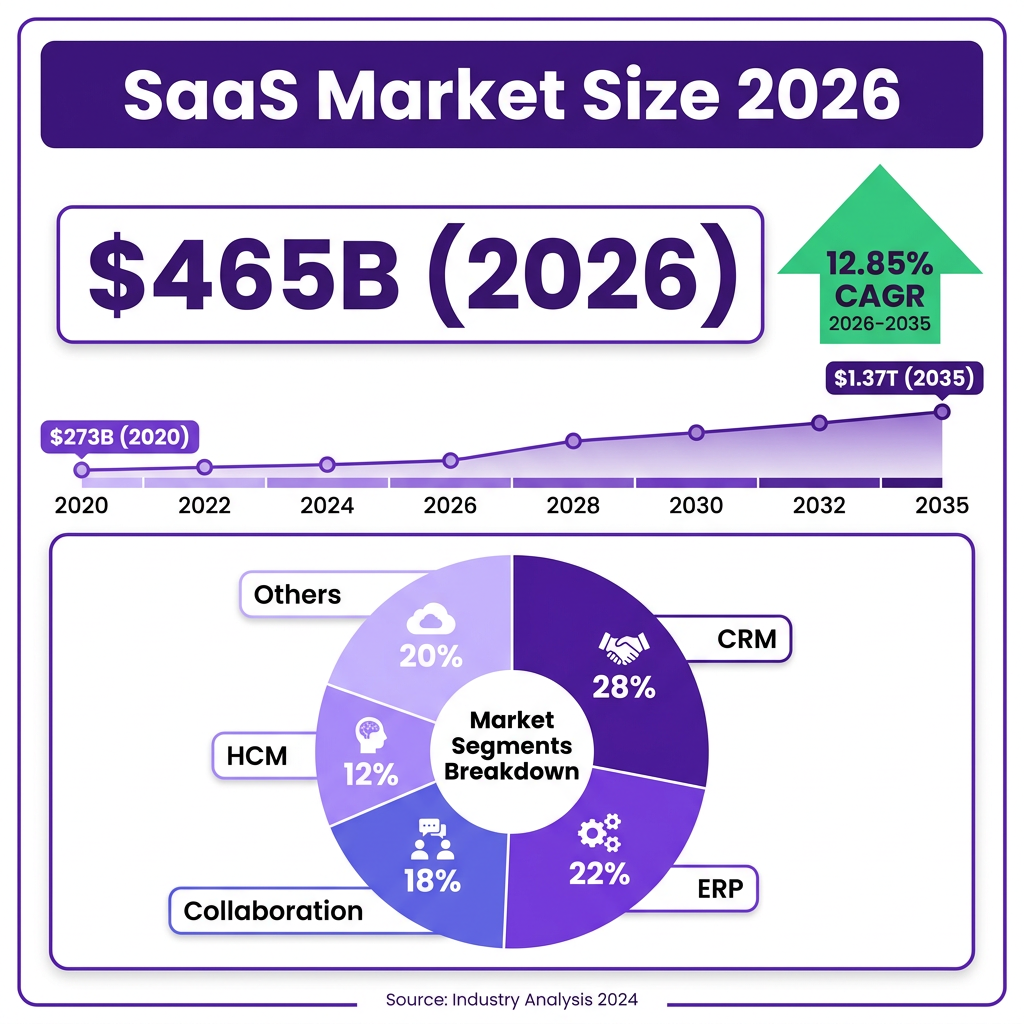

The global Software as a Service (SaaS) market has reached a pivotal inflection point in 2026. With a market valuation of $465.03 billion and projections indicating growth to $1.37 trillion by 2035, SaaS has evolved from a convenient alternative to on-premise software into the dominant model for enterprise software delivery. This represents a compound annual growth rate (CAGR) of 12.85% over the forecast period—a trajectory that underscores the fundamental shift in how businesses acquire, deploy, and consume software.

What makes this moment particularly significant is not just the scale of the market, but the nature of its transformation. Artificial intelligence has moved from experimental feature to strategic foundation. Product-led growth has evolved from startup tactic to enterprise imperative. And the very definition of SaaS is expanding to include AI-native applications that achieve $100 million in annual recurring revenue within their first two years of operation—growth trajectories that would have been unimaginable just five years ago.

Market Overview: The $465 Billion Ecosystem

The SaaS market’s current valuation of $465.03 billion in 2026 represents a significant acceleration from previous years. According to Precedence Research, the market stood at $408.21 billion in 2025, meaning the industry added nearly $57 billion in value in a single year. This growth is not an anomaly—it is the continuation of a decade-long trend that has seen SaaS transform from a niche delivery model to the default architecture for business software.

