The creator economy has officially entered its golden era. What started as a handful of YouTubers and bloggers experimenting with monetization has exploded into a $250+ billion global industry that is fundamentally reshaping how we think about work, entrepreneurship, and digital commerce. As we navigate through 2026, the landscape continues to evolve at breakneck speed—driven by AI innovation, platform consolidation, and a new generation of creators who think like founders, not freelancers.

Consider this: 1 in 40 people worldwide now identify as creators. That is more than 200 million individuals who have turned content creation from a hobby into a livelihood. The Goldman Sachs Research team projects the creator economy could approach half a trillion dollars by 2027, representing one of the fastest-growing sectors in the global economy. But beyond the headline figures, something more profound is happening. The fundamental nature of content creation is changing. The barriers to entry have never been lower, yet the bar for success has never been higher.

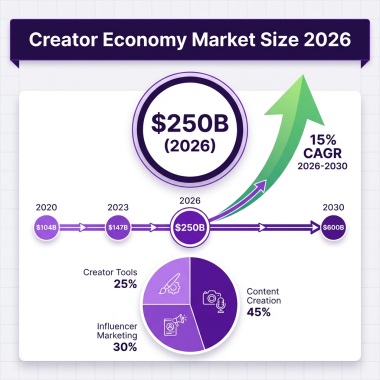

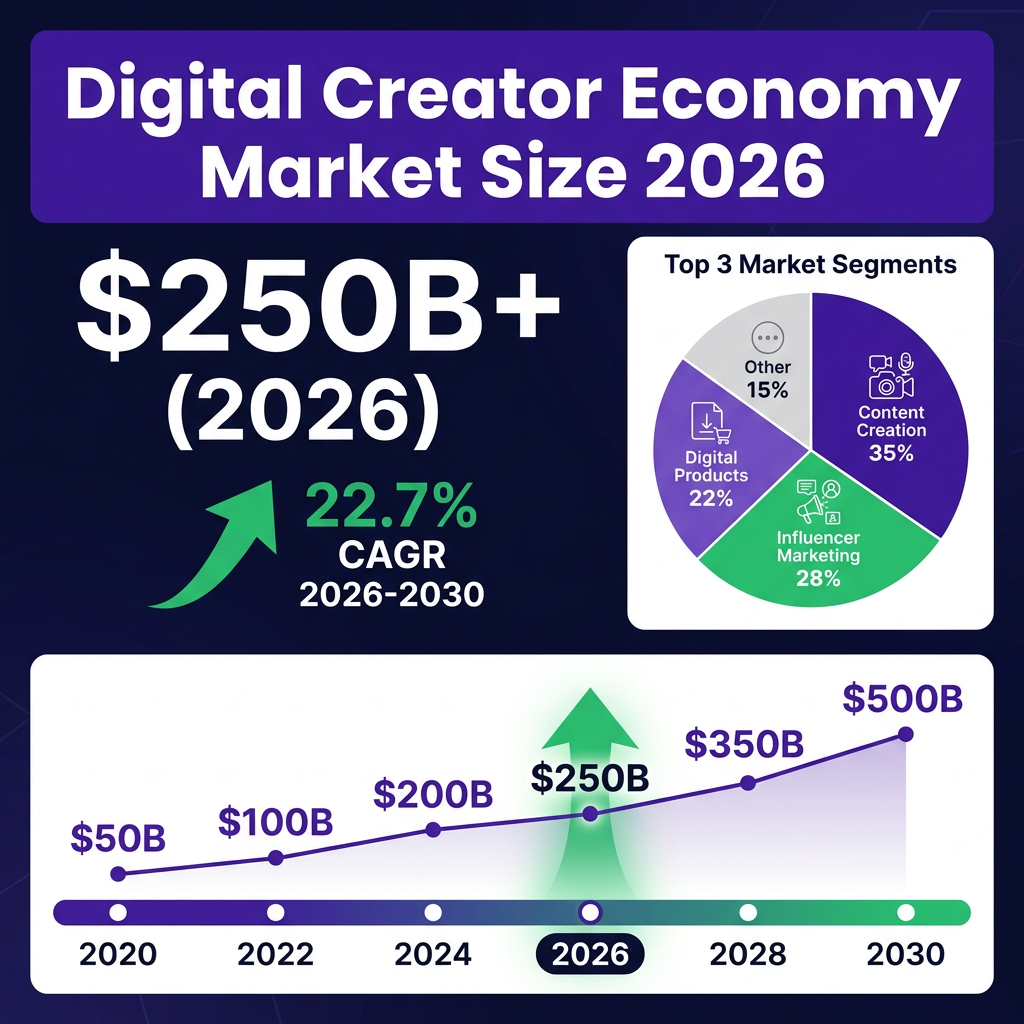

Market Overview: The $250 Billion Creator Ecosystem

The global creator economy has undergone a remarkable transformation over the past decade. According to market research from Coherent Market Insights, the creator economy was valued at approximately $200 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 22.7%, putting it on track to surpass $800 billion by the early 2030s. This growth trajectory positions the creator economy as one of the most significant economic shifts of our generation.

