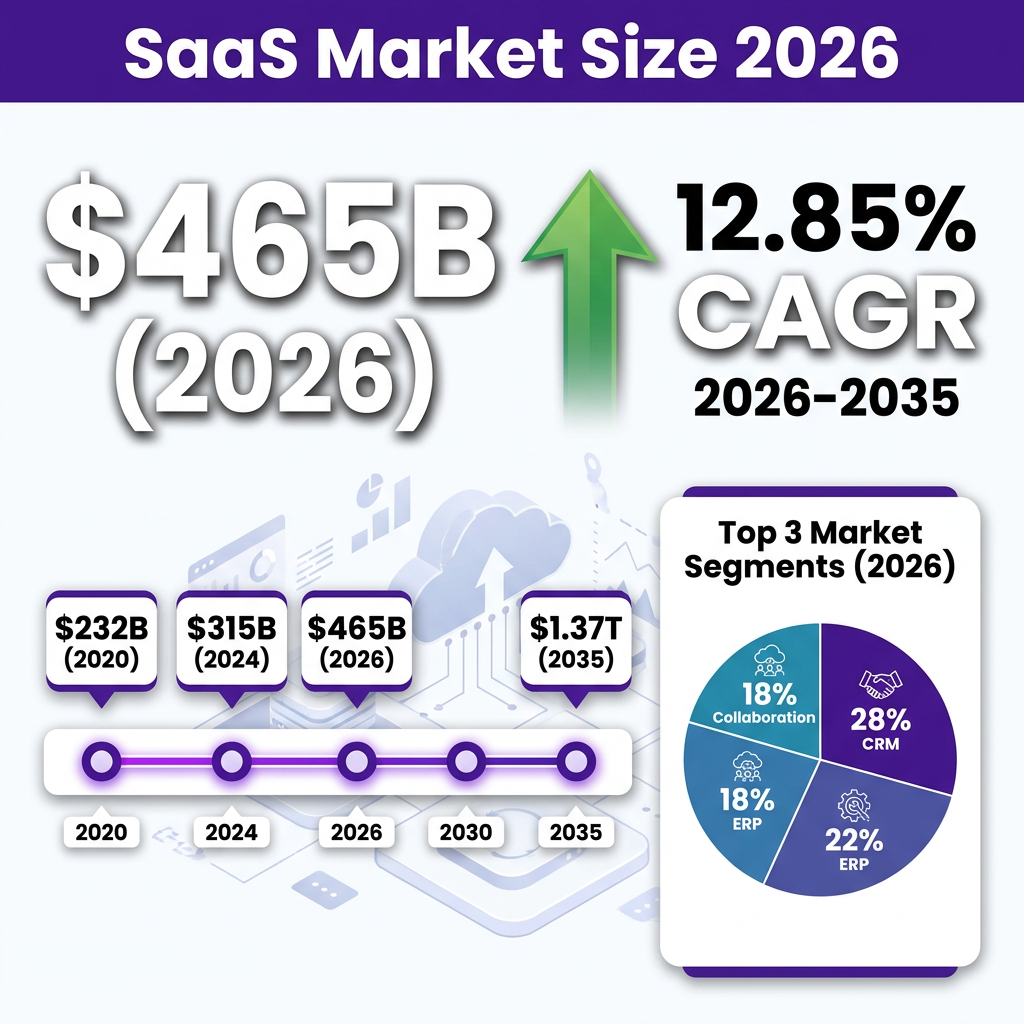

The global Software as a Service (SaaS) market has reached an unprecedented inflection point in 2026. With a market valuation of $465.03 billion and projections pointing toward $1.37 trillion by 2035, SaaS has evolved from a convenient alternative to on-premise software into the dominant model for enterprise and consumer applications alike. The industry is growing at a compound annual growth rate (CAGR) of 12.85%, a figure that reflects not just market expansion but a fundamental restructuring of how businesses consume technology worldwide.

From customer relationship management to human resources, from financial planning to project management, nearly every business function now has specialized SaaS solutions delivering capabilities that were once only available to the largest enterprises with massive IT budgets. Companies now use an average of 106 SaaS applications — down from a peak of 130 in 2022, but still representing a massive ecosystem of interconnected tools that power modern business operations.

Market Overview: The $465 Billion SaaS Ecosystem

The SaaS market in 2026 represents one of the most significant technology transformations in business history. What began as a niche delivery model for simple applications has matured into a comprehensive ecosystem serving every industry vertical and business function imaginable. Understanding the current state of this market requires examining its size, growth trajectory, and the fundamental shifts driving its expansion.

The global SaaS market size was valued at approximately $315.68 billion in 2025 and has grown to $465.03 billion in 2026. This represents a year-over-year growth rate that outpaces most traditional technology sectors, driven by continued digital transformation initiatives, the rise of remote work, and the increasing sophistication of cloud-based solutions. Multiple market research firms project slightly different figures, with estimates ranging from $375 billion to $492 billion for 2026, reflecting the dynamic nature of this rapidly evolving market.

The B2B SaaS segment specifically shows even more aggressive growth patterns. According to Mordor Intelligence, the B2B SaaS market was valued at $390 billion in 2025 and is estimated to grow to $492.34 billion in 2026, reaching an astounding $1.58 trillion by 2031 at a CAGR of 26.24%. This accelerated growth in the B2B segment reflects the increasing enterprise adoption of cloud-native solutions and the ongoing shift away from traditional on-premise software deployments.

