The digital creator economy has evolved from a side hustle phenomenon into a quarter-trillion-dollar global industry that is fundamentally reshaping how content is produced, distributed, and monetized. With over 207 million content creators worldwide and U.S. advertising spend alone reaching $37 billion in 2025, this sector now represents one of the fastest-growing segments of the digital economy. What began as a playground for hobbyists has matured into a sophisticated ecosystem where creators build empires, platforms compete fiercely for talent, and brands redirect billions in marketing budgets toward influencer partnerships.

\n\n

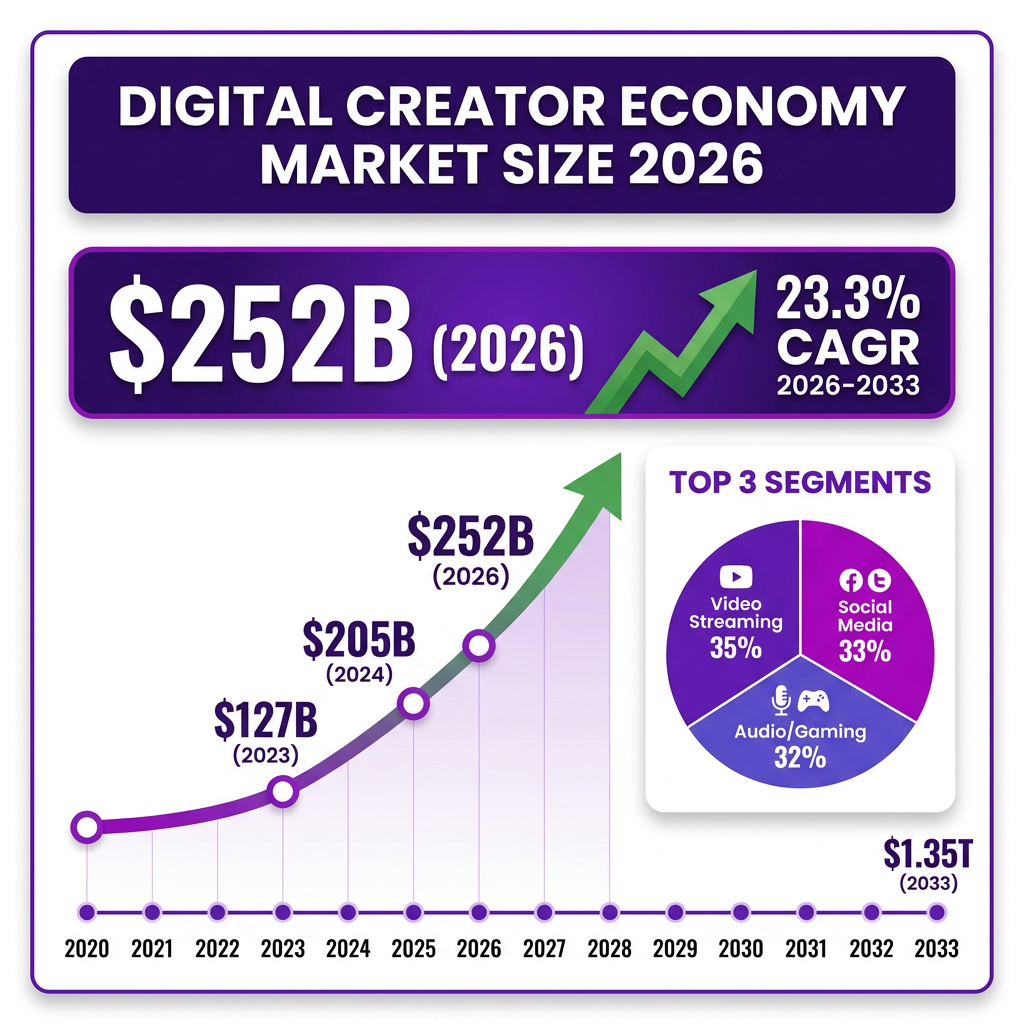

According to Grand View Research, the creator economy was valued at $205.25 billion in 2024 and is projected to reach an astounding $1.35 trillion by 2033, representing a compound annual growth rate (CAGR) of 23.3%. Research and Markets provides an even more aggressive near-term projection, estimating the market will grow from $255.66 billion in 2025 to $323.48 billion in 2026 at a CAGR of 26.5%. Goldman Sachs Research expects the creator economy to approach half a trillion dollars by 2027, with the 50 million global creators growing at a 10-20% compound annual growth rate during the next five years.

\n\n

This comprehensive analysis examines the digital creator economy’s current state, key statistics, emerging trends, major players, challenges, opportunities, and future outlook. Whether you’re a creator seeking to build a sustainable business, a brand looking to navigate influencer partnerships, or an investor evaluating opportunities in this rapidly evolving space, this report provides the data-driven insights you need to make informed decisions.