The numbers tell a compelling story of exponential growth. In 2020, the creator economy was valued at roughly $50 billion. By 2023, it had doubled to $100 billion. The pandemic accelerated this growth as millions of people turned to content creation as both a creative outlet and a source of income during uncertain times. What emerged was not just a trend, but a fundamental restructuring of how value is created and captured in the digital age.

Goldman Sachs Research offers an even more bullish projection, suggesting the creator economy could approach $480-500 billion by 2027. This forecast is based on several converging factors: the continued professionalization of creators, the expansion of monetization tools across platforms, and the integration of e-commerce directly into content experiences. The investment bank identifies six key enablers that create a “flywheel effect” for platform growth: scale (large global user bases), capital access, AI-powered recommendation engines, effective monetization tools, robust data and analytics, and integrated e-commerce options.

Regional distribution shows North America leading in creator economy market share, followed by Europe and Asia-Pacific. However, the fastest growth is occurring in emerging markets where mobile-first internet access has democratized content creation. Countries like India, Brazil, and Nigeria are producing creators who are building global audiences from local contexts, challenging the historical dominance of Western creators.

The market segmentation reveals interesting patterns. Content creation tools and platforms account for approximately 35% of the market value, driven by subscriptions to editing software, analytics platforms, and creator-focused SaaS products. Influencer marketing represents roughly 28% of the market, as brands increasingly allocate budget to creator partnerships. Digital products and direct monetization account for 22%, including courses, templates, memberships, and virtual goods. The remaining 15% comprises advertising revenue shares, tipping, and emerging monetization models.

Key Statistics and Data Points Every Creator Should Know

Understanding the creator economy requires diving deep into the data that defines it. The statistics for 2026 paint a picture of an industry in transition—from a hobbyist-driven space to a professionalized ecosystem where serious business outcomes are the norm rather than the exception.

Creator Demographics and Scale: There are now over 200 million people worldwide who identify as content creators. Of these, approximately 2 million earn enough to consider creation their primary profession. The IAB reports that U.S. annual creator economy ad spend alone reached $37.1 billion in 2025 and is projected to increase to $43.9 billion in 2026—a 18% year-over-year increase that significantly outpaces traditional media growth rates.

Operating Models: According to Circle’s 2026 Community Trends Report, 48% of creators operate completely solo, managing their communities, content, and monetization independently. 19% lead small community-focused teams, often blending content production with operations and member support. 15% work as hired community managers for brands or other creators. This distribution highlights that while solo entrepreneurship remains dominant, team-based creator businesses are increasingly common at the higher revenue tiers.

Monetization Patterns: 88% of community builders now monetize through memberships or subscriptions, representing a fundamental shift away from advertising-dependent models. 56% of creators launched their community businesses in the last two years (2024-2025), indicating that community-building has become a near-default strategy rather than a late-stage optimization. Interestingly, 44% of creator communities have between 1 and 100 members, showing that much of the growth is happening at smaller, more intimate scales where retention and transformation matter more than raw reach.

Platform Engagement: Despite the growth in creator numbers, 2025 saw widespread drops in engagement across all major platforms. Social media users are spending less time on apps for the first time in nearly a decade, driven by attention fatigue and platform saturation. Instagram’s top ranking signals now prioritize watch time and shares over likes and comments. YouTube emphasizes watch time, click-through rate, and user engagement history. TikTok focuses on watch time, completion rate, shares, and comments. These algorithmic shifts reward quality over quantity, forcing creators to adapt their content strategies.

Brand Partnership Dynamics: 92% of marketers intend to work with both macro (100,000 to 500,000 followers) and micro (5,000 to 100,000 followers) influencers in 2026, according to Linqia’s State of Influencer Marketing report. This demonstrates that a one-size-fits-all approach no longer works—a combination strategy drives better results. 60% plan to work with mega influencers (500,000 to 5 million followers), while 58% intend to partner with nano influencers (up to 5,000 followers). Only 29% are aiming to work with celebrities, signaling a shift toward authentic creator partnerships over traditional star power.

AI and Creator Content: 79% of marketers increased ad spend on generative AI creator content in 2025, and the same percentage plan to increase spend again in 2026. 76% of marketers agree that AI will increase total creator economy ad spend, while 77% plan to divert budgets away from traditional creator marketing to AI-generated content. This represents one of the most significant disruptions to the creator economy since its inception.