Looking at the broader forecast, Grand View Research projects the SaaS market will reach $819.23 billion by 2030, growing at a CAGR of 12.0% from 2025 to 2030. Fortune Business Insights offers an even more optimistic projection, estimating the market will grow from $375.57 billion in 2026 to $1.48 trillion by 2034, exhibiting a CAGR of 18.7%. These varying projections all point to the same conclusion: the SaaS market is in a sustained period of explosive growth that will continue for at least the next decade.

The geographic distribution of SaaS adoption reveals interesting patterns. North America continues to dominate the market, accounting for approximately 56.9% of global SaaS revenue. However, the Asia Pacific region represents the fastest-growing market, expected to grow at around 20% CAGR, with revenue likely reaching $176.2 billion by 2030. This regional shift reflects the digital transformation initiatives underway in emerging economies and the increasing technology adoption rates in countries like India, China, and Southeast Asian nations.

Europe maintains a strong position as the second-largest SaaS market, driven by stringent data protection regulations that have actually accelerated cloud adoption as companies seek compliant, managed solutions. The Middle East and Africa, while starting from a smaller base, show promising growth trajectories as infrastructure investments and digital initiatives take hold across the region.

Key Statistics and Data: 30+ Metrics Defining the Industry

The SaaS industry generates an enormous amount of data, and understanding the key statistics helps paint a comprehensive picture of where the market stands and where it is headed. Here are the most critical metrics that define the SaaS landscape in 2026:

Market Size and Growth: The global SaaS market reached $465.03 billion in 2026, up from $408.21 billion in 2025. The B2B SaaS segment alone accounts for $492.34 billion. The industry is projected to reach $1.37 trillion by 2035 at a 12.85% CAGR. Alternative projections suggest the market could reach $1.48 trillion by 2034 at an 18.7% CAGR, or $819 billion by 2030 at a 12.0% CAGR.

Company Ecosystem: There are over 33,200 SaaS companies globally as of 2026, representing a 32% increase from 2021 when there were 25,000 companies. This growth in the number of providers reflects both market opportunity and the relatively low barriers to entry for SaaS businesses compared to traditional software companies.

Enterprise Adoption: Companies now use an average of 106 SaaS applications, down 18% from the 2022 peak of 130 applications. This consolidation reflects a maturation of the market as organizations rationalize their software portfolios and eliminate redundant tools. However, over 50% of SaaS software used in companies is not managed by the IT team, creating significant governance and security challenges.

Application Usage by Company Size: The number of SaaS applications varies significantly by organization size. Small companies (1-50 employees) use an average of 25-40 applications. Mid-size companies (51-200 employees) use 50-80 applications. Large enterprises (201-500 employees) use 80-120 applications. Major enterprises (500+ employees) often use 150+ applications, with some Fortune 500 companies managing portfolios of 300+ SaaS tools.

Financial Benchmarks: The median annual revenue growth for SaaS companies stands at 26%, down from 47% in 2024, reflecting market maturation and increased competition. Median blended CAC payback for $5M-$25M ARR SaaS is 18 months, flat versus Q3 2025 but up from 15 months in 2023. The median SaaS valuation multiple dropped from 7x ARR at the start of 2025 to 3.8x by March 2026, indicating a return to more rational valuations after the exuberance of previous years.

Key Performance Metrics: A healthy LTV:CAC ratio ranges from 3:1 to 5:1, with top companies exceeding 4:1. B2B SaaS companies show a median CAC payback of 8.6 months with LTV:CAC of 3.8x. Top-quartile-valued companies achieve Net Revenue Retention (NRR) rates of 113%, meaning they grow 13% without adding any new business. The Rule of 40 — ARR growth rate plus profit margin — remains a key benchmark, with successful companies exceeding 40% combined.

AI and Automation Impact: AI adoption in enterprises has jumped over 280% according to a Salesforce CIO survey. AI-native SaaS raises at 40% higher valuations than traditional SaaS. Some AI-native software companies reach approximately $3M in annual recurring revenue within their first year and scale to roughly $100M by year four, far outpacing traditional SaaS growth timelines. A subset of high-performing AI-native companies achieves approximately $40M in ARR within the first year and exceeds $120M by the second year.

Vertical SaaS Growth: The vertical SaaS market is projected at $157.4 billion by 2025, with a 23.9% CAGR — roughly double the pace of many horizontal segments. Vertical AI SaaS companies for healthcare, legal, and financial services raised the largest early-stage rounds, with median Series A sizes of $22 million versus $15 million for traditional SaaS.

Security and Compliance: Nearly one in four organizations experienced a SaaS or cloud-related breach in the past year. 99% of organizations encountered at least one SaaS or AI-driven security incident in 2025. 82% of executives report significant increases in cloud, SaaS, and Gen AI costs. Only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically.

Regional Distribution: North America accounts for 56.9% of global SaaS revenue. Asia Pacific is the fastest-growing region at approximately 20% CAGR. Europe maintains strong adoption driven by GDPR compliance requirements. Latin America and Middle East/Africa show emerging growth as digital infrastructure expands.