\n\n

\n\n

Market Overview: The $252 Billion Ecosystem

\n\n

The creator economy’s explosive growth trajectory reflects a fundamental shift in how audiences consume content and how value is created in the digital age. Traditional media gatekeepers have been replaced by algorithms and authentic connections, enabling anyone with a smartphone and compelling content to build a global audience. This democratization of media has created unprecedented opportunities while simultaneously introducing new challenges around monetization, sustainability, and mental health.

\n\n

North America currently dominates the global creator economy, capturing more than 37.4% of market share in 2024 according to Market.us data. The U.S. market alone was valued at $50.9 billion in 2024, with projections pointing to $297.3 billion by 2034 at a 19.3% CAGR. However, the Asia-Pacific region is emerging as the fastest-growing market, driven by massive user bases on platforms like TikTok, YouTube, and emerging local platforms that prioritize creator monetization.

\n\n

The market’s growth is fueled by several converging factors. First, the proliferation of high-speed internet and affordable smartphones has lowered barriers to entry, enabling creators from emerging markets to participate in the global economy. Second, platforms have invested heavily in creator monetization tools, recognizing that sustainable creator businesses drive platform engagement and advertising revenue. Third, brands have shifted marketing budgets away from traditional advertising toward creator partnerships, seeking authentic connections with increasingly ad-averse consumers.

\n\n

By platform type, video streaming dominates with the largest market share, driven by YouTube’s mature monetization ecosystem and the explosive growth of short-form video on TikTok and Instagram Reels. Social media platforms account for approximately 32.8% of the market, while audio platforms, gaming platforms, and content-sharing platforms make up the remainder. Each platform type has developed distinct monetization models, from YouTube’s ad revenue sharing to TikTok’s Creator Rewards Program to podcast advertising and Twitch subscriptions.

\n\n

The end-use segmentation reveals that individual content creators lead the market with 58.7% of revenue share, followed by businesses and brands leveraging creator tools for marketing, and media companies adapting to the new content landscape. This distribution highlights the economy’s foundation: millions of individual creators building businesses around their expertise, personality, and audience relationships.

\n\n

Looking at the historical trajectory, the creator economy has experienced remarkable acceleration. In 2023, the market was valued at approximately $127.65 billion according to Exploding Topics data. By 2024, this grew to $205.25 billion, representing a 60% year-over-year increase. The 2025 valuation of $252.33 billion shows continued momentum despite economic headwinds affecting other sectors. This resilience demonstrates the creator economy’s structural shift from experimental marketing channel to permanent industry fixture.

\n\n

Industry Verticals: The creator economy spans numerous verticals, each with distinct characteristics and monetization patterns. Gaming creators represent one of the largest segments, with esports and streaming driving significant revenue. Beauty and fashion creators have built massive businesses through brand partnerships and affiliate marketing. Finance and business creators command premium rates due to high-value audiences. Education and how-to content creators leverage expertise into course sales and consulting. Fitness and wellness creators combine content with digital products and coaching services. Each vertical presents unique opportunities and challenges for creators seeking to build sustainable businesses.

Platform Competition Dynamics: The battle for creator talent has intensified among major platforms. YouTube’s $100 billion payout since 2021 represents the largest creator investment of any platform. TikTok’s Creator Rewards Program represents a significant upgrade from the original Creator Fund, with payouts increasing by an average of 312%. Instagram has introduced multiple monetization features including subscriptions, badges, and bonuses. Twitter/X has launched creator ad revenue sharing. This competition benefits creators through improved monetization options, though it also creates complexity in managing multi-platform presence.

Economic Impact: The creator economy has created entirely new career paths and economic opportunities. An estimated 4.2 million jobs are supported by the creator economy globally, including direct creator employment, platform staff, agency personnel, and supporting service providers. The economic impact extends beyond direct revenue to include secondary effects in areas like photography equipment, editing software, co-working spaces, and professional services tailored to creators.

\n\n

Key Statistics and Data

\n\n

The creator economy’s scale becomes even more impressive when examining the granular data behind the headline figures. Understanding these statistics is crucial for creators, brands, and platforms seeking to navigate this rapidly evolving landscape.

\n\n

Creator Population: Globally, over 207 million individuals identify as content creators, with the United States accounting for a significant share: 162 million creators, of whom 45 million work professionally. Nearly half of all creators (46.7%) are engaged in full-time content creation, while the remainder balance creative work with other employment. The average creator takes approximately six and a half months to earn their first dollar, highlighting the challenge of building monetizable audiences.