The historical trajectory reveals the scale of this transformation. In 2020, the global SaaS market was valued at approximately $273 billion. By 2024, it had grown to $399.10 billion according to Grand View Research. The COVID-19 pandemic served as an unexpected catalyst, accelerating digital transformation initiatives by an estimated five to seven years and establishing remote work infrastructure that permanently shifted software consumption patterns toward cloud-based solutions.

Looking ahead, the growth projections vary by research firm but consistently point to massive expansion. Fortune Business Insights projects the market reaching $1.48 trillion by 2034, representing a CAGR of 18.7%. Mordor Intelligence offers an even more aggressive forecast, predicting the B2B SaaS market alone will grow from $492.34 billion in 2026 to $1.58 trillion by 2031 at a 26.24% CAGR. Market Data Forecast projects $1.79 trillion by 2034 at a 21% CAGR. These variations reflect different methodological approaches and market definitions, but the consensus is clear: SaaS is entering its most expansive phase yet.

The geographic distribution of this growth reveals important strategic insights. North America currently dominates with approximately 45% market share, driven by the concentration of major SaaS vendors and early enterprise adoption. However, Asia-Pacific is emerging as the fastest-growing region with a projected 20% CAGR, expected to reach $176.2 billion by 2030. This regional shift represents both a challenge and opportunity for SaaS companies accustomed to North American-centric growth strategies.

Enterprise adoption has reached saturation levels that would have seemed impossible a decade ago. According to Zylo’s 2026 SaaS Management Index, 99% of organizations now use SaaS applications. The average company deploys 106 SaaS applications—down from a peak of 130 in 2022, reflecting consolidation and rationalization rather than reduced dependence. Large enterprises (1,000+ employees) average 231 applications, while smaller companies (under 100 employees) use approximately 44. This application density has created both opportunities for integration platforms and challenges for IT governance.

Key Statistics and Data Points

The SaaS industry’s scale is best understood through the lens of specific, quantified metrics that reveal both its current state and trajectory. These statistics paint a picture of an industry that has matured beyond its startup origins while retaining the growth characteristics of an emerging market.

Market Size and Growth: The global SaaS market reached $465.03 billion in 2026, up from $408.21 billion in 2025. The B2B SaaS segment specifically is valued at $492.34 billion according to Mordor Intelligence. The market is projected to grow to between $1.37 trillion and $1.79 trillion by 2034-2035, depending on the research source. The number of SaaS companies globally has grown to over 33,200 as of 2026, representing a 32% increase from 25,000 in 2021.

Enterprise Adoption Metrics: 99% of organizations now use at least one SaaS application. The average company uses 106 SaaS applications (down from 130 in 2022). Large enterprises average 231 applications, while mid-market companies use approximately 137. Small businesses (under 100 employees) average 44 applications. Over 50% of SaaS software used in companies is not managed by the IT team—what’s known as “shadow IT.”

Revenue and Growth Benchmarks: Median private SaaS revenue growth has declined from 35% YoY in 2022 to 25% in 2024, reflecting market maturation. Bootstrapped companies with $3M-$20M ARR show median growth of 15%, while equity-backed companies average 30%. The 90th percentile of bootstrapped companies achieves 42.3% annual growth. AI-native SaaS companies are achieving $3M ARR within their first year and $100M ARR by year four—significantly outpacing traditional SaaS benchmarks. A subset of high-performing AI-native companies reaches $40M ARR in year one and exceeds $120M by year two.

Retention and Churn Metrics: Median Net Revenue Retention (NRR) for bootstrapped SaaS companies is 103%, with top performers (90th percentile) achieving 117.9%. Gross Revenue Retention (GRR) median is 91%. Good monthly churn rates are below 1% (under 5% annually). Reducing churn by 5% can increase profit by 125% according to industry research. Median blended CAC payback for $5M-$25M ARR SaaS is 18 months, up from 15 months in 2023.

Product-Led Growth Metrics: Median free-to-paid conversion across all PLG models is 9%. Freemium products convert at 12% median, while opt-in free trials convert at 18.2%. Opt-out trials (requiring credit card) achieve 48.8% conversion. Expansion revenue accounts for approximately 40% of new ARR in high-performing SaaS companies.

Cost and Pricing Trends: 82% of executives report significant increases in cloud, SaaS, and Gen AI costs. 78% of IT leaders report unexpected costs from usage-based or AI pricing models. Only 2% of organizations have FinOps teams covering cloud, SaaS, and Gen AI holistically. Consumption-based pricing is becoming more common across the industry. Average license utilization sits at approximately 49%, indicating significant waste in SaaS spending.

