Complexity: Integrating AI into existing enterprise systems remains a significant challenge. Legacy systems, disparate data sources, and complex workflows create friction in AI deployment. Many organizations struggle with API limitations, data format incompatibilities, and the need for extensive customization. Successful AI implementation often requires substantial investment in integration infrastructure, middleware, and custom development.

8. Ethical and Social Concerns: As AI becomes more pervasive, concerns about job displacement, privacy erosion, and algorithmic bias are growing. The World Economic Forum estimates that AI could displace 85 million jobs by 2025 while creating 97 million new ones—a net positive but requiring massive workforce transition. Organizations must navigate these concerns carefully, investing in reskilling programs and transparent AI governance to maintain public trust and social license to operate.

Opportunities and Growth Strategies

Despite the challenges, the AI market presents extraordinary opportunities for organizations that approach adoption strategically. The following growth strategies have proven successful for AI leaders and offer a roadmap for organizations at various stages of AI maturity.

1. Focus on High-ROI Use Cases: Successful AI implementations typically start with well-defined use cases that offer clear, measurable ROI. Customer service automation, document processing, code generation, and predictive maintenance consistently deliver strong returns. Organizations should prioritize use cases where AI can augment human capabilities rather than attempting full automation immediately. This approach reduces risk while building organizational AI capabilities.

2. Invest in Data Infrastructure: Data is the foundation of AI success. Organizations should invest in modern data platforms that enable data integration, quality management, and governance. Cloud-based data warehouses, data lakes, and lakehouse architectures provide the scalability and flexibility needed for AI workloads. Establishing clear data ownership, quality standards, and access controls is essential before scaling AI initiatives.

3. Build AI Centers of Excellence: Organizations that create centralized AI offices or centers of excellence benefit from effective use of specialized expertise and collaboration across initiatives. These centers provide governance, share best practices, and ensure consistent approaches to AI development and deployment. They also serve as hubs for training, helping to address the talent shortage by upskilling existing employees.

4. Embrace Partnership Ecosystems: Given the complexity of AI technology, most organizations benefit from partnerships rather than attempting to build everything in-house. Cloud providers offer AI platforms and infrastructure, specialized vendors provide industry-specific solutions, and consulting firms offer implementation expertise. Strategic partnerships can accelerate time-to-value while reducing risk.

5. Prioritize Responsible AI: Organizations that proactively address AI ethics, bias, and transparency build trust with customers, employees, and regulators. Implementing responsible AI practices—including fairness testing, explainability features, and human oversight—reduces regulatory risk and enhances AI system acceptance. The World Economic Forum recommends responsible AI by design practices as a key strategy for accelerating adoption.

6. Plan for Agentic AI: Forward-thinking organizations are already experimenting with agentic AI capabilities. These systems can automate complex workflows, from software development to customer service to research. While still emerging, agentic AI represents the next frontier of AI value creation. Organizations should begin identifying processes that could benefit from autonomous AI agents and building the infrastructure to support them.

7. Develop AI Literacy Programs: Successful AI adoption requires more than technical implementation—it demands organizational culture change. Companies that invest in AI literacy programs for employees at all levels see higher adoption rates and better outcomes. Training programs should cover AI capabilities and limitations, ethical considerations, and practical applications relevant to each role. Organizations with strong AI literacy programs report 40% higher employee satisfaction with AI tools and 25% better ROI on AI investments.

8. Create Feedback Loops: AI systems improve with feedback, but many organizations fail to establish systematic feedback mechanisms. Successful companies create closed-loop systems where user feedback, performance metrics, and business outcomes continuously inform model improvements. This approach requires investment in monitoring infrastructure, feedback collection mechanisms, and rapid iteration processes. Organizations with mature feedback loops achieve 3x better model performance over time compared to those with static deployments.

Case Studies and Success Stories

Real-world implementations demonstrate how leading organizations are translating AI investments into measurable business results. These case studies illustrate best practices and provide templates for successful AI adoption.