Revenue Distribution: The creator economy follows a power law distribution where a small percentage of creators capture the majority of revenue. The top 10 Substack authors collectively make $40 million per year. MrBeast, the highest-earning creator, generates over $100 million annually across his various ventures. However, the median creator income remains modest—most creators earn less than $1,000 per year from their content, highlighting the gap between hobbyist and professional success.

Seven Major Trends Shaping the Digital Creator Economy in 2026

The creator economy in 2026 is defined by seven transformative trends that are reshaping how creators build audiences, monetize their work, and structure their businesses. Understanding these trends is essential for anyone looking to succeed in this rapidly evolving landscape.

1. AI-Assisted Content Creation Goes Mainstream

The integration of AI tools into the creative workflow is no longer experimental—it is expected. From AI-powered video editing to generative writing assistants, creators are leveraging technology to produce more content faster without sacrificing quality. This democratization of production capabilities is enabling smaller creators to compete with larger operations that previously had exclusive access to professional tools and teams.

The most successful creators in 2026 view AI not as a replacement for human creativity but as an amplifier of it. They are using AI tools to handle routine tasks—transcription, basic editing, content repurposing, thumbnail generation—while focusing their human attention on strategy, storytelling, and authentic engagement. Tools like Descript, Runway ML, and various GPT-based writing assistants have become standard in the creator tech stack.

This trend is accelerating the professionalization of the creator economy. Solo creators can now produce content that rivals small production studios, blurring the lines between amateur and professional content. The barrier to high-quality production has been effectively eliminated, shifting competition from production capability to creative vision and audience connection.

2. The Rise of AI-Generated Influencers

Perhaps the most transformative development in the creator economy is the emergence of fully AI-generated influencers. These virtual personalities, powered by sophisticated image generation and character development technologies, are attracting millions of followers and commanding significant brand deals. Virtual influencers like Lil Miquela have paved the way, but 2026 has seen an explosion of AI creators across niches.

AI creators offer several compelling advantages for brands: consistency (they never have bad days, never age unexpectedly, and never get embroiled in personal scandals), scalability (a single AI persona can produce content across multiple languages and formats simultaneously), creative control (brands have complete control over messaging and presentation), and innovation (they can embody aesthetics and personalities that push beyond human limitations).

However, this trend also raises important questions about authenticity, disclosure, and the future of human creators. Regulatory frameworks are beginning to emerge requiring clear labeling of AI-generated content. The most savvy brands are finding ways to blend AI efficiency with human authenticity, using virtual influencers for specific campaigns while maintaining relationships with human creators for authentic community building.

3. Creator and Entrepreneur Become Synonymous

The line between creator and entrepreneur is becoming increasingly blurred. Most entrepreneurs are now creators building their personal brand, and most creators are entrepreneurs using their audience as a distribution channel. Rather than relying on unpredictable platform payouts or brand deals, creators are building diversified income streams they own and control.

We are seeing more creators launch product lines, build teams, raise capital, and step into roles traditionally held by founders and C-suite executives. MrBeast, Emma Chamberlain, and Alex Cooper are prime examples—running multi-seven-figure businesses powered by everything from digital products and consumer lines to podcasts, streaming deals, and merchandise. They are not just “posting online.” They are building empires.

This shift is reflected in how creators structure their businesses. The solo creator working from their bedroom is giving way to professionalized operations with teams including editors, managers, marketers, and operations specialists. Creators are incorporating, raising venture capital, and building infrastructure that can scale beyond their personal brand. The creator economy is becoming the entrepreneurship economy.

4. Multi-Platform Strategy Becomes Essential

Where once YouTube and Instagram dominated, today’s creators must navigate an increasingly complex ecosystem. TikTok, Twitch, Patreon, Substack, OnlyFans, LinkedIn, and dozens of other platforms each offer unique opportunities and challenges. Smart creators are building multi-platform strategies that maximize reach while maintaining authentic connections with their audiences.

The platform fragmentation trend is driven by several factors. First, algorithm changes on major platforms have made reach increasingly unpredictable. Second, different platforms serve different purposes in the creator funnel—TikTok for discovery, YouTube for long-form content, Instagram for community, Substack for owned relationships. Third, platform risk has become a real concern as creators witness bans, policy changes, and the potential shutdown of platforms like TikTok in certain markets.

Successful creators in 2026 treat each platform as a distinct channel with its own content strategy, rather than simply cross-posting the same content everywhere. They understand that platform-native content outperforms repurposed content, and they invest in understanding the unique culture and algorithm of each platform they use.

5. Direct Monetization Overtakes Advertising

The shift from advertising-dependent to direct monetization models continues to accelerate. Subscriptions, memberships, digital products, and direct fan contributions now represent a larger share of creator income than ever before. This shift gives creators more control over their destiny but also requires them to develop new skills in community building and product development.