Market Share and Competitive Landscape: Salesforce holds 20.7% of the global CRM market, generating $21.6 billion in CRM revenue—more than Microsoft, Oracle, Adobe, and SAP combined. Salesforce’s total FY2026 revenue reached $41.5 billion. Software subscriptions represent 83.6% of SaaS market revenue. Hybrid cloud deployments account for 20.9% of the market and are growing at 20.1% CAGR.

AI and Technology Integration: AI/ML deal share in venture capital reached 65.6% in Q4 2025. AI-native SaaS raises at 40% higher valuations than traditional SaaS. Median Series B valuations for AI-powered SaaS hit $175 million in Q3 2025—a 38% YoY increase. AI captured 61% of global VC deal value in 2025. 31.4% of Salesforce deployments belong to companies with 10 or fewer employees, demonstrating SMB adoption of enterprise-grade tools.

Major Trends Shaping SaaS in 2026

The SaaS landscape of 2026 is being fundamentally reshaped by seven major trends that are redefining how software is built, sold, and consumed. These trends represent both opportunities for growth and challenges that require strategic adaptation.

1. AI-Native SaaS: From Feature to Foundation

Artificial intelligence has transitioned from an experimental add-on to the core architecture of new SaaS products. AI-native SaaS companies—those built with AI as their foundational technology rather than a bolt-on feature—are achieving growth trajectories that dwarf traditional SaaS benchmarks. According to Bessemer Venture Partners, these companies reach approximately $3 million in ARR within their first year and scale to roughly $100 million by year four.

The most successful AI-native companies are achieving even more impressive results. A subset of high performers reaches approximately $40 million in ARR within the first year and exceeds $120 million by the second year. This represents a fundamental shift in what’s possible for software companies and has attracted significant venture capital attention—AI/ML deal share reached 65.6% in Q4 2025, and AI captured 61% of global VC deal value.

However, this trend comes with challenges. Budgets are increasingly prioritizing AI readiness, reliability, and integration over feature-level demos. Organizations are demanding production-ready AI—systems that are observable, governable, cost-controlled, and able to operate continuously under real user load. The companies succeeding in this environment are those that have moved beyond experimentation to strategic implementation.

2. Vertical SaaS: Industry-Specific Solutions

Horizontal SaaS—applications designed to serve multiple industries—faced a reckoning in recent years as customers demanded deeper, industry-specific functionality. Vertical SaaS, which targets specific industries with tailored solutions, has emerged as the dominant growth strategy. Companies building vertical solutions for healthcare, legal, financial services, and other specialized sectors are raising larger early-stage rounds and achieving higher valuations.

According to VC mapping data, vertical AI SaaS companies for healthcare, legal, and financial services raised the largest early-stage rounds, with median Series A sizes of $22 million versus $15 million for traditional horizontal SaaS. This premium reflects both the higher barriers to entry in specialized domains and the greater customer willingness to pay for solutions that understand their specific workflows and compliance requirements.

3. Product-Led Growth Evolution

Product-led growth (PLG) has evolved from a startup tactic to a full-stack go-to-market engine. The success of companies like Cursor—the AI code editor that crossed $500 million ARR by mid-2025 and hit $2 billion ARR by February 2026—has demonstrated that PLG can scale to the highest revenue levels. Cursor became the fastest SaaS company to reach these milestones, reigniting industry interest in self-serve models.

However, the nature of PLG is changing. Free trials and freemium tiers still matter, but leading companies are layering sales-assisted motions, AI-driven onboarding, and usage-based expansion on top of their self-serve foundations. The result is a hybrid approach that combines the efficiency of product-led acquisition with the revenue acceleration of sales-led expansion.

Conversion benchmarks reveal the complexity of this landscape. Median free-to-paid conversion sits at 9% across all PLG models, with freemium products converting at 12% and opt-in free trials at 18.2%. Opt-out trials requiring credit card information achieve 48.8% conversion but at the cost of reduced top-of-funnel volume. The optimal model depends on target customer segment, price point, and competitive positioning.

4. Usage-Based Pricing and Cost Volatility

Consumption-based pricing models are becoming more common across the SaaS industry, driven by customer demand for cost alignment with value and vendor interest in capturing upside from customer growth. However, this shift has introduced cost volatility that many organizations are unprepared to manage. According to Zylo’s research, 78% of IT leaders report unexpected costs from usage-based or AI pricing models.