\n\n

Market Valuations: Different research firms provide varying estimates based on methodology, but all point to explosive growth. Grand View Research projects $205.25 billion in 2024 growing to $1.35 trillion by 2033 at 23.3% CAGR. Research and Markets forecasts $255.66 billion in 2025 reaching $323.48 billion in 2026 at 26.5% CAGR. SNS Insider estimates $203.6 billion in 2024 expanding to $1.18 trillion by 2032 at 24.6% CAGR. Goldman Sachs estimates approximately $250 billion for 2024 approaching $480 billion by 2027. Exploding Topics tracks growth from $127.65 billion in 2023 to $528.39 billion by 2030 at 22.5% CAGR.

\n\n

Influencer Marketing Spend: The influencer marketing industry reached $32.55 billion in 2025 and is projected to hit $40.51 billion in 2026. YouTube alone has paid out over $100 billion to creators since 2021 through its Partner Program. Unilever announced it will invest 50% of its marketing spend on influencers, resulting in hiring 20 times more creators than today. This represents a fundamental shift in how major brands allocate marketing resources.

\n\n

Creator Income Distribution: The income distribution within the creator economy is highly skewed. Only 4% of creators earn over $100K annually, while the vast majority struggle to generate sustainable income. Among full-time creators earning at least $60,000 annually, those with 3+ revenue streams earn $75,000 more on average than single-source creators. Nearly half of U.S. creators earn between $10K and $100K annually, making this a viable middle-class career path for those who succeed. However, 85% of TikTok creators earn less than $1,000 monthly from the Creator Fund, highlighting the platform payout limitations.

\n\n

Platform Monetization: TikTok’s Creator Rewards Program pays roughly $0.40 to $1.00 per 1,000 qualified views on videos 60 seconds or longer, meaning a video with 1 million views could generate $400 to $1,000+ in direct payouts. The original Creator Fund paid only $0.02-$0.04 per 1,000 views. YouTube’s Partner Program typically generates higher RPMs (revenue per mille), with rates varying significantly by niche, audience geography, and content length. Premium niches like finance and technology can command RPMs of $10-20, while entertainment content typically earns $2-5.

\n\n

AI Adoption: 84% of creators already leverage AI-powered tools for content creation, editing, and optimization. This adoption separates high-performing creator programs from the rest, with AI-enabled creators producing content more efficiently and at higher quality. AI tools are used for scripting, thumbnail generation, video editing, captioning, and audience analytics.

\n\n

Engagement Benchmarks: Average engagement rates vary significantly by platform: 5-15% on Instagram and 8-20% on TikTok. Nano-creators (1K-10K followers) typically achieve higher engagement rates than macro-influencers, making them valuable for brands seeking authentic connections with niche audiences. Micro-creators (10K-100K followers) often provide the optimal balance of reach and engagement for brand partnerships.

\n\n

Content Format Performance: Video content dominates with 28.5% market share by content type, followed by written content, audio, gaming, music, and photography. Music content is projected to be the fastest-growing content type through the forecast period, driven by the expansion of audio platforms and the integration of music into short-form video content.

Platform User Statistics: YouTube boasts over 2.7 billion monthly active users globally, making it the largest video platform and a cornerstone of the creator economy. TikTok has surpassed 1.5 billion monthly active users, with the average user spending 95 minutes per day on the platform. Instagram maintains over 2 billion monthly active users, with Reels driving significant engagement growth. Twitch attracts 140 million monthly unique visitors, with 7.5 million active streamers. These massive user bases provide creators with unprecedented reach potential.

Content Production Volume: YouTube creators upload over 500 hours of video content every minute. TikTok sees over 1 billion video views per day. Podcast creators publish over 4 million episodes annually across all platforms. The sheer volume of content being produced highlights both the opportunity and the challenge of standing out in an increasingly crowded landscape.

Demographic Insights: Gen Z (ages 18-26) represents the largest cohort of content creators, with 48% of creators falling into this age group. Millennials (ages 27-42) comprise 35% of creators, while Gen X and Boomers make up the remaining 17%. This demographic distribution reflects both digital native status and career stage considerations—younger creators often have fewer financial obligations and more flexibility to pursue creative careers.

Geographic Distribution: While North America leads in creator economy revenue, Asia-Pacific is the fastest-growing region with a projected CAGR of 28.5% through 2030. Europe represents approximately 22% of global creator economy revenue, with significant variation between Western and Eastern European markets. Latin America and Africa are emerging markets with high growth potential as internet infrastructure improves and mobile payment systems mature.

Platform Revenue Models: YouTube’s Partner Program shares 55% of ad revenue with creators for standard videos and 45% for Shorts. Twitch subscriptions provide creators with 50% of subscription revenue. Patreon takes a 5-12% platform fee depending on the plan tier. OnlyFans retains 20% of creator earnings. Understanding these revenue splits is crucial for creators evaluating platform options.