Deployment Models: Public cloud dominates with approximately 65% market share. Private cloud accounts for 25% of deployments, favored by regulated industries. Hybrid cloud represents 20.9% of the market and is forecasted to increase at a 20.1% CAGR, reaching $176.6 billion by 2030.

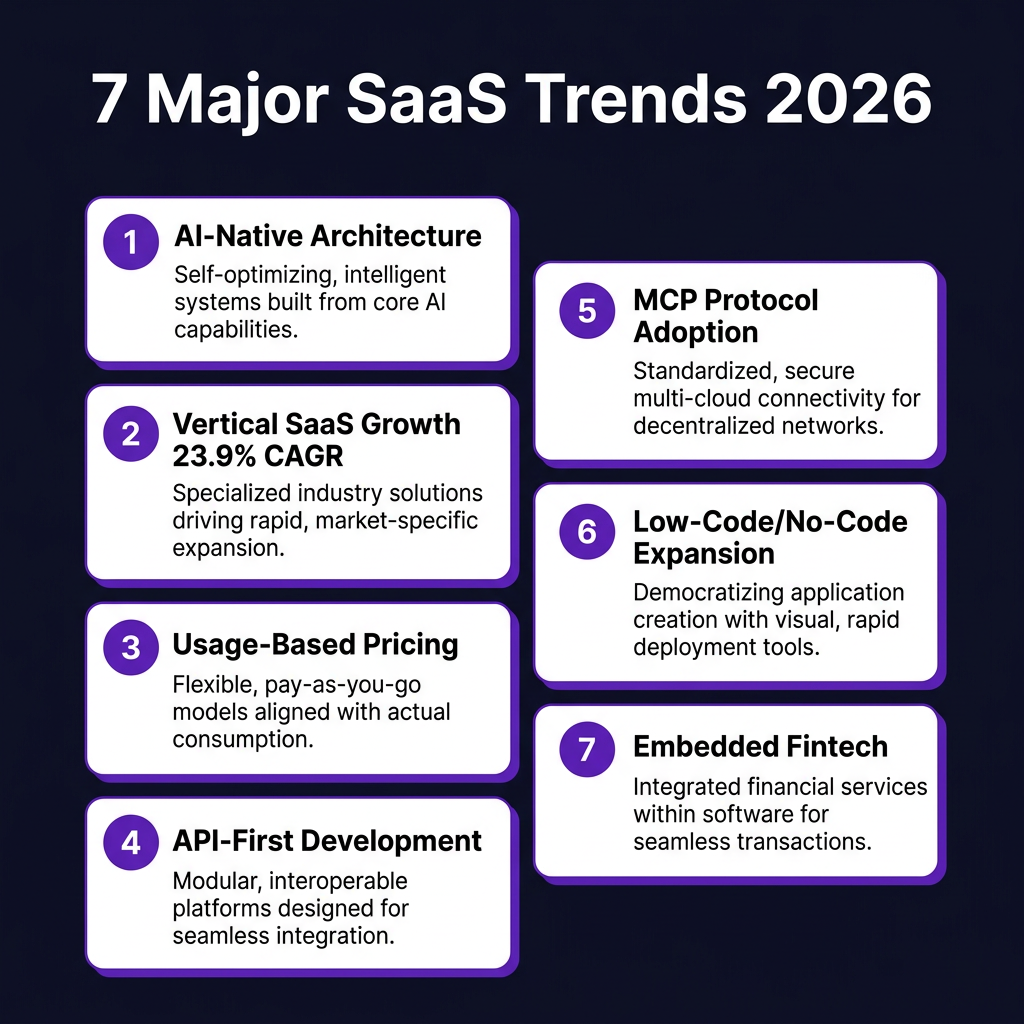

Major Trends Shaping SaaS in 2026

The SaaS industry is experiencing a paradigm shift in 2026, driven by technological advances, changing customer expectations, and market maturation. Here are the seven most significant trends reshaping the industry:

1. AI-Native Architecture Becomes the Default

In 2026, the conversation has shifted from “SaaS with AI features” to “AI-native SaaS.” Rather than bolting AI capabilities onto existing products, leading companies are architecting their platforms with AI at the core. This represents a fundamental change in how software is designed, built, and delivered.

AI-native SaaS products embed machine learning and generative AI capabilities throughout the user experience, not just as add-on features. These systems can autonomously process information, predict outcomes, and choreograph complex workflows. The impact on business metrics is substantial — AI-native SaaS companies raise at 40% higher valuations than traditional SaaS, and their growth trajectories significantly outpace conventional software companies.

Salesforce’s CIO survey reveals that AI adoption in enterprises has jumped over 280%, with “agentic” AI (multi-agent systems that act, not just chat) called out as a core 2026 priority. AI is no longer a feature; it sits at the core of product design, onboarding, and daily workflows. By the end of 2026, a majority of successful SaaS launches will advertise “MCP-native” (Model Context Protocol) as a core product capability, similar to how REST APIs became standard in the 2010s.

2. Vertical SaaS Surges at Double the Speed

While horizontal SaaS platforms continue to grow, vertical SaaS — software built for specific industries — is surging at a blistering CAGR of 23.9%, reaching a market size of $157.4 billion. This growth rate is roughly double that of many horizontal segments, reflecting the advantages of deep industry specialization.