This cost volatility has replaced predictable growth as a defining challenge for SaaS management. 82% of executives report significant increases in cloud, SaaS, and Gen AI costs. Yet only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically, with most teams remaining narrowly operational rather than strategic. This gap represents both a risk for customers and an opportunity for vendors who can provide cost predictability and management tools.

5. Workflow Orchestration Becomes Mandatory

Reliable AI at scale requires control planes and execution layers, not isolated features. Workflow orchestration—the ability to coordinate multiple AI agents, automate complex business processes, and ensure reliable execution—has become a mandatory capability for enterprise SaaS. Companies are discovering that AI features without orchestration create more problems than they solve, leading to inconsistent outputs, compliance risks, and user frustration.

This trend is driving investment in integration platforms, workflow automation tools, and AI orchestration frameworks. Organizations are moving from experimenting with individual AI features to implementing comprehensive automation strategies that span multiple applications and data sources. The winners in this environment will be platforms that can serve as the orchestration layer for the broader SaaS ecosystem.

6. Agentic AI: The Interface Disappears

Perhaps the most profound shift on the horizon is the rise of agentic AI—AI agents that use SaaS tools rather than human end users. As Wes Bush, who coined the term “Product Led Growth,” notes: “PLG is not dead, and won’t be—but it’s evolving quickly. PLG 1.0 = user-led. What’s interesting is companies like Netlify are already at 3.0 with 80% of their signups being agents, while the majority of traditional SaaS is still in 1.0.”

In this emerging paradigm, AI agents evaluate software by the outcomes produced and ease of agentic use rather than human interface design. When your product doesn’t need a traditional interface, the entire paradigm of user experience shifts. This doesn’t eliminate the importance of product—it transforms it. Product value will be measured by API reliability, integration depth, and the quality of outcomes delivered to agent users.

7. Hybrid Cloud and Multi-Cloud Strategies

Organizations are increasingly adopting multi-cloud strategies, utilizing different cloud providers for various applications and services. Hybrid cloud deployments—combining public cloud, private cloud, and on-premise infrastructure—now represent 20.9% of the SaaS market and are growing at 20.1% CAGR, faster than the overall market.

This trend reflects both risk management concerns (avoiding vendor lock-in) and regulatory requirements (data residency and sovereignty). SaaS vendors that can operate seamlessly across cloud environments, or that offer deployment flexibility, are gaining competitive advantage. The ability to deploy in customer VPCs, on-premise, or across multiple clouds is becoming a standard enterprise requirement rather than a premium feature.

Key Players and Competitive Landscape

The SaaS competitive landscape is characterized by a mix of established giants, emerging challengers, and AI-native upstarts that are rewriting the rules of the industry. Understanding this landscape is essential for strategic positioning and competitive analysis.

Market Leaders

Salesforce remains the dominant force in CRM and a bellwether for the broader SaaS industry. With $41.5 billion in FY2026 revenue and 20.7% of the global CRM market, Salesforce generates more CRM revenue than Microsoft, Oracle, Adobe, and SAP combined. The company’s $21.6 billion in CRM revenue alone demonstrates the scale of its market position. Notably, 31.4% of Salesforce deployments belong to companies with 10 or fewer employees, showing successful penetration into the SMB market.

Microsoft continues to leverage its Office 365 and Azure ecosystems to drive SaaS adoption. The company’s comprehensive suite of productivity, collaboration, and infrastructure services creates a sticky platform that competitors struggle to displace. Microsoft’s AI integration through Copilot represents a significant competitive moat and pricing power opportunity.

Adobe has successfully transitioned from perpetual license to subscription model, demonstrating that even mature software categories can be reinvented through SaaS delivery. The company’s Creative Cloud and Experience Cloud businesses continue to grow, supported by AI features that enhance rather than replace creative workflows.

ServiceNow has established itself as the platform of choice for enterprise workflow automation, expanding from IT service management into HR, customer service, and custom application development. The company’s platform strategy creates significant switching costs and expansion revenue opportunities.

Emerging Challengers

Cursor (Anysphere) represents the new generation of AI-native SaaS companies. The AI code editor crossed $500 million ARR by mid-2025 and reached $2 billion ARR by February 2026—making it the fastest SaaS company to achieve these milestones. Cursor’s success demonstrates the growth potential of AI-native applications that deliver immediate, tangible value.

Notion has redefined the productivity and collaboration category through its flexible, block-based approach that combines notes, databases, wikis, and project management. The company’s product-led growth strategy and vibrant template ecosystem have created a passionate user base and significant expansion revenue.