\n\n

Major Trends Shaping the Creator Economy in 2026

\n\n

The creator economy is entering a new phase of maturity in 2026, characterized by consolidation, professionalization, and the integration of emerging technologies. Seven major trends are defining this evolution:

\n\n

1. AI-Powered Content Creation

\n\n

Artificial intelligence has become an indispensable tool for creators, with 84% adoption rates across the industry. AI is being used for processes rather than end-to-end content generation—helping with ideation, scripting, editing, thumbnail creation, and optimization. The key insight from 2026 is that successful creators use AI to enhance their workflow while maintaining human authenticity in the final output. Tools like ChatGPT, Claude, and specialized creator platforms have democratized access to capabilities that previously required expensive software or professional teams.

\n\n

The AI tools landscape for creators includes writing assistants for scripting and caption generation, image generators for thumbnails and visual content, video editing AI for automated cuts and enhancements, voice synthesis for narration and dubbing, and analytics AI for optimizing posting times and content strategy. The most successful creators have integrated these tools into streamlined workflows that multiply their output without sacrificing quality.

\n\n

2. Community-Led Growth Models

\n\n

As algorithmic reach becomes increasingly unpredictable, creators are prioritizing owned communities over platform-dependent audiences. Circle’s data shows that 44% of creator communities have between 1 and 100 members, indicating that much growth is happening at smaller, more intimate scales. These community-led business models and owned memberships are emerging as the most sustainable foundation for creator income. Platforms like Circle, Discord, and Mighty Networks enable creators to build direct relationships with their most engaged fans, reducing dependency on social media algorithms.

\n\n

The shift toward community-led growth reflects creators’ desire for stability in an unpredictable landscape. By building email lists, private communities, and direct fan relationships, creators can maintain communication channels regardless of algorithm changes or platform policies. This approach also enables higher-value monetization, as engaged community members are more likely to purchase premium products, courses, and membership subscriptions.

\n\n

3. Brand Partnerships as Primary Revenue

\n\n

Nearly 69% of creators rely on brand collaborations as their primary income source. However, the nature of these partnerships is evolving. Creator and influencer marketing now represent a permanent line item in global marketing plans, not an experimental channel. Brands are moving beyond one-off sponsored posts toward long-term ambassador relationships, co-created products, and equity partnerships. Steven Bartlett’s vision to build the “Disney of the Creator economy” includes seven-figure investments in creator brands like Maggie Sellers Reum’s Hot Smart Rich.

\n\n

The evolution of brand partnerships reflects maturation on both sides. Creators are becoming more sophisticated business operators, understanding their value and negotiating better terms. Brands are developing dedicated creator marketing teams, investing in long-term relationships, and measuring ROI more effectively. The most successful partnerships align creator authenticity with brand values, creating content that resonates with audiences while achieving marketing objectives.

\n\n

4. Multi-Revenue Stream Diversification

\n\n

Successful creators are diversifying across multiple revenue streams rather than relying on platform payouts alone. The data is clear: creators with 3+ revenue streams earn $75,000 more on average than single-source creators. Common revenue combinations include platform monetization (YouTube Partner Program, TikTok Creator Rewards), brand partnerships, affiliate marketing, merchandise sales, digital products (courses, templates), membership subscriptions, and live event appearances.

\n\n

This diversification strategy protects creators from platform policy changes, algorithm updates, and seasonal fluctuations in advertising spend. It also enables creators to serve different audience segments with appropriate offerings—free content for casual followers, premium content for superfans, and educational products for those seeking deeper expertise.

\n\n

5. TikTok SEO and Generative Engine Optimization

\n\n

Discovery is changing through chat-based tools and generative engine optimization (GEO)—the evolution of search engine optimization. TikTok has become a search engine for Gen Z, with creators optimizing content for discoverability within the platform. This shift requires brands to think beyond traditional channels, including community-driven sources such as Reddit and Wikipedia. Predictability is becoming the new consistency—creators who can reliably deliver content that performs are more valuable than those who simply post frequently.

\n\n

The rise of AI-powered search and chat interfaces is fundamentally changing content discovery. Instead of typing keywords into Google, users increasingly ask AI assistants for recommendations. This requires creators to optimize content for AI understanding—using clear titles, structured information, and comprehensive coverage of topics. Early adopters of GEO principles are capturing disproportionate attention in this emerging landscape.