Vertical SaaS delivers software built for one industry’s workflows, data, and compliance needs. Instead of trying to serve everyone, niche-focused SaaS businesses are winning by solving highly specific operational problems for targeted industries. This shift is creating a new era of AI-native Vertical SaaS platforms that are smarter, more scalable, and far more defensible than traditional SaaS models.

Success stories abound: Veeva Systems dominates life sciences, Procore Technologies leads construction management, and Toast has captured significant market share in restaurant technology. Vertical AI SaaS companies for healthcare, legal, and financial services have raised the largest early-stage rounds, with median Series A sizes of $22 million versus $15 million for traditional horizontal SaaS.

3. Usage-Based Pricing Goes Mainstream

The traditional per-seat subscription model is giving way to more flexible, consumption-based pricing. Usage-based pricing aligns vendor success with customer success — customers pay for what they use, and vendors benefit when their customers grow. This model is particularly well-suited to infrastructure services, API-based products, and AI-powered tools where value correlates directly with consumption.

Perhaps the most transformative trend is outcome-based pricing, where vendors share risk and reward with customers based on measurable business outcomes. This approach requires sophisticated tracking and attribution capabilities but creates powerful alignment between vendor and customer interests. Companies like Snowflake, Twilio, and AWS have pioneered this approach, and it is increasingly being adopted across the industry.

However, usage-based pricing brings challenges. 78% of IT leaders report unexpected costs from usage-based or AI-driven pricing models. Cost volatility has replaced predictable growth as a defining challenge, requiring new approaches to budgeting, forecasting, and financial operations (FinOps).

4. API-First and MCP-Native Development

API-first development has become standard practice, but 2026 marks the emergence of MCP (Model Context Protocol) as the next evolution in software interoperability. SaaS vendors are increasingly shipping MCP endpoints out of the box, enabling AI agents to interact with their platforms programmatically.

This shift enables a marketplace of MCP adapters and “AI-ready” SaaS integrations. Rather than building custom integrations for every use case, platforms can expose their capabilities through standardized protocols that AI systems can discover and use autonomously. This represents a fundamental change in how software systems interact, moving from human-directed integrations to AI-mediated orchestration.

The implications extend beyond technical architecture. API-first and MCP-native products can be integrated into complex workflows more easily, reducing friction for enterprise adoption and enabling new categories of automation and orchestration tools.

5. Low-Code and No-Code Democratization

The low-code and no-code movement continues to accelerate, enabling business users to build applications and automate workflows without traditional programming skills. This democratization of software development is expanding the addressable market for SaaS tools and changing the relationship between IT and business units.

Modern SaaS platforms increasingly include workflow builders, form creators, and automation tools that let non-technical users customize their experience. This reduces the burden on development teams while increasing user satisfaction and platform stickiness. The trend is particularly pronounced in CRM, project management, and business process automation categories.

However, this democratization brings governance challenges. As business users create their own applications and integrations, organizations struggle to maintain visibility, security, and compliance across their expanding SaaS portfolios.

6. Embedded Fintech Integration

SaaS companies are increasingly embedding financial services directly into their platforms. From payment processing to lending to insurance, fintech capabilities are becoming standard features of business software. This trend creates new revenue streams for SaaS vendors while simplifying financial operations for their customers.

The merchant of record model — where SaaS platforms handle payments, tax compliance, and regulatory requirements on behalf of their customers — is gaining traction, particularly among platforms serving SMBs and international markets. Companies like Stripe, Paddle, and Fungies.io enable this embedded fintech approach, allowing SaaS vendors to offer comprehensive solutions without building financial infrastructure from scratch.

7. Micro-SaaS and Workflow Automation

The rise of micro-SaaS — small, focused tools that solve specific problems — continues alongside the consolidation of larger platforms. These lightweight applications often integrate with major platforms to fill gaps in functionality or address niche use cases that larger vendors ignore.

Workflow automation tools like Zapier, Make, and n8n have created ecosystems where micro-SaaS products can thrive by connecting disparate systems. This trend enables a new generation of indie developers and small teams to build sustainable businesses serving specific customer needs without requiring massive capital investment.

Key Players and Competitive Landscape

The SaaS competitive landscape in 2026 is characterized by established giants defending their positions, fast-growing challengers disrupting categories, and a long tail of specialized providers serving niche markets. Understanding the key players helps illuminate where the industry is heading and where opportunities exist for new entrants.

The SaaS Giants

Salesforce remains the dominant force in CRM, generating $41.5 billion in FY2026 revenue and holding 20.7% of the global CRM market according to IDC. The company earned $21.6 billion in CRM revenue alone — more than Microsoft, Oracle, Adobe, and SAP combined. Salesforce has successfully transitioned from a single-product company to a comprehensive platform spanning sales, service, marketing, commerce, and analytics.

Microsoft continues to leverage its enterprise relationships and Office 365 dominance to push Azure and Dynamics 365. The company’s AI integration through Copilot represents one of the most comprehensive enterprise AI strategies, embedding generative AI capabilities across the entire Microsoft ecosystem.

Adobe has successfully transitioned from perpetual licenses to a subscription model, with Creative Cloud and Experience Cloud driving consistent recurring revenue. The company’s AI initiatives, including Firefly for generative AI, position it well for the next phase of creative software evolution.