Figma (now part of Adobe) demonstrated that design tools could be successfully delivered as SaaS, with real-time collaboration as a core differentiator. The company’s acquisition by Adobe for $20 billion validated the market opportunity for design SaaS while raising questions about competitive dynamics in the space.

Vertical SaaS Leaders

Vertical SaaS companies are achieving significant scale in specific industries. In healthcare, companies like Veeva Systems have built dominant positions by addressing industry-specific compliance and workflow requirements. In financial services, Plaid and Stripe have become infrastructure layers for fintech innovation. In real estate, companies like CoStar and Zillow have transformed how properties are marketed and transacted.

The common thread among successful vertical SaaS companies is deep industry expertise combined with modern technology architecture. These companies win not by being the best software company, but by being the best solution for their specific industry’s problems.

Market Segmentation by Application

The SaaS market can be segmented by application type, with each category showing distinct growth dynamics:

Customer Relationship Management (CRM): The largest application segment, representing approximately 28% of the SaaS market. Salesforce dominates, but Microsoft Dynamics, HubSpot, and Zoho maintain significant positions. AI-powered sales engagement and revenue intelligence are driving the next wave of innovation.

Enterprise Resource Planning (ERP): Approximately 22% of the market. Traditional vendors like SAP and Oracle are transitioning to cloud delivery while facing competition from native cloud ERP providers like NetSuite (Oracle), Workday, and emerging players.

Content, Collaboration & Communication: Approximately 18% of the market. This segment includes productivity suites (Microsoft 365, Google Workspace), communication tools (Slack, Teams), and project management platforms (Asana, Monday.com, ClickUp).

Human Capital Management (HCM): Approximately 12% of the market. Workday, SAP SuccessFactors, and Oracle HCM Cloud lead in enterprise, while companies like Gusto, BambooHR, and Rippling serve the SMB and mid-market segments.

BI & Analytics: A rapidly growing segment driven by demand for data-driven decision making. Tableau (Salesforce), Power BI (Microsoft), Looker (Google), and emerging AI-native analytics platforms compete in this space.

Challenges and Pain Points

Despite the industry’s growth and innovation, SaaS companies and their customers face significant challenges that require strategic attention. Understanding these pain points is essential for both vendors seeking competitive advantage and buyers making procurement decisions.

1. Retention and Churn

User retention has become the defining factor between SaaS products that scale and those that stall. As competition intensifies and switching costs decrease, customers are more willing than ever to abandon products that don’t deliver immediate, sustained value. Most SaaS products don’t fail because of bad ideas—they fail because users don’t stick around.

The economics of churn are brutal. A SaaS company with 5% monthly churn must replace its entire customer base every 20 months just to maintain flat revenue. Reducing churn by 5% can increase profit by 125% according to industry research. Yet many companies focus disproportionately on acquisition rather than retention, masking churn problems with growth that is ultimately unsustainable.

Modern churn reduction requires a signal density approach—collecting and analyzing the leading indicators that predict churn before it happens. These indicators include relationship health, sentiment, and strategic alignment—none of which show up in traditional product analytics. NPS and satisfaction surveys generate response rates of only 5-15% and rarely capture the “why” behind customer dissatisfaction.

2. Cost Management and Shadow IT

The proliferation of SaaS applications has created significant cost management challenges. 82% of executives report significant increases in cloud, SaaS, and Gen AI costs. 78% of IT leaders experience unexpected costs from usage-based pricing. Average license utilization sits at approximately 49%, meaning companies are paying for twice the capacity they actually use.

Compounding this problem is shadow IT—the use of SaaS applications without IT department knowledge or approval. Over 50% of SaaS software used in companies is not managed by the IT team. This creates security risks, compliance gaps, and redundant spending as different departments purchase overlapping tools.

Only 2% of organizations have FinOps teams that cover cloud, SaaS, and Gen AI holistically. Most teams are narrowly operational rather than strategic, focused on bill payment rather than cost optimization. This gap represents a significant opportunity for SaaS management platforms and a risk for organizations that fail to establish governance.

3. AI Integration and Technical Debt

The pressure to integrate AI capabilities has created a new form of technical debt. Many SaaS companies have bolted AI features onto legacy architectures without the data infrastructure, observability, or governance frameworks required for production reliability. The result is AI features that work well in demos but fail under real user load.

Production-ready AI requires observable, governable, cost-controlled systems that can operate continuously. This demands investment in data platforms, integration layers, and ownership models that many organizations have neglected in their rush to market with AI capabilities. The companies that will win in this environment are those that invested in AI readiness before it became a competitive requirement.