Platforms like Patreon, Substack, and Stan Store have made it easier than ever for creators to monetize directly. Substack now has over 20 million monthly active subscribers—more than double that of 2024—with 17,000 paid creators earning income through the platform. The top 10 Substack authors collectively make $40 million per year, demonstrating the earning potential of owned audience relationships.

This trend reflects a broader shift in consumer behavior. Audiences are increasingly willing to pay for content they value directly, rather than accepting the implicit transaction of attention for free content supported by advertising. Creators who can deliver genuine transformation, entertainment, or education are finding that direct monetization not only pays better but also creates more sustainable businesses.

6. Community-Led Business Models Emerge

Community is becoming the core of creator businesses, not just an extension of them. Circle’s data shows that 18,000+ active communities are now supported on their platform, underscoring a steady migration toward spaces where creators control access, monetization, and member relationships. For many creators, communities are no longer a side project—they are the whole business.

This shift is both recent and accelerating. 56% of creators launched their community in the last couple of years (2024-2025), indicating that community-building has become a near-default move for newer creator businesses. Interestingly, scale is not the defining factor—44% of communities have between 1 and 100 members, showing that much of this growth is happening at smaller scales where retention, outcomes, and recurring revenue matter more than rapid audience expansion.

The community-led model offers several advantages: predictable recurring revenue through memberships, higher engagement rates than social platforms, the ability to deliver transformation rather than just content, and ownership of the relationship that cannot be taken away by platform algorithm changes. 69% of community builders say member transformation is their top growth strategy, signaling a shift from attention-based to outcome-based value creation.

7. Professionalization and Consolidation

The creator economy is entering what Forbes calls “the era of consolidation.” For most of its existence, the creator economy expanded without much structure. Independent creators, boutique managers, influencer agencies, and software vendors all grew at the same time, often in parallel rather than in coordination. That fragmentation helped the market scale quickly, but it also postponed the operational discipline that large brand budgets ultimately require.

In 2026, that phase is over. Creator and influencer marketing now represent a permanent line item in global marketing plans, not an experimental channel. Brands want reliability, repeatability, and measurable performance. Creators want partners who can help build lasting businesses, not just secure the next deal. Those expectations are reshaping the industry.

The most visible shift is happening in talent management. The traditional manager operated as a relationship-driven broker, focused on negotiating deals and maximizing short-term earnings. That approach is increasingly outdated. Leading creators now function like multi-platform media brands. Supporting that level of ambition requires centralized legal, financial, production, and data capabilities. Consolidated talent platforms are better positioned to provide that support, spreading risk across a portfolio of creators and investing in shared infrastructure.

Key Players and the Competitive Landscape

The creator economy ecosystem comprises several categories of key players, each playing a distinct role in supporting creator success. Understanding this landscape is crucial for creators looking to build their businesses and for brands looking to navigate the space effectively.

Platform Giants

The major social platforms remain the foundation of the creator economy. YouTube continues to lead in creator payouts through its Partner Program, having paid out over $70 billion to creators since its inception. The platform’s long-form content model and search-based discovery make it particularly valuable for educational and entertainment creators building lasting libraries of content.

Instagram has doubled down on personalization, giving users more control over what they want to see while prioritizing richer engagement signals like watch time and shares. The platform’s shopping features and Reels monetization have made it essential for lifestyle, fashion, and consumer product creators.

TikTok remains the discovery engine of the creator economy, with its algorithm capable of catapulting unknown creators to millions of views overnight. Despite ongoing regulatory uncertainty in the U.S., 26% of brands and 27% of agencies intend to use TikTok the most for creator marketing in 2026, according to CreatorIQ data.

Substack has emerged as the leading platform for newsletter-first creators, with over 20 million monthly active subscribers and 17,000 paid creators. The platform’s expansion into video, podcasts, and community features has made it a comprehensive home for creators building owned audiences outside social media algorithms.

Monetization Infrastructure

Beyond the social platforms, a robust ecosystem of monetization tools has emerged. Patreon pioneered the membership model for creators and continues to be a major player, though it faces increasing competition from platform-native monetization features. Stan Store has gained traction as an all-in-one creator store platform, enabling creators to sell digital products, courses, and memberships from a single link.

Circle has positioned itself as the leading community platform for creators, supporting 18,000+ active communities with tools for courses, live events, and member engagement. The platform’s focus on community-led business models has resonated with creators looking to build sustainable recurring revenue.

Gumroad, Teachable, Kajabi, and Podia compete in the digital products space, each offering different trade-offs between features, pricing, and ease of use. The choice between these platforms often depends on the creator’s specific needs—courses, downloads, coaching, or community.