Oracle and SAP continue to serve enterprise customers with comprehensive ERP and database solutions, though both face pressure from cloud-native competitors. Their strategies increasingly focus on hybrid cloud deployments and industry-specific solutions.

ServiceNow has established itself as the platform of choice for enterprise workflow automation, expanding from IT service management into HR, customer service, and custom application development. The company’s platform strategy creates significant switching costs and expansion opportunities.

Fast-Growing Challengers

Workday continues to gain share in HR and financial management, particularly among large enterprises seeking cloud-native alternatives to legacy systems. The company’s focus on AI and machine learning differentiates its offerings in a crowded market.

Zoom has evolved from a video conferencing tool to a comprehensive communications platform, though it faces increasing competition from Microsoft Teams and Google Meet. The company’s challenge is expanding beyond its pandemic-driven growth into sustainable, diversified revenue.

Slack (now part of Salesforce) and Teams battle for workplace messaging dominance, with the winner increasingly becoming the platform for app integration and workflow automation. This category illustrates how SaaS markets tend toward winner-take-most dynamics.

Datadog, Snowflake, and Cloudflare represent the new generation of infrastructure SaaS companies, providing essential services for modern application development and operations. These companies benefit from the continued migration of workloads to cloud environments.

Vertical SaaS Leaders

Veeva Systems dominates life sciences with specialized CRM and data management solutions. The company’s deep industry expertise creates formidable competitive moats.

Procore Technologies leads construction management software, providing project management, quality control, and financial tools specifically designed for the construction industry.

Toast has captured significant market share in restaurant technology, offering point-of-sale, payroll, and marketing tools tailored to the food service industry.

Shopify powers e-commerce for millions of merchants, expanding from a simple store builder to a comprehensive commerce platform including payments, shipping, and capital services.

Emerging Categories

The AI infrastructure layer is creating new categories of SaaS companies. OpenAI, Anthropic, and Cohere provide foundation models that power thousands of AI-native applications. Infrastructure providers like LangChain, Pinecone, and Weaviate enable developers to build AI-powered features into their products.

Security and compliance SaaS continues to grow as organizations face increasing regulatory requirements and cyber threats. Companies like SentinelOne, CrowdStrike, and Cloudflare provide essential security infrastructure for modern enterprises.

Challenges and Pain Points

Despite the impressive growth and opportunity in the SaaS market, significant challenges confront both vendors and customers. Understanding these pain points is essential for navigating the industry successfully.

1. SaaS Sprawl and Shadow IT

The average company uses 106 SaaS applications, but over 50% of this software is not managed by the IT team. This “shadow IT” creates significant governance, security, and compliance risks. Organizations struggle to maintain visibility into what software is being used, who has access to it, and what data is being shared.

The proliferation of AI tools has exacerbated this problem. In 2026, the biggest threat is not malware — it is employees integrating AI tools that have not been vetted by security teams. 99% of organizations encountered at least one SaaS or AI-driven security incident in 2025, highlighting the scale of the challenge.

2. Security and Compliance Complexity

Nearly one in four organizations experienced a SaaS or cloud-related breach in the past year. The shared responsibility model of cloud security creates confusion about who is responsible for what, leading to gaps in protection. According to IBM’s Cost of a Data Breach Report, approximately 82% of data breach incidents now involve data stored in the cloud.

Compliance requirements continue to multiply. GDPR in Europe, CCPA in California, and emerging AI regulations create a complex landscape that SaaS vendors must navigate. For customers, ensuring that all their SaaS providers meet compliance requirements is a significant operational burden.

3. Cost Management and Predictability

82% of executives report significant increases in cloud, SaaS, and Gen AI costs. The shift to usage-based pricing, while beneficial in many ways, has introduced cost volatility that makes budgeting difficult. 78% of IT leaders report unexpected costs from usage-based or AI-driven pricing models.

Only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically. Most teams are narrowly operational rather than strategic, lacking the expertise to optimize spending across their SaaS portfolios. This cost management challenge is particularly acute for mid-size companies that lack the resources of large enterprises but face similar complexity.

4. Integration and Data Silos

Despite the promise of connected ecosystems, data silos remain a significant problem. Each SaaS application collects and stores data in its own format, making comprehensive analysis difficult. Integration platforms help, but they add cost and complexity and often require technical expertise to configure properly.

The rise of AI has made this problem more acute. AI systems need access to comprehensive, clean data to deliver value, but data scattered across dozens of SaaS applications is difficult to consolidate and prepare. Organizations are increasingly recognizing that their data architecture is as important as their application architecture.

5. Customer Acquisition and Retention

The SaaS market is increasingly saturated, making customer acquisition more expensive and difficult. Median blended CAC payback has increased to 18 months, up from 15 months in 2023. The median SaaS valuation multiple has dropped from 7x ARR to 3.8x, reflecting investor concern about growth sustainability.

Retention has become the primary growth driver. Top-quartile companies achieve NRR rates of 113%, while bottom-quartile peers only reach 98%. In a mature market, the ability to expand existing customer relationships matters more than new customer acquisition. This shift requires different skills, metrics, and organizational focus than the growth-at-all-costs approach of previous years.