4. Growth Rate Compression

Median private SaaS revenue growth has declined from 35% YoY in 2022 to 25% in 2024. This compression reflects market maturation, increased competition, and macroeconomic headwinds that have made buyers more conservative. The “growth at all costs” era has ended, replaced by a focus on efficient growth and capital discipline.

For SaaS companies, this shift requires fundamental changes in go-to-market strategy. The playbook that worked in 2020-2021—aggressive paid acquisition, generous free tiers, and rapid hiring—no longer delivers results. Companies must now optimize for unit economics, with CAC payback periods, LTV:CAC ratios, and net revenue retention as primary metrics.

5. Customer Acquisition Cost Inflation

Median blended CAC payback for $5M-$25M ARR SaaS has increased to 18 months, up from 15 months in 2023. This inflation reflects increased competition for attention, higher advertising costs, and more sophisticated buyers who conduct extensive research before engaging with sales teams.

The most fixable lever for many teams isn’t pricing or product—it’s the data quality feeding their pipeline. Poor targeting, weak messaging, and inefficient funnel design drive CAC higher even when product-market fit is strong. Companies that invest in data infrastructure, ideal customer profile definition, and funnel optimization can achieve significant competitive advantage.

Opportunities and Growth Strategies

Despite the challenges, the SaaS market offers significant opportunities for companies that can execute effectively. These opportunities span product strategy, go-to-market approaches, and operational excellence.

1. AI-Native Product Development

The most significant opportunity in SaaS is building AI-native products from the ground up rather than retrofitting AI onto existing architectures. AI-native companies are achieving growth rates that were previously unimaginable—$100M ARR in two years, $40M ARR in year one. These companies treat AI not as a feature but as the fundamental building block of their product.

The key to success is identifying workflows where AI can deliver 10x improvements in speed, quality, or cost. Cursor succeeded because it made developers significantly more productive. Similar opportunities exist across every industry and function—legal document review, medical diagnosis, financial analysis, creative production, and countless others.

2. Vertical SaaS Expansion

Vertical SaaS companies raise larger early-stage rounds and achieve higher valuations than horizontal competitors because they solve specific, high-value problems for defined customer segments. The median Series A for vertical AI SaaS is $22 million versus $15 million for traditional SaaS.

The opportunity lies in identifying industries that are underserved by horizontal solutions and building deep, compliant, integrated products that address their specific needs. Healthcare, legal, financial services, real estate, construction, agriculture, and logistics all present significant vertical SaaS opportunities.

3. Product-Led Growth Optimization

PLG remains the most efficient way to build a software business, but it requires sophisticated execution. The opportunity lies in moving beyond basic free trials to comprehensive product-led strategies that encompass acquisition, activation, expansion, and retention.

Key optimization opportunities include: improving time-to-value through better onboarding, implementing usage-based triggers for expansion revenue, creating viral loops through collaboration features, and layering sales-assisted motions on top of self-serve foundations. Companies that master these tactics can achieve the efficiency of PLG with the revenue acceleration of traditional sales.

4. International Expansion

Asia-Pacific is the fastest-growing SaaS region with a projected 20% CAGR, expected to reach $176.2 billion by 2030. This growth represents a significant opportunity for SaaS companies that can adapt their products, pricing, and go-to-market strategies for regional markets.

Success in international markets requires more than translation. Companies must address local compliance requirements (GDPR in Europe, data residency in China and Russia), adapt to local business practices, and build partnerships with regional system integrators and resellers. The companies that invest in true internationalization will capture disproportionate growth.

5. Platform and Ecosystem Strategies

The most valuable SaaS companies are those that become platforms—ecosystems around which other applications and integrations cluster. Salesforce’s AppExchange, Slack’s app directory, and Shopify’s app store demonstrate the power of platform strategies to create competitive moats and capture value from ecosystem activity.

The opportunity for emerging SaaS companies is to identify integration points where they can become the orchestration layer for broader workflows. Rather than building every feature, platform companies enable third-party developers to extend their capabilities while capturing a portion of the value created.

Case Studies and Success Stories

The theoretical frameworks of SaaS growth are best understood through the lens of specific companies that have achieved exceptional results. These case studies illustrate the strategies, tactics, and market conditions that drive outsized success.

Case Study 1: Cursor—The Fastest-Growing SaaS Company in History

Cursor, the AI code editor built by Anysphere, has redefined what’s possible for SaaS growth. The company crossed $500 million in ARR by mid-2025 and reached $2 billion ARR by February 2026—making it the fastest SaaS company to achieve these milestones in history.