Talent Management and Agencies

The talent management landscape is consolidating as creator businesses become more complex. Traditional influencer agencies are evolving into full-service creator economy firms, offering services spanning brand partnerships, IP development, product launches, and investment advisory.

Rare Global, founded by Ashley Villa, represents the new breed of creator management—treating creators as founders and providing operating partner-level support. Similarly, United Talent Agency (UTA), Creative Artists Agency (CAA), and other traditional talent agencies have built dedicated creator divisions to serve this growing market.

On the brand side, influencer marketing agencies like Billion Dollar Boy, Obviously, and The Influencer Marketing Factory have scaled to serve enterprise clients with creator campaigns that rival traditional advertising in sophistication and measurement.

Creator-Led Investment

A fascinating development in the creator economy is the emergence of creators as investors in the ecosystem itself. Top creators are backing creator platforms, funding other creator brands, and investing in the infrastructure that powers the industry.

Steven Bartlett and GaryVee backed Stan’s largest creator-led funding round. Bartlett has continued investing heavily in other creators’ brands as part of his vision to build the “Disney of the creator economy,” including seven-figure investments in creator-led businesses. This trend of creators investing in creators is creating a flywheel effect that strengthens the entire ecosystem.

Challenges and Pain Points in the Creator Economy

Despite its growth and promise, the creator economy faces significant challenges that creators, platforms, and brands must navigate. Understanding these pain points is essential for building sustainable creator businesses.

1. Platform Risk and Algorithm Dependency

The most significant challenge facing creators is platform risk. Creators who build their entire business on a single platform are vulnerable to algorithm changes, policy updates, account bans, and platform shutdowns. The potential TikTok ban in the U.S. has highlighted this risk, with creators who built massive followings on the platform facing the potential loss of their primary distribution channel.

Algorithm changes can decimate a creator’s reach overnight. Instagram’s shift toward video and away from photos hurt many creators who had built their audiences on static content. YouTube’s algorithm updates have similarly disrupted creator businesses throughout the platform’s history. This volatility makes it difficult for creators to plan and invest in their businesses with confidence.

2. Creator Burnout and Mental Health

Creator burnout has become an epidemic in the industry. The pressure to consistently produce content, engage with audiences, and stay relevant creates unsustainable workloads. Unlike traditional jobs, the creator economy never sleeps—there is always more content to make, another comment to respond to, another trend to capitalize on.

The personal nature of creator work adds another layer of difficulty. Creators are the product, which means criticism feels personal. The constant exposure to public opinion takes a toll on mental health. Many successful creators have taken extended breaks or quit entirely due to burnout, despite having large audiences and significant earning potential.

3. Income Inequality and Sustainability

The creator economy follows a stark power law distribution where a small percentage of creators capture the majority of revenue. While headlines focus on creators earning millions, the median creator income remains modest. Most creators earn less than $1,000 per year from their content, making it difficult to sustain creation as more than a hobby.

This inequality creates a “middle class crunch” where creators who have achieved some success but haven’t broken through to the top tier struggle to make their businesses sustainable. They have enough audience to demand significant time investment but not enough to generate reliable income that justifies full-time commitment.

4. Measurement and Attribution Challenges

Despite advances in analytics, measuring the true impact of creator marketing remains challenging. Attribution across platforms, understanding the incremental value of creator partnerships, and comparing creator ROI to other marketing channels are ongoing struggles for brands.

Creators themselves often lack access to the data they need to optimize their content and demonstrate value to brand partners. Platform analytics can be limited, and third-party measurement tools are often expensive or incomplete. This data gap makes it harder for creators to improve and for brands to invest confidently.

Opportunities and Growth Strategies for Creators

Despite the challenges, the creator economy offers unprecedented opportunities for those who approach it strategically. Here are the key growth strategies that successful creators are employing in 2026.

1. Build Owned Audiences

The most important strategy for creator sustainability is building owned audiences outside of social platforms. Email lists, community memberships, and direct relationships with fans provide insurance against platform risk and typically generate higher revenue per follower than platform-dependent monetization.

Creators like Jennifer Chou exemplify this strategy. When she was unexpectedly laid off from her full-time job, having an audience she owned gave her something to fall back on, opening doors to new opportunities when she needed them most. Building a personal brand creates options that no employer, platform, or AI innovation can take away.

2. Diversify Revenue Streams

Successful creators in 2026 have multiple revenue streams rather than relying on a single source. The typical diversified creator business includes a mix of brand partnerships, affiliate marketing, digital products, memberships, coaching or consulting, and potentially physical products or software.

This diversification provides stability—when one revenue stream underperforms, others can compensate. It also allows creators to serve different audience segments at different price points, from free content for broad reach to high-ticket coaching for committed fans.