Opportunities and Growth Strategies

Despite the challenges, significant opportunities exist for SaaS companies that can navigate the evolving landscape effectively. Here are the key strategies driving growth in 2026:

1. AI-Native Product Development

AI-native SaaS companies are achieving growth rates and valuations that far exceed traditional SaaS. The key is not adding AI features but architecting products with AI at the core. This approach enables capabilities that were previously impossible and creates significant competitive differentiation.

Successful AI-native companies focus on specific use cases where AI can deliver clear, measurable value. They invest heavily in data infrastructure, model training, and user experience design to ensure their AI capabilities are reliable, trustworthy, and easy to use. The companies that master AI integration will define the next generation of SaaS leaders.

2. Vertical Market Expansion

Vertical SaaS continues to grow at roughly double the rate of horizontal SaaS. The strategy of focusing on a specific industry enables deeper functionality, stronger customer relationships, and higher switching costs. Vertical AI SaaS is particularly attractive, combining the growth dynamics of vertical software with the valuation premiums of AI-native companies.

Opportunities exist in virtually every industry. Healthcare, legal services, construction, agriculture, and professional services all have room for specialized SaaS solutions. The key is deep industry expertise combined with modern technology architecture.

3. Platform and Ecosystem Strategies

Successful SaaS companies are increasingly building platforms that enable third-party developers and integrators. This ecosystem approach extends the value of the core product while creating network effects that strengthen competitive position.

The MCP (Model Context Protocol) standard is enabling a new wave of AI-ready integrations. SaaS vendors that adopt these standards early can position themselves as essential infrastructure for the AI-powered enterprise. Platform strategies require significant investment in developer experience, documentation, and support, but the returns in terms of ecosystem lock-in can be substantial.

4. International Expansion

The Asia Pacific region is growing at approximately 20% CAGR, significantly faster than North America and Europe. SaaS companies that can navigate the complexity of international expansion — including localization, compliance, and go-to-market strategies — can access substantial growth opportunities.

International expansion requires more than translation. Successful global SaaS companies adapt their products, pricing, and marketing to local market conditions. They invest in local teams and partnerships to build trust and navigate regulatory requirements. The companies that master international growth will capture disproportionate value in the coming decade.

Case Studies and Success Stories

Real-world examples illustrate the strategies and outcomes that define success in the SaaS market. Here are three case studies from 2026:

Case Study 1: TripleDart and Signeasy — AI-Powered SEO Growth

Signeasy, an e-signature SaaS platform, partnered with TripleDart to improve their organic visibility for LLM-related searches. The results were impressive: Signeasy achieved 800 monthly sessions with 60-68% consistent month-over-month growth in LLM visibility.

The strategy focused on creating comprehensive, authoritative content around e-signature use cases, compliance requirements, and integration patterns. By positioning Signeasy as the definitive resource for electronic signature information, the company captured significant organic traffic and established thought leadership in their category.

Key Takeaway: Content marketing remains a powerful growth lever for SaaS companies, particularly when focused on high-intent keywords and comprehensive resource creation. The rise of AI search makes authoritative, well-structured content even more valuable.

Case Study 2: SentinelOne — Enterprise Cybersecurity Scale

SentinelOne, one of the largest cybersecurity platforms, partnered with TripleDart to drive organic growth. The results: a 250% increase in organic traffic through strategic SEO and content initiatives.

The approach combined technical SEO optimization with comprehensive threat research and educational content. By publishing detailed analysis of emerging threats, security best practices, and product capabilities, SentinelOne positioned itself as a thought leader while capturing high-intent search traffic.

Key Takeaway: Technical products benefit from educational content that addresses customer pain points and demonstrates expertise. SEO success requires both technical optimization and substantive, authoritative content.

Case Study 3: EmailOctopus — Conversion Rate Optimization

EmailOctopus, an email marketing platform, worked with TripleDart to improve their conversion funnel. The results: 40% improvement in purchases and 15% increase in signups through targeted optimization efforts.

The strategy involved analyzing the entire customer journey from first touch to purchase, identifying friction points, and implementing targeted improvements. By focusing on the metrics that matter — purchases and signups rather than vanity metrics — EmailOctopus achieved meaningful business results.

Key Takeaway: Growth requires focusing on business outcomes rather than vanity metrics. Understanding and optimizing the full customer journey delivers better results than isolated tactical improvements.

Future Outlook and Predictions: 2026-2030

The SaaS market will undergo significant transformation in the coming years. Here are the key predictions for 2026-2030:

Market Growth Projections

The global SaaS market is projected to reach $819 billion by 2030 at a 12.0% CAGR according to Grand View Research. More aggressive projections suggest the market could reach $1.48 trillion by 2034 at an 18.7% CAGR. The B2B SaaS segment shows particularly strong growth, with projections of $1.58 trillion by 2031 at a 26.24% CAGR.

These projections reflect continued digital transformation, the shift to remote and hybrid work, and the increasing sophistication of cloud-based solutions. Even conservative estimates suggest the market will nearly double by 2030, creating substantial opportunities for both established players and new entrants.

AI Integration Accelerates

By 2030, AI will be embedded in virtually every SaaS application. The distinction between “AI-powered” and traditional software will become meaningless as AI capabilities become table stakes. Agentic AI — systems that can take autonomous actions rather than just providing recommendations — will become standard in enterprise software.