\n\n

6. Creator Burnout and Mental Health

\n\n

According to a 2025 Creator Economy Report, 78% of creators report burnout impacting their motivation and mental and physical health. This has fueled demand for creator-specific support services, mental health resources, and more sustainable workflows. The always-on nature of content creation, algorithm anxiety, and income uncertainty create unique psychological pressures. Forward-thinking platforms and creator economy companies are addressing this through community support, educational resources, and tools that streamline workflows.

\n\n

The creator burnout crisis has sparked innovation in wellness tools and services specifically designed for content creators. Retreats like Joel Roache’s Creative Minds and Sarah Perl’s intimate NYC gatherings provide spaces for creators to connect, recharge, and share experiences. Platforms are implementing features that encourage healthy boundaries, such as scheduled posting, comment moderation tools, and analytics that focus on sustainable growth rather than vanity metrics.

\n\n

7. Platform Consolidation and Professionalization

\n\n

The creator economy is entering an era of consolidation. Independent creators, boutique managers, influencer agencies, and software vendors are coordinating more closely rather than operating in parallel. Management roles are evolving from deal facilitators to operating partners. The platforms best positioned to attract influential creators are those offering multiple forms of monetization, robust analytics, and creator support services.

\n\n

This consolidation trend extends to the creator tools market, where all-in-one platforms are replacing point solutions. Creators increasingly prefer integrated solutions that handle content scheduling, analytics, monetization, and community management in one place. This shift favors well-funded platforms that can invest in comprehensive feature sets and creator support.

\n\n

\n\n

Key Players and Competitive Landscape

\n\n

The creator economy ecosystem comprises multiple layers, each with dominant players competing for market share and creator loyalty.

\n\n

Content Platforms

\n\n

YouTube remains the gold standard for creator monetization, having paid out over $100 billion to creators since 2021. Its Partner Program offers the most mature monetization infrastructure, including ad revenue sharing, channel memberships, Super Chat, and merchandise shelves. YouTube’s long-form content model generates higher RPMs than short-form competitors, making it essential for creators seeking sustainable income. The platform’s recent focus on Shorts demonstrates its commitment to competing in the short-form video space while maintaining its long-form strengths.

\n\n

TikTok has revolutionized content discovery and creator careers through its algorithm-driven For You Page. The Creator Rewards Program, which replaced the original Creator Fund, now pays $0.40-$1.00 per 1,000 qualified views—a significant improvement that has increased creator earnings by an average of 312% compared to the original fund. TikTok Shop has added e-commerce monetization, enabling creators to earn commissions on product sales. The platform’s ability to catapult unknown creators to viral fame remains unmatched.

\n\n

Instagram continues to evolve its creator offerings, balancing photo, video, and short-form Reels content. While its monetization tools are less mature than YouTube’s, Instagram remains essential for brand partnerships and lifestyle content creators. The platform’s shopping features and subscription options provide growing monetization opportunities.

\n\n

Twitch dominates live streaming, particularly in gaming, with subscription revenue, bits (virtual goods), and ad sharing forming the core monetization model. The platform’s community features and real-time interaction create strong creator-fan relationships that translate to sustainable income.

\n\n

Patreon and Substack lead in direct fan support for creators seeking subscription-based income outside platform ecosystems. These platforms enable creators to build direct relationships with their most dedicated fans, generating predictable recurring revenue independent of algorithm changes.

\n\n

Creator Tools and Infrastructure

\n\n

CreatorIQ leads the enterprise creator marketing platform space, recently unveiling the industry’s first standardized benchmarking suite for creator performance. Their “Share Of” Metrics Suite and Industry Benchmarks Calculator give brands standardized tools to measure creator marketing ROI. The platform serves major brands and agencies managing large-scale creator programs.

\n\n

Stan Store and similar platforms enable creators to build monetizable storefronts directly linked to their social media profiles, selling digital products, courses, and services. These tools reduce friction between content consumption and commerce, enabling creators to capture value from their audience relationships.

\n\n

Canva, Adobe, and CapCut provide essential creation tools that have democratized professional-quality content production. AI-powered editing tools are increasingly integrated into these platforms, further lowering production barriers. CapCut’s integration with TikTok has made it particularly popular among short-form video creators.

\n\n

Linktree and Beacons dominate the link-in-bio space, providing creators with centralized hubs for directing audiences to various content, products, and social profiles. These tools have become essential infrastructure for multi-platform creators.

\n\n

Investor and Venture Capital Activity

\n\n

In 2025, over a dozen creator economy startups pulled in at least $50 million in new funding, with more than half of the roughly $2 billion in funding going to AI tools for content creation. Creator Ventures has emerged as a founder-first fund dedicated exclusively to the Creator Economy, providing not just capital but operational support, strategic guidance, and network access. Steven Bartlett and other high-profile creators are investing in creator-founded businesses, signaling the maturation of the ecosystem.