3. Focus on Transformation, Not Just Content

The creators who are thriving in 2026 have shifted from delivering content to delivering transformation. Rather than simply entertaining or informing, they help their audiences achieve specific outcomes—learning a skill, improving their health, growing their business, or transforming their mindset.

This focus on transformation justifies premium pricing for memberships and courses. Audiences are willing to pay significantly more for outcomes than for content. Creators who can demonstrate clear transformation for their community members build more sustainable and profitable businesses.

Case Studies: Creator Economy Success Stories

The best way to understand the creator economy is to examine the creators who have built remarkable businesses. These case studies illustrate different paths to success in the creator economy.

Case Study 1: MrBeast — The Content Empire

Jimmy Donaldson, known as MrBeast, has built the most successful creator business in history. What started as gaming commentary videos has evolved into a multi-platform empire generating over $100 million annually. MrBeast’s success comes from understanding that content is a product that must be optimized for engagement.

His business model spans multiple revenue streams: YouTube ad revenue from multiple channels, brand partnerships with major companies, MrBeast Burger (a virtual restaurant chain), Feastables (a chocolate bar brand), and various merchandise lines. He employs over 100 people and operates with the infrastructure of a traditional media company.

The key lesson from MrBeast is the power of reinvestment. He famously reinvests every dollar earned back into content production, creating a virtuous cycle where better content generates more revenue, which enables even better content. His approach treats creation as a capital-intensive business rather than a lifestyle pursuit.

Case Study 2: Emma Chamberlain — From Vlogger to Founder

Emma Chamberlain represents the evolution from creator to entrepreneur. Starting as a YouTube vlogger in 2017, she has built a business that extends far beyond content creation. Her coffee brand, Chamberlain Coffee, has become a significant business in its own right, available in major retailers and generating millions in revenue.

Chamberlain’s strategy demonstrates the power of authentic brand building. Her audience trusts her recommendations because she has maintained authenticity throughout her career. When she launched her coffee brand, it felt like a natural extension of her content rather than a cynical cash grab.

Her success shows that creators can build product businesses that rival traditional CPG companies when they leverage their audience relationships effectively. The direct connection to consumers that creators enjoy provides advantages that traditional brands struggle to replicate.

Case Study 3: Alex Cooper — Podcasting Powerhouse

Alex Cooper built Call Her Daddy into one of the most successful podcasts in the world, eventually signing a $60 million deal with Spotify. Her success demonstrates the power of niche content and community building. By creating content that resonated deeply with a specific audience segment, she built a loyal following that translated into massive commercial success.

Cooper’s evolution from a Barstool Sports podcast to a Spotify-exclusive show to her current Unwell Network demonstrates the maturation of the podcasting business. She has expanded from a single show to a network of podcasts, leveraging her expertise and audience to launch new creators.

Her case study illustrates how creators can build media companies around their personal brands, creating value that extends beyond their individual content. The Unwell Network represents a new model for creator-led media companies that could reshape the podcasting landscape.

Future Outlook: The Creator Economy Through 2030

Looking ahead, the creator economy is poised for continued growth and evolution. Several key developments will shape the industry through 2030.

Market Projections

Market research firms project the creator economy will reach $500-800 billion by the early 2030s, representing a 3-4x increase from current levels. This growth will be driven by continued platform innovation, the expansion of creator tools, and the increasing allocation of marketing budgets to creator partnerships.

Goldman Sachs Research suggests the creator economy could approach half a trillion dollars by 2027 alone, with the largest platforms capturing the majority of this value. The investment bank expects a “flight to quality” as creators prioritize platforms with stability, scale, and monetization potential, particularly as macroeconomic uncertainty impacts brand spending.

Technology Trends

AI will continue to transform the creator economy, with several developments on the horizon. Generative AI tools will become more sophisticated, enabling creators to produce higher-quality content with less effort. AI-powered analytics will provide deeper insights into audience behavior and content performance. Virtual and augmented reality will create new formats for creator content, potentially enabling entirely new categories of creator businesses.

The rise of AI-generated creators will accelerate, potentially creating competition for human creators while also opening new opportunities for creators who can effectively collaborate with AI tools. Regulatory frameworks will emerge to address disclosure requirements and ethical considerations around AI-generated content.

Industry Maturation

The creator economy will continue its evolution from a fragmented, experimental space to a mature industry with established best practices, professional standards, and institutional infrastructure. This maturation will bring both benefits and challenges—greater stability and professionalism, but also higher barriers to entry and more intense competition.

Creator education will become a significant industry segment, with courses, coaching, and certification programs helping aspiring creators develop the skills needed to succeed. Universities and business schools will increasingly offer programs focused on creator entrepreneurship, treating it as a legitimate career path rather than a novelty.

Global Expansion

While North America and Europe currently dominate the creator economy, the next decade will see significant growth in emerging markets. Mobile-first internet access, affordable smartphones, and localized platforms are enabling creators in Africa, Southeast Asia, and Latin America to build global audiences.