The MCP (Model Context Protocol) will emerge as a standard for AI-to-software integration, enabling seamless interoperability between AI agents and SaaS platforms. Companies that fail to adopt AI-native architectures will face increasing competitive pressure as AI-enabled competitors deliver superior user experiences and outcomes.

Vertical SaaS Dominates New Entrants

Horizontal SaaS markets are increasingly saturated, making it difficult for new entrants to compete with established players. The most successful new SaaS companies will focus on specific verticals, bringing deep industry expertise and tailored solutions to underserved markets.

Vertical AI SaaS will be particularly attractive to investors, combining the growth dynamics of vertical software with the valuation premiums of AI-native companies. Industries like healthcare, legal services, construction, and agriculture will see significant vertical SaaS innovation.

Consolidation and Platform Wars

The SaaS market will see continued consolidation as larger players acquire smaller companies to expand their capabilities and customer bases. Platform companies like Salesforce, Microsoft, and ServiceNow will compete to become the central operating system for business, integrating an ever-wider range of capabilities.

At the same time, the long tail of specialized SaaS applications will persist, as businesses require best-of-breed solutions for specific use cases. The winners will be platforms that can integrate effectively with this ecosystem while providing compelling core capabilities.

Regulatory Evolution

Regulatory requirements around data privacy, AI ethics, and cybersecurity will continue to evolve. SaaS vendors will need to invest heavily in compliance capabilities, and compliance will become a key competitive differentiator. The vendors that can simplify compliance for their customers will capture significant market share.

The EU AI Act and similar regulations in other jurisdictions will create new compliance requirements for AI-powered SaaS. Vendors that proactively address these requirements will have an advantage over those that react to regulatory pressure.

Key Takeaways

- The SaaS market reached $465 billion in 2026 and is projected to grow to $1.37 trillion by 2035, representing one of the most significant technology transformations in business history.

- AI-native architecture is becoming the default, with AI adoption in enterprises jumping over 280% and AI-native SaaS companies raising at 40% higher valuations than traditional SaaS.

- Vertical SaaS is growing at double the rate of horizontal SaaS, with a 23.9% CAGR and $157.4 billion market size, driven by deep industry specialization.

- Security and compliance remain critical challenges, with 99% of organizations encountering SaaS or AI-driven security incidents and only 2% having holistic FinOps teams.

- Retention has become the primary growth driver, with top-quartile companies achieving 113% NRR while median CAC payback has increased to 18 months.

- The Asia Pacific region represents the fastest growth opportunity at 20% CAGR, significantly outpacing North America and Europe.

- Platform and ecosystem strategies are essential for competitive positioning, with MCP-native capabilities becoming a standard requirement.

Usage-based pricing is going mainstream, though it brings cost volatility challenges that require new approaches to FinOps and budgeting.

Sources and Citations

- Precedence Research — Software as a Service (SaaS) Market Size, Share, and Trends 2026 to 2035: https://www.precedenceresearch.com/software-as-a-service-market

- Mordor Intelligence — B2B SaaS Market Size, Share Analysis, Growth Report 2026-2031: https://www.mordorintelligence.com/industry-reports/b2b-saas-market

- Grand View Research — Software as a Service Market Size, Industry Report, 2030: https://www.grandviewresearch.com/industry-analysis/saas-market-report

- Fortune Business Insights — Software as a Service (SaaS) Market Size, Global Report, 2034: https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222

- SellersCommerce — 31 Eye-Opening SaaS Statistics In 2026: https://www.sellerscommerce.com/blog/saas-statistics

- Zylo — 175+ Unmissable SaaS Statistics for 2026: https://zylo.com/blog/saas-statistics

- Digital Applied — SaaS Marketing Statistics 2026: 150+ Data and Trends: https://www.digitalapplied.com/blog/saas-marketing-statistics-2026-data-points-trends

- Phoenix Strategy Group — Benchmarking SaaS KPIs: Industry Standards 2026: https://www.phoenixstrategy.group/blog/benchmarking-saas-kpis-industry-standards-2026

- Cyclr — 7 SaaS Predictions for 2026: The Year AI-Native Platforms Go Mainstream: https://cyclr.com/resources/ai/7-saas-predictions-for-2026

- Tridens — Top 6 SaaS Industry Trends for 2026: https://tridenstechnology.com/saas-trends

- TechnologyChecker.io — Salesforce Statistics: Trends, Insights and Salesforce Market Share 2026: https://technologychecker.io/blog/salesforce-statistics

- TripleDart — SaaS Growth Playbooks and Case Studies for 2026: https://www.tripledart.com/case-studies

- Big Moves Marketing — B2B SaaS Growth in 2026: 5 Lessons for B2B Startups: https://www.bigmoves.marketing/blog/b2b-saas-growth-in-2026

Regional Market Analysis

Understanding the regional dynamics of the SaaS market is essential for companies looking to expand their global footprint. Each region presents unique opportunities and challenges that shape go-to-market strategies and product development priorities.

North America: The Mature Market Leader

North America continues to dominate the global SaaS market, accounting for 56.9% of global revenue. The United States alone represents the largest single market, driven by high enterprise technology spending, mature cloud infrastructure, and a culture of early technology adoption. Silicon Valley remains the epicenter of SaaS innovation, with major players like Salesforce, Microsoft, and Google setting the pace for industry development.