\n\n

The venture capital landscape for creator economy startups has evolved from generalist investors to specialized funds that understand the unique dynamics of creator businesses. These investors recognize that creator-founded companies often have built-in distribution advantages and authentic connections with target audiences that traditional startups lack.

\n\n

\n\n

Challenges and Pain Points

\n\n

Despite its impressive growth, the creator economy faces significant challenges that threaten the sustainability of creator careers and the health of the ecosystem.

\n\n

1. Extreme Income Inequality

\n\n

The most significant challenge is the highly skewed income distribution. While headlines celebrate creator millionaires, the reality is that only 4% of creators earn over $100K annually. The vast majority struggle to generate sustainable income, with many earning less than minimum wage when accounting for the hours invested. This inequality creates a winner-take-most dynamic that can discourage new entrants and lead to high burnout rates among mid-tier creators who see limited path to financial sustainability.

\n\n

The income inequality challenge is compounded by the visibility bias—successful creators are highly visible while struggling creators remain invisible, creating unrealistic expectations about earning potential. This dynamic attracts new creators who may invest significant time and resources before realizing the difficulty of building a sustainable career.

\n\n

2. Platform Dependency and Algorithm Volatility

\n\n

Creators remain vulnerable to platform decisions, algorithm changes, and policy shifts. A single algorithm update can decimate a creator’s reach and income overnight. This dependency creates anxiety and uncertainty, pushing creators toward diversifying across platforms while simultaneously fragmenting their audience and increasing workload. The recent TikTok ban discussions in the United States highlighted the existential risk platform dependency creates for creator businesses.

\n\n

Platform dependency extends beyond algorithms to include monetization policies, content moderation decisions, and competitive dynamics. Creators who build businesses entirely on a single platform face significant risk if that platform changes direction or loses market position.

\n\n

3. Creator Burnout and Mental Health Crisis

\n\n

With 78% of creators reporting burnout, mental health has become a critical issue. The pressure to constantly produce content, engage with audiences, and chase algorithmic favor creates unsustainable working conditions. Unlike traditional employment, there are no paid time off, no mental health days, and no separation between work and personal life. The isolation of solo creator work, combined with public scrutiny and performance pressure, contributes to anxiety, depression, and career abandonment.

\n\n

The mental health crisis is exacerbated by the public nature of creator work—negative comments, harassment, and constant evaluation by audiences create unique psychological stressors. Many creators report feeling unable to take breaks for fear of losing momentum or disappointing their audience.

\n\n

4. Measurement and Attribution Challenges

\n\n

Despite recent advances, measuring creator marketing ROI remains challenging. Brands struggle to attribute sales to specific creator campaigns, compare performance across creators, and justify budget allocation to skeptical stakeholders. While platforms like CreatorIQ have introduced standardized metrics, the industry still lacks universal measurement standards that would enable true performance comparison.

\n\n

5. Content Saturation and Discovery Challenges

With over 500 hours of video uploaded to YouTube every minute and millions of posts published daily across social platforms, content saturation has become a critical challenge. New creators face an uphill battle in gaining visibility, with algorithmic feeds favoring established accounts with proven engagement patterns. The cost of attention has increased dramatically—what garnered 100,000 views in 2020 might struggle to reach 10,000 today without paid promotion or existing audience leverage.

This saturation drives creators toward increasingly sensational content, controversial takes, and clickbait tactics to cut through the noise. The result is a race to the bottom that can compromise content quality and creator authenticity. Platforms are experimenting with new discovery mechanisms—including chronological feeds, topic-based recommendations, and friend-surfaced content—but the fundamental challenge of standing out in a saturated market remains.

Opportunities and Growth Strategies

\n\n

Despite these challenges, significant opportunities exist for creators, platforms, and brands willing to adapt to the evolving landscape.

\n\n

1. Niche Community Building

\n\n

The data shows that smaller, engaged communities often generate more sustainable income than large, passive audiences. Creators who focus on building deep relationships with niche audiences can command higher rates for brand partnerships, sell premium products and services, and create more predictable revenue streams. The shift from chasing virality to building community represents a maturation of creator business models.

\n\n

Niche creators often benefit from higher engagement rates, more loyal audiences, and less competition for brand partnerships. A creator with 10,000 highly engaged followers in a specific niche can often generate more revenue than a creator with 100,000 generalist followers.

\n\n

2. AI-Enhanced Workflows

\n\n

Creators who embrace AI tools for editing, scripting, thumbnail creation, and optimization can produce more content with less effort, improving their competitive position. The key is using AI to enhance rather than replace human creativity—maintaining authentic voice while increasing production efficiency.

\n\n

AI adoption creates a competitive moat for early adopters. As AI tools become more sophisticated, creators who master their use will produce higher-quality content more efficiently than those relying on traditional methods.