Case Study 1: Nasdaq’s AI Platform: Nasdaq, one of the world’s premier stock exchanges, built a comprehensive AI platform to optimize internal operations and enhance external products. The platform improves functionality and user experience while streamlining internal work processes. By leveraging AI for market surveillance, Nasdaq has significantly improved its ability to detect market manipulation and insider trading. The implementation demonstrates how financial services firms can deploy AI for both operational efficiency and regulatory compliance.

Case Study 2: HCLTech’s GenAI Lab for Pharma: HCLTech helped accelerate innovation in research and drug development for a global pharmaceutical company by establishing a GenAI Lab. This facility enabled the company to effectively develop and test AI proofs of concept, identify and prioritize safe and compliant use cases, and ultimately reduce the turnaround time required for pilots and prototypes. The lab approach allowed the pharma company to explore high-value use cases while maintaining strict compliance with healthcare regulations.

Case Study 3: European Manufacturing AI Transformation: A leading European manufacturer implemented AI across its production facilities, achieving 15-30% cost reductions with a 6-18 month payback period. The company deployed computer vision for quality control, predictive maintenance for equipment, and optimization algorithms for supply chain management. Change management investment was 9x the technology cost, highlighting the importance of organizational transformation alongside technology deployment.

Case Study 4: Telecommunications Productivity Gains: In NVIDIA’s State of AI in Telecommunications report, 99% of respondents said AI helped improve employee productivity, with a quarter reporting major or significant improvements. A major telecom provider deployed AI for network optimization, customer service automation, and predictive maintenance. The implementation reduced network downtime by 40% and improved customer satisfaction scores by 25%.

Case Study 5: Retail and CPG Optimization: A global consumer packaged goods company implemented AI for demand forecasting, inventory optimization, and personalized marketing. The AI system analyzes point-of-sale data, weather patterns, and social media trends to predict demand with 85% accuracy, reducing waste by 30% and improving stock availability by 20%. The implementation required significant data integration efforts but delivered measurable ROI within 12 months.

Case Study 6: Healthcare Diagnostic AI: A leading hospital network deployed AI-powered diagnostic imaging across its radiology department. The system assists radiologists in detecting anomalies in X-rays, CT scans, and MRIs, reducing diagnostic time by 45% and improving accuracy by 12%. The AI system has been particularly effective in early cancer detection, identifying potential malignancies that might have been missed in initial screenings. The implementation required extensive validation and regulatory approval but has now been expanded to 15 hospitals in the network.

Case Study 7: Financial Services Fraud Detection: A major credit card company implemented an AI-powered fraud detection system that analyzes transaction patterns in real-time. The system reduced false positives by 60% while increasing fraud detection rates by 35%. Customer satisfaction improved significantly as legitimate transactions were no longer incorrectly flagged. The AI system processes over 10,000 transactions per second and has saved the company an estimated $250 million in fraud losses annually.

Future Outlook and Predictions

Looking beyond 2026, the AI market is poised for continued explosive growth, with several key developments expected to shape the industry through 2030 and beyond.

Market Projections: By 2027, the global AI market is projected to reach $1.42 trillion, growing to $1.64 trillion by 2028 and $2.16 trillion by 2030 under moderate growth scenarios. Optimistic scenarios suggest the market could reach $3.79 trillion by 2030 if adoption accelerates faster than expected. The generative AI segment is expected to maintain the highest growth rate, potentially reaching $442 billion by 2031.

Technological Milestones: According to the AI 2027 forecast from the AI Futures Project, AI systems are expected to achieve superhuman coding capabilities by early 2027, followed by superhuman AI research capabilities by mid-2027. These milestones could trigger an acceleration in AI development as AI systems begin to improve themselves. Multimodal AI that seamlessly integrates text, image, audio, and video will become standard, while AI reasoning capabilities continue to advance.

Enterprise Transformation: By 2030, AI is expected to be embedded in virtually every enterprise application and workflow. The distinction between “AI companies” and “traditional companies” will become meaningless as AI becomes as ubiquitous as electricity. Organizations that fail to adapt will face existential competitive threats from AI-native competitors.