This global expansion will bring new voices, perspectives, and business models to the creator economy. It will also create opportunities for cross-cultural collaboration and the emergence of truly global creator brands that transcend national boundaries.

Key Takeaways for Creators and Brands

- The creator economy is a $250+ billion industry growing at 22.7% CAGR, projected to reach $500-800 billion by the early 2030s.

- AI is transforming creation—both as a tool for human creators and through the emergence of AI-generated influencers that are capturing significant brand budgets.

- Direct monetization is overtaking advertising—88% of community builders now monetize through memberships, and creators are building diversified income streams they control.

- Community-led business models are emerging—creators are building owned audiences outside social platforms, with 18,000+ active communities on platforms like Circle.

- Professionalization is the new norm—the era of the solo bedroom creator is giving way to professionalized operations with teams, infrastructure, and venture capital.

Sources and Citations

- Goldman Sachs Research — “The creator economy could approach half-a-trillion dollars by 2027” — https://www.goldmansachs.com/insights/articles/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027

- Coherent Market Insights — Global Creator Economy Market Report — https://www.coherentmarketinsights.com/industry-reports/global-creator-economy-market

- Circle — 2026 Community Trends Report — https://circle.so/2026-community-trends-report

- Forbes — “The Creator Economy In 2026: The Era Of Consolidation” — https://www.forbes.com/sites/jasondavis/2026/01/26/the-creator-economy-in-2026—the-era-of-consolidation

- Digiday — “Here’s what the creator economy is expected to look like in 2026” — https://digiday.com/marketing/in-graphic-detail-heres-what-the-creator-economy-is-expected-to-look-like-in-2026

- Stan Store — “8 Trends That Will Define the Creator Economy in 2026” — https://stan.store/blog/creator-economy-trends-2026

- Stan Store — “The State of the Creator Economy 2026” — https://stan.store/blog/state-of-the-creator-economy

- Linqia — 2026 State of Influencer Marketing Report — https://www.linqia.com/2026-state-of-influencer-marketing/

- Billion Dollar Boy — “The Real Impact of AI on the Creator Economy” — https://www.billiondollarboy.com/muse-report-ai-creator-economy/

- Playbella — “The Creator Economy in 2026: Trends, Opportunities, and the Rise of AI Influencers” — https://playbella.org/blog/creator-economy-2026-trends

- IAB — Creator Economy Advertising Spend Forecasts 2026

- Backlinko — Substack Statistics — https://backlinko.com/substack-users

Additional Insights: The Economics of Digital Creation

Beyond the headline statistics, understanding the economics of digital creation requires examining the micro-level dynamics that determine creator success. The creator economy operates on principles that differ significantly from traditional employment or even traditional media businesses.

The cost structure of creator businesses has evolved dramatically. In the early days of YouTube, creators needed little more than a webcam and an internet connection. Today, professional creators invest significantly in equipment, software, team members, and marketing. A mid-tier creator might spend $50,000-100,000 annually on production costs, while top creators operate with seven-figure budgets. This capital intensity creates barriers to entry but also opportunities for creators who can operate efficiently.

Revenue per follower varies enormously across creator tiers. Nano influencers (under 5,000 followers) might earn $100-500 per sponsored post. Micro influencers (5,000-100,000 followers) typically command $500-5,000 per post. Macro influencers (100,000-500,000 followers) can earn $5,000-25,000 per partnership. Mega influencers (500,000+ followers) often charge $25,000-100,000+ for major campaigns. However, these figures vary significantly by niche, engagement rate, and content format.

The most successful creators have moved beyond one-off sponsorships to long-term partnerships and equity arrangements. Rather than charging per post, they negotiate annual retainers, revenue shares, or equity stakes in brands they promote. This evolution reflects the maturation of the creator economy and the increasing value of authentic, ongoing relationships between creators and brands.

The Role of Platforms in Creator Success

Social platforms serve as the foundation of the creator economy, but their role is more complex than simple distribution. Each platform has developed distinct creator ecosystems with different monetization mechanisms, audience behaviors, and content norms.

YouTube remains the most creator-friendly platform in terms of direct monetization through its Partner Program. The platform shares 55% of ad revenue with creators, providing a predictable income stream based on viewership. YouTube Shorts has emerged as a significant revenue source, with the platform distributing $100 million to Shorts creators in its first year. The platform’s search functionality also provides long-tail discoverability that other platforms lack.

Instagram has shifted aggressively toward video with Reels, responding to competition from TikTok. The platform’s creator marketplace connects brands with creators for partnerships, while its shopping features enable direct product sales. However, Instagram’s algorithm changes have frustrated many creators who saw their reach decline as the platform prioritized Reels over static content.