\n\n

3. Direct-to-Consumer Monetization

\n\n

Moving beyond platform-dependent income toward direct fan relationships through memberships, courses, digital products, and merchandise creates more sustainable businesses. Platforms like Circle, Patreon, and Stan Store enable creators to own their audience relationships and reduce platform dependency.

\n\n

Direct monetization also enables creators to capture more value from their audience relationships. While platforms take significant cuts of advertising revenue, direct sales and memberships allow creators to keep the majority of revenue generated.

\n\n

4. B2B Creator Opportunities

\n\n

While most attention focuses on consumer-facing creators, significant opportunities exist for B2B creators who develop expertise in specific industries. These creators can command premium rates for consulting, speaking, and educational content targeted at professional audiences. B2B creators often face less competition and can build more stable revenue streams through corporate partnerships, training programs, and industry-specific content.

\n\n

5. Educational Content and Course Creation

The online education market, projected to reach $350 billion by 2025, presents massive opportunities for creators with expertise to share. Unlike brand partnerships that provide one-time payments, courses and educational content generate recurring revenue and establish creators as authorities in their fields. The most successful creator-educators combine free content that demonstrates expertise with premium courses that provide structured learning paths.

Platforms like Teachable, Kajabi, and Thinkific have made course creation accessible to creators without technical expertise. The key to success is identifying specific transformation promises—what will students be able to do after completing the course that they couldn’t do before? Creators who can clearly articulate and deliver on transformation promises can command premium prices ($500-5,000+) for their educational products.

Case Studies and Success Stories

\n\n

Case Study 1: MrBeast – The Content Empire

\n\n

Jimmy Donaldson (MrBeast) has built one of the most successful creator businesses by reinvesting nearly all revenue into increasingly ambitious content. With over 300 million YouTube subscribers, MrBeast has diversified into Feastables (chocolate bars), MrBeast Burger (virtual restaurant chain), and various philanthropic initiatives. His success demonstrates the power of reinvesting creator earnings into building a diversified business empire rather than extracting personal income.

\n\n

MrBeast’s approach inverts traditional business logic—instead of maximizing profit, he maximizes content quality and audience growth, trusting that scale will eventually generate returns. This strategy has created a content moat that competitors struggle to replicate due to the capital requirements and operational complexity involved.

\n\n

Case Study 2: Pamela Reif – Fitness Empire

\n\n

German fitness creator Pamela Reif transformed her Instagram following into a multi-million dollar business through workout programs, an app, cookbook sales, and brand partnerships. Her success illustrates how creators can leverage audience trust to build product businesses that generate significantly more revenue than platform payouts alone.

\n\n

Reif’s strategy focused on providing consistent value through free workout content while building premium offerings for committed followers. Her diversified revenue streams—digital products, physical products, brand partnerships, and app subscriptions—create a resilient business model not dependent on any single platform.

\n\n

Case Study 3: Creator-Led Brand Partnerships

\n\n

Boksi’s user-generated content platform demonstrated that creator-generated content can outperform traditional studio content. In one case study, Boksi’s UGC generated 27% more sales than studio content with the same media budget. This data point validates the shift toward creator partnerships and demonstrates the ROI potential for brands willing to invest in authentic creator collaborations.

\n\n

The case study highlights a key insight: audiences increasingly trust authentic creator content over polished advertising. Brands that embrace this shift and partner effectively with creators can achieve superior marketing outcomes compared to traditional approaches.

\n\n

Future Outlook and Predictions

\n\n

The creator economy is projected to continue its explosive growth trajectory through 2030 and beyond. Goldman Sachs expects the market to approach half a trillion dollars by 2027, while Precedence Research projects the market reaching $2.08 trillion by 2035. Between 2025 and 2030, the market is projected to expand from $253.1 billion to $748.9 billion, representing a value increase of $495.8 billion.

\n\n

Several factors will drive this growth. First, the creator population will continue expanding, with Goldman Sachs projecting 50 million global creators growing at 10-20% CAGR. Second, brand investment in creator marketing will increase as measurement tools improve and ROI becomes more demonstrable. Third, emerging markets will contribute increasing shares of creator activity as internet penetration grows.

\n\n

The platforms best positioned for this future are those offering multiple monetization methods, robust creator support, and fair revenue sharing. We can expect continued consolidation as smaller platforms are acquired or fail, while major players invest heavily in creator retention.

\n\n

AI will play an increasingly central role, with generative AI tools becoming standard in creator workflows. However, the most successful creators will be those who use AI to enhance rather than replace human creativity, maintaining the authentic connections that drive audience loyalty.