Cursor’s success is attributable to several factors. First, the product delivers immediate, tangible value—developers using Cursor report 2-3x productivity improvements in coding tasks. Second, the company employed a viral freemium strategy: any user could create a basic agent for free, but sharing it with 3+ team members unlocked collaborative features. This created organic growth loops that drove adoption without proportional marketing spend.

Third, Cursor rode the wave of AI enthusiasm while delivering genuine utility. Unlike many AI products that generated hype without substance, Cursor’s AI capabilities were production-ready from launch, with reliable code generation, explanation, and refactoring. This positioned the company to capture the surge in developer interest in AI-assisted coding tools.

The lesson for other SaaS companies is clear: identify a workflow where AI can deliver 10x improvement, build a product that works reliably from day one, and create viral loops that turn users into advocates. Cursor didn’t just build an AI feature—they built an AI-native product that redefined a category.

Case Study 2: NeuroFlow AI—From $500K to $100M ARR in 18 Months

NeuroFlow AI demonstrates the growth potential of AI-native SaaS in specialized domains. The company turned $500K in seed funding into $100M ARR in just 18 months by making AI agents the core product rather than a feature.

NeuroFlow’s strategy focused on solving a specific, high-value problem: automating complex business workflows that previously required human judgment. By building AI agents that could understand context, make decisions, and execute actions, NeuroFlow delivered value that traditional automation tools couldn’t match.

The company’s product-led growth engine kicked in when they launched a viral freemium tier. Users could create basic agents for free, but collaborative features required team adoption. This created natural expansion revenue as successful use cases spread within organizations.

NeuroFlow’s success illustrates the power of AI-native architecture combined with product-led distribution. The company didn’t spend heavily on sales and marketing—it built a product so compelling that it sold itself, with AI capabilities that improved with each user interaction.

Case Study 3: EcoTrack Analytics—Bootstrapped Growth to $20M ARR

Not all SaaS success requires venture capital. EcoTrack Analytics, a sustainability-focused analytics platform, reached $20M ARR without raising external funding by weaponizing community-driven customer acquisition.

EcoTrack’s strategy centered on building a passionate community of sustainability professionals who became advocates for the platform. The company invested heavily in educational content, industry events, and user forums that established it as a thought leader in sustainability analytics.

This community-driven approach generated high-quality leads at a fraction of the cost of traditional paid acquisition. More importantly, it created network effects—users who joined because of community recommendations were more likely to become advocates themselves, creating a self-reinforcing growth loop.

EcoTrack’s success demonstrates that bootstrapped SaaS growth is still possible in 2026, but it requires a different playbook than venture-backed competitors. Rather than buying growth through paid acquisition, bootstrapped companies must earn it through community building, content marketing, and product excellence.

Case Study 4: DirectIQ—Customer Education as Growth Strategy

DirectIQ, an email marketing platform, achieved significant growth through a strategic emphasis on educational content. The company invested heavily in “how-to” videos, tutorials, and best practice guides that helped customers succeed with email marketing—not just with DirectIQ’s product.

This educational approach served multiple objectives. First, it reduced support queries by helping customers self-serve solutions to common problems. Second, it improved customer success by teaching best practices that led to better campaign results. Third, it generated organic traffic through SEO, creating a sustainable acquisition channel.

The key insight from DirectIQ’s success is that customer education can be a competitive differentiator in crowded markets. When products are functionally similar, the company that helps customers achieve better outcomes wins. Educational content creates value before the sale, building trust and demonstrating expertise that converts to revenue.

Future Outlook and Predictions

The SaaS market’s trajectory through 2030 and beyond will be shaped by technological evolution, changing customer expectations, and macroeconomic factors. While precise predictions are impossible, several trends appear likely to define the next phase of industry development.

Market Size Projections

By 2030, the global SaaS market is projected to reach between $774 billion and $1.1 trillion, depending on the research source. By 2034-2035, estimates range from $1.37 trillion to $1.79 trillion. These projections assume continued cloud adoption, digital transformation, and the emergence of new application categories enabled by AI.

The US SaaS market specifically is valued at approximately $187 billion and is expected to maintain its position as the largest single market, though its share of global revenue will likely decline as Asia-Pacific and other regions grow faster.

Technology Evolution

AI will continue to transform SaaS, moving from current capabilities (generative text, code assistance, image generation) to more sophisticated applications (autonomous agents, complex reasoning, multi-modal understanding). By 2028, a significant portion of SaaS usage may be by AI agents rather than human users, fundamentally changing product design priorities.

Edge computing and 5G will enable new categories of SaaS applications that require low latency and high bandwidth. Real-time collaboration, AR/VR applications, and IoT orchestration will become viable at scale, opening new market opportunities.