TikTok’s Creator Fund and Creator Marketplace have established it as a viable income source for top creators, though many complain that the payouts are lower than other platforms relative to viewership. The platform’s algorithm remains its superpower—capable of making unknown creators viral overnight. However, regulatory uncertainty in the U.S. has created risk for creators who have built their businesses primarily on TikTok.

Twitch dominates live streaming, particularly for gaming creators. The platform’s subscription model, where viewers pay monthly to support creators, has proven highly effective. Top Twitch streamers earn millions annually through subscriptions, donations, and sponsorships. However, the platform’s recent controversies and policy changes have led some creators to explore alternatives like YouTube Live and Kick.

Niche Markets and Specialized Creator Economies

While the creator economy is often discussed as a monolith, it actually comprises numerous specialized sub-economies with distinct dynamics. Understanding these niches is essential for creators looking to establish themselves and for brands seeking partnerships.

The gaming creator economy is one of the largest and most mature segments. Gaming creators benefit from built-in monetization through platforms like Twitch and YouTube Gaming, as well as sponsorships from gaming hardware and software companies. Esports has created a professional pathway for top gaming creators, with tournament winnings and team salaries supplementing content income. The gaming audience is highly engaged and valuable to advertisers, making gaming creators some of the highest earners in the industry.

Finance and business creators have emerged as a high-value niche. Creators who explain investing, entrepreneurship, and personal finance attract audiences with disposable income and purchase intent. Brands in fintech, banking, and business software pay premium rates for partnerships with finance creators. The niche has also produced successful creator-led products, from investment courses to financial planning tools.

Health and wellness creators operate in a highly regulated but lucrative space. Fitness creators can monetize through workout programs, supplements, and apparel. Mental health creators have found audiences hungry for accessible guidance, though they must navigate ethical considerations around providing advice. The wellness niche has seen significant growth as consumers prioritize health post-pandemic.

Educational creators represent a growing segment as audiences turn to creators for learning. Language learning, skill development, and academic subjects have all found audiences on platforms like YouTube and TikTok. These creators often monetize through courses and memberships, leveraging their content as marketing for higher-ticket educational products.

The Impact of Economic Conditions on Creator Businesses

The creator economy does not exist in isolation from broader economic conditions. Macroeconomic factors significantly impact creator income, brand spending, and platform dynamics.

Economic downturns typically lead to reduced brand marketing budgets, which directly impacts creator sponsorship income. During the 2022-2023 tech downturn, many creators reported significant declines in brand partnership opportunities as companies cut marketing spend. However, economic uncertainty can also drive people to pursue creator careers as traditional employment becomes less secure.

Interest rate environments affect the creator economy through their impact on venture capital. Many creator economy startups rely on VC funding to offer competitive payouts and develop new features. When interest rates rise and VC funding becomes scarce, these platforms may reduce creator payouts or slow feature development. The 2022-2023 period saw several creator economy startups shut down or pivot due to funding challenges.

Consumer spending patterns also impact creator businesses. During economic downturns, consumers may cut discretionary spending on memberships, courses, and creator merchandise. However, the relatively low cost of creator subscriptions compared to traditional entertainment can make them resilient during downturns. Some creators report that their businesses actually grow during recessions as consumers seek affordable entertainment and education.

Regulatory Landscape and Legal Considerations

As the creator economy matures, it is attracting increased regulatory attention. Creators and platforms must navigate an evolving legal landscape that touches on advertising disclosure, intellectual property, labor classification, and content moderation.

Advertising disclosure requirements have become stricter in many jurisdictions. The FTC in the United States requires clear disclosure of sponsored content, and enforcement has increased. Creators who fail to properly disclose partnerships face fines and reputational damage. Similar regulations exist in the EU, UK, and other major markets. The rise of AI-generated content has added complexity, with regulators considering additional disclosure requirements for virtual influencers.

Intellectual property issues plague the creator economy. Music licensing remains a significant challenge, with creators frequently facing copyright claims or muted videos due to background music. The use of clips from movies, TV shows, and other creators’ content creates ongoing legal gray areas. Platforms have developed content ID systems to manage these issues, but creators often feel these systems are overly aggressive and lack due process.

Labor classification questions have emerged as creator businesses professionalize. When does a creator assistant become an employee rather than a contractor? How should creator income be taxed? These questions become more pressing as creator businesses grow and hire teams. Some jurisdictions are exploring whether creators should have employment protections or collective bargaining rights.

Content moderation policies impact creator businesses directly. Platform decisions about what content is allowed can make or break creator careers. Creators have complained about inconsistent enforcement, lack of transparency, and limited appeal options. As platforms face pressure from advertisers and regulators, content policies are likely to become stricter, potentially limiting the types of content that can be monetized.