\n\n

Regulatory attention will likely increase as the creator economy’s economic significance grows. Issues around labor classification, platform accountability, and consumer protection will require thoughtful policy approaches that balance innovation with creator welfare.

\n\n

By 2030, we can expect the creator economy to surpass $500 billion globally, potentially overtaking the traditional agency sector in value. The lines between creator, entrepreneur, and media company will continue blurring as successful creators build sophisticated businesses around their brands. The creator economy will no longer be a subset of digital marketing but a fundamental pillar of the global media and entertainment industry.

\n\n

Emerging Technologies: Several emerging technologies are poised to reshape the creator economy in coming years. Virtual and augmented reality will enable new forms of immersive content creation and fan interaction. Blockchain and NFTs offer potential new monetization models through digital ownership and creator coins, though adoption has been slower than initially predicted. Live commerce, already massive in Asian markets, is expanding globally and creating new revenue streams for creators. The integration of shopping directly into content platforms is blurring the lines between entertainment and commerce.

Regulatory Landscape: As the creator economy matures, regulatory attention is increasing. The European Union’s Digital Services Act and Digital Markets Act will impact platform operations and creator relationships. In the United States, discussions around labor classification could affect how creators are treated for tax and benefits purposes. Advertising disclosure requirements continue to evolve, with the FTC increasing enforcement of influencer marketing guidelines. Data privacy regulations like GDPR and CCPA affect how creators collect and use audience data. Staying compliant with this evolving regulatory landscape is becoming an essential skill for professional creators.

Global Expansion: While North America and Europe currently dominate creator economy revenue, significant growth is expected from emerging markets. India’s creator economy is projected to grow at 35% CAGR through 2030, driven by increasing internet penetration and mobile-first content consumption. Brazil, Indonesia, and Nigeria represent other high-growth markets. Localization and cultural adaptation will be key success factors for platforms and creators seeking to capture these opportunities.

Creator Economy Infrastructure Evolution

The infrastructure supporting the creator economy has matured significantly. Payment processors like Stripe and PayPal have streamlined how creators receive income from multiple sources. Tax and accounting services specifically designed for creators help navigate the complexities of multi-platform income, deductible expenses, and quarterly estimated taxes. Legal services tailored to creator needs address contract review, intellectual property protection, and business entity formation. This infrastructure maturation enables creators to operate as sophisticated businesses rather than gig workers.

Financial services for creators have also evolved. Creator-focused banks and financial management tools help with cash flow management, which can be irregular in the creator economy. Investment platforms designed for creators enable diversification of earnings into long-term wealth building. Insurance products tailored to creator businesses protect against liability, equipment loss, and income interruption. These financial tools are essential for creators seeking to build sustainable long-term careers.

The Rise of Creator Agencies and Management

As the creator economy has professionalized, a robust ecosystem of agencies and management companies has emerged. Traditional talent agencies like CAA and UTA have launched creator divisions, bringing established entertainment industry expertise to digital-native talent. Specialized creator agencies like Digital Brand Architects and VaynerTalent focus exclusively on digital creators, offering services tailored to platform-specific needs. Management companies provide strategic guidance, brand partnership negotiation, and business development support.

The decision of when to seek management depends on creator career stage. Emerging creators (10K-100K followers) typically benefit from self-management or shared management services that provide education and resources without high fees. Growing creators (100K-1M followers) often engage dedicated managers who can negotiate better brand deals and handle business operations. Established creators (1M+ followers) may employ full teams including managers, agents, lawyers, and financial advisors. The right management structure enables creators to focus on content while professionals handle business complexities.

Key Takeaways

\n\n

- The digital creator economy reached $252 billion in 2025 and is projected to grow to $1.35 trillion by 2033 at a 23.3% CAGR

- Over 207 million content creators worldwide, with 162 million in the United States alone

- Only 4% of creators earn over $100K annually, while those with 3+ revenue streams earn $75,000 more on average

- 84% of creators leverage AI-powered tools for content creation and optimization

- 78% of creators report burnout, highlighting the need for sustainable workflows and mental health support

- Brand partnerships represent the primary revenue source for 69% of creators

- The creator economy is projected to approach half a trillion dollars by 2027 and $2.08 trillion by 2035

\n\n

Sources and Citations

\n\n

- Grand View Research: Creator Economy Market Report 2024-2033

- Research and Markets: Creator Economy Global Market Report 2025

- Goldman Sachs Research: The Creator Economy: A New Frontier

- Exploding Topics: Creator Economy Statistics 2025

- Market.us: Creator Economy Market Size and Share Report

- SNS Insider: Creator Economy Market Analysis 2024-2032

- Circle: Community-Led Growth Report 2025

- CreatorIQ: Industry Benchmarks Calculator 2025