Business Model Evolution

Usage-based pricing will become the dominant model for infrastructure and platform services, while seat-based pricing will persist for collaboration and productivity tools. Outcome-based pricing—where customers pay for results rather than usage—will emerge in categories where AI can reliably deliver measurable outcomes.

The distinction between SaaS and professional services will blur as AI-enabled platforms deliver outcomes that previously required human consultants. “SaaS with a service” models will become common, combining software automation with human expertise for complex implementations.

Competitive Dynamics

Consolidation will accelerate as larger platforms acquire specialized tools to fill portfolio gaps. The number of independent SaaS companies will decline, but the total number of applications will increase as platform ecosystems expand.

AI-native challengers will continue to disrupt established categories, achieving faster growth than incumbents but facing challenges in enterprise sales and trust-building. The most successful incumbents will be those that effectively integrate AI while leveraging their existing distribution and customer relationships.

Regulatory Environment

Data privacy regulations will continue to proliferate, creating compliance burdens but also competitive moats for companies that invest in privacy-preserving technologies. AI regulation will emerge as a significant factor, with requirements for transparency, bias testing, and human oversight affecting product development.

Antitrust scrutiny of major platforms will intensify, potentially creating opportunities for independent vendors. Data portability requirements will make it easier for customers to switch providers, increasing competitive pressure on incumbents.

Key Takeaways

- The SaaS market has reached $465.03 billion in 2026 and is projected to grow to $1.37-1.79 trillion by 2034-2035, representing one of the largest and fastest-growing segments of the technology industry.

- AI-native SaaS is rewriting growth benchmarks—companies built with AI as their foundation are achieving $100M ARR in 2-4 years, compared to 7-10 years for traditional SaaS.

- Product-led growth has evolved from a startup tactic to a full-stack go-to-market engine, with hybrid models combining self-serve acquisition and sales-assisted expansion showing the best results.

- Vertical SaaS commands premium valuations—industry-specific solutions raise larger rounds and achieve higher valuations than horizontal competitors due to deeper customer relationships and higher switching costs.

- Retention has become the defining competitive factor—with acquisition costs rising and switching costs falling, the ability to keep customers engaged and expanding is what separates scaling companies from those that stall.

- Cost volatility is the new normal—usage-based pricing and AI costs have introduced unpredictability that requires new management approaches, with only 2% of organizations having holistic FinOps capabilities.

- Asia-Pacific represents the fastest growth opportunity—with 20% projected CAGR through 2030, international expansion is essential for companies seeking to maintain growth rates.

- Agentic AI will transform product design—as AI agents become primary users of SaaS tools, product value will be measured by API reliability and integration depth rather than interface design.

Sources and Citations

- Precedence Research – Software As A Service (SaaS) Market Size, Share, and Trends 2026 to 2035: https://www.precedenceresearch.com/software-as-a-service-market

- Fortune Business Insights – Software as a Service [SaaS] Market Size, Global Report, 2034: https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222

- Mordor Intelligence – B2B SaaS Market Size, Share Analysis, Growth Report 2026 – 2031: https://www.mordorintelligence.com/industry-reports/b2b-saas-market

- Zylo – 175+ Unmissable SaaS Statistics for 2026: https://zylo.com/blog/saas-statistics

- SaaS Capital – 2026 Benchmarking Metrics for Bootstrapped SaaS Companies: https://www.saas-capital.com/blog-posts/benchmarking-metrics-for-bootstrapped-saas-companies

- Digital Applied – SaaS Marketing Statistics 2026: 150+ Data and Trends: https://www.digitalapplied.com/blog/saas-marketing-statistics-2026-data-points-trends

- TechnologyChecker – Salesforce Statistics: Trends, Insights and Market Share 2026: https://technologychecker.io/blog/salesforce-statistics-trends-insights-and-salesforce-market-share

- VC Mapping – 500+ SaaS Investors & VC Firms in 2026: https://vc-mapping.gilion.com/venture-capital-firms/saas-investors

- Innovecs – Top SaaS Trends in 2026: AI, Security & Growth Models: https://innovecs.com/blog/the-top-7-saas-trends

- SaaS Fourm – Case Studies: SaaS Success Stories from 2026: https://www.saasfourm.com/case-studies-saas-success-stories-from-lessons-from-explosive-growth

- SaaS Mag – PLG in 2026: Product-Led Growth Evolves Into Full-Stack GTM Engine: https://www.saasmag.com/product-led-growth-next-chapter-saas-2026

- Ken Research – US SaaS Market Outlook to 2030: https://www.kenresearch.com/industry-reports/us-saas-market-outlook-to-2028