Regulatory Evolution: The regulatory landscape will continue evolving, with the EU AI Act serving as a template for other jurisdictions. The United States is expected to pass comprehensive AI legislation, while China will likely expand its AI governance framework. International coordination on AI safety and standards will become increasingly important as AI systems become more powerful.

Workforce Transformation: AI will fundamentally reshape the workforce, automating routine cognitive tasks while creating new roles for AI trainers, explainability specialists, and human-AI interaction designers. The World Economic Forum predicts that while AI will displace some jobs, it will create more new roles than it eliminates—but the transition will require massive reskilling efforts.

Scientific Revolution: AI is expected to accelerate scientific R&D across multiple domains. In drug discovery, AI-designed molecules are already entering clinical trials. In materials science, AI is discovering new compounds with novel properties. In physics and mathematics, AI systems are assisting with proofs and predictions. By 2030, AI may be contributing to major scientific breakthroughs at an unprecedented pace.

AI and Climate Solutions: AI is increasingly being deployed to address climate change and environmental challenges. AI-powered climate models are improving prediction accuracy, while optimization algorithms are reducing energy consumption in buildings and transportation. AI is being used to monitor deforestation, optimize renewable energy grids, and develop new materials for carbon capture. The AI for climate solutions market is projected to reach $12 billion by 2030, representing a significant growth opportunity within the broader AI ecosystem.

Personalized AI Assistants: By 2028, most professionals are expected to have personalized AI assistants that understand their work patterns, preferences, and communication styles. These assistants will manage schedules, draft communications, conduct research, and provide proactive recommendations. The market for personal AI assistants is projected to grow to $45 billion by 2030, with enterprise adoption driving much of this growth.

Key Takeaways

- The global AI market will reach $539.45 billion in 2026, growing to over $2.1 trillion by 2030

- Enterprise AI adoption has doubled year-over-year to 24%, with digital leaders at 38% adoption

- Generative AI is the fastest-growing segment, expanding 79% in 2026 with a 37.9% CAGR through 2030

- Agentic AI represents the next frontier, with autonomous AI systems capable of complex task completion

- North America dominates with 42% market share, but Asia-Pacific is growing fastest at 28.5% CAGR

- 42% of AI initiatives fail, highlighting the importance of strategic implementation and change management

- Successful AI adoption requires investment in data infrastructure, talent, and responsible AI practices

- By 2030, AI will be embedded in virtually every enterprise application and workflow

Sources and Citations

- Grand View Research – Artificial Intelligence Market Size Report 2026: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-market

- AI Statistics 2026 – Global Data & Trends: https://aistatistics.ai

- Statista AI Market Forecast: https://www.statista.com/outlook/tmo/artificial-intelligence/worldwide

- IBM AI Tech Trends Predictions 2026: https://www.ibm.com/think/news/ai-tech-trends-predictions-2026

- Microsoft – What’s Next in AI: 7 Trends to Watch in 2026: https://news.microsoft.com/source/features/ai/whats-next-in-ai-7-trends-to-watch-in-2026

- Exploding Topics – AI Statistics January 2026: https://explodingtopics.com/blog/ai-statistics

- NVIDIA State of AI Report 2026: https://blogs.nvidia.com/blog/state-of-ai-report-2026

- Crunchbase – Q1 2026 Venture Funding Records: https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026

- Forbes AI 50 List 2026: https://www.forbes.com/lists/ai50

- CompaniesHistory – AI Market Share by Company 2026: https://www.companieshistory.com/ai-market-share-by-company

- TEKsystems – Enterprise AI Adoption 2026: https://www.teksystems.com/en/insights/infographic/ai-adoption-enterprise-2026

- Deloitte – State of AI in the Enterprise 2026: https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- World Economic Forum – AI Adoption Strategies: https://www.weforum.org/stories/2026/02/5-strategies-accelerate-responsible-ai-adoption

- Alice Labs – AI Implementation Case Studies 2026: https://alicelabs.ai/en/insights/ai-implementation-case-studies

- Epoch AI – What Will AI Look Like in 2030: https://epoch.ai/publications/what-will-ai-look-like