However, the North American market is increasingly saturated, with high competition and mature customers demanding sophisticated solutions. Growth in this region increasingly comes from expansion revenue and upselling existing customers rather than new customer acquisition. SaaS companies targeting North America must focus on differentiation, customer success, and product innovation to succeed.

Europe: Compliance-Driven Growth

Europe represents the second-largest SaaS market, with particular strength in the UK, Germany, and France. The General Data Protection Regulation (GDPR) has paradoxically accelerated SaaS adoption, as companies seek compliant, managed solutions rather than building and maintaining their own infrastructure. European customers tend to be more conservative in their technology adoption but demonstrate high loyalty once they select a vendor.

The European market requires careful attention to localization, data residency requirements, and privacy regulations. SaaS companies must invest in EU-based data centers, local language support, and compliance certifications to compete effectively. The upcoming EU AI Act will create additional requirements for AI-powered SaaS applications.

Asia Pacific: The Growth Engine

The Asia Pacific region is the fastest-growing SaaS market, expected to grow at approximately 20% CAGR through 2030. China and India represent massive opportunities, though each presents unique challenges. China’s domestic technology ecosystem favors local players, while India shows strong appetite for international SaaS solutions, particularly in the IT services and outsourcing sectors.

Southeast Asian markets including Singapore, Indonesia, Thailand, and Vietnam are experiencing rapid digital transformation and represent attractive opportunities for SaaS expansion. These markets often leapfrog traditional technology adoption patterns, moving directly to cloud-based solutions without the legacy infrastructure that constrains Western markets.

Latin America and Middle East/Africa: Emerging Opportunities

Latin America and the Middle East/Africa regions represent smaller but rapidly growing SaaS markets. Brazil and Mexico lead Latin American adoption, while the UAE and South Africa anchor Middle East/Africa growth. These markets benefit from improving internet infrastructure, growing mobile penetration, and increasing technology investment by both enterprises and governments.

SaaS companies entering these markets must navigate currency volatility, payment infrastructure challenges, and varying levels of technology maturity. However, first-mover advantages can be significant, and local competitors often lack the resources to compete with well-funded international players.

The Evolution of SaaS Business Models

The SaaS business model has evolved significantly since the early days of simple subscription pricing. Today’s successful SaaS companies employ sophisticated monetization strategies that align vendor success with customer outcomes.

From Per-Seat to Usage-Based Pricing

The traditional per-seat subscription model, while still common, is increasingly supplemented or replaced by usage-based pricing. This shift reflects the reality that value delivered often correlates more closely with consumption than with the number of users. Infrastructure SaaS companies like AWS and Snowflake pioneered this approach, and it has spread to application software as well.

Usage-based pricing creates natural expansion revenue as customers grow, reduces friction for initial adoption, and aligns incentives between vendor and customer. However, it also introduces revenue volatility and requires sophisticated metering and billing infrastructure. Companies adopting usage-based pricing must invest in customer education and cost management tools to help customers predict and control their spending.

Outcome-Based and Risk-Sharing Models

The most sophisticated SaaS companies are moving toward outcome-based pricing, where fees are tied to measurable business results. This approach requires deep understanding of customer workflows and careful attribution of outcomes to the SaaS solution. While complex to implement, outcome-based pricing can create powerful competitive differentiation and customer loyalty.

Risk-sharing models take this concept further, with vendors guaranteeing specific results or refunding fees if outcomes are not achieved. These models demonstrate confidence in the product and create strong alignment between vendor and customer interests. They are particularly common in marketing technology, sales automation, and financial services SaaS.

Freemium and Product-Led Growth

Freemium models remain popular for customer acquisition, allowing prospects to experience product value before committing to paid plans. However, the bar for free plans has risen as customers expect more functionality before upgrading. Successful freemium strategies require careful balancing of free and paid features to drive conversion while delivering genuine value to free users.

Product-led growth (PLG) has emerged as a dominant go-to-market strategy, particularly for horizontal SaaS targeting SMBs and mid-market customers. PLG relies on the product itself to drive acquisition, activation, and expansion, reducing reliance on traditional sales and marketing. Companies like Slack, Zoom, and Notion have demonstrated the power of this approach, though it requires significant investment in user experience and self-service capabilities.

Conclusion

The SaaS market in 2026 represents a mature yet rapidly evolving industry. With a market size of $465 billion and projections pointing toward $1.37 trillion by 2035, the sector continues to offer substantial opportunities for both established players and new entrants. The shift toward AI-native architectures, vertical specialization, and usage-based pricing is reshaping competitive dynamics and creating new categories of winners and losers.

Success in this market requires more than just building good software. Companies must master AI integration, navigate complex security and compliance requirements, and develop sophisticated monetization strategies that align with customer success. The bar for entry has risen, but the rewards for those who can clear it have never been higher.

For SaaS buyers, the abundance of options creates both opportunity and complexity. Organizations must develop disciplined approaches to SaaS management, including governance frameworks, cost optimization practices, and integration strategies. The companies that can simplify this complexity for their customers will capture significant value in the coming years.

As we look toward 2030, one thing is clear: SaaS is no longer just a delivery model for software. It has become the dominant paradigm for how businesses consume technology, and its influence will only continue to grow. The question is not whether SaaS will continue to expand, but which companies will capture the value created by this transformation.